Overview

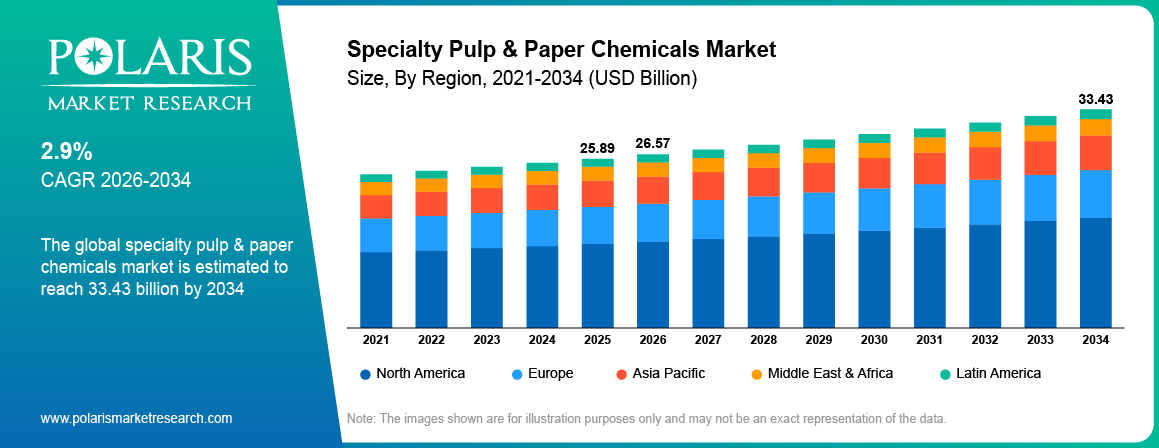

The global specialty pulp & paper chemicals market is estimated around USD 25.89 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by growth in paper packaging production and rising e-commerce packaging demand worldwide. The market is projected to grow at a CAGR of 2.9% during the forecast period.

Key Takeaways:

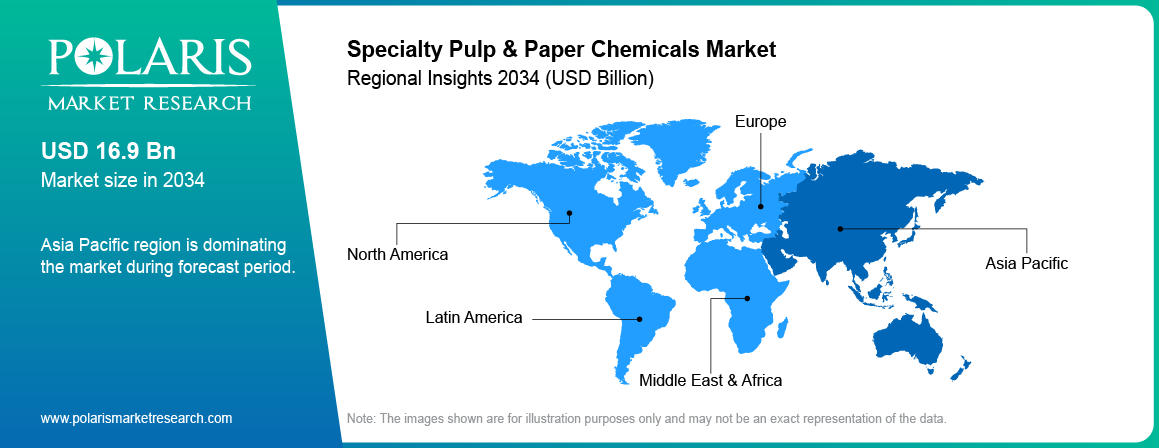

- By Region, Asia Pacific accounted for the largest market share of around 46% in 2025, driven by rapid industrialization and increasing demand for packaging materials across China and India.

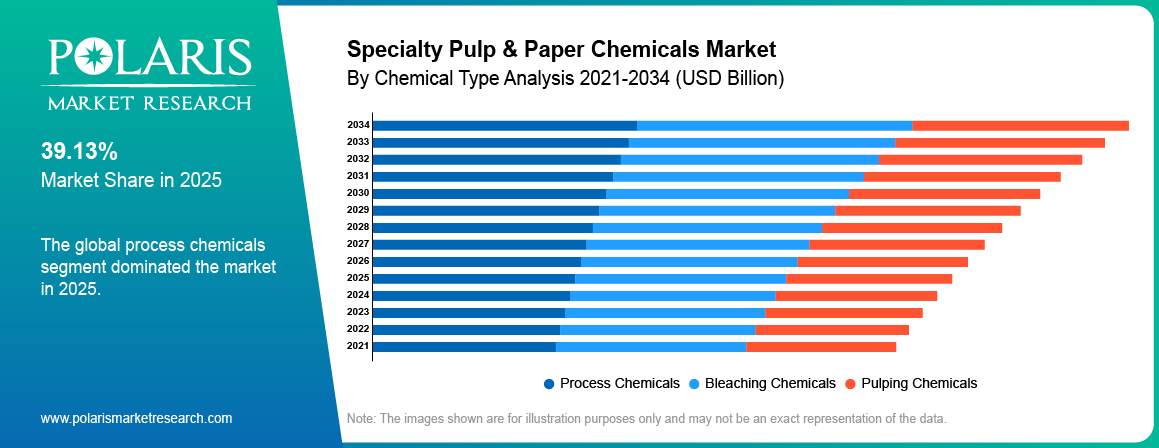

- By Chemical Type, Process Chemicals segment accounted for the largest market share of around 58% in 2025, driven by high demand for efficient pulp processing and increasing production of recycled paper.

- By Application, Packaging segment accounted for the largest market share of around 64% in 2025, driven by rising demand for packaging materials in e-commerce and logistics industries.

Market Statistics

- 2025 Market Size: USD 25.89 Billion

- 2034 Projected Market Size: USD 33.43 Billion

- CAGR (2026-2034): 2.9%

- Asia Pacific: Largest market in 2025

Industry Dynamics

- The growth of paper packaging materials also creates a demand for pulp and paper chemicals used for packaging materials.

- The growth of e-commerce packaging also increases the demand for corrugated boxes and paper packaging materials.

- Environmental regulations related to chemical use also pose challenges for chemical manufacturers.

- Sustainable pulp chemical innovations create long term opportunities in the pulp and paper chemicals market.

What Are Specialty Pulp & Paper Chemicals?

The specialty pulp & paper chemicals market refers to the production and application of chemical formulations used to improve pulp processing and paper manufacturing performance. Specialty chemicals differ from commodity pulp and paper chemicals. Commodity chemicals perform basic processing tasks, while specialty chemicals in the paper industry provide targeted functional benefits that improve product quality and operational efficiency. These chemicals support fiber treatment, sheet formation, and surface performance across printing paper, packaging paper, tissue, and specialty paper grades.

The specialty paper chemicals market includes a wide range of pulp chemical additives used during different stages of paper production. These chemicals fall into two groups. Functional paper chemicals enhance the final properties of paper products. Process chemicals for paper manufacturing improve machine performance and production stability. Common products include retention aids, sizing agents, bleaching chemicals, coating binders, wet strength resins, dry strength additives, and defoamers. Manufacturers use these chemicals to optimize fiber bonding, control water retention, and improve sheet formation during the papermaking process.

To Understand More About this Research:Request a Free Sample Report

Specialty chemicals play an important role in modern pulp and paper manufacturing operations. These pulp and paper chemicals help improve paper strength, enhance printability, and increase production efficiency on high-speed paper machines. Chemical additives also support recyclability by improving fiber recovery and reducing process contamination. Furthermore, specialty chemicals are used to prevent pitch deposits and foaming in pulp processing equipment. The continuous innovation of products and increasing demand for performance-based paper products also fuel the growth of the specialty pulp & paper chemicals market for paper manufacturing industries worldwide.

Drivers & Opportunities

Growth in paper packaging production: Paper packaging products are in demand in food delivery, consumer products, and retail distribution industries. Companies are increasing production capacity for corrugated boxes, paper bags, and paper-based protective packaging materials. In March 2025, Kemira, a leading chemicals company, declared that it will expand its production capacity for paper and board chemicals in Thailand to meet growing demand from the regional packaging industry.

Rising e-commerce packaging demand: E-commerce businesses are fueling demand for corrugated shipping boxes and paper-based packaging materials. E-commerce companies need a high volume of paper packaging materials for their shipping operations. Companies are increasing production capacity for paperboard and corrugated materials to meet demand for shipping boxes. This trend will boost demand for paper processing chemicals, which are used to enhance strength, moisture resistance, and printability in paper packaging materials.

Restraints & Challenges

Environmental regulations on chemical usage: There are environmental regulations for chemicals used in the processing of pulp, as well as waste management for packaging materials. The European and North American governments have enforced strict regulations for the discharge of wastewater and the use of chemicals for the production of paper. This puts pressure on the paper industry to invest in the production of chemicals that are compatible with the regulations. This increases the cost of production for the industry, thereby slowing the use of new chemical additives.

Opportunity

Bio-based chemicals and recycled fiber innovation: There is sustainability pressure on the use of recycled fibers for the production of paper packaging. The production of paper requires the use of special chemicals for the deinking, treatment, and strength of the recycled fibers. The chemicals used for the production of recycled fibers are derived from natural sources. For instance, in January 2026, Valmet launched its new Bioneer press roll covers made from recycled materials and bio-based materials. The product was launched for the purpose of reducing the use of fossil resources as well as carbon emissions for the production of pulp and paper. The product is compatible with digital printing applications.

Emerging Trends

PFAS free coatings and biodegradable chemicals: Increasing sustainability demands are leading to the requirement for PFAS free coatings and biodegradable paper chemicals. There is a rise in the use of sustainable paper chemicals and eco-friendly pulp chemicals for packaging materials. This is to ensure that regulatory requirements are met. There is an introduction of bio-based paper additives that enhance barrier properties for recyclability in paper-based packaging materials.

AI driven paper manufacturing optimization: There is an increasing use of AI-based manufacturing systems for optimizing the efficiency of pulp processing in paper mills. This helps to ensure the monitoring of chemical usage in the paper industry. Paper industry chemical innovations help to ensure the reduction of costs while improving product quality.

Circular economy initiatives and recycled fiber processing: The use of recycled fibers is becoming more prominent through the initiatives taken to promote the circular economy. Paper mills need pulp and paper chemicals to facilitate the recycled pulp production process. This increases the pulp and paper chemicals market trend. This increases the demand for pulp and paper chemicals used to produce recycled paper products.

Segmental Insights

This report offers detailed coverage of the specialty pulp & paper chemicals market by technology, material, application, and end use industry to help readers identify the fastest expanding and most attractive demand segments.

By Chemical Type

-

Process Chemicals

The pulp and paper chemicals market accounted for the largest market share in 2025. This is due to the high demand for efficient pulp processing. Paper mills use pulp and paper chemicals to treat fibers, control deposits, and enhance machine performance. The increasing production of paper packaging products and recycled fibers increases the demand for pulp and paper chemicals to produce recycled papers.

-

Bleaching Chemicals

Bleaching chemicals segment is expected to register the highest CAGR during the forecast period. This is due to the increasing demand for high brightness paper products, which are achieved through the use of modern bleaching chemicals for the production of pulp. This is expected to drive the eco-friendly pulp chemicals used for the production of paper products.

By Application

-

Packaging

Packaging segment held the highest share in the market in 2025. This is due to the increasing demand for packaging materials used for e-commerce logistics. With the rise of e-commerce, the demand for packaging materials, which are made from pulp and paper chemicals, is increasing. The use of corrugated boxes, bags, and packaging materials for shipping purposes requires the use of chemical additives for better quality.

-

Printing

Printing segment is expected to register the fastest CAGR during the forecast period, driven by the growing adoption of digital printing technologies in packaging and labeling. Paper manufacturers require specialized coatings and additives to support high quality print performance. Rising demand for printed packaging and branded labels increases demand for advanced paper chemicals.

Regional Analysis

Asia Pacific Market Assessment

Asia Pacific pulp chemicals market accounts for the largest share due to rapid industrialization and strong packaging demand. For instance, in January 2026, according to data released by the National Bureau of Statistics (NBS) shows that China’s industrial output increased by 5.2% year-on-year in December 2025. The pulp production capacity in China and India is increasing for supporting the growth in paper and paperboard packaging and corrugated packaging materials. This improves the Asia Pacific pulp chemicals market and raises the demand for process chemicals used in pulp production.

North America Specialty Pulp & Paper Chemicals Market Insights

North America specialty pulp & paper chemicals market is projected to grow at the fastest CAGR during the forecast period, driven by rising demand for sustainable packaging in the US and Canada. Packaging producers are adopting North America specialty paper chemicals to improve paper strength and print quality. Regulatory compliance for chemical usage also raises the demand for eco-friendly pulp chemicals in regional paper mills.

Europe Specialty Pulp & Paper Chemicals Market Overview

Europe was the second-largest market for specialty pulp & paper chemicals, with a focus on environmental regulations and circular economy projects. The European Union has a range of policies, including REACH and the chemicals strategy for sustainability, which are designed to ensure the safe use of chemicals, protect human health, and protect the environment. There are 40 laws governing chemicals within the EU, with 90% of Europeans concerned about the environmental impact of chemicals, as well as 84% concerned about health risks from chemicals used within everyday products. Recycled fibers are increasing within Germany, France, and the UK, which is a positive trend for the use of eco-friendly chemicals within the industry.

Key Players & Competitive Analysis Report

The pulp and paper chemicals market shows a moderately consolidated structure dominated by large global chemical companies. Major players are focusing on strategic positioning in terms of specialty chemicals for packaging, printing, and pulp processing. Organizations are investing more in innovation in terms of sustainable paper chemicals, eco-friendly pulp chemicals, and bio-based paper additives for recyclable packaging and recyclable fibers. Partnerships with paper mills, sustainability, and acquisitions are major strategies for expanding their market presence and enhancing their chemical offerings.

Leading companies in the specialty pulp & paper chemicals market are BASF SE, Kemira Oyj, Solenis LLC, Ecolab Inc., Nouryon, Buckman Laboratories International Inc., SNF Group, Ashland Inc., Clariant AG, Arkema S.A., Kurita Water Industries Ltd., Evonik Industries AG, and many more.

Future Outlook

The pulp and paper chemicals market outlook remains strong through 2034 due to rising investment in packaging grade paper production and recycled fiber processing. Process chemicals and advanced bleaching chemicals are considered major investment pockets, as these are widely used in pulp processing and paper manufacturing. In addition, the growing demand for sustainable packaging is expanding the market for specialty paper chemicals in global paper mills.

The sustainability transformation in the paper sector is speeding up the development of sustainable pulp chemical innovation and bio-based paper additives. There is an increasing focus by manufacturers on investing in sustainable pulp chemical products that are recycled and offer efficient pulp treatment solutions. The specialty paper chemical future trends also include new technologies such as AI-based paper manufacturing optimization and chemical formulations for digital printing.

Key Players

- Arkema S.A.

- Ashland Inc.

- BASF SE

- Buckman Laboratories International Inc.

- Clariant AG

- Ecolab Inc.

- Evonik Industries AG

- Kemira Oyj

- Kurita Water Industries Ltd.

- Nouryon

- SNF Group

- Solenis LLC

Industry Developments

- December 2025: Huatai Group launched a USD 2.33 billion integrated forest-pulp-paper project in Guangxi, China, designed to produce about 1.9 million tons of pulp and paper annually.

- May 2025: Axchem Solutions launched a new paper chemical manufacturing plant in Visakhapatnam, India to locally produce additives and specialty formulations for the pulp and paper industry and reduce import dependence.

Specialty Pulp & Paper Chemicals Market Segmentation

By Chemical Type Outlook (Revenue, USD Billion, 2021-2034)

- Process Chemicals

- Bleaching Chemicals

- Pulping Chemicals

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Printing

- Packaging

- Labeling

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Specialty Pulp & Paper Chemicals Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 25.89 Billion |

|

Market Size in 2026 |

USD 26.57 Billion |

|

Revenue Forecast by 2034 |

USD 33.43 Billion |

|

CAGR |

2.9% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 25.89 Billion in 2025 and is projected to grow to USD 33.43 Billion by 2034.

Asia Pacific dominated the market due to large scale pulp production, strong packaging demand, and expansion of paper manufacturing

Major applications include packaging, printing, labeling, and other paper processing activities across paper and packaging industries.

A few of the key players in the market are BASF SE, Kemira Oyj, Solenis LLC, Ecolab Inc., Nouryon, Buckman Laboratories International Inc., SNF Group, Ashland Inc., Clariant AG, Arkema S.A., Kurita Water Industries Ltd., Evonik Industries AG, and others.

Key drivers include growth in paper packaging demand, expansion of e-commerce packaging, and rising use of recycled fiber in paper production.

Major industries include packaging, printing, consumer goods packaging, labeling, and commercial paper manufacturing.

The specialty pulp & paper chemicals market outlook remains strong due to sustainable packaging demand, bio based chemical innovation, and increasing recycled fiber processing.

Page last updated on:

Apr-2026

Research Methodology | Polaris Market Research

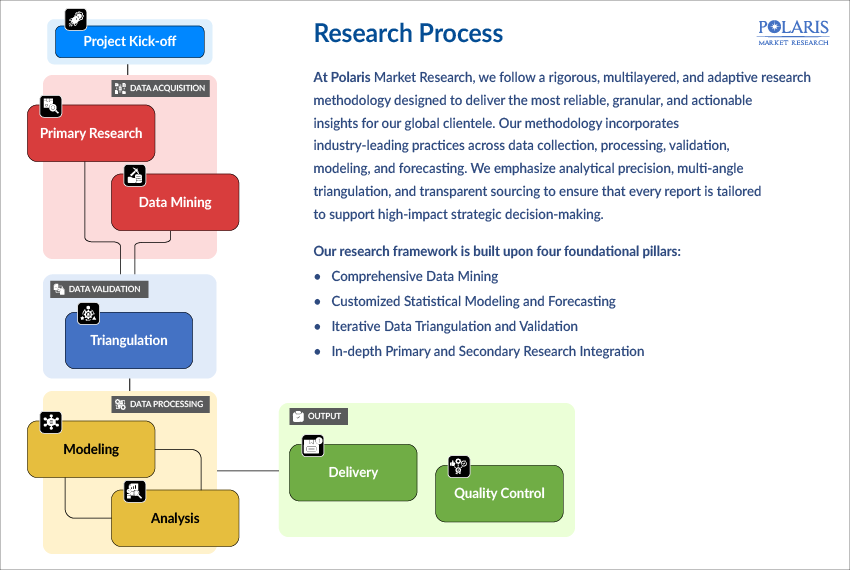

1. Comprehensive Data Mining

Our research journey begins with extensive data mining to construct a reliable and expansive data foundation. We leverage both historical and real-time data sourced from:

- Verified proprietary databases and paid subscription platforms

- Company websites, SEC filings, product literature, and investor presentations

- Industry association publications and trade consortium reports

- Government databases and policy/regulatory repositories

- Reputable media, trade journals, white papers, and academic publications

This multi-source data architecture enables us to map the entire market ecosystem—spanning supply chains, regulatory frameworks, technological advancements, consumer behavior patterns, and emerging industry disruptors. We employ whitespace analysis, IP trend tracking, and patent landscape assessments (where applicable) to identify innovation zones and strategic whitespace opportunities.

2. Customized Statistical Modeling and Forecasting

Our market estimates and forecasts are derived from proprietary statistical models that are specifically designed for each research study. These models integrate:

- Econometric modeling for short-term forecasting (1–3 years)

- Technology lifecycle models for long-term projections (4–10 years)

- Time series analysis, correlation/regression modeling, and scenario-based simulation

Each model incorporates macroeconomic indicators, industry-specific growth drivers, technological evolution, demand elasticity, pricing shifts, and competitive intensity.

Key forecasting parameters include:

- Market drivers and restraints with real-time weight assignment

- Raw material supply-demand dynamics and pricing volatility

- Technological adoption curves and disruption patterns

- Regional capacity utilization and production additions

- Regulatory impact modeling and policy change scenarios

We follow both bottom-up and top-down estimation approaches. The bottom-up approach ensures granularity from regional and segmental perspectives, whereas the top-down approach allows consistency with broader industry indicators.

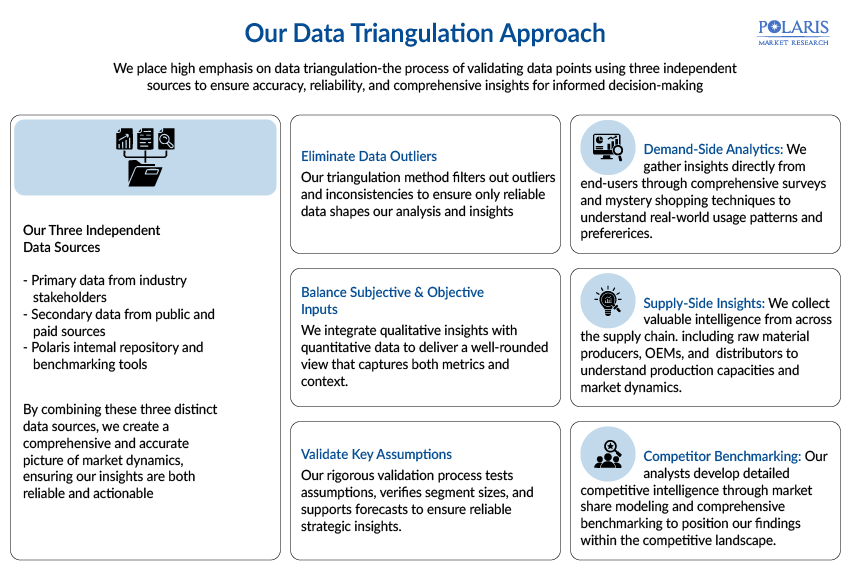

3. Iterative Data Triangulation and Validation

4. Primary and Secondary Research Integration

We combine secondary research data with real-time primary validation to enhance the credibility of data. Secondary research is used to shape the market structure and identify data gaps, while primary research is used to refine, verify, and fill those gaps.

Secondary Research Includes:

Global, regional, and country-level market data are collected from the following sources:

- Government and regulatory bodies (e.g., WHO, FDA, WTO, EPA)

- Corporate financial statements, annual reports, and press releases

- International trade databases and customs records

- Historical trends from previous Polaris studies

Primary Research is Conducted Via:

- Telephonic and virtual in-depth interviews

- One-on-one meetings with key opinion leaders (KOLs)

- Focus group discussions with domain experts

- Surveys targeting end users, distributors, R&D heads, and supply chain executives

Key Industry Participants (KIPs) or Key Opinion Leaders (KOLs) Engaged:

- C-level executives and decision-makers

- R&D leaders and innovation officers

- Procurement and strategy managers

- End users and channel partners

Interviews with Industry Leaders Help us:

- Validate forecast assumptions

- Understand real-time market dynamics

- Identify new opportunity zones and customer pain points

- Cross-check supply-demand gaps and pricing models

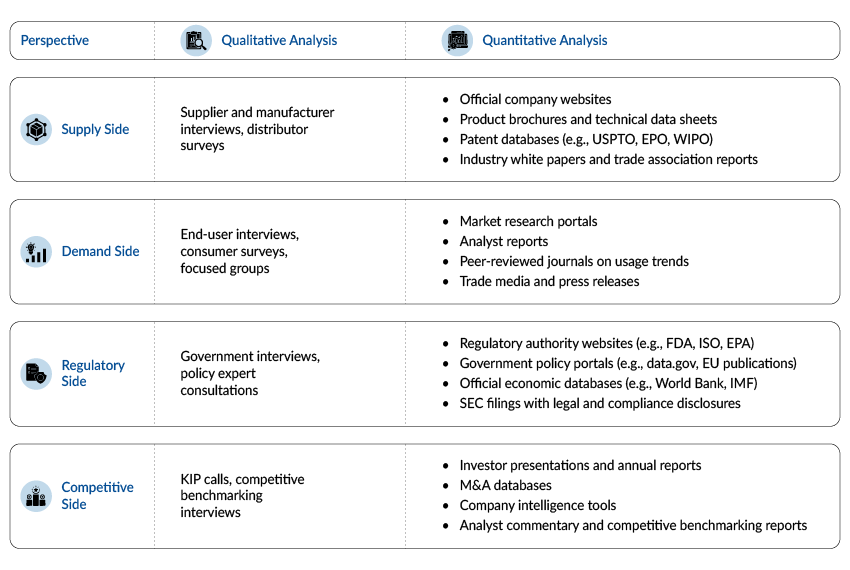

5. Data Collection Matrix

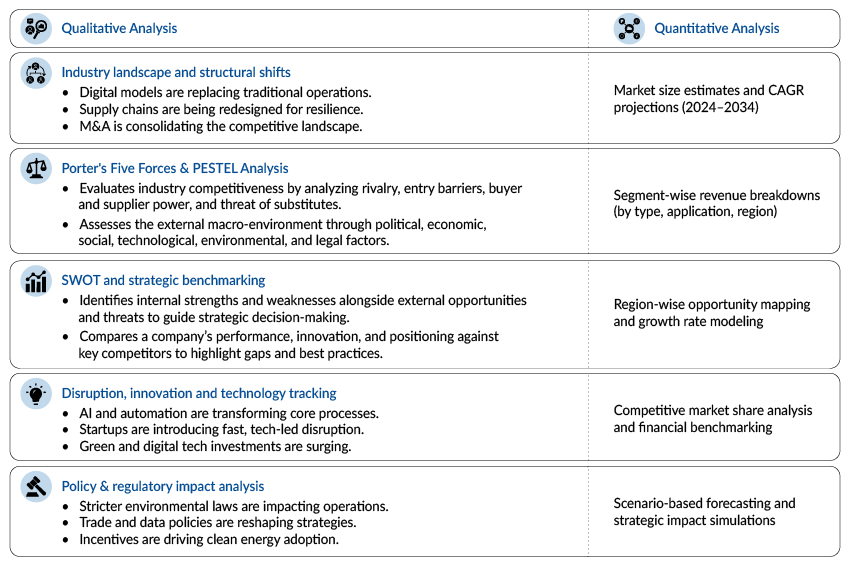

6. Industry Analysis Matrix

7. Reporting and Customization

All Polaris reports are:

- Delivered with interactive Excel datasets

- Supplemented with customizable dashboards and graphs

- Built for cross-segmental filtering and KPIs monitoring

- Supported with analyst consultation on request

We also offer bespoke research solutions based on:

- Country-specific opportunity assessments

- Entry strategy evaluation

- New product launch planning

- Competitive intelligence deep dives

8. Final Quality Check and Continuous Validation

Before publishing, each report undergoes a multi-step review process:

- Editorial and peer-review quality checks for relevance and consistency

- Methodology audit for logic and traceability

- Re-validation through short-cycle expert calls, where needed

After delivering the research report, Polaris continues to monitor emerging trends and provides updates or flash reports on critical market shifts, which enhance clients' strategies.

Polaris Market Research is committed to delivering best-in-class research supported by structured methodology, real-world insights, and domain depth. Our iterative, triangulated, and stakeholder-validated approach ensures that each report offers more than just numbers—it delivers foresight, clarity, and strategic impact. Our goal is to empower decision makers with accurate data, as well as timely and transformative insights that align with evolving market realities.