Osteoarthritis Injectable Market Size Report 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Osteoarthritis Injectable Market Summary

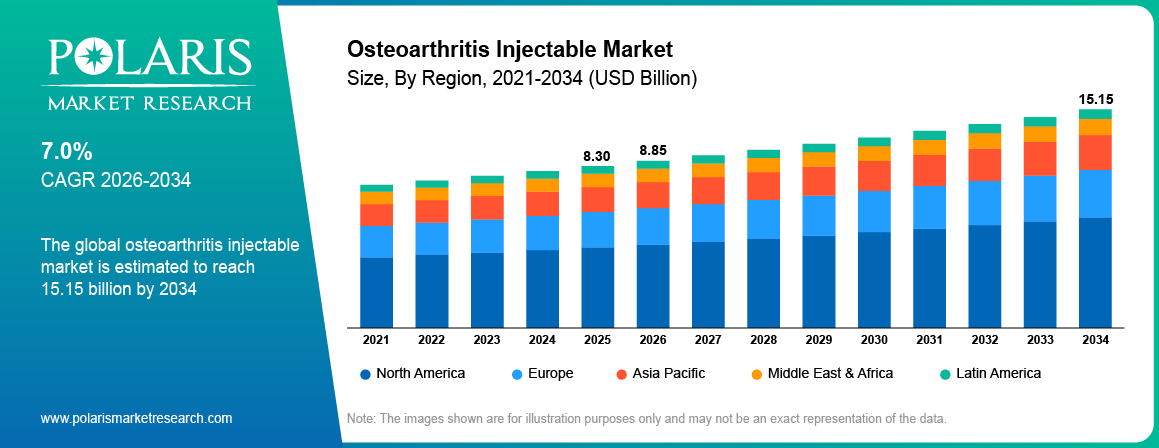

The global osteoarthritis injectable market is estimated around USD 8.30 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by rising osteoarthritis burden and growing elderly population that are increasing demand for osteoarthritis injectables across global markets. The market is projected to grow at a CAGR of 7.0% during the forecast period.

Market Statistics

Key Takeaways

- The hyaluronic acid injections segment was dominant by 39.7% revenue share in 2025 due to strong use in joint lubrication and pain management therapies.

- The hospital pharmacies segment dominated in 2025 with 48.5% revenue share due to high patient volume and physician-led treatment administration.

- The PRP injections market is anticipated to show rapid at CAGR of 7.8% growth due to the increasing demand for regenerative joint therapy products.

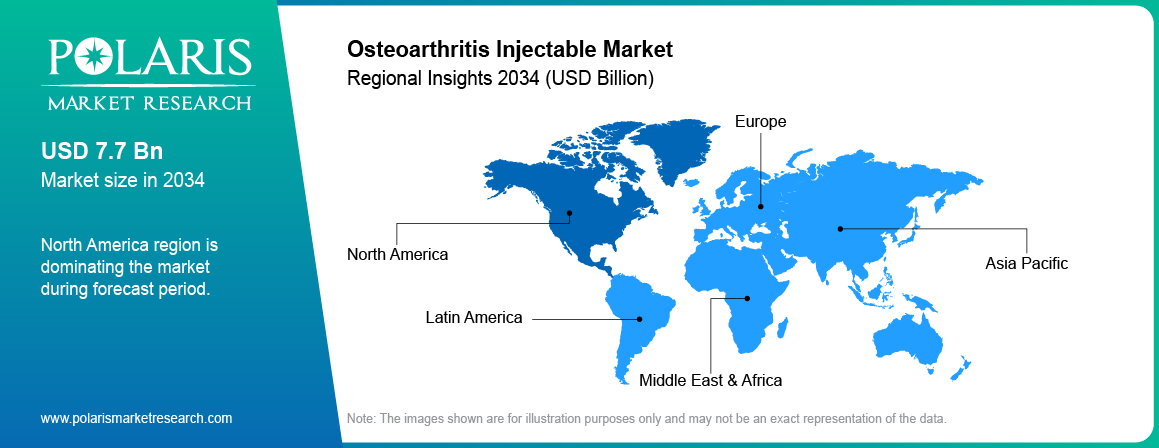

- North America dominated the osteoarthritis injectable market by 51.74% market share due to advanced healthcare systems and strong treatment adoption.

- Asia Pacific is the fastest-growing region in the osteoarthritis injectable market, growing at a CAGR of 7.7% owing to the rising geriatric population, increasing prevalence and diagnosis of osteoarthritis.

Industry Dynamics

- Rising prevalence of osteoarthritis is increasing demand for injectable pain management therapies.

- Increasing elderly patient population is driving the number of treatments worldwide.

- Expensive biologics injection therapies deter their use in economies that cannot afford them.

- Expansion of outpatient orthopedic centers is improving treatment access and procedure volumes.

What is Osteoarthritis Injectable?

Osteoarthritis injectable drugs are medications administered intra-articularly to address the pain, stiffness, and decreased mobility caused by osteoarthritis. This technique can be employed on the knees, hips, and shoulders and functions as a method of avoiding surgery and improving the functional capacity of the patients. Treatment modalities include hyaluronic acid injections, corticosteroid injections, platelet-rich plasma injections, and novel regenerative biologics. The market for such drugs is experiencing growth owing to the increasing occurrence of osteoarthritis, aging population, and the need for non-surgical pain relief treatment options.

The osteoarthritis injectable value chain consists of product innovation, drug testing, FDA approval, manufacturing, purchase from hospitals and clinics, medical administration, and post-treatment follow-ups. The main aim of this industry is to reduce pain, improve joint movement, and extend the life of affected joints. Increasing capital expenditure in biologics, imaging support, and sports medicine practices has helped in driving the adoption of the products. High demand by orthopedic practices, pain management centers, and ambulatory clinics has been fueling the growth of the market.

The market initially took shape through corticosteroid injections for temporary relief of pain in osteoarthritis patients. With advancements in treatment techniques, market demand has been seen shifting towards hyaluronic acid injections and biological injections that provide relief for a prolonged period. Increasing healthcare expenditure, obesity, and patient education are additional growth drivers in this sector.

Drivers & Opportunities

Rising osteoarthritis cases are increasing demand for injectable pain management therapies: Rise in the number of patients suffering from osteoarthritis of knee joints, hips, and shoulders has increased the need for non-surgical treatment methods. According to the Professional Society for Health Economics and Outcomes Research (ISPOR), global osteoarthritis prevalence reached 8.13% in 2023, while the age-standardized prevalence was 7.16%. The rising prevalence of this disorder is driving up demand for corticosteroid injections, hyaluronic acid injections, and regenerative injections.

Growing elderly population is supporting higher treatment volumes for joint disorders: Senior citizens have a relatively higher probability of cartilage degeneration, joint stiffening, and impaired mobility. According to WHO, the world’s population aged 60 years and over is expected to grow from 1 billion in 2020 to 2.1 in 2050. Such changes make the pool of patients suffering from conditions like osteoarthritis more substantial. The provision of musculoskeletal services is becoming more extensive due to increased needs.

Restraints & Challenges

High cost of advanced biologic injections is limiting patient adoption: These types of biologic drugs like platelet rich plasma and stem cell therapy are relatively expensive compared to traditional treatments for pain. In many cases, there is little or no insurance reimbursement for these drugs. The reluctance of patients to undergo treatment due to higher costs is impacting market penetration of premium injectable drugs.

Opportunity

Expansion of outpatient orthopedic centers is increasing procedure volumes: Outpatient orthopedic centers are improving access to fast and convenient osteoarthritis treatments without long hospital stays. In October 2025, Hospital for Special Surgery and General Atlantic created a nationwide outpatient care network to improve accessibility to orthopedic and spinal care using outpatient surgery centers throughout the country. These surgery centers provide image-guided injections, rehabilitation assistance, and day-of-discharge care. Such developments have opened up avenues for injectable therapy companies and specialty clinics.

Segmental Insights

This report offers detailed coverage of the osteoarthritis injectable market injectable type, anatomy, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Injectable Type

-

Hyaluronic Acid Injections

The hyaluronic acid injections segment was dominant by 39.7% revenue share in 2025 due to strong usage in knee osteoarthritis treatment for pain relief and joint lubrication. For instance, in July 2024, LG Chem announced that its partner Yifan Pharmaceutical launched Synovian, LG Chem’s single-injection osteoarthritis treatment in China. Wide physician acceptance and repeat treatment demand supported segment growth. Favorable product availability across major markets is increasing adoption.

-

Platelet-rich Plasma (PRP) Injections

The PRP injections market is anticipated to show rapid at CAGR of 7.8% growth during the forecast period owing to rising demand for regenerative therapies and non-surgical joint care solutions. Growing patient awareness is supporting adoption. Expanding sports medicine applications are aiding fast segment growth.

By Anatomy

-

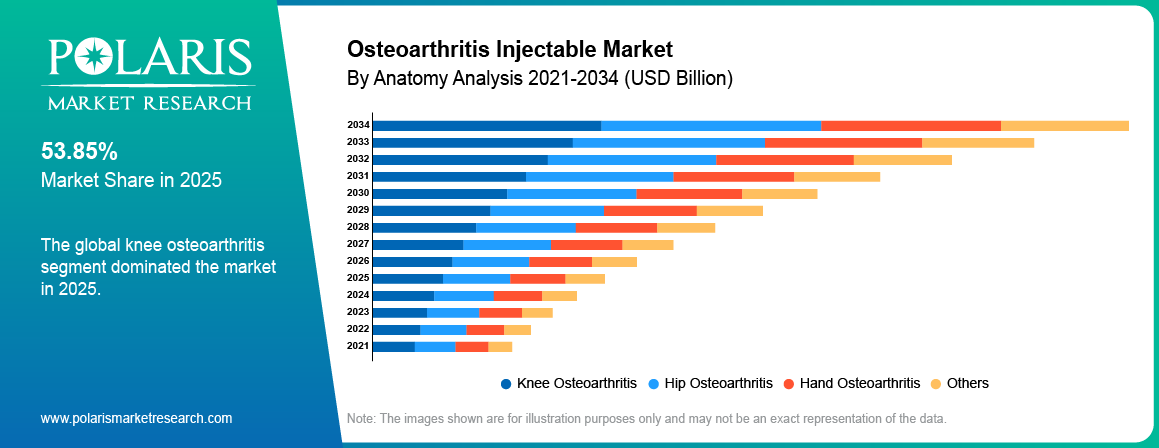

Knee Osteoarthritis

Knee Osteoarthritis segment held 53.85% of total market in 2025 due to the high global prevalence of knee joint degeneration and rising obesity-related joint stress. Strong demand for injectable pain management supported segment growth. Increasing aging population is driving treatment volumes.

-

Hip Osteoarthritis

Hip Osteoarthritis segment is expected to grow at the highest CAGR during the forecast period owing to rising diagnosis rates and growing preference for early non-surgical intervention. Improving imaging-guided injection procedures is supporting adoption. Higher mobility care demand is aiding growth.

By End User

-

Hospital Pharmacies

The hospital pharmacies segment dominated in 2025 with 48.5% revenue share due to strong availability of advanced imaging systems, skilled surgeons, and hybrid operating rooms. Higher patient admissions supported segment demand. Large hospitals remain key centers for complex procedures.

-

Retail Pharmacies

Specialized cardiac centers segment is expected to grow at the highest CAGR during the forecast period owing to rising demand for focused cardiac care and faster treatment pathways. Increasing specialist expertise is supporting adoption. Better patient outcomes are aiding segment growth.

Regional Analysis

North America Osteoarthritis Injectable Market Overview

North America dominated the market by 51.74% market share owing to its high number of patients suffering from osteoarthritis, developed orthopedic medical system, and high acceptance of pain injections therapy. In July 2025, Johnson & Johnson made an announcement regarding their strategic alliance with Pacira BioSciences that aims to provide more patients with ZILRETTA, which is a non-surgical pain injection therapy for knee osteoarthritis. In addition, the US was at the forefront of this region owing to its sizable aging population.

Asia Pacific Osteoarthritis Injectable Market Insights

Asia Pacific is the fastest-growing region in the market, growing at a CAGR of 7.7% during the forecast period due to rising elderly population and improving access to orthopedic care in China, India, Japan, and South Korea. For instance, in February 2025, Seikagaku Corporation has initiated Phase III clinical trials for Gel-One, a treatment for osteoarthritis in the knee and hip regions, in Japan. Since Japan is one of the prominent markets in the region owing to extensive use of hyaluronic acid injections and efficient musculoskeletal care systems.

Europe Market Insights

Europe holds a substantial market share owing to efficient healthcare facilities and increasing demand for non-invasive treatments for osteoarthritis. Countries such as Germany, France, Italy, and the UK are major markets supported by growing elderly populations and increasing mobility care needs. According to Eurostat, the EU population reached 450.6 million in January 2025, and 22.0% of people were aged 65 years and above.Eurostat, 'Population Structure and Ageing', ec.europa.eu Presence of established orthopedic clinics and favorable treatment awareness are supporting market growth.

Competitive Landscape & Key Players

Osteoarthritis injectables industry fragmentation falls between moderate and highly fragmented, as it involves stiff competition between pharmaceutical firms, biotechnology companies, medical devices firms, and others. Competitive factors include effectiveness, safety, approval, doctors' preferences, and price. The increase in regenerative injections offered by companies, collaborations with clinics, distribution channels, and regional coverage are some approaches are adopted to improve competitive positions.

Among the major companies operating in this industry are Sanofi S.A., Bioventus Inc., Fidia Farmaceutici S.p.A., Ferring Pharmaceuticals A/S, Anika Therapeutics, Inc., Pacira BioSciences, Inc., Paradigm Biopharmaceuticals Ltd., Merck KGaA, Biosplice Therapeutics, Inc., Novartis AG, Smith & Nephew plc, Globus Medical, Inc., and others.

Premium Insights

Shift Toward Regenerative Injectables is Reshaping Market Demand

The trend driving the injectables market for osteoarthritis patients is the move from using treatments that simply relieve pain for shorter periods of time to using regenerative medicines like PRP injections. The patients want treatments that not only enhance their ability to move around but also prolong the time before they undergo joint surgery. The orthopedic surgeons have begun applying PRP injections more frequently in mild to moderate osteoarthritis cases owing to rising demand by patients.

Outpatient Care Expansion is Changing Treatment Delivery Models

The rapid expansion of outpatient orthopedic centers is transforming how osteoarthritis injectable therapies are delivered. Patients prefer faster procedures, shorter waiting times, and lower treatment costs compared with hospital-based care. Ambulatory centers are increasing adoption of image-guided injections and same-day treatment models. This trend is helping providers to have better market access, more repeated treatments, and better growth opportunities.

Key Players

- Anika Therapeutics, Inc.

- Bioventus Inc.

- Biosplice Therapeutics, Inc.

- Ferring Pharmaceuticals A/S

- Fidia Farmaceutici S.p.A.

- Globus Medical, Inc.

- Merck KGaA

- Novartis AG

- Pacira BioSciences, Inc.

- Paradigm Biopharmaceuticals Ltd.

- Sanofi S.A.

- Smith & Nephew plc

Industry Developments

- April 2026: ARPA-H stated that its NITRO program is speeding regenerative osteoarthritis treatments toward human trials to repair joints and reduce joint replacement needs. [source: arpa-h.gov]

- April 2026: Duke University stated that its researchers achieved key preclinical milestones in regenerative osteoarthritis therapy, bringing new joint repair treatments closer to human clinical trials. [source: edwards.com]

Osteoarthritis Injectable Market Segmentation

By Injectable Type Outlook (Revenue, USD Billion, 2021-2034)

- Hyaluronic Acid Injections

- Corticosteroid Injections

- Platelet-rich Plasma (PRP) Injections

- Placental Tissue Matrix (PTM) Injections

- Acetylsalicylic Acid (ASA) Injections

- Others

By Anatomy Outlook (Revenue, USD Billion, 2021-2034)

- Knee Osteoarthritis

- Hip Osteoarthritis

- Hand Osteoarthritis

- Others

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Hospital Pharmacies

- Retail Pharmacies

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Osteoarthritis Injectable Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 8.30 Billion |

| Market Size in 2026 | USD 8.85 Billion |

| Revenue Forecast by 2034 | USD 15.15 Billion |

| CAGR | 7.0% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 8.30 Billion in 2025 and is projected to grow to USD 15.15 Billion by 2034.

North America dominated the market by 51.74% market share due to advanced orthopedic care infrastructure and high adoption of injectable joint pain treatments.

Major applications include treatment of knee osteoarthritis, hip osteoarthritis, hand osteoarthritis, and other degenerative joint conditions.

A few of the key players in the market are Sanofi S.A., Bioventus Inc., Fidia Farmaceutici S.p.A., Ferring Pharmaceuticals A/S, Anika Therapeutics, Inc., Pacira BioSciences, Inc., Paradigm Biopharmaceuticals Ltd., Merck KGaA, Biosplice Therapeutics, Inc., Novartis AG, Smith & Nephew plc, Globus Medical, Inc., and others.

Key drivers include rising osteoarthritis cases, growing elderly population, and increasing preference for non-surgical pain management.

Major demand comes from hospitals, orthopedic clinics, ambulatory care centers, and rehabilitation providers.

The market outlook remains positive due to regenerative therapy innovation, wider outpatient access, and growing awareness of early joint care.

Download Sample Report of Osteoarthritis Injectable Market

Please fill out the form to request a customized copy of the research report.