Silicon Photonics Market Size, Share & Forecast, 2026-2034

REPORT DETAILS

Market Statistics

Silicon Photonics Market Overview

The global silicon photonics market was valued at USD 2.89 billion in 2025. It is projected to grow at a CAGR of 28.5% from 2026 to 2034. Rising data traffic and demand for faster optical communication are accelerating market adoption. The market for silicon photonics is gaining prominence because conventional electrical interconnects are struggling to provide the required bandwidth in today’s cloud infrastructure. Silicon photonics technology enhances data transmission and reduces power consumption by allowing optical data transmission on silicon chips.

Key Takeaways

- The Asia Pacific silicon photonics market led the global market with 45.0% share in 2025. China’s "Made in China 2025" plan is influencing investments and R&D expenditures in silicon photonics. Beyond policy initiatives, the dominance of the region is supported by the rapid expansion of data center infrastructure and the growing 5G rollout.

- The North America silicon photonics market is expected to develop at the fastest rate of 32.0% during the forecast period. This is due to the increasing demand for silicon photonics across various sectors. They include quantum computing, telecommunications, healthcare, and defense.

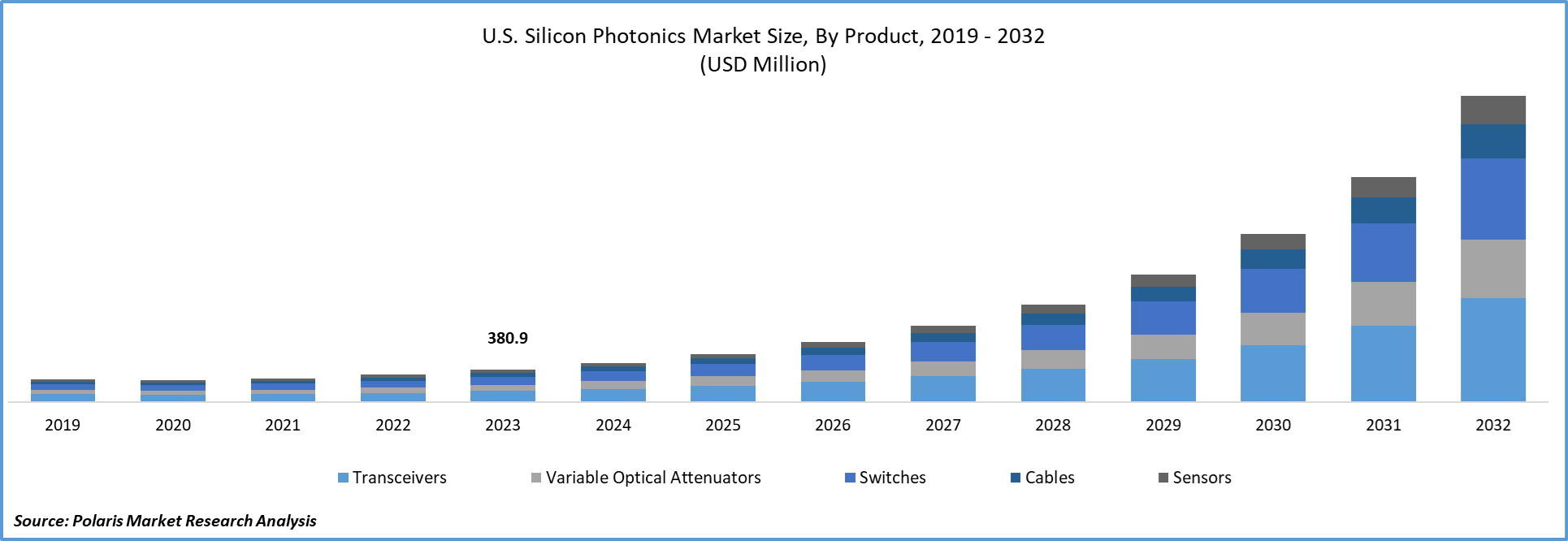

- Transceivers were the market leader in 2025 with a revenue share of 52.0% in 2025. Silicon photonics transrecivers are increasingly adopted as they support higher bandwidth density and lower power consumption per bit. These are key requirements for hyperscale data centers and telecom network upgrades.

- The telecommunications segment is expected to grow the fastest with 27.9% during the forecast period. The segment’s growth is driven by the increased use of silicon photonics in high-speed optical communications.

- The 1,310–1,550 NM segment accounted for 60.0% revenue share in 2025, as it covers the optimal low-loss, low-dispersion optical transmission windows used in telecom, datacom, and data center interconnects.

*

Source: Polaris Market Research Analysis

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.Industry Dynamics

- One of the key silicon photonics market drivers is the transition towards automated manufacturing technology. This has led to growing demand for silicon photonics technology.

- The workload associated with artificial intelligence, IoT, and cloud computing is causing network congestion. This has created increased demand for energy-efficient, low-latency data transmission technologies. Silicon photonics supports higher data transmission rates while consuming less energy per transmitted bit. It addresses one of the most pressing issues associated with digital systems today.

- The rising use cases in telecommunication, data centers, the military, and the medical sector drive the widespread adoption of silicon photonics solutions.

- Silicon photonics packaging challenges remain a major market hindrance. Thermal and fiber alignment-related challenges make the packaging process complex.

Market Statistics

- 2025 Market Size: USD 2.89 billion

- 2034 Projected Market Size: USD 21.49 billion

- CAGR (2026-2034): 28.5%

- Asia Pacific: Largest Market Share

AI Impact on Silicon Photonics Market

- The demand for silicon photonics is being fueled by AI, including advancements that improve data processing speeds and support high-performance computing analysis.

- AI application workloads have created the need for high-bandwidth and low-latency interconnects. Silicon photonics allows for scalable AI data centers through co-packaged optics silicon photonics solutions.

- The dependence of AI on huge volumes of data, particularly in cloud computing and big data analysis, increases the demand for high-speed and low-latency interconnects, which silicon photonics can deliver.

- AI and machine learning software hasten the design and optimization of silicon photonics devices, enhancing their efficiency and flexibility.

- AI-powered manufacturing automation allows for the production of silicon photonics components with greater accuracy and at scale. This improves yield and reduces costs.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

What is Silicon Photonics?

Silicon photonics is a technology that uses light (photons) instead of electrical signals. The technology is used to transfer data through silicon-based chips. It enables faster data transmission, higher bandwidth, and lower power consumption. Due to these features, it is widely used in data centers, telecommunications, high-performance computing, and advanced sensing applications.

What is the Difference Between Silicon Photonics and Electronic Chips?

| Parameter | Silicon Photonics | Electronic Chips |

| Data Transmission Medium | Light (photons) | Electrical signals |

| Speed | Very high | Moderate to high |

| Bandwidth | Extremely high | Limited compared to optical systems |

| Power Consumption | Lower for high-speed transfer | Higher at high data rates |

| Heat Generation | Lower | Higher |

| Signal Loss | Minimal over longer distances | Higher due to resistance |

| Scalability | Better for large data centers | Limited for ultra-high-speed scaling |

| Cost | Higher initial cost | Lower initial cost |

| Common Applications | Data centers, telecom, HPC, AI | PCs, smartphones, embedded systems |

Source: Polaris Market Research Analysis

Industry Trends

The increasing acceptance of automated manufacturing practices, along with the innovative developments in technology, is anticipated to boost the market growth globally. The wide range of applications of silicon photonics, including medical & life sciences, military, telecommunication, and data center, among others, is anticipated to drive the demand worldwide. Pressing bandwidth, virtualization, fast-growing internet traffic, and cloud computing, among others, are key factors driving the silicon photonics market growth.

Furthermore, the current use of silicon for the development of IC (integrated circuits), along with the compatibility of this technology with the present fabrication techniques, is encouraging various companies to adopt this technology in the electronics manufacturing industry. In addition, 5G technology, with its higher bandwidth, is likely to create new demand in the market in the near future. The growth of IoT and the adoption of AI-powered devices also contribute to the market expansion.

What’s Driving Silicon Photonics Market Demand?

Increasing Adoption of Private Networks

5G technology offers an enhanced platform with built-in support for important critical capabilities, lower latency, increased reliability, and improved security, which is expected to meet the business requirements. In addition, the need for critical wireless communication in industrial operations is likely to create novel opportunities for 5G networks. In the industrial sector, a company can either opt for a public network to connect to or choose a private 5G network for its business operations, in which case the business entity can purchase its own infrastructure and rely on the 5G network provider for operational support.

Advantages associated with 5G private networks include customized configurations based on location and manufacturing site. In addition, a company can determine the deployment and coverage quality of the private network based on its requirements. Furthermore, private networks can be installed and maintained by personnel working on-site. This leads to faster responses to problems and issues that occur during day-to-day operations without time loss.

Thus, the increasing demand for 5G networks in industrial applications such as manufacturing facilities and logistics is expected to drive market growth over the forecast period. As private 5G networks support high data rates and ultra-low latency, they need robust optical backhaul infrastructure. Optical fiber communication, enabled by silicon photonics technology, helps meet performance needs by providing energy-efficient data transmission. Furthermore, with the digitalization of the industrial sector, there is a need for networks with improved connectivity. This is expected to contribute to the increased demand for private 5G networks and boost the adoption of silicon photonics solutions worldwide.

What’s Restaining Demand for Silicon Photonics?

Presence of Alternative Materials

It has been evident in recent years that packaging remains a key challenge across areas such as source and electronic integration, fiber-array coupling, and efficient thermal management. The primary reason for the growth of the silicon photonics industry is that it can meet the high-volume application needs. Although wafer-scale processing can certainly cater to this need, packaging has to be a device-by-device process, which is difficult to scale.

To address such hurdles, stakeholders across the value chain are implementing strategies such as highly innovative designs, increased collaboration with equipment suppliers, a focus on developing faster alignment processes, and the integration of passive and automated systems into the overall process. Companies are integrating novel practices alongside standard packaging design rules to overcome the packaging challenges currently faced by the industry.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Report Segmentation

By Product Insights

Based on product analysis, the silicon photonics market is segmented into transceivers, variable optical attenuators, switches, cables, and sensors. Transceivers held the largest market share of 52.0% in 2025. The silicon photonics transceiver uses silicon photonics technology to seamlessly combine photoelectric conversion and data transmission on a silicon chip. At its essence, silicon optical technology revolves around the concept of "substituting electricity with light," where a laser beam replaces electronic signals for data transmission, and optical devices and electronic components are integrated into a self-contained microchip. Furthermore, utilizing silicon photonics technology in transceivers facilitates the creation of compact and cost-efficient devices. This helps meet the substantial demand within the expanding data communication sector.

By Application Insights

Based on application analysis, the silicon photonics market has been segmented on the basis of data centers and high-performance computing, telecommunication, military & defense and aerospace, medical and life science, and other applications. The telecommunication segment is expected to be the fastest-growing with 27.9% CAGR during the forecast period. Telecommunications is another substantial arena for the use of silicon photonics. In the realm of telecommunications applications, the focus is on implementing silicon photonics-based devices to enable high-speed optical communications across both long-haul and metro networks. Significant advancements are being observed in this industry's technologies, such as Wavelength-Division Multiplexing (WDM), optical amplifiers, and coherent transmission systems. These advancements are ushering in higher data rates, extended transmission distances, and improved network performance.

The silicon photonics market is presently undergoing significant growth within the data center sector. The present trends in the data center market span advancements in high-speed data transfer, higher bandwidth, greater power efficiency, and greater scalability. Silicon photonics technology is a vital aspect in advancing high-speed optical interconnects, optical switches, and other optical components to meet the growing demand for data-intensive applications, including cloud computing, AI, big data analytics, and more.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

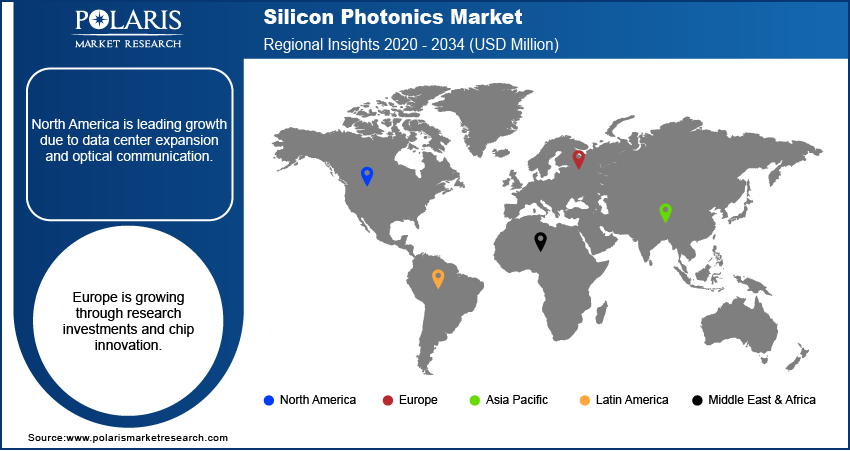

Regional Insights

Asia Pacific

Asia Pacific accounted for the largest silicon photonics market share of 45.0% in 2025. The demand for silicon photonics in the Asia Pacific region is significantly shaped by the Chinese government's strategic efforts. The most notable of them is the "Made in China 2025" plan. This initiative supports research and development (R&D) efforts in factory automation and associated technologies. It also contributes to investments in these areas.

A major objective of the "Made in China" initiative is to minimize the country’s reliance on the importation of automation technology. Additionally, the initiative intends to enhance automation technology in the country. Consequently, this accelerates the growth of Silicon Photonics because of its significance in improving the efficiency of automation technology.

Furthermore, the rest of the Asia Pacific, including countries such as India, Singapore, and Taiwan, is experiencing rapid technological advancements. They include AI, IoT, 5G, and virtual reality, as well as the commercial application of these innovations. This technological evolution is driving a surge in demand for data processing and information interaction. As a result, data center construction is on the rise, with China, Japan, Australia, India, and Singapore among the top markets, according to Cloud Scene.

North America

North America is likely to have the fastest growth with 32.0% CAGR in the forecast period. This is due to increasing awareness of the transformative potential of silicon photonics across industries. Silicon photonics allows for the integration of optical components into semiconductor materials. This enables faster data transfer rates and lowers power dissipation. It also opens new performance possibilities. As the advantages become increasingly apparent, demand for silicon photonics solutions is growing rapidly.

Notable in this region is the significant spending on research and development. The North America region also has the dominance of top companies in silicon photonics. It can be seen from the joint venture between SkyWater Technology and PsiQuantum that various firms in the silicon photonics market are working to develop silicon photonics. Joint ventures in silicon photonics boost research and development. They also allow companies to leverage new technologies, such as silicon photonics, in quantum computing.

Government programs further strengthen market demand for silicon photonics in the region. In October 2021, the investment of more than USD 321 million was made by the government of the State of New York in the American Institute of Manufacturing Photonics, the Air Force Research Laboratory, and the State University of New York Research Foundation. This highlighted the country's overall photonics readiness and its significance to the U.S. national security. Such projects underscore the importance of silicon photonics in the development of high-performance microelectronics.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Landscape

The silicon photonics competitive landscape is dominated by major participants such as Intel Corporation, Cisco Systems Inc., and Broadcom Inc. As major players have strong knowledge and expertise in semiconductor technology and optical communication, they have been able to maintain their market positions. The new entrants, especially from the Asia Pacific, have also begun to show interest in the market and are adopting innovative strategies by developing silicon photonics solutions tailored to specific applications. Strategic collaborations and foundry partnerships are accelerating commercialization timelines.

Some of the major players operating in the global silicon photonics market include:

- AIO Core Co., Ltd

- Cisco Systems, Inc.

- Finisar Corporation

- Hamamatsu Photonics K.K

- International Business Machines Corporation (IBM)

- Infinera Corporation

- Intel Corporation

- IPG Photonics Corporation

- NVIDIA Corporation

- Sicoya

- STMicroelectronics N.V

Silicon Photonics Industry Developments

- January 2026: Flexcompute announced collaboration with GlobalFoundries (GF). The companies aim to integrate GF's silicon photonics technology stack into PhotonForge. It is a photonic design and simulation platform powered by the Tidy3D multi-physics engine. (Source: https: prnewswire)

- December 2025: GlobalFoundries (GF) partnered with Finnish venture capital firm Cloudberry to reinforce Europe’s semiconductor and photonics startup ecosystem. GF will invest in Cloudberry’s new fund while offering technology know-how, resources, and design support to help startups progress from concept to industrial-scale production. (Source: gf.com)

- September 2025: Coherent Corp. introduced 400 mW continuous-wave lasers for silicon photonics and co-packaged optics uses. Operating at 1311 nm, the lasers deliver stable high output, low noise, and narrow linewidths, addressing major optical interconnect challenges. Engineering samples are currently available, with volume production planned for Q3 2026. (Source: coherent.com)

Report Coverage

The silicon photonics report emphasizes key regions across the globe to provide a better understanding of the product to the users. Also, the report provides market insights into recent developments, trends, and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market, focusing on key aspects such as competitive analysis, product, component, application, waveguide, and their future growth opportunities.

Silicon Photonics Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Transceivers

- Variable Optical Attenuators

- Switches

- Cables

- Sensors

By Component Outlook (Revenue – USD Billion, 2021–2034)

- Lasers

- Modulators

- Photo Detectors

- Optical Waveguide

- Wavelength Division Multiplexing (WDM) Filters

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Data Centres and High-performance Computing

- Telecommunication

- Military & Defence and Aerospace

- Medical and Life Science

- Other Applications

By Waveguide Outlook (Revenue – USD Billion, 2021–2034)

- 400-1,500 NM

- 1,310-1,550 NM

- 900-7000 NM

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

What is the Future of Silicon Photonics Market?

The market is expected to witness strong growth in the coming years. The expansion will be driven by the rising adoption of AI, cloud computing, and hyperscale data centers. The increasing demand for high-speed communication and low-latency data transfer will drive market expansion. The integration of silicon photonics into next-generation semiconductors is improving performance and scalability. The growing focus on energy-efficient data transmission solutions would also support innovation and long-term market development.

Silicon Photonics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2.89 billion |

| Market Size in 2026 | USD 3.71 billion |

| Revenue Forecast by 2034 | USD 21.49 billion |

| CAGR | 28.5% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Silicon Photonics Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Silicon Photonics Market FAQ's

Silicon photonics involves the integration of the optical element with semiconductor materials. This results in high-speed data transmission, low power usage, and advanced performance.

The silicon photonics market is expected to reach USD 21.49 billion by 2034, growing at a CAGR of 28.5%.

The Asia Pacific had the leading share of 45.0% in 2025 due to investments by China.

Key areas of application are data centers, telecommunications, military and defense, healthcare, and high-performance computing. The largest product segment driving demand in the market is transceivers.

AI drives demand for high-speed, low-latency interconnects in cloud computing and big data. AI-powered automation improves the efficiency of silicon photonics manufacturing and design optimization.

Silicon Photonics integrates optical elements with semiconductor materials on silicon chips, enabling high-speed data transmission, low power consumption, and compatibility with existing semiconductor manufacturing processes across diverse applications.

Key trends include surging data center demand, rising cloud computing and 5G adoption, AI-driven bandwidth needs, and growing silicon photonics use in telecom, healthcare, and quantum computing applications.

Download Sample Report of Silicon Photonics Market

Please fill out the form to request a customized copy of the research report.