Overview

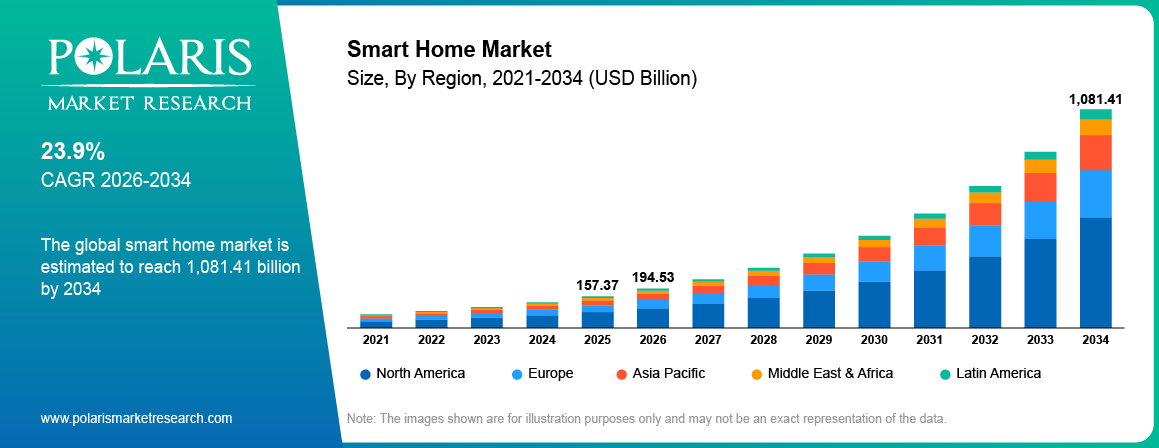

The global smart home market is estimated around USD 157.37 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by increasing demand for energy-efficient homes and IoT smart home technology adoption globally. The market is projected to grow at a CAGR of 23.9% during the forecast period.

Key Takeaways:

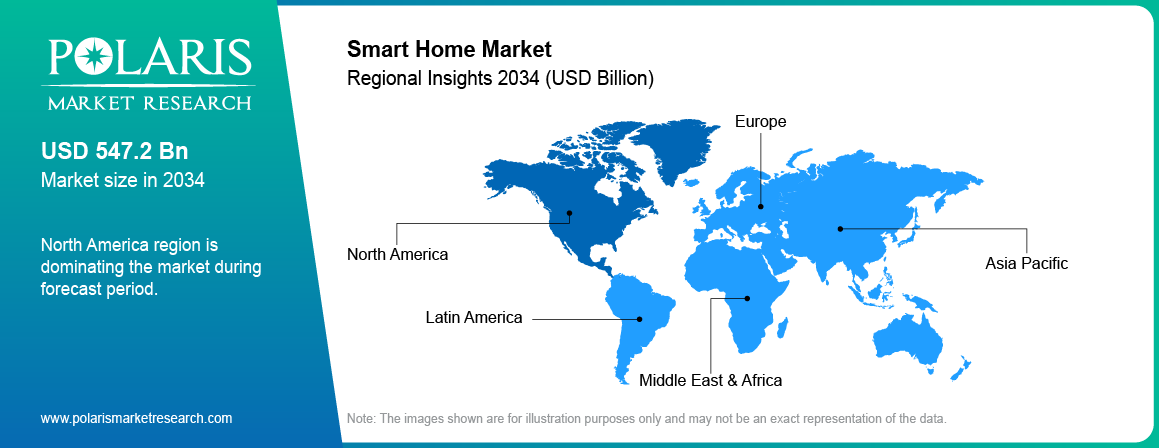

- By Region, North America accounted for the largest market share of around 38% in 2025, driven by early adoption of smart home technologies and strong IoT ecosystem across residential infrastructure.

- By Product, Smart Security Systems segment accounted for the largest market share of around 35% in 2025, driven by rising demand for connected surveillance solutions and smart home security devices.

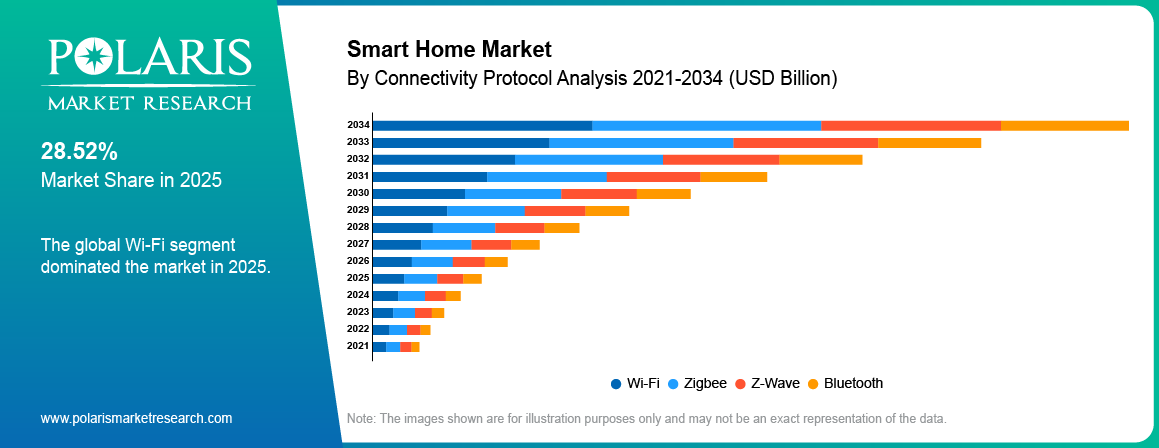

- By Connectivity Protocol, Wi-Fi segment accounted for the largest market share of around 61% in 2025, driven by widespread availability of wireless internet infrastructure and compatibility with most smart home devices.

- By Installation Type, Retrofit Homes segment accounted for the largest market share of around 57% in 2025, driven by increasing adoption of smart home devices in existing residential buildings.

- By Application, Home Security and Surveillance segment accounted for the largest market share of around 42% in 2025, driven by high demand for connected cameras, smart locks, and monitoring systems.

Market Statistics

- 2025 Market Size: USD 157.37 Billion

- 2034 Projected Market Size: USD 1,081.41 Billion

- CAGR (2026-2034): 23.9%

- North America: Largest market in 2025

Industry Dynamics

- Growth of IoT smart home technology is increasing connected home adoption.

- Demand for energy-efficient homes is expanding smart home energy management systems.

- Privacy and cybersecurity concerns limit connected home adoption.

- AI smart homes and next generation smart home systems create long-term opportunities.

What the Smart Home Market Includes?

The smart home industry refers to the structured development and deployment of connected technologies used in residential environments. A connected home integrates multiple digital devices through internet connectivity to enable centralized control of household functions. IoT smart home devices such as sensors, smart hubs, and connected appliances support data exchange and device coordination. Home automation platforms enable users to manage lighting, security, temperature, and appliances through mobile applications or voice assistants. Rising demand for convenience, improved home security, and energy efficiency supports the expansion of connected home technologies.

The smart home market includes smart home security systems, smart lighting solutions, smart HVAC systems, smart appliances, entertainment systems, smart speakers, and energy management systems. These solutions include a combination of IoT devices, wireless technology, cloud technology, and automation software. Smart speakers or home hubs are used as a primary interface for controlling all the devices in a home. Factors like increasing IoT device usage, integration of artificial intelligence technology into IoT devices, and increasing discretionary spending are driving consumer spending on smart home solutions. Increasing usage of smart energy solutions like smart thermostats and energy management systems is also boosting the market.

To Understand More About this Research:Request a Free Sample Report

A connected home is different from a home automation system or a smart home ecosystem. Connected homes are those homes where internet-connected devices are found. Home automation is the automation of a specific home function by schedules or remote control. The smart home ecosystem is the integration of connected devices, home automation systems, artificial intelligence, and data analytics to create a smart home environment. This makes smart homes a technology framework.

Drivers & Opportunities

Growth of IoT ecosystems: The expansion of IoT smart home technology is also a major contributor to the expansion of the smart home industry. This is based on the increased level of communication between smart home devices. In this regard, Samsung Electronics announced in March 2026 that it would be launching Digital Home Key on Samsung Wallet, which would enable users of its technology to access smart door locks using smartphones. The increasing integration of IoT technology into residential infrastructure is contributing to the strengthening of smart home adoption drivers.

Increasing demand for energy-efficient homes: The increasing interest in smart home energy management is driving the need for smart home technology. Smart home devices such as smart thermostats and smart lighting are allowing people to efficiently manage their home electricity consumption. The home automation trend is driving the need for smart home devices that efficiently manage home electricity consumption. The need for smart home technology is driving the growth of IoT smart home technology for residential buildings.

Restraints & Challenges

Privacy and cybersecurity concerns: The risks of privacy are creating cybersecurity concerns that are acting as a barrier for the adoption of smart home technology. The security system of smart home technology collects data from users and transmits information through digital networks. The security framework is also creating concerns that are acting as a barrier for consumers who are considering adopting smart home technology based on IoT technology.

Opportunity

Integration of smart homes with smart city infrastructure: The integration of smart homes and smart cities presents a new opportunity for the connected home world. For instance, in India’s Union Budget 2024-25, a budgetary allocation of 19.67 billion USD was given to the Smart Cities Mission. Out of 8,062 projects, 7,502 were completed by March 2025. Currently, 560 projects are in implementation. Additionally, communication between residential systems and energy grids are facilitated by urban digital infrastructure. Smart home security and smart home energy management are integrated with safety management.

Technology Trends Transforming the Market

|

Technology Trend |

Description |

Market Impact |

|

Matter Interoperability Standard |

Matter enables interoperability between IoT smart home devices from different brands within a connected home ecosystem. |

Improves device compatibility and accelerates smart home adoption drivers. |

|

AI-Enabled Automation |

AI smart home devices automate lighting, security, and appliances through behavioral data analysis. |

Strengthens home automation trends and improves connected home efficiency. |

|

Edge Computing |

Edge computing processes data locally within smart home devices and hubs. |

Reduces latency and improves performance of smart home security systems. |

|

Predictive Home Management Systems |

Predictive systems analyze device and energy data to manage household operations. |

Supports smart home energy management and enhances connected home ecosystem efficiency. |

Segmental Insights

This report offers detailed coverage of the smart home market by technology, material, application, and end use industry to help readers identify the fastest expanding and most attractive demand segments.

By Product

-

Smart Security Systems

Smart security systems dominated the market in terms of revenue share in 2025, driven by rising demand for smart home security systems and connected surveillance solutions. Homeowners are deploying connected cameras, motion sensors, and smart locks to improve residential security within the connected home ecosystem.

-

Smart Lighting

The smart lighting market is expected to grow at the highest rate during the forecast period among all these markets, considering the increasing trend of adopting energy-efficient lighting systems that are integrated into smart home technology through IoT devices. The automated control of lighting is also increasing home convenience through smart home energy management systems.

By Connectivity Protocol

-

Wi-Fi

Wi-Fi dominated the market in terms of revenue share in 2025, driven by widespread availability of wireless internet infrastructure in residential environments. Most IoT smart home devices rely on Wi-Fi networks to support real-time connectivity and device control.

-

Zigbee

The Zigbee segment is projected to grow at the fastest CAGR during the forecast period, due to increasing adoption of low-power communication protocols for connected home devices. Zigbee networks support stable connectivity across multiple IoT smart home technology platforms.

By Installation Type

-

Retrofit Homes

Retrofit homes dominated the market in terms of revenue share in 2025, driven by increasing installation of IoT smart home devices in existing residential buildings. Homeowners are retrofitting conventional living spaces with smart home security systems, lighting systems, and automation systems.

-

New Construction

The new construction segment is projected to grow at the fastest CAGR during the forecast period, due to rising integration of connected home infrastructure in modern residential projects. Real estate builders are integrating smart home technology during building development.

By Application

-

Home Security and Surveillance

Home security/surveillance dominated the market in terms of revenue share in 2025, owing to high demand for connected cameras, locks, and other home security devices that increase safety within the connected home ecosystem.

-

Energy Management

The energy management segment is projected to grow at the fastest CAGR during the forecast period, due to increasing adoption of smart thermostats, energy monitoring systems, and automated climate control solutions that support smart home energy management.

Regional Analysis

North America Market Assessment

North America smart home market dominated in 2025, driven by early technology adoption and a strong IoT ecosystem across residential infrastructure. The increasing rate of smart device adoption and broadband connectivity is fueling the growth of the connected home market in the region. In March 2026, ZTE and Orange Morocco partnered to unveil the Livebox 7 smart home gateway, which is the first prplOS 4.0-based smart home gateway globally to support Wi-Fi 7 connectivity for high-speed internet access. The US and Canada are major markets supported by strong deployment of smart speakers, smart home security systems, and AI smart home devices. This trend is strengthening the smart home market North America and supporting expansion of the global smart home industry.

Asia Pacific Smart Home Market Insights

Asia Pacific smart home market is projected to grow at the fastest CAGR during the forecast period, driven by rapid urbanization and rising middle class population. China, Japan, South Korea, and India are major markets that are expanding deployment of IoT smart home technology and home automation solutions. The increasing number of smartphone users and internet connectivity is driving the adoption of connected home services in urban households. The UN ESCAP found that the Asia Pacific region has an urban population of over 2.2 billion people. The region is also expected to experience an increase of 50% in the coming years to reach 2050.

Europe Smart Home Market Overview

Europe was the second largest market for smart home technology, influenced by energy efficiency regulations and sustainability programs. Smart building integration across residential and commercial infrastructure is increasing demand for smart home energy management systems and connected home devices. Germany, the UK, and France are the major markets for smart home technology, influenced by energy-efficient housing programs and digital building solutions. These developments are strengthening the smart home market Europe within the global smart home industry

Latin America Smart Home Market Outlook

Latin America smart home market is expanding due to growing demand for smart home security systems and urban housing development. Rising concerns related to residential safety are increasing adoption of connected surveillance and smart access control solutions. This trend is supporting connected home adoption across developing urban centers.

Middle East & Africa Smart Home Market Outlook

Middle East & Africa smart home market is growing due to increasing luxury smart home adoption and large-scale smart city projects. In addition, residential schemes in the region are incorporating advanced smart home automation technologies and smart home infrastructure into their developments. For example, Ansarada reported that social infrastructure investments are increasing in the region, with a projected growth trend from USD 1.6 billion in 2024 to USD 2.0 billion in 2027, thus supporting smart home infrastructure in residential developments in the region, which are expanding the smart home market in different regions within the global smart home industry.

Key Players & Competitive Analysis Report

The smart home market competition is driven by leading smart home technology companies and smart home platform providers expanding connected devices and automation platforms. Smart home companies are strengthening the connected home ecosystem through IoT smart home technology, AI smart home devices, and integrated software platforms. Innovation in interoperability and platform integration is increasing the role of smart home ecosystem players in the global smart home industry.

Leading companies in the smart home market are Amazon.com, Inc., Apple Inc., Alphabet Inc., Samsung Electronics Co., Ltd., Honeywell International Inc., Siemens AG, Schneider Electric SE, Johnson Controls International plc, Robert Bosch GmbH, LG Electronics Inc., Panasonic Holdings Corporation, ABB Ltd., and many more.

Future Outlook

- AI smart homes are expected to shape the future of smart homes with intelligent automation for smart lighting, security, and home appliances.

- AI smart home automation is expected to shape the future of smart home technology, enabling the control of smart home ecosystems.

- Next generation smart home systems help to integrate IoT devices, cloud platforms, and advanced analytics for intelligent residential environments.

- Energy-efficient homes increase adoption of smart thermostats, connected appliances, and smart home energy management systems.

- Integration with smart cities are expanding connected home ecosystems through interaction with urban infrastructure and digital energy networks.

Smart home technology trends are expected to create strategic opportunities for smart home device manufacturers, smart home platforms, and smart home ecosystems.

Key Players

- ABB Ltd.

- Alphabet Inc.

- Amazon.com, Inc.

- Apple Inc.

- Honeywell International Inc.

- Johnson Controls International plc

- LG Electronics Inc.

- Panasonic Holdings Corporation

- Robert Bosch GmbH

- Samsung Electronics Co., Ltd.

- Schneider Electric SE

- Siemens AG

Industry Developments

- March 2026: KPower Servo introduced high-performance micro-servo motion technology to enhance automation and precision control in smart home devices.

- March 2026: ABB announced the launch of its System Access Point 3.0 Wireless at Light + Building 2026 to expand its ABB-free@home platform and enable more scalable, secure, and flexible smart home automation.

Smart Home Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021-2034)

- Smart Security Systems

- Smart Lighting

- Smart HVAC

- Smart Appliances

- Smart Speakers

- Entertainment Systems

By Connectivity Protocol Outlook (Revenue, USD Billion, 2021-2034)

- Wi-Fi

- Zigbee

- Z-Wave

- Bluetooth

By Installation Type Outlook (Revenue, USD Billion, 2021-2034)

- New Construction

- Retrofit Homes

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Energy Management

- Home Security and Surveillance

- Lighting Control

- Entertainment Control

- Assisted Devices

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Smart Home Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 157.37 Billion |

|

Market Size in 2026 |

USD 194.53 Billion |

|

Revenue Forecast by 2034 |

USD 1,081.41 Billion |

|

CAGR |

23.9% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 157.37 Billion in 2025 and is projected to grow to USD 1,081.41 Billion by 2034.

North America dominates due to strong IoT ecosystems and high connected device penetration.

Key applications include home security and surveillance, energy management, lighting control, entertainment control, and assisted devices.

A few of the key players in the market are Amazon.com, Inc., Apple Inc., Alphabet Inc., Samsung Electronics Co., Ltd., Honeywell International Inc., Siemens AG, Schneider Electric SE, Johnson Controls International plc, Robert Bosch GmbH, LG Electronics Inc., Panasonic Holdings Corporation, ABB Ltd., and others.

Major smart home adoption drivers include expansion of IoT smart home technology, demand for energy-efficient homes, and growth of AI smart home devices.

Major adoption occurs across residential housing, real estate development, consumer electronics, and home security services.

The future of smart homes is driven by AI smart homes, next generation smart home systems, and connected home ecosystems.

Page last updated on:

Apr-2026

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements