Overview

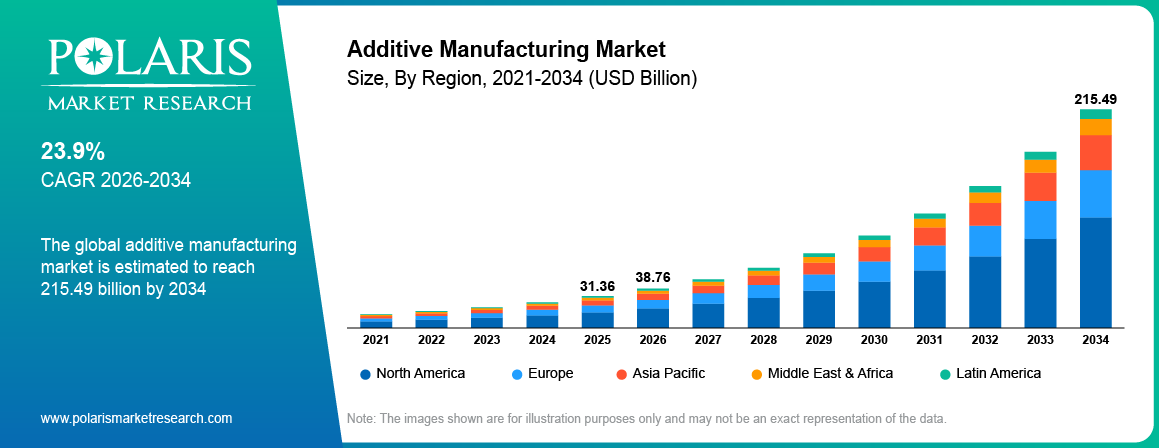

The global additive manufacturing market is estimated around USD 31.36 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rising demand for lightweight components in aerospace and healthcare coupled with increasing demand for rapid prototyping in product development. The market is projected to grow at a CAGR of 23.9% during the forecast period.

Key Takeaways:

- By Region, Asia Pacific accounted for the largest market share of around 44.7% in 2025, driven by strong electronics manufacturing, semiconductor fabrication, and expanding industrial activities across China, Japan, South Korea, and Taiwan.

- By Product Type, Super Abrasives is expected to register a CAGR of 6.9% during the forecast period, driven by increasing demand for precision tools such as diamond and CBN abrasives in electronics and hardened steel applications.

- By Material Type, Aluminum Oxide Abrasives accounted for the largest market share of around 46.3% in 2025, supported by versatility, cost-effectiveness, and widespread use in grinding wheels and finishing tools.

- By Application, Grinding accounted for the largest market share of nearly 61.5% in 2025, supported by extensive usage in metal fabrication, machine tooling, and automotive component manufacturing.

Market Statistics

- 2025 Market Size: USD 31.36 Billion

- 2034 Projected Market Size: USD 215.49 Billion

- CAGR (2026-2034): 23.9%

- North America: Largest market in 2025

Industry Dynamics

- Rising demand for lightweight components in aerospace and healthcare is increasing additive manufacturing adoption.

- Increasing demand for rapid prototyping is expanding industrial 3D printing use in manufacturing.

- High equipment and material costs limit adoption among small and mid-size manufacturers.

- AI driven design and digital manufacturing create long term opportunities in the market.

What is Additive Manufacturing?

The term additive manufacturing industry refers to the organized development and utilization of manufacturing systems that utilize the additive manufacturing technology. Additive manufacturing technology involves the creation of objects from digital data using a variety of materials like polymers, metals, and composites. The market for additive manufacturing technology involves industrial 3D printing systems, design software, printing materials, and post-processing systems that assist in the creation of components for different industries.

The market for additive manufacturing technology involves different kinds of technology like fused deposition modeling, selective laser sintering, stereolithography, binder jetting, and direct metal laser sintering. These are industrial 3D printing systems that utilize different kinds of materials along with design software for creating parts or components from computer-aided design data. The technology is utilized by different manufacturers for creating prototypes, tooling parts, or for creating complex parts on a small scale. The process reduces material waste and supports faster product development cycles in comparison to conventional manufacturing methods.

To Understand More About this Research:Request a Free Sample Report

The additive manufacturing industry differs from traditional manufacturing processes such as machining, casting, and injection molding. Traditional manufacturing removes material from solid blocks or forms parts through molds and tooling. Additive manufacturing involves the production of a product through the layering of digital manufacturing systems, which use minimal tools for production. This concept allows for the customization of products, decentralized production, and decentralized networks. The growth of industrial adoption for additive manufacturing is increasing due to the improvement of production efficiency through innovation in additive manufacturing.

Drivers & Opportunities

Rising demand for lightweight components in aerospace and healthcare: The increasing demand for the production of lightweight components for the aerospace industry and the healthcare industry drives the market. Aerospace companies use the additive manufacturing technology to create lightweight aircraft, which improves the fuel efficiency of the aircraft. Healthcare companies use industrial 3D printing for the production of implants and prosthetics for customers. In January 2026, Hadrian launched a dedicated additive manufacturing division to deliver scalable, production-ready AM capacity and strengthen domestic production for U.S. defense and aerospace programs. This increases the adoption of additive manufacturing for the aerospace industry, which is known as the additive manufacturing aerospace market, and the healthcare industry, which is known as the additive manufacturing healthcare market.

Increasing demand for rapid prototyping in product development: The demand for rapid prototyping is increasing in the automobile industry, consumer electronics, and industrial equipment industries. Additive manufacturing technology helps companies create prototypes from digital data without any tooling requirement. This helps companies reduce product development cycles. This benefits the additive manufacturing technology used in modern industries for manufacturing.

Restraints & Challenges

High equipment and production costs: Cost challenges for the additive manufacturing technology are a major challenge for the industries to adopt the technology. Industrial 3D printing technology involves a high cost for the equipment, materials, and post-processing requirements. Industries face budget challenges for implementing the large-scale additive manufacturing technology. These cost barriers slow additive manufacturing adoption in price sensitive industries.

Opportunity

AI driven design and manufacturing innovation: Additive manufacturing innovation is helping in the development of additive manufacturing market opportunities through innovation in AI-driven design systems. Artificial intelligence is utilized for generative design and production optimization in digital manufacturing systems. For instance, in November 2025, Aibuild announced the opening of its U.S. headquarters in Silicon Valley, located inside Nikon's research facility. The company aims to advance AI-driven automation and collaboration in industrial additive manufacturing.

Segmental Insights

This report offers detailed coverage of the additive manufacturing market by technology, material, application, and end use industry to help readers identify the fastest expanding and most attractive demand segments.

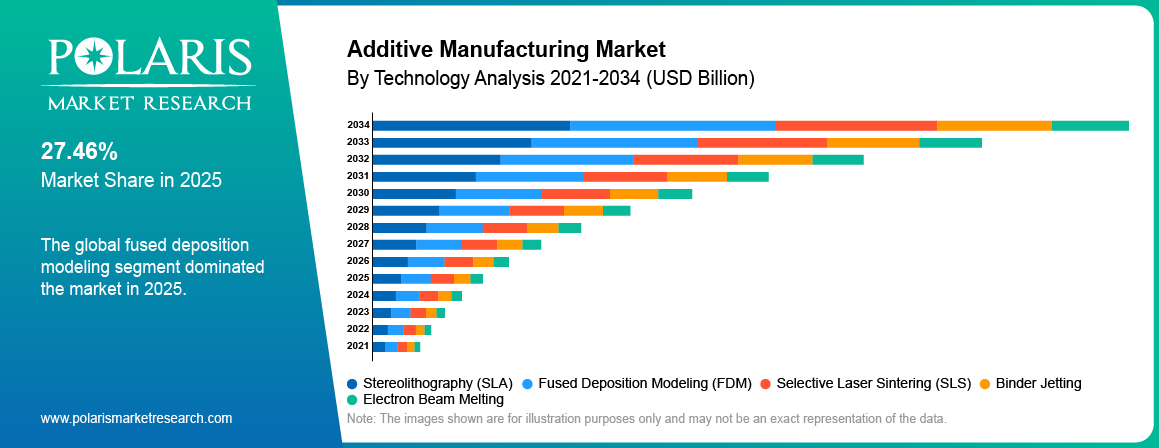

By Technology

-

Fused Deposition Modeling (FDM)

Fused Deposition Modeling dominated the industrial 3D printing technology market in 2025, driven by strong use in prototyping and product development. It provides low equipment cost and ease of operation. FDM systems are used in product testing in manufacturing and research organizations, leading to increased demand for industrial 3D printing technology.

-

Selective Laser Sintering (SLS)

Selective Laser Sintering segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for complex functional components. SLS provides precision production without tooling requirements. Aerospace and automotive industries are adopting SLS for lightweight production.

By Material

-

Polymers

Polymers held major segment share of the additive manufacturing market in 2025, due to the increasing demand for rapid prototyping and product design testing for the manufacturing industry. Additive manufacturing of polymers involves the production of lightweight and cost-effective products. These advantages strengthen the polymer additive manufacturing market across automotive and consumer electronics industries.

-

Metals

Metals segment is projected to grow at the fastest CAGR during the forecast period, due to increasing use of metal additive manufacturing for high strength components. Aerospace and healthcare sectors use metal printing for aircraft parts and medical implants. This trend supports growth of the metal additive manufacturing market.

By Application

-

Prototyping

Prototyping dominated the additive manufacturing market in 2025, driven by increasing demand for rapid production of products. Industrial 3D printing technology offers a business opportunity for the manufacturers to print the prototypes directly from the designs.

-

Functional Parts

Functional parts segment is projected to grow at the fastest CAGR during the forecast period, due to increasing use of additive manufacturing for end use component production. Adoption of additive manufacturing technology is on the rise in the additive manufacturing aerospace, additive manufacturing automotive, and additive manufacturing healthcare industries.

By End Use Industry

-

Aerospace & Defense

The aerospace & defense industry accounted for the largest market size in the additive manufacturing market in 2025. This is due to the high demand for lightweight aircraft parts. Additive manufacturing aerospace helps to reduce waste materials and enables the development of complex components.

-

Healthcare

Healthcare segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for personalized medical devices. Additive manufacturing healthcare applications support customized implants, prosthetics, and additive manufacturing dental products.

Regional Analysis

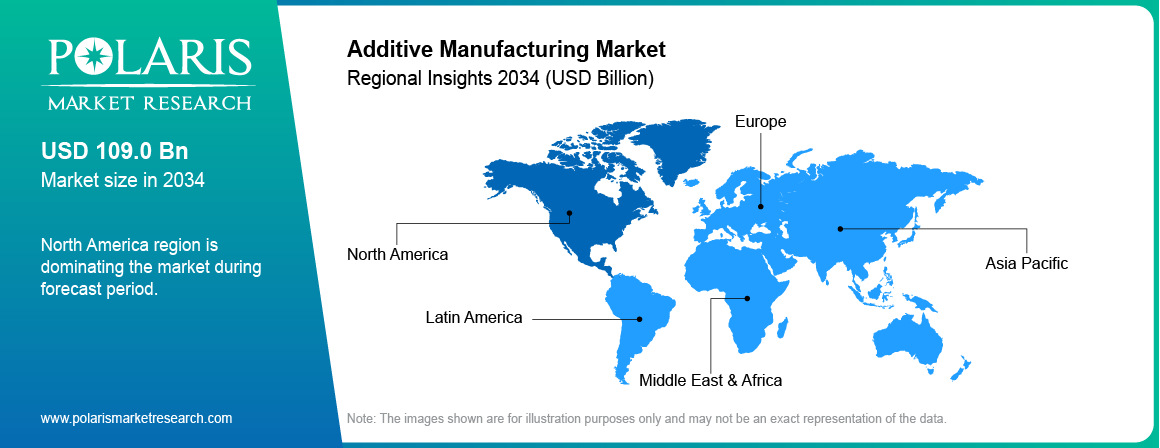

North America Market Assessment

North America additive manufacturing market dominated in 2025, driven by a strong aerospace industry and continuous technological innovation across the US and Canada. Aerospace companies are increasing the adoption of industrial 3D printing technology to produce lightweight aircraft components. For example, in March 2026, GE Aerospace announced a USD 1 billion investment to boost U.S. manufacturing capacity due to high demand for aircraft engines and parts, thus increasing the adoption of innovative production technology such as additive manufacturing technology.

Asia Pacific Additive Manufacturing Market Insights

Asia Pacific additive manufacturing market is expected to grow at the highest CAGR during the forecast period. The growth in the Asia Pacific region is attributed to the high growth rate in manufacturing in China, Japan, and India. Governments in the region are promoting advanced production technologies through industrial modernization programs. For instance, the Reserve Bank of India reported that India’s manufacturing sector is strengthening and may reach USD 1 trillion by FY26, while the country holds potential to contribute over USD 500 billion annually to the global economy by 2030 through expansion as a global manufacturing hub. These developments are strengthening the China additive manufacturing market and the India additive manufacturing market.

Europe Additive Manufacturing Market Overview

Europe was the second largest market for additive manufacturing, driven by strong industrial manufacturing and a large automotive sector. The countries that are using industrial 3D printing technology include Germany, France, and the UK. In March 2026, DN Solutions announced the opening of the first European Additive Solutions Center in Gütersloh, Germany. The main focus is to increase the adoption rate for metal additive manufacturing technology and combine it with CNC machining for industrial production.

Key Players & Competitive Analysis Report

The competitive environment for the additive manufacturing market is driven by continuous innovation in industrial 3D printing metals and materials. Companies are expanding the additive manufacturing environment with better machines, software, and materials. Strategic partnerships with aerospace, automotive, and healthcare manufacturers are strengthening additive manufacturing adoption across industrial production.

The key players operating in the additive manufacturing market are Stratasys, 3D Systems, EOS GmbH, GE Additive, HP Inc., Desktop Metal, Markforged, SLM Solutions, Materialise NV, Voxeljet AG, Nikon SLM Solutions, Renishaw plc, and many more.

Premium Insights

Economics of Additive Manufacturing

|

Economic Factor |

Explanation |

|

Cost Drivers |

Equipment investment, printing materials, and post-processing operations represent the major cost drivers in the additive manufacturing market. |

|

Production Efficiency |

Industrial 3D printing reduces tooling costs and minimizes material waste compared with traditional manufacturing methods. |

|

Manufacturing Economics |

The technology improves cost efficiency for rapid prototyping and low-volume production environments. |

|

ROI Advantage |

Additive manufacturing technology provides strong return on investment for complex and lightweight component production. |

Value Chain Analysis

|

Value Chain Stage |

Process Description |

|

Design |

Engineers create digital models using computer-aided design software. |

|

Printing |

Industrial 3D printing systems build components through layer-by-layer material deposition. |

|

Post-Processing |

Finishing processes include heat treatment, polishing, and structural reinforcement. |

|

Quality Control |

Inspection and testing verify component accuracy, strength, and performance standards. |

Decision Framework

|

Decision Factor |

Commercial Relevance |

|

Design Complexity |

Additive manufacturing becomes viable for complex geometries that traditional methods cannot easily produce. |

|

Production Volume |

The technology suits rapid prototyping and low-volume manufacturing where tooling costs remain high. |

|

Customization Needs |

Industries requiring personalized components benefit from additive manufacturing technology. |

|

Supply Chain Flexibility |

Digital manufacturing supports decentralized production and faster product development cycles. |

Industry Case Examples

|

Industry |

Use Case |

|

Aerospace |

Additive manufacturing technology produces lightweight aircraft components that improve fuel efficiency. |

|

Healthcare |

Industrial 3D printing supports customized implants, prosthetics, and dental devices for patient-specific treatments. |

|

Automotive |

Manufacturers use additive manufacturing applications for rapid prototyping and tooling development. |

|

Industrial Manufacturing |

The companies are using digital manufacturing systems for creating complex machine parts or spare parts. |

Key Players

- 3D Systems

- Desktop Metal

- EOS GmbH

- GE Additive

- HP Inc.

- Markforged

- Materialise NV

- Nikon SLM Solutions

- Renishaw plc

- SLM Solutions

- Stratasys

- Voxeljet AG

Industry Developments

- January 2026: 3D Systems has announced investments in expanding its capabilities for additive manufacturing in aerospace and defense industries for large-scale production of 3D-printed parts for aircraft and defense systems.

- October 2025: EOS GmbH has introduced four new metal-based additive manufacturing materials before the Formnext 2025 event for expanding the scope of industrial additive manufacturing for aerospace, energy, automobile, and chemical industries.

Additive Manufacturing Market Segmentation

By Technology Outlook (Revenue, USD Billion, 2021-2034)

- Stereolithography (SLA)

- Fused Deposition Modeling (FDM)

- Selective Laser Sintering (SLS)

- Binder Jetting

- Electron Beam Melting

By Material Outlook (Revenue, USD Billion, 2021-2034)

- Metals

- Polymers

- Ceramics

- Composite

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Prototyping

- Tooling

- Functional Parts

By End Use Industry Outlook (Revenue, USD Billion, 2021-2034)

- Automotive

- Aerospace & Defense

- Healthcare

- Consumer Electronics

- Power & Energy

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Additive Manufacturing Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 31.36 Billion |

|

Market Size in 2026 |

USD 38.76 Billion |

|

Revenue Forecast by 2034 |

USD 215.49 Billion |

|

CAGR |

23.9% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 31.36 Billion in 2025 and is projected to grow to USD 215.49 Billion by 2034.

North America led due to high aerospace industry demand and capabilities in industrial manufacturing.

The major applications are rapid prototyping, tooling development, and functional parts manufacturing in industrial manufacturing industries.

A few of the key players in the market are Stratasys, 3D Systems, EOS GmbH, GE Additive, HP Inc., Desktop Metal, Markforged, SLM Solutions, Materialise NV, Voxeljet AG, Nikon SLM Solutions, Renishaw plc, and others.

The major drivers are increasing demand for rapid prototyping, lightweight parts manufacturing, and digital manufacturing technology adoption.

The major industries for additive manufacturing are aerospace, healthcare, automotive, consumer products, and industrial manufacturing.

The forecast for the additive manufacturing market looks positive due to the increasing adoption of digital manufacturing, generative design tools, and advanced printing materials.

Page last updated on:

Mar-2026

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements