Hydrogen Hubs Market Share, Size, Trends, Industry Analysis Report,

By Industry (Automotive, Marine, Aviation, Space, Defense); By Supply Technique; By End Use; By Region; Segment Forecast, 2024- 2032

- Published Date:Jan-2024

- Pages: 115

- Format: PDF

- Report ID: PM4394

- Base Year: 2023

- Historical Data: 2019 – 2022

Report Outlook

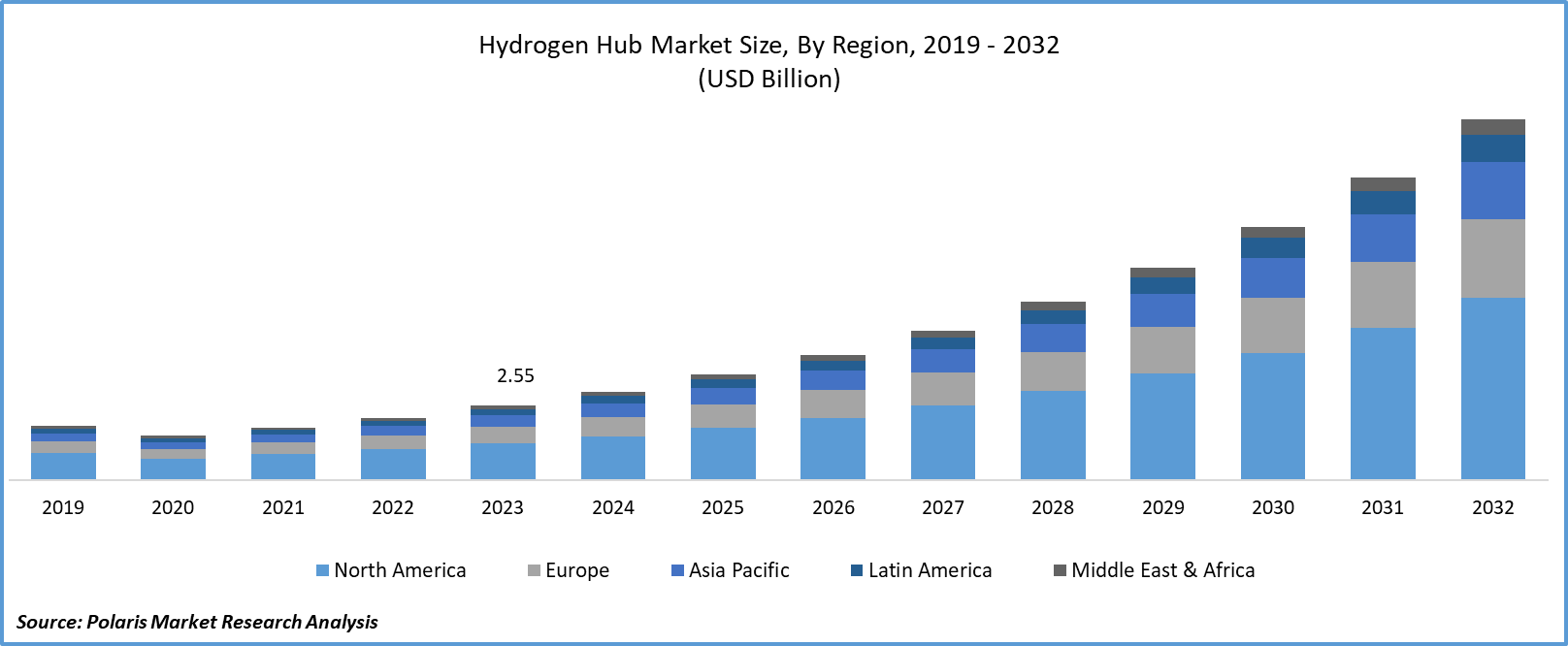

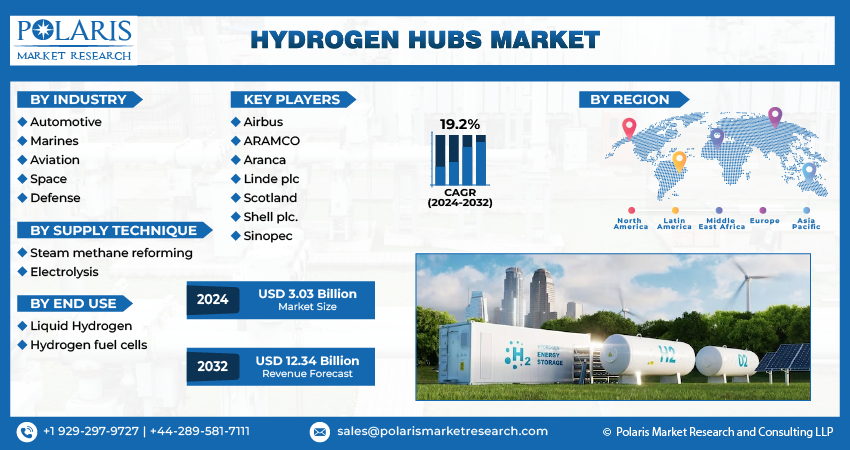

Hydrogen Hubs Market size was valued at USD 2.55 billion in 2023. The market is anticipated to grow from USD 3.03 billion in 2024 to USD 12.34 billion by 2032, exhibiting a CAGR of 19.2% during the forecast period

Industry Overview

A hydrogen hub refers to a geographic area or industrial complex where various hydrogen-related activities are concentrated, promoting an integrated and collaborative ecosystem for the production, distribution, storage, and consumption of hydrogen. These hubs are crucial components of the emerging hydrogen economy, which aims to utilize hydrogen as a clean and sustainable energy carrier. Hydrogen can be used in various applications, including fuel cells for vehicles, industrial processes, and power generation. Hydrogen is typically stored as compressed gas or in liquid form.

Continuous research and development efforts are essential within hydrogen hubs to advance technologies, improve efficiency, and reduce costs associated with hydrogen production and utilization. Hydrogen hubs are seen as strategic initiatives to accelerate the adoption of hydrogen as a clean energy source. They bring together industry, government, and research organizations to collaborate on developing the necessary infrastructure and technologies. The success of hydrogen hubs depends on a combination of technological advancements, supportive policies, and collaboration across various sectors.

- For instance, In April 2023, A long-term contract was signed by Linde to supply green hydrogen to the well-known specialty chemicals manufacturer Evonik.

However, Hydrogen hubs need robust storage infrastructure to ensure a steady supply for different applications. The concept of hydrogen hubs is gaining attention globally as countries seek to transition to cleaner energy sources and reduce carbon emissions. Governments, industries, and research institutions are exploring ways to create and develop such hubs to foster the growth of the hydrogen economy. Increasing government initiatives increases the market demand for hydrogen hubs and thus anticipates growing hydrogen hubs' market share during the forecast period.

To Understand More About this Research: Request a Free Sample Report

Furthermore, green hydrogen is utilized as a feedstock in industries such as chemicals and refining, reducing carbon emissions in sectors that are challenging to electrify, which increases the opportunities in the hydrogen hubs market.

Key Takeaways

- North America dominated the largest market and contributed to more than 40% of share in 2023

- Asia Pacific dominated the fastest market and contributed to more than xx% of share in 2023

- By industry category, automotive segment accounted for the largest market share in 2023

- By end use category, the hydrogen fuel cells expected to witness the highest revenue share during the forecast period

What are the market drivers driving the demand for Hydrogen Hubs Market?

Increasing Focus for Clean Energy

The global shift towards cleaner and more sustainable energy sources to combat climate change has led to a growing interest in Hydrogen as a clean energy carrier. Hydrogen hubs play a crucial role in facilitating the production and utilization of green Hydrogen, produced using renewable energy sources like wind and solar power. Many governments worldwide are implementing policies and incentives to promote the development of hydrogen infrastructure, including hydrogen hubs. The industry growth drivers are the financial support, subsidies, and regulatory frameworks that can significantly boost investments in the hydrogen sector. Growing market size for Hydrogen may result in growing market revenue of hydrogen hubs in the upcoming years.

Moreover, ongoing advancements in hydrogen production technologies, such as electrolysis and steam methane reforming, are making the production of Hydrogen more efficient and cost-effective. Improved technologies contribute to the scalability and competitiveness of hydrogen hubs. Hydrogen is used in various industrial processes, such as refining, chemical production, and manufacturing. As industries seek cleaner alternatives to reduce carbon emissions, the demand for Hydrogen in industrial applications is expected to increase, which ultimately grow share of hydrogen hubs market share.

Which factor is restraining the demand for Hydrogen Hubs?

High initial cost

Establishing hydrogen hubs involves significant upfront investments in infrastructure, such as production facilities, storage, and distribution networks. The high initial costs can act as a barrier, particularly in regions where there is uncertainty about the return on investment. The market challenges restraining the growth of market share are the availability of low-cost and sustainable hydrogen production methods, such as electrolysis using renewable energy sources, which may be limited. There are constraints on the capacity to produce hydrogen in an environmentally friendly and economically viable manner, which could challenge the hydrogen hubs' market size growth.

Report Segmentation

The market is primarily segmented based on Industry, supply technique, end use and region.

|

By Industry |

By Supply Technique |

By End use |

By Region |

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

Category Wise Insights

By Industry Insights

Based on industry analysis, the market is segmented on the basis of automotive, marines, aviation, space, and defense. In 2023, the automotive segment accounted for the largest market share. It is also anticipated that the automotive sector will be a major supplier and user of hydrogen and hydrogen fuel cell stacks inside hubs. In light of the increased emphasis on decarbonization and the search for sustainable substitutes, hydrogen presents itself as a viable option for fuel cell technology-based vehicle fuel. The growing market for hydrogen hubs is being driven by the automotive industry, which is a key user and contributor due to its growing demand for hydrogen-based vehicles and the developments in fuel cell stack technology. It is expected that the automotive sector will see significant investments, partnerships, and innovations during the projected timeframe, which will facilitate the smooth adaptation of H2 Hubs into the larger context of clean and efficient transportation. This shows a significant increase in the market size of the hydrogen hub market.

By End-use Insights

Based on end-use analysis, the market has been segmented on the basis of liquid hydrogen and hydrogen fuel cells. The hydrogen fuel cells are expected to witness the highest revenue share during the forecast period. Its efficiency and benefits to the environment, hydrogen fuel cells are essential for supplying industrial backup power as well as powering a variety of transportation modes. In addition, the manufacturing of liquid hydrogen is essential for long-distance and effective storage, especially in aircraft and other sectors. Intentionally combining these outputs from regional green hydrogen hubs highlights a holistic approach to utilizing hydrogen's potential in multiple industries, promoting a more integrated and sustainable energy ecosystem.

Regional Insights

North America

North America dominated the largest market share in 2023. North America emerged as the dominant force in the global hydrogen hubs market, showcasing robust growth and leadership in the transition towards a hydrogen-based economy. The region's prominence in this market is attributed to the development of hydrogen infrastructure. First and foremost, a supportive policy environment and strategic government initiatives played a pivotal role in incentivizing investments and accelerating the deployment of hydrogen hubs.

Additionally, Hydrogen hubs contribute to the development of a hydrogen infrastructure for FCEVs (fuel cell electric vehicles) in North America. They support the growth of hydrogen-powered transportation, including buses, trucks, and potentially passenger vehicles. The development of hydrogen hubs in North America involves collaboration among government agencies, industry players, research institutions, and technology providers. This collaborative approach fosters innovation, accelerates technology advancements, and supports the growth of the hydrogen economy.

Asia Pacific

The hydrogen hubs market in the Asia Pacific is anticipated to witness the fastest growth during the forecast period, driven by the region's commitment to decarbonization, renewable energy deployment, and the development of a hydrogen-based economy. Robust policy frameworks, including substantial investments, incentives, and regulatory support, created a conducive environment for the development of hydrogen hubs. The significant advancements in renewable energy technologies, particularly solar and wind power, played a crucial role in the production of green hydrogen through cost-effective electrolysis. The region's increasing focus on decarbonizing industries, such as manufacturing and transportation, fueled a growing demand for hydrogen, further stimulating the establishment of hydrogen hubs, which anticipates the hydrogen hubs market growth during the forecast period.

Competitive Landscape

The hydrogen hubs market is characterized by intense competition, with established players relying on advanced technology, high-quality products, and a strong brand image to drive revenue growth. These companies employ various strategies such as research and development, mergers and acquisitions, and technological innovations to expand their product portfolios and maintain a competitive edge in the market.

Some of the major market key players operating in the global market include:

- Airbus

- ARAMCO

- Aranca

- Linde plc

- Scotland

- Shell plc.

- Sinopec

Recent Developments

- In July 2022, Shell Overseas Investments B.V., subsidiaries of Shell plc, and Shell Nederland B.V. announced their investment decisions to build Holland Hydrogen. This project aims to establish Europe's largest renewable hydrogen plant by the year 2025. The hydrogen generated will be employed at the Shell Energy and Chemicals Park Rotterdam, replacing conventional grey hydrogen in the refinery.

Report Coverage

The hydrogen hubs market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive industry, supply technique, end use and their futuristic growth opportunities.

Hydrogen Hubs Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 3.03 billion |

|

Revenue forecast in 2032 |

USD 12.34 billion |

|

CAGR |

19.2% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024– 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments Covered |

By Industry, By Supply Technique, By End use, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The global hydrogen hubs market size is expected to reach USD 12.34 billion by 2032

Key players in the market are ARAMCO, Shell plc., Linde plc, Airbus, Sinopec

North America contribute notably towards the global Hydrogen Hubs Market

Hydrogen Hubs Market exhibiting the CAGR of 19.2% during the forecast period

The Hydrogen Hubs Market report covering key segments are Industry, supply technique, end use and region.

© 2025 Polaris Market Research and Consulting. All rights reserved