Direct-To-Consumer Testing Market Trends Analysis Report, 2026-2034

REPORT DETAILS

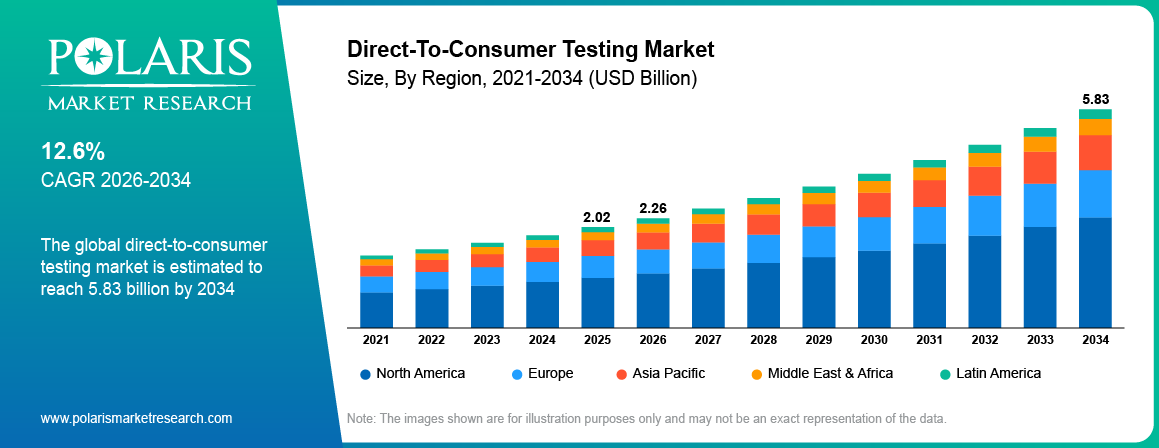

Direct-To-Consumer Testing Market Summary

The global direct-to-consumer testing market is estimated around USD 2.02 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by rising chronic disease burden and expanding genetic testing applications that are increasing demand for direct-to-consumer testing across global markets. The market is projected to grow at a CAGR of 12.6% during the forecast period.

Market Statistics

Key Takeaways

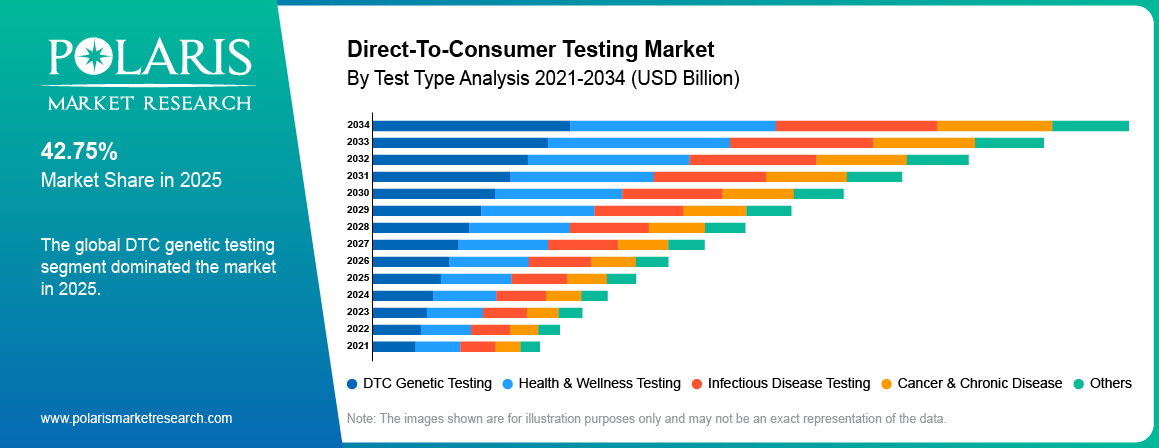

- The DTC genetic testing segment was dominant in 2025 by holding 42.7% share due to strong consumer interest in ancestry and risk analysis.

- The online platform segment dominated the global market by 64.6% revenue share in 2025 due to convenient ordering and direct digital result access.

- Rapid growth is expected in the health & wellness testing segment with CAGR of 12.9% due to rising demand for preventive health monitoring.

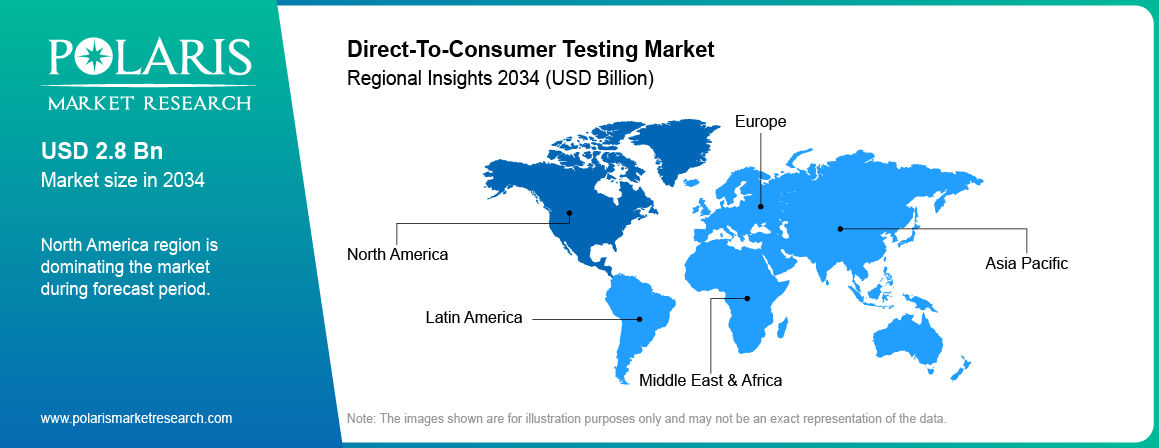

- North America dominated the market by holding 49.72% share due to advanced diagnostics infrastructure and strong consumer awareness.

- Asia Pacific is experiencing growth at a CAGR of 13.3% in the market owing to increasing consumer awareness regarding preventive healthcare.

Industry Dynamics

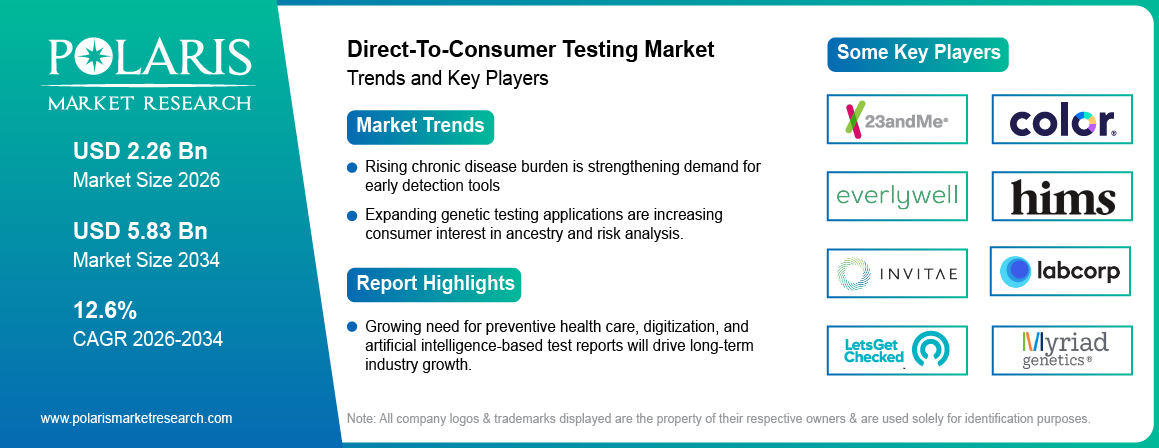

- Rising chronic disease burden is strengthening demand for early detection tools.

- Expanding genetic testing applications are increasing consumer interest in ancestry and risk analysis.

- Stringent regulatory requirements are increasing compliance costs for providers.

- AI-based health insights are improving the value of test reports.

What is Direct-To-Consumer Testing?

Direct-to-consumer testing is the process through which individuals can order health tests, collect samples at home or visit partner labs, and receive results without a mandatory physician visit. Some of these tests include genetic testing, wellness biomarker testing, hormone testing, screening of infectious diseases, and assessment of the risk of developing chronic conditions. This sector is experiencing traction owing to increasing health consciousness, convenience, and the increasing interest in preventive care.

The value chain of the direct-to-consumer testing industry includes test kit development, digital platform integration, sample collection, laboratory analysis, result reporting, and post-test consultation services. The main aim of this industry is to enhance personal health information accessibility, test time reduction, and making healthy life choices based on facts. Rising demand for telemedicine services, personalized medications, and digital diagnostics has made companies invest in testing innovations and expansion of their platforms. A strong trend of consumer adoption is backing the growth of the market for an extended period.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

The growth of the market has been witnessed through ancestry and genetic testing, wherein consumers require data related to their ancestral background and genetics. In addition, with the rising prevalence of digital healthcare the market requirement is expected to rise for wellness, disease screening, and health monitoring purposes. Increasing use of smartphones and digital health solutions is expected to fuel market growth.

Drivers & Opportunities

Rising chronic disease burden is strengthening demand for early detection tools: The rising prevalence of diabetes, cardiovascular disease, obesity, and cancer is pushing people to test the risk factors of their diseases during an early stage. Chronic diseases like heart disease, cancer, and diabetes have emerged as the leading causes of mortality in the US, accounting for around USD 4.9 trillion in healthcare expenditure each year. Consumers can easily undergo their screenings and biomarker tests through direct-to-consumer testing kits. Besides, preventive care services have increased significantly in the last few years.

Expanding genetic testing applications are increasing consumer interest in ancestry and risk analysis: Individuals are eager to learn about their genetic profile and potential threats that are associated with it. According to WHO, roughly 7.9 million babies born annually have genetic disorders or partial genetic disorders, and the Eastern Mediterranean zone contributes 26% of all global β-thalassemia pregnancies. Therefore, there is a rising demand for genetic testing products that provide services in wellness, carrier testing, and pharmacogenomics, which promotes home-based testing services.

Restraints & Challenges

Stringent regulatory requirements are increasing compliance costs for providers: Compliance with laboratory protocols, patient data privacy policies, and test approvals are necessary. With the changing regulations in developing regions, more funds are allocated to quality management, documentation, and drug trials. Small firms are finding it difficult to cope with costly procedures and lengthy approval periods.

Opportunity

AI-based health insights are improving the value of test reports: AI is leveraged by corporations in providing personalized recommendations along with better interpretation of test results. In June 2025, Macrogen enhanced the use of AI for direct-to-consumer testing by launching GenTok, an AI-driven platform that provides personalized information about health from 129 genetic traits. As AI tools help identify trends, risk indicators, and wellness actions from complex health data. This added value is improving customer engagement and creating growth opportunities for premium testing services.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report offers detailed coverage of the direct-to-consumer testing market test type, technology, and distribution channel to help readers identify the fastest expanding and most attractive demand segments.

By Test Type

-

DTC Genetic Testing

The DTC genetic testing segment was dominant in 2025 by holding 42.7% share due to strong consumer demand for ancestry insights, inherited trait analysis, and disease risk screening. Established brand awareness and wider online availability supported segment growth. Rising interest in personalized healthcare is strengthening demand.

-

Health & Wellness Testing

Rapid growth is expected in the health & wellness testing segment with CAGR of 12.9% in the forecast period owing to increased emphasis on preventive healthcare. People are now inclined towards conducting biomarker tests, hormonal tests, vitamin tests, and metabolic tests. Rising awareness regarding wellness is aiding the fast growth of this market.

By Technology

-

Single Nucleotide Polymorphism Chips

Single nucleotide polymorphism chips segment was dominating the market in 2025 due to cost efficiency and high scalability for ancestry and trait-based genetic testing. Many providers use this technology for mass-market consumer kits. Fast processing timelines supported segment leadership.

-

Whole Genome Sequencing

Whole genome sequencing is likely to record the highest growth rate in terms of CAGR throughout the forecast period owing to improvements in sequencing efficiency and declining processing expenses. Consumers now need detailed information about their genes rather than mere information on traits.

By Distribution Channel

-

Online Platform

The online platform segment dominated the global market by 64.6% revenue share in 2025 due to easy test ordering, digital result access, and direct consumer engagement. Companies are using e-commerce channels and mobile apps to expand reach. According to the report issued by the US Census Bureau, the total sales from retail e-commerce in the US stood at USD 304.2 billion in the second quarter of 2025, showing an increase of 1.4% from the previous quarter.Also, rising convenience is supporting strong segment demand.

-

OTC

OTC segment is projected to grow at the fastest CAGR during the forecast period due to rising availability of test kits across pharmacies and retail stores. Consumers prefer quick offline access for urgent or first-time purchases. Expanding retail partnerships are supporting segment growth.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

North America Direct-to-Consumer Testing Market Overview

North America dominated the market by holding 49.72% share owing to consumer awareness, high adoption of digital healthcare, and the availability of diagnostic equipment. The US is at the forefront, facilitated by telehealth services, wellness programs in the workplace, and heavy investments in preventative screening. In August 2025, Ultima Genomics entered into an agreement with Gene by Gene to provide low-cost sequencing of DNA samples using their UG 100 technology for consumer genetics. The regulatory environment is contributing towards improved quality and market confidence.

Asia Pacific Direct-To-Consumer Testing Market Insights

Asia Pacific is experiencing growth at a CAGR of 13.3% in the market over the forecast period, owing to the high adoption of digital health and growing middle class expenditure on healthcare in China, India, Japan, and South Korea. According to National Healthcare Security Administration, China’s basic medical insurance fund reported USD 520 billion in revenue and USD 439 billion in spending in 2025, while covered outpatient visits rose 25.51% to USD 1.05 billion. As China remains the largest regional market due to strong e-commerce healthcare platforms and rising consumer interest in wellness testing.

Europe Market Insights

Europe has significant market share owing to rising demand for at-home diagnostics and preventive health services. The countries such as Germany, France, and the UK are important markets that receive support through increasing health awareness and adoption of self-tests. Regulatory convergence for diagnostic products is leading to high-quality products and pushing market penetration.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Landscape & Key Players

The consumer-direct testing industry is moderately fragmented, featuring competition between diagnostics firms, digital health firms, genetic testing services, and local laboratories. Test accuracy, regulatory compliance, brand trust, user experience for digital tests, and speed of results are the crucial factors to consider. The use of artificial intelligence in analytics, rising portfolio of tests offered, security of test data, and partnering with healthcare entities are helping companies compete in the sector.

Among the major companies operating in this industry are Everlywell, Inc., LetsGetChecked, Inc., 23andMe, Inc., Color Health, Inc., Myriad Genetics, Inc., Quest Diagnostics Incorporated, Labcorp Holdings Inc., Vault Health, Inc., Viome Life Sciences, Inc., Nurx, Inc., Hims & Hers Health, Inc., Invitae Corporation, and others.

Premium Insights

Shift from Ancestry Testing to Clinical Utility

The direct-to-consumer testing industry is evolving from first-generation ancestry testing to clinically actionable health information. Consumers require tests that have practical implications like genetic predispositions towards certain conditions, pharmacogenomic tests, hormones, and metabolism. Privacy issues, accuracy of data, and medical consultation have gained significance in the decision-making process. There are companies that are establishing a strong position due to the provision of a secure platform, physician interpretations, and prevention services.

AI and Digital Ecosystems Are Reshaping Consumer Testing

Artificial intelligence and connected digital health platforms are improving the long-term value of direct-to-consumer testing services. Providers are using AI tools to simplify reports, identify health trends, and recommend next steps based on results. Telehealth integration, wellness subscription, and online coaching have growing the number of repeat purchases after initial testing. This trend has enabled firms to adopt sustainable business models and improve customer retention rates.

Key Players

- 23andMe, Inc.

- Color Health, Inc.

- Everlywell, Inc.

- Hims & Hers Health, Inc.

- Invitae Corporation

- Labcorp Holdings Inc.

- LetsGetChecked, Inc.

- Myriad Genetics, Inc.

- Nurx, Inc.

- Quest Diagnostics Incorporated

- Vault Health, Inc

- Viome Life Sciences, Inc.

Industry Developments

- March 2026: Everlywell announced a new partnership with Jona to launch an advanced at-home microbiome test that expands consumer access to personalized gut health insights. [source: jona.health]

- February 2026: 23andMe announced a study showing that direct-to-consumer genetic testing drove strong medical follow-up, with 88% of participants following doctor recommendations after sharing results. [source: 23andme.com]

Direct-To-Consumer Testing Market Segmentation

By Test Type Outlook (Revenue, USD Billion, 2021-2034)

- DTC Genetic Testing

- Health & Wellness Testing

- Infectious Disease Testing

- Cancer & Chronic Disease

- Other

By Technology Outlook (Revenue, USD Billion, 2021-2034)

- Whole Genome Sequencing

- Single Nucleotide Polymorphism Chips

- Targeted Analysis

- Others

By Distributional Channel Outlook (Revenue, USD Billion, 2021-2034)

- Online Platform

- OTC

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Direct-To-Consumer Testing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2.02 Billion |

| Market Size in 2026 | USD 2.26 Billion |

| Revenue Forecast by 2034 | USD 5.83 Billion |

| CAGR | 12.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Direct-To-Consumer Testing Market FAQ's

The global market size was valued at USD 2.02 Billion in 2025 and is projected to grow to USD 5.83 Billion by 2034.

North America dominates the market due to advanced diagnostics infrastructure and high digital health adoption.

Major applications include genetic screening, wellness biomarker testing, infectious disease testing, and chronic disease risk assessment.

A few of the key players in the market are Everlywell, Inc., LetsGetChecked, Inc., 23andMe, Inc., Color Health, Inc., Myriad Genetics, Inc., Quest Diagnostics Incorporated, Labcorp Holdings Inc., Vault Health, Inc., Viome Life Sciences, Inc., Nurx, Inc., Hims & Hers Health, Inc., Invitae Corporation, and others.

Key drivers include rising preventive healthcare demand, growing chronic disease burden, and expanding digital health platforms.

Major demand comes from healthcare consumers, wellness providers, employers, telehealth platforms, and diagnostic laboratories.

The market outlook remains positive due to AI-based insights, personalized healthcare demand, and expanding at-home diagnostics adoption.

Download Sample Report of Direct-To-Consumer Testing Market

Please fill out the form to request a customized copy of the research report.