Additive Manufacturing Market Size, Share, Global Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Overview

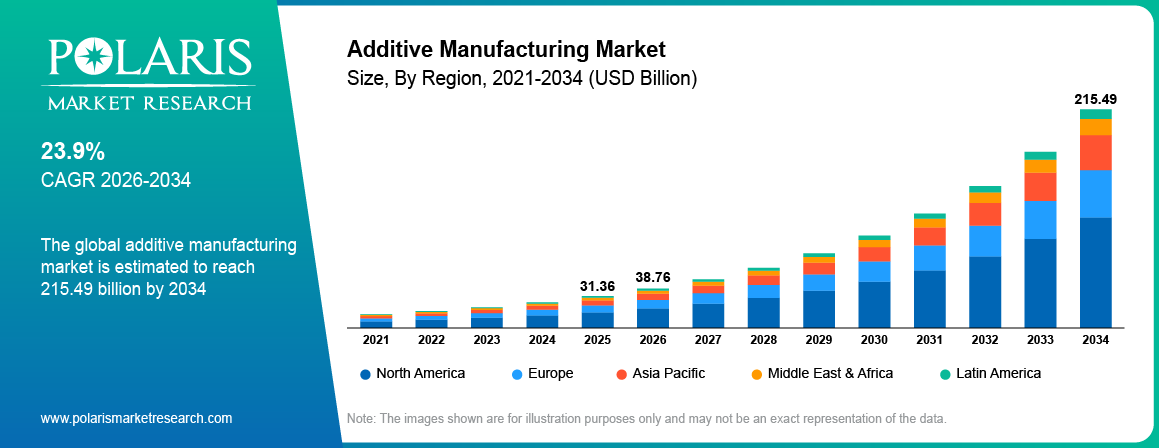

The global additive manufacturing market is estimated around USD 31.36 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rising demand for lightweight components in aerospace and healthcare coupled with increasing demand for rapid prototyping in product development. The market is projected to grow at a CAGR of 23.9% during the forecast period.

Key Takeaways:

- By Region, Asia Pacific accounted for the largest market share of around 44.7% in 2025, driven by strong electronics manufacturing, semiconductor fabrication, and expanding industrial activities across China, Japan, South Korea, and Taiwan.

- By Product Type, Super Abrasives is expected to register a CAGR of 6.9% during the forecast period, driven by increasing demand for precision tools such as diamond and CBN abrasives in electronics and hardened steel applications.

- By Material Type, Aluminum Oxide Abrasives accounted for the largest market share of around 46.3% in 2025, supported by versatility, cost-effectiveness, and widespread use in grinding wheels and finishing tools.

- By Application, Grinding accounted for the largest market share of nearly 61.5% in 2025, supported by extensive usage in metal fabrication, machine tooling, and automotive component manufacturing.

Market Statistics

- 2025 Market Size: USD 31.36 Billion

- 2034 Projected Market Size: USD 215.49 Billion

- CAGR (2026-2034): 23.9%

- North America: Largest market in 2025

Industry Dynamics

- Rising demand for lightweight components in aerospace and healthcare is increasing additive manufacturing adoption.

- Increasing demand for rapid prototyping is expanding industrial 3D printing use in manufacturing.

- High equipment and material costs limit adoption among small and mid-size manufacturers.

- AI driven design and digital manufacturing create long term opportunities in the market.

What is Additive Manufacturing?

The term additive manufacturing industry refers to the organized development and utilization of manufacturing systems that utilize the additive manufacturing technology. Additive manufacturing technology involves the creation of objects from digital data using a variety of materials like polymers, metals, and composites. The market for additive manufacturing technology involves industrial 3D printing systems, design software, printing materials, and post-processing systems that assist in the creation of components for different industries.

The market for additive manufacturing technology involves different kinds of technology like fused deposition modeling, selective laser sintering, stereolithography, binder jetting, and direct metal laser sintering. These are industrial 3D printing systems that utilize different kinds of materials along with design software for creating parts or components from computer-aided design data. The technology is utilized by different manufacturers for creating prototypes, tooling parts, or for creating complex parts on a small scale. The process reduces material waste and supports faster product development cycles in comparison to conventional manufacturing methods.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The additive manufacturing industry differs from traditional manufacturing processes such as machining, casting, and injection molding. Traditional manufacturing removes material from solid blocks or forms parts through molds and tooling. Additive manufacturing involves the production of a product through the layering of digital manufacturing systems, which use minimal tools for production. This concept allows for the customization of products, decentralized production, and decentralized networks. The growth of industrial adoption for additive manufacturing is increasing due to the improvement of production efficiency through innovation in additive manufacturing.

Drivers & Opportunities

Rising demand for lightweight components in aerospace and healthcare: The increasing demand for the production of lightweight components for the aerospace industry and the healthcare industry drives the market. Aerospace companies use the additive manufacturing technology to create lightweight aircraft, which improves the fuel efficiency of the aircraft. Healthcare companies use industrial 3D printing for the production of implants and prosthetics for customers. In January 2026, Hadrian launched a dedicated additive manufacturing division to deliver scalable, production-ready AM capacity and strengthen domestic production for U.S. defense and aerospace programs. This increases the adoption of additive manufacturing for the aerospace industry, which is known as the additive manufacturing aerospace market, and the healthcare industry, which is known as the additive manufacturing healthcare market.

Increasing demand for rapid prototyping in product development: The demand for rapid prototyping is increasing in the automobile industry, consumer electronics, and industrial equipment industries. Additive manufacturing technology helps companies create prototypes from digital data without any tooling requirement. This helps companies reduce product development cycles. This benefits the additive manufacturing technology used in modern industries for manufacturing.

Restraints & Challenges

High equipment and production costs: Cost challenges for the additive manufacturing technology are a major challenge for the industries to adopt the technology. Industrial 3D printing technology involves a high cost for the equipment, materials, and post-processing requirements. Industries face budget challenges for implementing the large-scale additive manufacturing technology. These cost barriers slow additive manufacturing adoption in price sensitive industries.

Opportunity

AI driven design and manufacturing innovation: Additive manufacturing innovation is helping in the development of additive manufacturing market opportunities through innovation in AI-driven design systems. Artificial intelligence is utilized for generative design and production optimization in digital manufacturing systems. For instance, in November 2025, Aibuild announced the opening of its U.S. headquarters in Silicon Valley, located inside Nikon's research facility. The company aims to advance AI-driven automation and collaboration in industrial additive manufacturing.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report offers detailed coverage of the additive manufacturing market by technology, material, application, and end use industry to help readers identify the fastest expanding and most attractive demand segments.

By Technology

-

Fused Deposition Modeling (FDM)

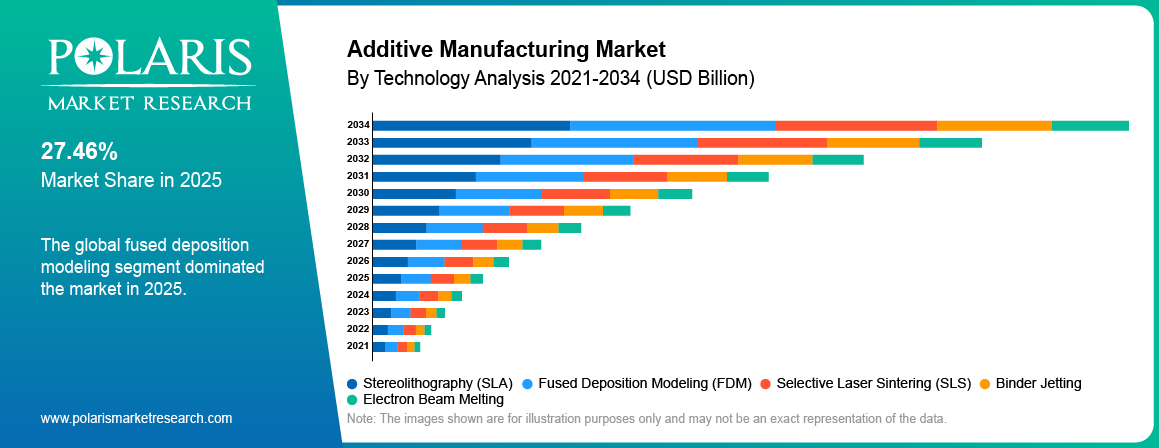

Fused Deposition Modeling dominated the industrial 3D printing technology market in 2025, driven by strong use in prototyping and product development. It provides low equipment cost and ease of operation. FDM systems are used in product testing in manufacturing and research organizations, leading to increased demand for industrial 3D printing technology.

-

Selective Laser Sintering (SLS)

Selective Laser Sintering segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for complex functional components. SLS provides precision production without tooling requirements. Aerospace and automotive industries are adopting SLS for lightweight production.

By Material

-

Polymers

Polymers held major segment share of the additive manufacturing market in 2025, due to the increasing demand for rapid prototyping and product design testing for the manufacturing industry. Additive manufacturing of polymers involves the production of lightweight and cost-effective products. These advantages strengthen the polymer additive manufacturing market across automotive and consumer electronics industries.

-

Metals

Metals segment is projected to grow at the fastest CAGR during the forecast period, due to increasing use of metal additive manufacturing for high strength components. Aerospace and healthcare sectors use metal printing for aircraft parts and medical implants. This trend supports growth of the metal additive manufacturing market.

By Application

-

Prototyping

Prototyping dominated the additive manufacturing market in 2025, driven by increasing demand for rapid production of products. Industrial 3D printing technology offers a business opportunity for the manufacturers to print the prototypes directly from the designs.

-

Functional Parts

Functional parts segment is projected to grow at the fastest CAGR during the forecast period, due to increasing use of additive manufacturing for end use component production. Adoption of additive manufacturing technology is on the rise in the additive manufacturing aerospace, additive manufacturing automotive, and additive manufacturing healthcare industries.

By End Use Industry

-

Aerospace & Defense

The aerospace & defense industry accounted for the largest market size in the additive manufacturing market in 2025. This is due to the high demand for lightweight aircraft parts. Additive manufacturing aerospace helps to reduce waste materials and enables the development of complex components.

-

Healthcare

Healthcare segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for personalized medical devices. Additive manufacturing healthcare applications support customized implants, prosthetics, and additive manufacturing dental products.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

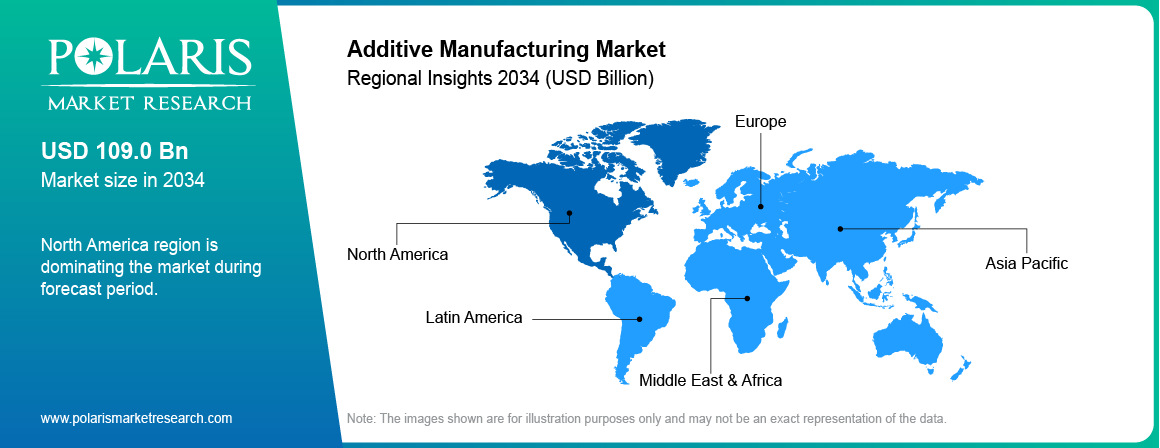

North America Market Assessment

North America additive manufacturing market dominated in 2025, driven by a strong aerospace industry and continuous technological innovation across the US and Canada. Aerospace companies are increasing the adoption of industrial 3D printing technology to produce lightweight aircraft components. For example, in March 2026, GE Aerospace announced a USD 1 billion investment to boost U.S. manufacturing capacity due to high demand for aircraft engines and parts, thus increasing the adoption of innovative production technology such as additive manufacturing technology.

Asia Pacific Additive Manufacturing Market Insights

Asia Pacific additive manufacturing market is expected to grow at the highest CAGR during the forecast period. The growth in the Asia Pacific region is attributed to the high growth rate in manufacturing in China, Japan, and India. Governments in the region are promoting advanced production technologies through industrial modernization programs. For instance, the Reserve Bank of India reported that India’s manufacturing sector is strengthening and may reach USD 1 trillion by FY26, while the country holds potential to contribute over USD 500 billion annually to the global economy by 2030 through expansion as a global manufacturing hub. These developments are strengthening the China additive manufacturing market and the India additive manufacturing market.

Europe Additive Manufacturing Market Overview

Europe was the second largest market for additive manufacturing, driven by strong industrial manufacturing and a large automotive sector. The countries that are using industrial 3D printing technology include Germany, France, and the UK. In March 2026, DN Solutions announced the opening of the first European Additive Solutions Center in Gütersloh, Germany. The main focus is to increase the adoption rate for metal additive manufacturing technology and combine it with CNC machining for industrial production.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The competitive environment for the additive manufacturing market is driven by continuous innovation in industrial 3D printing metals and materials. Companies are expanding the additive manufacturing environment with better machines, software, and materials. Strategic partnerships with aerospace, automotive, and healthcare manufacturers are strengthening additive manufacturing adoption across industrial production.

The key players operating in the additive manufacturing market are Stratasys, 3D Systems, EOS GmbH, GE Additive, HP Inc., Desktop Metal, Markforged, SLM Solutions, Materialise NV, Voxeljet AG, Nikon SLM Solutions, Renishaw plc, and many more.

Premium Insights

Economics of Additive Manufacturing

| Economic Factor | Explanation |

| Cost Drivers | Equipment investment, printing materials, and post-processing operations represent the major cost drivers in the additive manufacturing market. |

| Production Efficiency | Industrial 3D printing reduces tooling costs and minimizes material waste compared with traditional manufacturing methods. |

| Manufacturing Economics | The technology improves cost efficiency for rapid prototyping and low-volume production environments. |

| ROI Advantage | Additive manufacturing technology provides strong return on investment for complex and lightweight component production. |

Source: Polaris Market Research Analysis

Value Chain Analysis

| Value Chain Stage | Process Description |

| Design | Engineers create digital models using computer-aided design software. |

| Printing | Industrial 3D printing systems build components through layer-by-layer material deposition. |

| Post-Processing | Finishing processes include heat treatment, polishing, and structural reinforcement. |

| Quality Control | Inspection and testing verify component accuracy, strength, and performance standards. |

Source: Polaris Market Research Analysis

Decision Framework

| Decision Factor | Commercial Relevance |

| Design Complexity | Additive manufacturing becomes viable for complex geometries that traditional methods cannot easily produce. |

| Production Volume | The technology suits rapid prototyping and low-volume manufacturing where tooling costs remain high. |

| Customization Needs | Industries requiring personalized components benefit from additive manufacturing technology. |

| Supply Chain Flexibility | Digital manufacturing supports decentralized production and faster product development cycles. |

Source: Polaris Market Research Analysis

Industry Case Examples

| Industry | Use Case |

| Aerospace | Additive manufacturing technology produces lightweight aircraft components that improve fuel efficiency. |

| Healthcare | Industrial 3D printing supports customized implants, prosthetics, and dental devices for patient-specific treatments. |

| Automotive | Manufacturers use additive manufacturing applications for rapid prototyping and tooling development. |

| Industrial Manufacturing | The companies are using digital manufacturing systems for creating complex machine parts or spare parts. |

Source: Polaris Market Research Analysis

Key Players

- 3D Systems

- Desktop Metal

- EOS GmbH

- GE Additive

- HP Inc.

- Markforged

- Materialise NV

- Nikon SLM Solutions

- Renishaw plc

- SLM Solutions

- Stratasys

- Voxeljet AG

Industry Developments

- January 2026: 3D Systems has announced investments in expanding its capabilities for additive manufacturing in aerospace and defense industries for large-scale production of 3D-printed parts for aircraft and defense systems.

- October 2025: EOS GmbH has introduced four new metal-based additive manufacturing materials before the Formnext 2025 event for expanding the scope of industrial additive manufacturing for aerospace, energy, automobile, and chemical industries.

Additive Manufacturing Market Segmentation

By Technology Outlook (Revenue, USD Billion, 2021-2034)

- Stereolithography (SLA)

- Fused Deposition Modeling (FDM)

- Selective Laser Sintering (SLS)

- Binder Jetting

- Electron Beam Melting

By Material Outlook (Revenue, USD Billion, 2021-2034)

- Metals

- Polymers

- Ceramics

- Composite

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Prototyping

- Tooling

- Functional Parts

By End Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- Automotive

- Aerospace & Defense

- Healthcare

- Consumer Electronics

- Power & Energy

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Additive Manufacturing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 31.36 Billion |

| Market Size in 2026 | USD 38.76 Billion |

| Revenue Forecast by 2034 | USD 215.49 Billion |

| CAGR | 23.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Additive Manufacturing Market FAQ's

The global market size was valued at USD 31.36 Billion in 2025 and is projected to grow to USD 215.49 Billion by 2034.

North America led due to high aerospace industry demand and capabilities in industrial manufacturing.

The major applications are rapid prototyping, tooling development, and functional parts manufacturing in industrial manufacturing industries.

A few of the key players in the market are Stratasys, 3D Systems, EOS GmbH, GE Additive, HP Inc., Desktop Metal, Markforged, SLM Solutions, Materialise NV, Voxeljet AG, Nikon SLM Solutions, Renishaw plc, and others.

The major drivers are increasing demand for rapid prototyping, lightweight parts manufacturing, and digital manufacturing technology adoption.

The major industries for additive manufacturing are aerospace, healthcare, automotive, consumer products, and industrial manufacturing.

The forecast for the additive manufacturing market looks positive due to the increasing adoption of digital manufacturing, generative design tools, and advanced printing materials.

Download Sample Report of Additive Manufacturing Market

Please fill out the form to request a customized copy of the research report.