Structural Heart Procedures Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

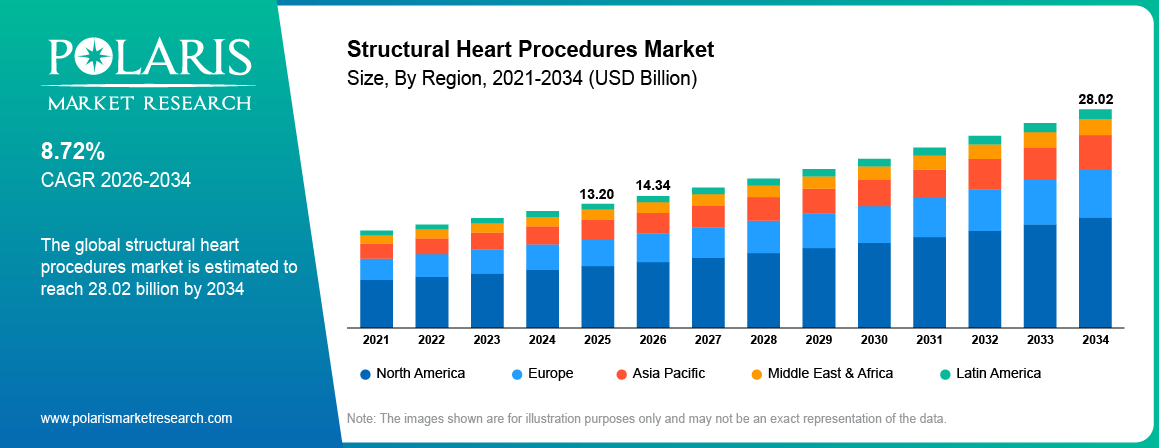

Structural Heart Procedures Market Summary

The global structural heart procedures market is estimated around USD 13.20 Billion in 2025,with consistent growth anticipated during 2026–2034. This growth is driven by rising valvular heart disease burden and growing elderly population that are increasing demand for structural heart procedures across global markets. The market is projected to grow at a CAGR of 8.72% during the forecast period.

Market Statistics

Key Takeaways

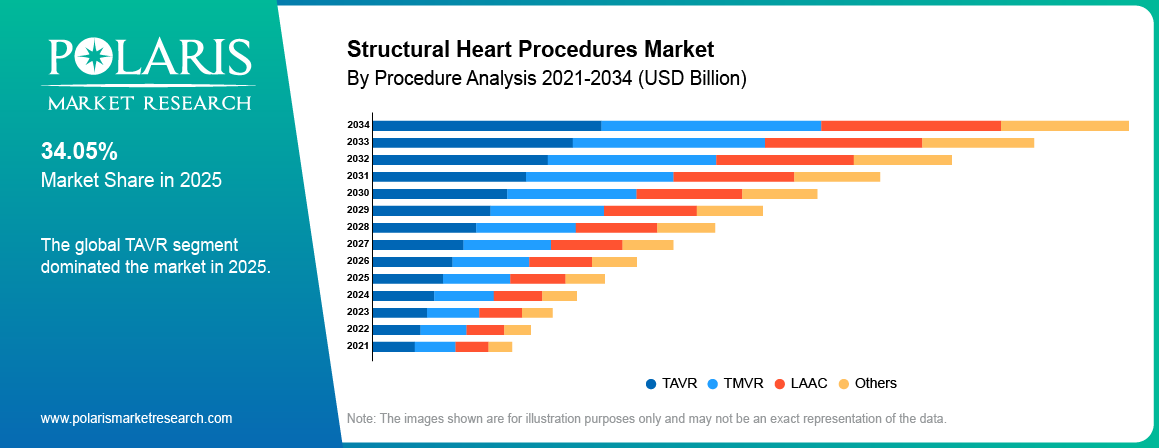

- The TAVR segment was dominant in 2025, accounting for nearly 62.40% market share due to strong adoption of minimally invasive aortic valve replacement procedures.

- The hospitals segment dominated in 2025, contributing approximately 68.70% market share due to advanced cardiac infrastructure and skilled specialists.

- TMVR segment is expected to grow at the highest CAGR, registering around 13.20% during the forecast period owing to increasing cases of mitral valve disorders.

- Tricuspid regurgitation segment is expected to grow at the highest CAGR, registering nearly 12.80% during the forecast period owing to rising awareness of untreated valve disease.

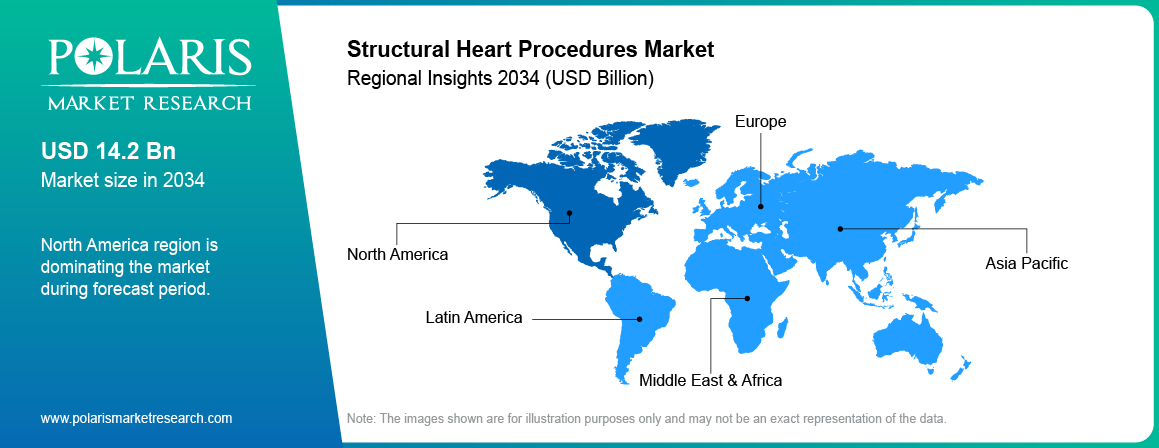

- North America dominated the market, accounting for nearly 41.60% market share in 2025 due to advanced healthcare systems and strong treatment adoption.

Industry Dynamics

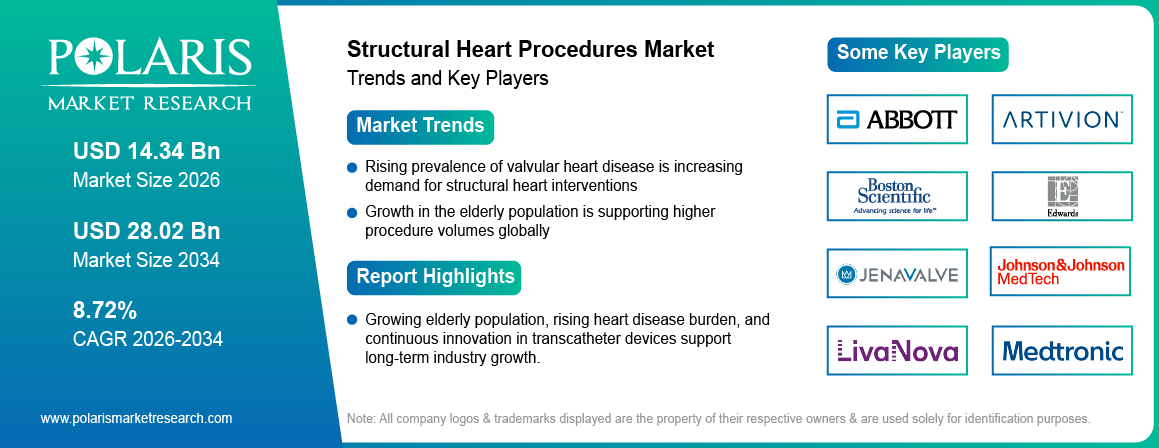

- Rising prevalence of valvular heart disease is increasing demand for structural heart interventions.

- Growth in the elderly population is supporting higher procedure volumes globally.

- High procedure and device costs limit adoption in price-sensitive markets.

- Integration of AI-based imaging tools improve procedural accuracy.

What is Structural Heart Procedures?

Structural heart disease is a field in medicine that involves procedures meant to rectify conditions of the heart valve, wall, and chambers through a process that does not necessitate open heart surgery. Procedures under this field include transcatheter aortic valve replacement, mitral valve repair, left atrial appendage occlusion, and septal defect closure. Growth in this industry is driven by rise in the prevalence of cardiovascular diseases, an aging population, and consumer preference for minimal-invasive surgeries.

The value chain for the structural heart procedures industry consists of design, clinical trials, regulatory approval, procurement by hospitals, surgery planning, surgery implementation, and follow-up after the procedure. The main aim of this industry is to improve patient outcomes, reduce hospital stay, and lower recovery time. Rising investments in advanced cardiac devices, imaging systems, and physician training programs are supporting product adoption. Strong demand from hospitals and specialty cardiac centers is supporting steady market growth.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

Market forces are based on the surgeries performed for valve replacement and repair. With better advancements in catheterization techniques, market needs are shifting toward minimally invasive approaches with quick recovery times. Increasing health care spending, rising disease diagnosis rates, and greater access to heart care are aiding industry development.

Drivers & Opportunities

Rising prevalence of valvular heart disease is increasing demand for structural heart interventions: The increase in incidences of various conditions including aortic stenosis and mitral regurgitation necessitates immediate treatment. According to the American Heart Association, global heart valve disease cases in 2021 reached 54.8 million for rheumatic heart disease, 13.3 million for calcific aortic valve disease, and 15.5 million for degenerative mitral valve disease.The development has been fueling due to increase in healthcare facilities.

Growth in the elderly population is supporting higher procedure volumes globally: The chances of developing heart valve problems increase among older patients owing to the age-related deterioration of valves and reduced strength of the heart muscle. According to the World Health Organization, the number of people in the world aged 60 years and above expected to increase from 1 billion in 2020 to 2.1 billion in 2050.Thus, it is projected to increase in patients requiring surgery on their heart valves.

Restraints & Challenges

High procedure and device costs limit adoption in price-sensitive markets: Structural heart treatment techniques using advanced technology are associated with high costs as they require complicated technological machinery and advanced imaging technologies. Financially, health institutions in underdeveloped countries are unable to afford such costs due to lack of reimbursement programs. Patients experience delay treatment due to affordability concerns. This factor is slowing wider market penetration in cost-sensitive countries.

Opportunity

Integration of AI-based imaging tools improve procedural accuracy: AI in medical imaging systems have been assisting clinicians in understanding anatomy, choosing devices, and designing procedures more accurately. In March 2026, Medtronic announced that its clinician alerts powered by AI had helped them diagnose heart valves better and perform timely intervention procedures on heart valve patients. This helps during transcatheter procedures and avoid planning mistakes. This trend is creating growth opportunities for technology providers and hospitals.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report offers detailed coverage of the structural heart procedures market procedure, indication, and end user to help readers identify the fastest expanding and most attractive demand segments.

By Procedure

-

TAVR

The TAVR segment was dominant in 2025, accounting for nearly 62.40% market share due to rising adoption of minimally invasive valve replacement procedures for aortic stenosis treatment. In October 2025, Medtronic launched the Stedi Extra Support Guidewire to improve performance and procedural support for its TAVR systems. Strong clinical outcomes and shorter recovery time supported segment growth. Expanding approvals for broader patient groups are increasing demand.

-

TMVR

TMVR segment is expected to grow at the highest CAGR, registering around 13.20% owing to increasing cases of mitral valve disorders and rising preference for catheter-based repair solutions. Ongoing product innovation is also supporting adoption. Growing high-risk patient demand is aiding fast segment growth.

By Indication

-

Aortic Stenosis

Aortic stenosis segment was dominating the market in 2025 due to high disease prevalence among elderly patients and strong use of valve replacement procedures. Rising diagnosis rates supported segment expansion. Better screening programs are increasing treatment volumes.

-

Tricuspid Regurgitation

Tricuspid regurgitation segment is expected to grow at the highest CAGR, registering nearly 12.80% during the forecast period owing to rising awareness of untreated valve disease and new transcatheter treatment options. Increasing clinical focus is supporting demand. Expanding innovation is aiding growth.

By End User

-

Hospitals

The hospitals segment dominated in 2025, contributing approximately 68.70% market share due to strong availability of advanced imaging systems, skilled surgeons, and hybrid operating rooms. Higher patient admissions supported segment demand. Large hospitals remain key centers for complex procedures.

-

Specialized Cardiac Centers

Specialized cardiac centers segment is expected to grow at the highest CAGR during the forecast period owing to rising demand for focused cardiac care and faster treatment pathways. Increasing specialist expertise is supporting adoption. Better patient outcomes are aiding segment growth.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

North America Structural Heart Procedures Market Overview

North America dominated the market, accounting for nearly 41.60% market share in 2025 due to advanced cardiac care infrastructure, strong adoption of minimally invasive procedures, and high healthcare spending. The US leads the region, supported by a large elderly population and strong presence of leading medical device companies. According to the U.S. Census Bureau, the US population aged 65 and older is projected to rise from 58 million in 2022 to 82 million by 2050, increasing its share of the population from 17% to 23%.

Asia Pacific Structural Heart Procedures Market Insights

Asia Pacific is expected to witness the fastest growth in terms of CAGR during the forecast period due to rising cardiovascular disease burden and improving access to advanced healthcare in China, India, Japan, and South Korea. In February 2026, Medanta Noida launched its structural heart programme after successfully completing its first three TAVI procedures for severe aortic stenosis patients, expanding minimally invasive cardiac care access in Delhi-NCR. Also, growing hospital investments and rising awareness of early heart treatment are supporting demand. China remains a key regional market due to rapid healthcare modernization and growing procedure volumes.

Europe Market Insights

Europe has a considerable market share owing to its robust healthcare facilities and increasing usage of catheterization for cardiac surgeries. According to OECD, cardiovascular disease remains the leading cause of illness and death in the EU, causing one in three deaths, or 1.7 million fatalities in 2022, and affecting around 62 million people.Countries such as Germany, France, and the UK are major markets supported by aging populations and increasing diagnosis of valvular heart disease. The availability of expert cardiac centers is contributing to the development of the procedures.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Landscape & Key Players

The structural heart devices business is moderately concentrated, with competition from international medical device players, cardiac technology firms, and specialty healthcare manufacturers. Innovations in product development, efficacy, regulatory clearance, physician training, and pricing are some of the main competitive areas in the industry. Companies are using portfolio diversification to include transcatheter procedures, using AI-powered imaging technologies, forging hospital collaborations, and expanding geographically.

The following are some of the leading companies in the industry Edwards Lifesciences, Medtronic, Abbott Laboratories, Boston Scientific, Johnson & Johnson MedTech, Meril Life Sciences, LivaNova, Artivion, JenaValve Technology, MicroPort Scientific, Venus Medtech, Peijia Medical, and others.

Premium Insights

AI integration in cardiac imaging: The use of AI in cardiology is leading to better accuracy in diagnoses, treatment options, and procedures related to heart innovations.

Rise of robotic-assisted interventions: Robotic assistance is becoming popular due to better precision in conducting procedures associated with heart innovations.

Increasing outpatient procedures: Outpatient procedures are on the rise owing to the shorter recovery periods involved.

Key Players

- Abbott Laboratories

- Artivion

- Boston Scientific

- Edwards Lifesciences

- JenaValve Technology

- Johnson & Johnson MedTech

- LivaNova

- Medtronic

- Meril Life Sciences

- MicroPort Scientific

- Peijia Medical

- Venus Medtech

Industry Developments

- Nov 2025: Philips introduced an AI-based imaging system that would increase precision and efficiency of transcatheter mitral valve repair procedures. [source: www.philips.com]

- December 2025: Edwards Lifesciences awarded FDA clearance for its SAPIEN M3 system, which is the first transseptal transcatheter mitral valve replacement treatment for severe mitral regurgitation patients ineligible for surgery. [source: www.fiercebiotech.com]

Structural Heart Procedures Market Segmentation

By Procedure Outlook (Revenue, USD Billion, 2021-2034)

- TAVR

- TMVR

- LAAC

- Others

By Indication Outlook (Revenue, USD Billion, 2021-2034)

- Aortic Stenosis

- Mitral Regurgitation

- Congenital Heart Defects

- Atrial Fibrillation

- Tricuspid Regurgitation

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Specialized Cardiac Centers

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Structural Heart Procedures Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 13.20 Billion |

| Market Size in 2026 | USD 14.34 Billion |

| Revenue Forecast by 2034 | USD 28.02 Billion |

| CAGR | 8.72% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Structural Heart Procedures Market FAQ's

The global market size was valued at USD 13.20 Billion in 2025 and is projected to grow to USD 28.02 Billion by 2034.

North America dominated the market due to advanced cardiac care infrastructure and high adoption of minimally invasive heart procedures.

Major applications include treatment of aortic stenosis, mitral regurgitation, atrial fibrillation, congenital heart defects, and tricuspid regurgitation.

A few of the key players in the market are Edwards Lifesciences, Medtronic, Abbott Laboratories, Boston Scientific, Johnson & Johnson MedTech, Meril Life Sciences, LivaNova, Artivion, JenaValve Technology, MicroPort Scientific, Venus Medtech, Peijia Medical, and others.

Key drivers include rising valvular heart disease cases, growing elderly population, and increasing preference for less invasive treatments.

Major demand comes from hospitals, specialized cardiac centers, ambulatory care facilities, and healthcare providers.

The market outlook remains positive due to AI-based imaging tools, product innovation, and wider access to advanced cardiac care.

Download Sample Report of Structural Heart Procedures Market

Please fill out the form to request a customized copy of the research report.