Agricultural Robots Market Demand, Industry Analysis, 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

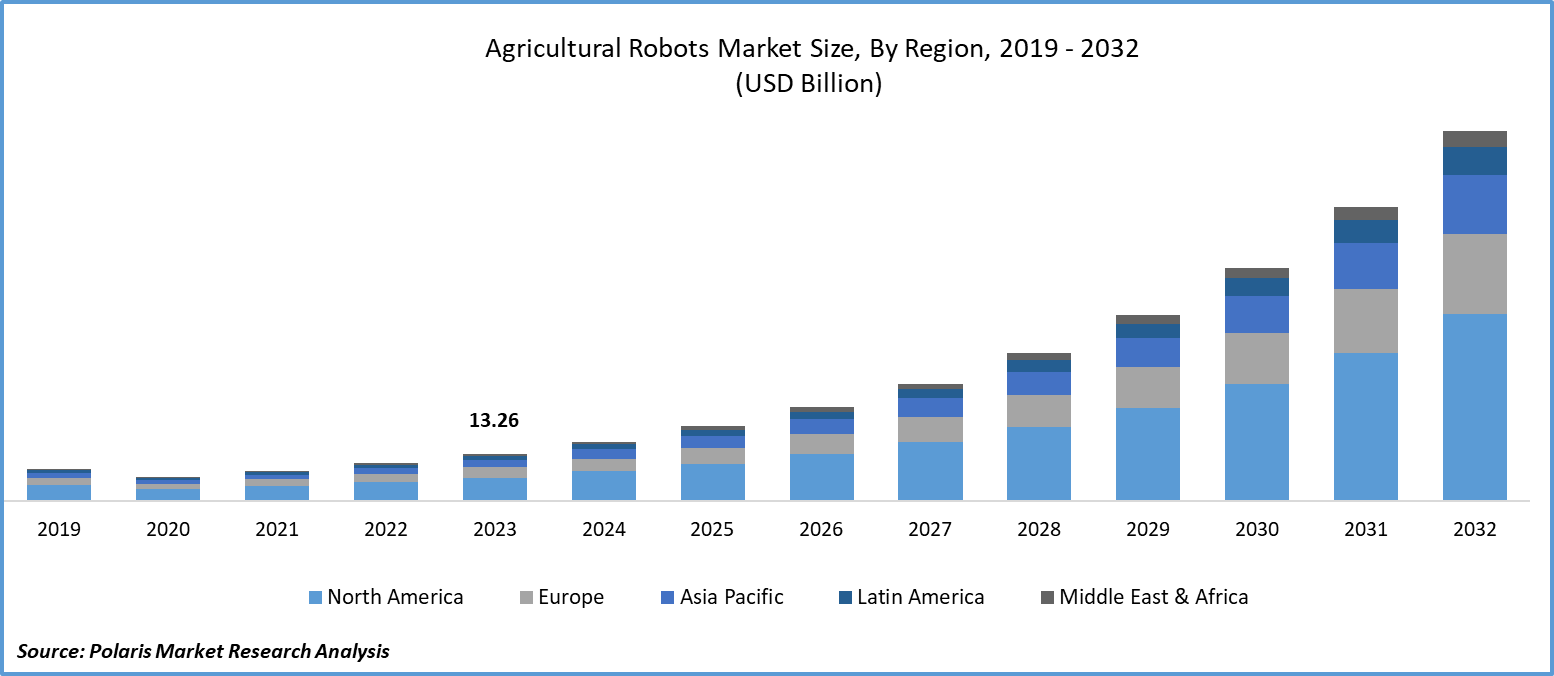

The global agricultural robots market size was valued at USD 18.52 billion in 2025 and is expected to grow at a CAGR of 26.1% from 2026 to 2034. Market growth is fueled by labor shortages in agriculture and the increasing adoption of precision farming technologies. Growing demand for higher farm productivity and better resource efficiency also boosts the growth. Further, data-driven crop management accelerates the shift toward agricultural robotics across open-field and controlled-environment farming systems.

Market Insights

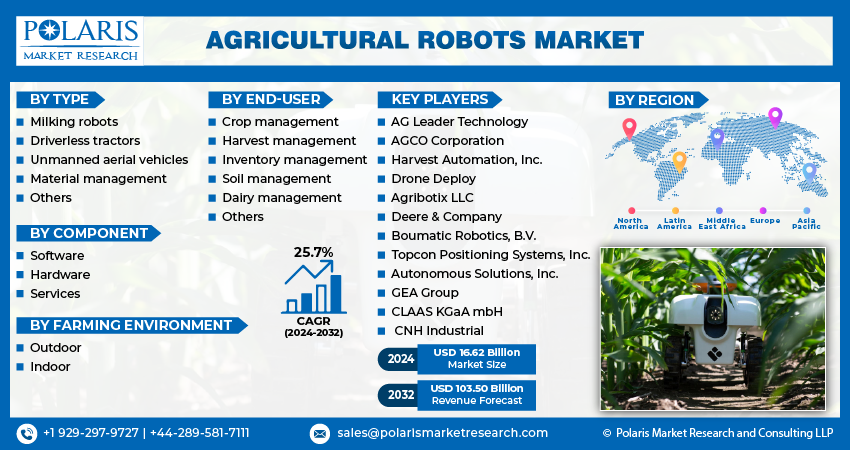

- Based on type, the milking robots segment held the largest share in 2025. The rising demand for more milk production and the emphasis on animal welfare drive the segment dominance.

- In terms of component, the hardware segment led the market share in 2025. Hardware is the foundation for robotic farming solutions, which boost the segment growth.

- By farming environment, the indoor segment is anticipated to witness highest growth rate. Indoor farming can be practiced at any indoor space with controlled indoor cultivation settings.

- By end user, the dairy management segment led the market. It is due to rising adoption of automated milking equipment such as milking robots.

- North America held the largest share of the global market in 2025. The dominance of the segment is largely attributed to the rising labor cost and shortage of skilled farmers.

- The Asia Pacific market is expected to grow fastest during the projected period. It is driven by the growing adoption of technological advancements for efficient agricultural methods.

Industry Dynamics

- Increasing adoption of automation in farming practices boosts the agricultural robots industry growth.

- Shortage of human labor for in agriculture contributes to thr rising requirement for agricultural robots.

- Rising technological developments in agricultural robots are expected to create lucrative opportunities in the market in the future.

- High cost on investment hinders the deployement of agricultural robots in small and medium-size farms.

Market Statistics

- Market Size in 2025: USD 18.52 billion

- Projected Market Size in 2034: USD 149.78 billion

- CAGR, 2026–2034: 26.1%

- Largest Regional Market, 2025: North America

AI Impact on Agricultural Robots Market

- Artificial intelligence facilitates precision farming through real-time analysis of soil, crop, and weather.

- The technology supports autonomous operations. It reduces labor dependency and human intervention.

- AI uses computer vision and predictive analytics to enhance crop monitoring.

- It helps with pest and weed control and reduces chemical use.

- AI-enabled devices lower crop wastage and boost harvesting accuracy.

- Smart farm management software that integrates AI and IoT assists farmers in making data-driven decisions.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Agricultural robots are increasingly being deployed for spraying, monitoring, seeding, harvesting, milking, and weed control. These use cases make them a practical choice for farms that seek higher yields, less input waste, and better operational continuity. The rising awareness for agricultural robots is due to the increasing adoption of environmentally conscious farming practices, and the need to solve the challenges posed by a climate change and labor shortage. The agricultural robotics industry is expected to grow as long as technology keeps developing. After implementation, these robots offer innovative ways to improve production and fulfil the agricultural industry's evolving needs.

The government and NGOs are making a conscious effort toward the adoption of agricultural robots. In March 2024, Garuda announced its support for drone manufacturing due to demand from fertilizer companies through India’s Drone Didi scheme. The initiative aims to increase the use of UAVs in agriculture. These policy-backed efforts are helping to widen access to agricultural drones, especially in emerging markets where improving labor efficiency, input precision, and crop monitoring are important priorities.

Farming is becoming easier with the deployment of large and small drone and robotic technologies. GPS navigation and vision systems for crop tillage and spraying, and other agricultural technologies increase precision in farming. Traditional high-mass tractors are now expected to be replaced in the future by fleets of tiny, light robots. Advances in machine vision, AI-based decision support, remote sensing, and autonomous navigation enable robots to perform repetitive farm tasks with greater consistency and lower chemical and fuel intensity.

Market Dynamics

Market Drivers

Rise in Agricultural Automation

The agricultural industry is experiencing growing demand for automation in tasks such as planting, harvesting, and monitoring. Agricultural robots offer effective solutions by reducing the need for human labor. These robots improve productivity, efficiency, and accuracy. This leads to better yields and lower production costs. More farmers are finding it appealing to use agricultural robots because they help with labor shortages and make better use of resources. This shift will support sustainable farming and drive growth in the agricultural robotics market.

In November 2023, Aigen raised USD 12 million to develop solar-powered autonomous robots for crop management without chemicals or fossil fuels using ML, AI, and battery technology. This trend shows a wider move toward automating precision agriculture. Robotics helps with more focused spraying, autonomous scouting, and real-time field monitoring. It reduces the need for manual work.

Shortage of Skilled Labors

Farms face persistent labor shortages for repetitive manual work. The agricultural robots can work around the clock, leading to no dependency on labor. Thus, many agricultural practitioners are moving toward the adoption of automated agricultural technologies. The adoption of agricultural robots requires a stronger technical ecosystem for installation, maintenance, software use, and data interpretation. This dual pressure prompts farms to invest in automation. It increases demand for training, service support, and user-friendly robotic platforms. Hence, the shortage of skilled labor drives the agricultural robots market growth.

Market Restraints

High Cost of Investment

The cost of agricultural robots is quite high. It prevents many farmers, especially small and medium-sized ones, from adopting them despite their several advantages. Agricultural robots impose financial hurdles due to their initial investment and maintenance expenses, which prevent many farmers from accessing modern technology. Beyond the purchase price, adoption can also be slowed by integration costs, retrofitting requirements, service availability, software subscriptions, and uncertainty around payback periods, particularly for smaller farms with limited capital budgets.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Analysis

By Type Analysis

The milking robots segment dominated the market in 2025. It is due to its ability to be done automatically, without the need for an operator. This makes the procedure flexible and enables the animals to deliver milk on their schedule. The demand for more milk production, the lack of workforce, and the emphasis on farm sustainability and animal welfare fuel the segment dominance. Milking robots witness strong adoption as dairy operations offer a clear and measurable automation use case. Their benefits are labor savings, animal monitoring, milking consistency, and herd management efficiency.

The unmanned aerial vehicles (UAV) segment is anticipated to register the highest CAGR during the forecast period. It is due to their ability to offer benefits for agricultural tasks, including information gathering, air seeding, air spraying, remote sensing detection., and others. Therefore, drone research is crucial to the advancement of precision agricultural. UAVs are increasingly valued for crop surveillance, field mapping, variable-rate application, and real-time decision support. These benefits make them one of the most scalable robotics categories across large farming regions.

By Component Analysis

The hardware segment led the market share in 2025. Hardware items include motors, batteries, and other mechanical parts. They allow robots to perform many tasks in agriculture. Due to their complexity, hardware components often require specialized technical knowledge, precise production processes, and strict quality control. Sensors, cameras, robotic arms, mobility systems, batteries, and embedded components directly impact field performance, durability, and precision. Thus, the segment is expected to maintain its leadership in the coming years.

The software segment is expected to record the fastest growth rate in the coming years. It is due to the rapid development of AI and machine learning (ML) technologies. These innovations have enhanced the capabilities of agricultural robots, enabling them to analyze vast volumes of data, make real-time judgments, and adapt to changing conditions. Farms seek analytics, route optimization, machine vision, predictive maintenance, and workflow integration with digital farm management platforms. Thus, software is becoming a higher-value layer of the market.

By Farming Environment Analysis

The outdoor farming segment dominated the market in 2025. Outdoor farming is an intensive farming. It is heavily automated and has significant financial incentives. Land that is cultivated without the support of a regulated environment is referred to as outdoor farming. It is entirely rain-fed agricultural; the farmer has no influence over the substrate (soil), temperature, or humidity. Outdoor robotics adoption is strong in large-scale row crop systems where navigation, spraying, scouting, and autonomous movement deliver direct productivity and labor benefits.

The indoor farming environment is anticipated to expand at the fastest rate as it can be practiced at any indoor space with controlled indoor cultivation settings, such as using growth media rather than soil, which reduces the risk of insect infections and genetic crop diseases. Greenhouse and vertical farming environments include repetitive tasks. These tasks are easier to standardize, automate, and optimize through robotics and AI-based monitoring. Thus, indoor farming is a high-potential segment for agricultural robots.

By End-User Analysis

The dairy management segment dominated the market in 2025. Automated milking equipment such as milking robots lowers labor expenses and increases milk output. This reduces the physical contact with the cows. It minimizes their stress and pain throughout the milking process. Moreover, agricultural robots can identify and treat any anomalies or health problems in the milk. It improves the well-being of the cows by keeping an eye on the milking procedure using sensors and cameras.

The harvest management segment is expected to register the highest CAGR during the forecast period. It provides more accurate, streamlined, and data-driven techniques to maximize agricultural yields and reduce losses. Advanced robots include sensors, artificial intelligence (AI), and imaging capabilities. Thus, they are essential to the harvest season. They use drones to deliver real-time crop monitoring and assessment.

Agricultural Robots Use Case Matrix

| Robot Type | Farming Task | Crop/Farm Setting |

| Autonomous Tractors | Plowing, seeding, and spraying | Large-scale row crops such as wheat, corn, soybean) |

| Harvesting Robots | Picking and sorting | Fruits & vegetables such as berries, apples, tomatoes) |

| Weeding Robots | Weed detection and removal | Row crops and organic farms |

| Spraying Robots/Drones | Precision pesticide & fertilizer spraying | Vineyards, orchards, and field crops |

| Monitoring Drones | Crop health analysis and mapping | Large farms and plantations |

| Seeding Robots | Precision planting | Row crops and indoor vertical farms |

| Milking Robots | Automated milking | Dairy farms |

| Feeding Robots | Livestock feeding | Poultry, dairy, and livestock farms |

| Greenhouse Robots | Pruning, harvesting, and monitoring | Controlled environments such as greenhouses) |

| Multi-purpose Field Bots | End-to-end farm operations | Mixed farms and small-to-medium holdings |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

North America dominated with the largest global agricultural robots market share. The growth of the segment market can be largely attributed to the rapidly increasing adoption of robotic agricultural farming practices with advanced techniques and technologies. The rising labor cost and shortage of skilled farmers are increasing this region’s growth. Moreover, the high per-capita disposable income is driving the adoption of advanced techniques.

For instance, in May 2023, Farm-ng, a U.S.-based company, demonstrated Amiga, its robot that can adapt to any farm’s cropping system. It can be personalized for a range of tasks, including lifting, planting, seeding, harvesting, and other activities that are unsuitable for costly tractors or dedicated implements.

The Asia Pacific agricultural robots market is expected to register the highest CAGR during the projected period. It is due to the growing adoption of technological advancements for efficient agricultural methods. Rising food demand due to an expanding population and growing concerns about food security boost regional market growth. Robots for agricultural provide a solution by increasing crop yields and automating labor-intensive operations.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Landscape

The Agricultural robots market is fragmented and is anticipated to witness competition due to several players' presence. Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

List of Key Companies

- AG Leader Technology

- AGCO Corporation

- Agribotix LLC

- Autonomous Solutions, Inc.

- Boumatic Robotics, B.V.

- CLAAS KGaA mbH

- CNH Industrial

- Deere & Company

- Drone Deploy

- GEA Group

- Harvest Automation, Inc.

- Topcon Positioning Systems, Inc.

Recent Developments

- In April 2025, John Deere announced it will commercialize its first all-electric autonomous tractor by 2026 after taking a majority stake in Kreisel Electric.

- In March 2025, AGCO introduced its OutRun retrofit autonomy kits for mixed tractor fleets. It will offer 7–8% fuel savings.

- In February 2025, Carbon Robotics launched the LaserWeeder G2. It features a 25% lighter build and modular configurations. It will be suitable for farms ranging from 80 to 800 acres.

- In October 2024, Carbon Robotics raised USD 70 million in a Series D funding round led by NVentures. The company plans to scale production of its LaserWeeder platform, which uses computer vision and CO₂ lasers to remove weeds without chemicals.

- In August 2024, DENSO and Certhon launched Artemy, a fully automated cherry truss tomato harvesting robot, in Europe. Drawing on DENSO’s automotive expertise, the robot addressed labor shortages and boosted efficiency in greenhouses through advanced AI, robotics, and automation.

- In March 2024, the DigiAgro project received USD 3.12 million in financial support from the European Commission to develop Agrobots, which are intended to make Agricultural more efficient and ensure that farmers can continue to earn money sustainably.

- In April 2024, AGCO Corporation and Trimble announced their joint venture to provide farmers with agricultural technologies that minimize the environmental impact.

- In December 2023, Solinftec launched Solix Robot in Agricultural to enhance its agricultural presence and production in the American Midwest and expand its manufacturing capacity in the United States.

Report Coverage

The agricultural robots market report emphasizes on key regions worldwide to provide users with a better understanding of the product. It also provides market insights into recent developments and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis of various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, type, component, farming environment, end-users, and their futuristic growth opportunities.

Agricultural Robots Market Segmentation

By Type Outlook (Revenue – USD Billion, 2021–2034)

- Milking Robots

- Driverless Tractors

- Unmanned Aerial Vehicles

- Material Management

- Others

By Component Outlook (Revenue – USD Billion, 2021–2034)

- Software

- Hardware

- Services

By Farming Environment Outlook (Revenue – USD Billion, 2021–2034)

- Outdoor

- Indoor

By End-User Outlook (Revenue – USD Billion, 2021–2034)

- Crop Management

- Harvest Management

- Inventory Management

- Soil Management

- Dairy Management

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Australia

- Rest of Asia Pacific

- Latin America

- Argentina

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

- Rest of Middle East & Africa

Agricultural Robots Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 18.52 billion |

| Market Size in 2026 | USD 23.26 billion |

| Revenue Forecast in 2034 | USD 149.78 billion |

| CAGR | 26.1% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Agricultural Robots Market FAQ's

The global market is projected to grow from USD 18.52 billion in 2025 to USD 149.78 billion by 2034. It is expected to register a CAGR of 26.1% during 2026-2034.

A few key agricultural robot types are unmanned aerial vehicles, milking robots, driverless tractors, and automated harvesting robots. These robots are used to enhance operational precision and productivity.

Rising food demand and limited workforce availability boost the global market growth. Benefits of robots such as versatile task-handling capacity and reduced long-term operating costs propel the market growth.

North America holds the largest market share due to the presence of key market players. Asia Pacific is the fastest-growing region. It is driven by increasing precision agriculture adoption.

High automation costs for small farmers and technological barriers to fully autonomous systems hinder the market growth. Also, lack of standardization remain critical challenge limiting broader agricultural robot adoption.

Download Sample Report of Agricultural Robots Market

Please fill out the form to request a customized copy of the research report.