Aerospace Valves Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Aerospace Valves Market Overview

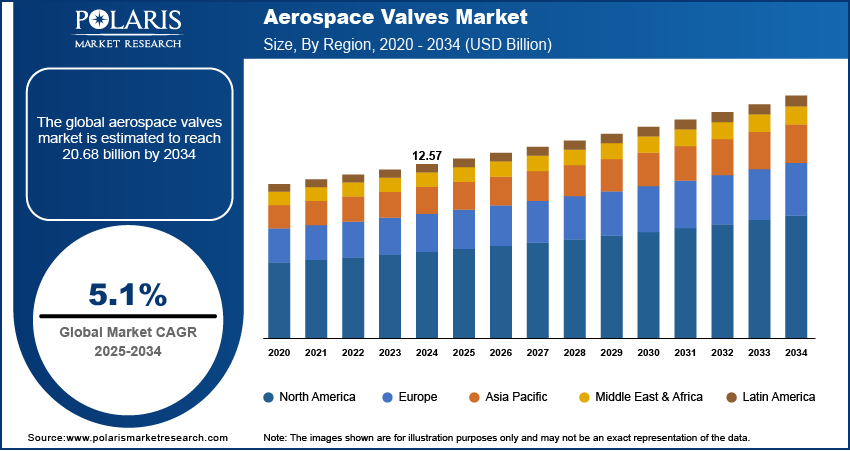

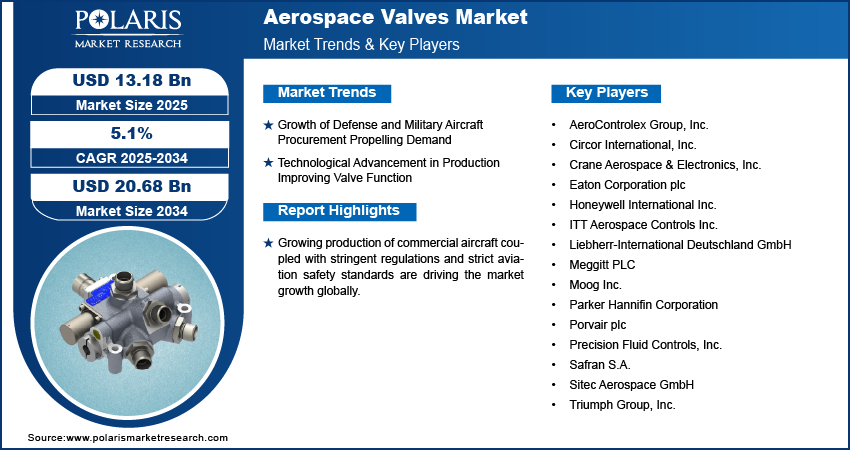

The global aerospace valves market size was valued at USD 13,353.7 million in 2025. The market is projected to account for a CAGR of 4.2% between 2026 and 2034. The growth of defense and military aircraft procurement, coupled with technological advancements in valve production, is driving market growth.

Key Insights

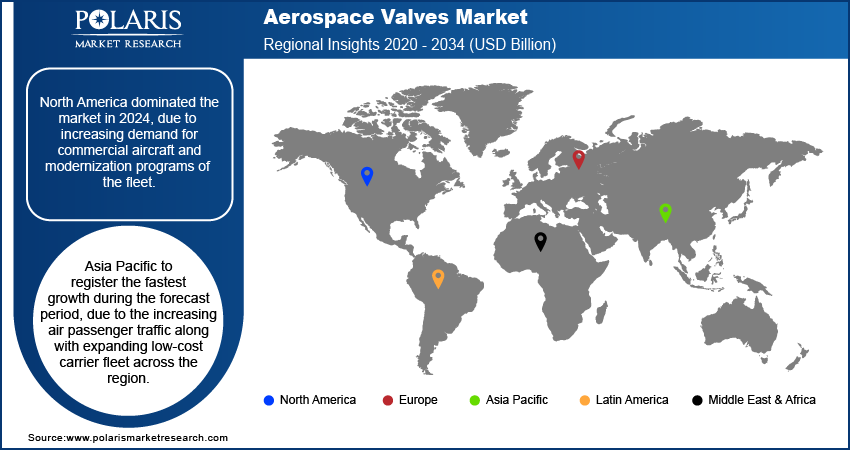

- North America accounted for the largest market share of 38.73% in 2025. The rising need for commercial aircraft, as well as modernization programs, is fueling regional market leadership.

- Asia Pacific is expected to grow at a fast pace with CAGR of 4.7%. The rapid expansion of air passenger traffic as well as low-cost carrier operations is boosting aircraft valve demand.

- By product, the butterfly valves segment led the market with market share of 18.22% in 2025. This is due to the lightweight design and the ability to efficiently regulate high-flow fluids of these valves.

- By material, titanium valves are projected to witness rapid growth with CAGR 4.7%. This is because titanium is lightweight and has a high strength-to-weight ratio.

Market Statistics

- 2025 Market Size: USD 13,353.7 million

- 2034 Projected Market Size: USD 19,985.7 million

- CAGR (2026–2034): 4.2%

- North America: Largest Market Share in 2025

Industry Dynamics

- Rise in geopolitical risks and defense spending worldwide is resulting in an increase in defense and military aircraft requirements. This is further driving the aerospace valves market growth.

- Advancements in manufacturing technology are enabling the creation of lightweight, precise parts for aerospace valves through techniques such as additive manufacturing and 3D printing.

- The high cost of manufacturing precision-engineered aerospace valves acts as a barrier to growth.

- Sensors and digital monitoring are being integrated to track the performance of aerospace valves. This is creating market growth opportunities.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The aerospace valves market consists of rugged parts for effective control of fluids and gases within airplane systems. Aerospace valves are widely used throughout fuel management, hydraulics, environmental control, and lubrication systems to achieve aircraft safety and performance. The use of more advanced materials and designs is enhancing efficiency, reliability, and cost efficiency, and thus, aerospace valves are a vital component in defense and commercial aviation.

The aerospace valves industry is growing steadily, mainly due to increasing requirements for superior-quality aircraft parts that are capable of controlling fluids and gases accurately. These are used for applications such as fuel systems, hydraulic actuation, pneumatic control, environment control, and lubrication. These are all essential requirements for aircraft to be safe, efficient, and reliable. The industry is closely related to aircraft manufacturing, defense modernization, and overall aviation requirements.

The increase in the number of passengers carried by air, the expansion of the number of aircraft fleets, and the growth of low-cost airlines are some of the factors that contribute to the growth of aircraft production. Narrow-body aircraft are in great demand due to their cost-effectiveness. This is likely to boost the growth of aerospace valves. Boeing projects that the global aerospace services market is expected to be worth approximately USD 4.7 trillion over the next 20 years. This emphasizes the long-term role of aftermarket demand, maintenance, and replacement cycles in supporting aerospace valve consumption.

Aerospace valves are critical components designed to operate in extreme environments that may experience high pressure, temperature variations, and corrosive conditions. They manage both aerospace fluid control systems and gas systems. The use of these systems enables safe, efficient aircraft flight in both commercial and defense aviation. Advanced materials and compact designs are being used to enhance the performance and reliability of valve systems used in aircraft.

Stringent regulations on aerospace valves and aviation safety norms are contributing to higher adoption rates for aerospace valves. The aerospace industry has strict regulations to be followed, such as FAA standards or EASA certification requirements. These regulations are necessary to ensure that the valves will operate correctly under extreme conditions, such as pressure changes, heat stress, and other environmental conditions. This makes the process more complicated, but it increases the product's credibility.

Market Dynamics

Growth of Defense and Military Aircraft Procurement

Geopolitical tensions and rising defense spending budgets are increasing the demand for aerospace valves in military aircraft. Valves play a vital role in fuel, hydraulic, and environmental control systems, providing operational efficiency and safety in harsh conditions. The increasing defense spending is fuelling growth in defense procurements in military aircraft, UAVs, helicopters, and transport aircraft. These systems require high-performance valves that can perform in mission-critical conditions. Therefore, defense modernization is an important growth driver for the aerospace defense market and aerospace valves.

Technological Advancements in Manufacturing

Additive manufacturing is improving valve performance. New technologies, including 3D printing, digital monitoring, and smart valve integration, are changing the aerospace valve market. Companies are designing smart valves. The smart valve is designed to have sensors for better performance through predictive maintenance aerospace. The use of smart valve technology enables real-time monitoring of the valve for better efficiency. Additive manufacturing valves are being used to reduce weight and increase production speed.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

By Product Type Insights

Based on product type, the aerospace valves market is classified into butterfly valves, rotary valves, solenoid valves, flapper-nozzle valves, poppet valves, gate valves, ball valves, and others. the butterfly valves segment led the market with market share of 18.22% in 2025. This is because of their low weight, long life, and high efficiency in controlling high-flow fluids. These valves are used in the fuel, hydraulic, and environmental control systems of commercial and military aircraft. The compact design and low pressure drop of butterfly valves aerospace make them suitable for use in aerospace applications.

The ball valves segment is anticipated to register robust growth during the forecast period. This is driven by their accurate control of fluids and their ability to be automated. Ball valves aerospace are also compatible with advanced aerospace applications.

By Aircraft Type Insights

On the basis of aircraft type, the aerospace valves market is divided into commercial aviation, and defense aviation. The commercial aviation segment led the aerospace valves market in 2025, driven by rising air passenger traffic and increased aircraft production. Growing fleet expansion, maintenance requirements, and demand for fuel-efficient systems accelerated valve adoption, while advancements in lightweight materials and precision engineering further supported market growth across commercial aircraft applications.

The defense aviation segment is expected to register rapid growth with CAGR of 4.4%, driven by increasing defense budgets, rising procurement of advanced military aircraft, and modernization programs. Growing demand for high-performance, durable valve systems in extreme operating conditions further supports market expansion across defense aviation applications globally.

By Material Insights

Based on material, the market is classified into stainless steel, titanium, aluminum, and others. Stainless steel dominated the market in 2025. This is because they possess durability characteristics, high corrosion resistance, and performance in critical aerospace applications. Their widespread use in commercial and military aircraft has also contributed to their position in the market.

titanium valves are projected to witness rapid growth with CAGR 4.7%. This is because they are lightweight and strong, thus improving fuel efficiency and aircraft performance. They can also resist temperatures and corrosion. This makes them suitable for advanced aerospace applications.

By Application Insights

By application, the market is divided into fuel system, hydraulic system, environmental control system, pneumatic system, lubrication system, and water & wastewater system. The fuel system segment dominated the market in 2025. This is due to the need to have accurate and reliable fuel flow control in aircraft. The emphasis on fuel efficiency and safety is driving the demand for advanced valve systems in this industry.

The hydraulic system segment is expected to grow significantly in the forecast period. Modern aircraft utilize more advanced hydraulic systems to ensure better safety. New aircraft designs are entering the market, which is driving growth in this segment. Reliability in critical operations is also contributing to the segment’s growth.

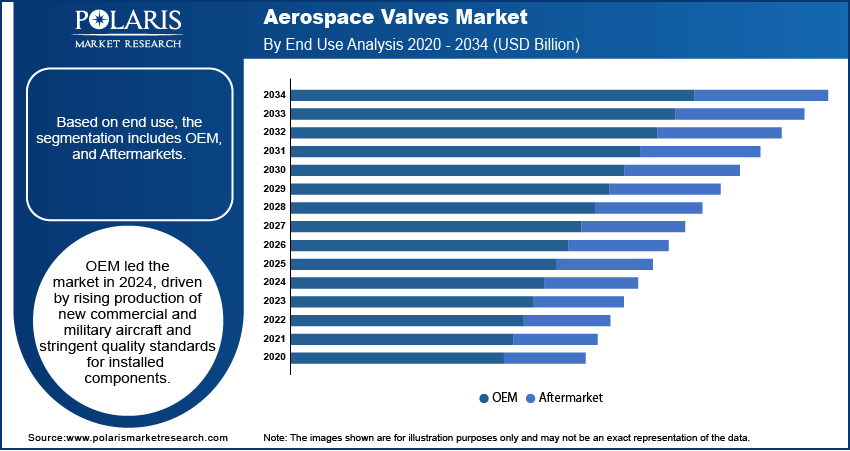

By End Use Insights

Based on end use, the aerospace valves market is categorized into OEM and aftermarket. The OEM segment dominated the market in 2025, owing to the increasing number of newly produced commercial and military aircraft and the stringent quality requirements for components used. The growing use of advanced, highly efficient systems in newly produced aircraft is another factor contributing to the segment’s dominance.

The aftermarket segment is expected to grow significantly in the future. This is mainly due to fleet upgrades, aircraft replacements, and maintenance, repair, and overhaul activities. The demand for reliable, high-performance replacement valves is also boosting the aftermarket segment.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

North America accounted for a considerable share of 38.73% the global market in 2025. This is due to the rising requirement for commercial aircraft and the modernization of existing aircraft in the region. The growing trend of air travel, both domestically and internationally, has prompted airlines to add more aircraft to their fleets. This is increasing the need for valves on their aircraft. The region is also home to many aircraft OEMs and MROs. This further contributes to the demand for high-reliability valves.

U.S. Aerospace Valves Market Overview

The U.S. continues to dominate the North America market with a CAGR of 4.0%. The region is driven by high defense spending and aircraft upgrade projects. According to data provided by the Stockholm International Peace Research Institute (SIPRI), defense spending in the U.S. increased by 2.3% to reach 916 billion U.S. dollars in 2023. This includes the production of future fighter jets, spy planes, and transport aircraft. Innovation in aerospace production and defense preparedness is creating strong demand for hydraulic, pneumatic, and fuel system valves.

Asia Pacific Aerospace Valves Market Insights

Asia Pacific is expected to grow rapidly with CAGR of 4.7% over the forecast period. Increasing passenger air traffic, along with the growth of low-cost carriers, is driving demand for commercial aircraft in this region. In addition, increased defense spending and the modernization of defense fleets in India, China, and Japan are boosting the regional market. The governments in this region are investing heavily in developing local aerospace manufacturing capabilities. This is enabling increased integration of valve systems in aircraft platforms.

India Aerospace Valves Market Analysis

India is emerging as an important growth center for aerospace valve manufacturers, driven by increased aircraft manufacturing and assembly capacity. According to the International Air Transport Association (IATA), India is predicted to surpass China and the U.S. to become the world’s third-largest air passenger market by 2030. Increasing domestic manufacturing capacity in line with the ‘Make in India’ initiative, coupled with an increase in air travel, is driving demand for suppliers to fuel valves, hydraulic systems, and pneumatic systems for civil and defense aircraft.

Europe Aerospace Valves Market Assessment

The market for aerospace valves in Europe is expected to grow robustly in the coming years, driven by safety standards and sustainability initiatives in aviation. The focus on advanced materials and high-efficiency valve technology, which can help design lightweight, fuel-efficient aircraft, is gaining traction in the region. The region's carbon-emission-reduction drive, as well as the adoption of sustainable aviation fuels, is also driving innovation in the market. The high demand from leading aircraft manufacturers in France, Germany, and the UK is also driving the regional market.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Analysis

The global aerospace valve market is highly competitive. The industry is driven by innovation and technological changes. The key players in this industry are striving to increase efficiency, reduce weight, and increase product durability to meet the performance criteria of modern airplanes. Establishing new production facilities, working with OEMs, and developing new valve systems for electric and hybrid airplanes are among the key strategic objectives.

Key players in the global aerospace valves market are AeroControlex Group, Inc., Circor International, Inc., Crane Aerospace & Electronics, Inc., Eaton Corporation plc, Honeywell International Inc., ITT Aerospace Controls Inc., Liebherr-International Deutschland GmbH, Meggitt PLC, Moog Inc., Parker Hannifin Corporation, Porvair plc, Precision Fluid Controls, Inc., Safran S.A., Sitec Aerospace GmbH, and Triumph Group, Inc.

Eaton Corporation plc is a leading manufacturer of aerospace valves. Its valves are used in fuel, hydraulic, pneumatic, and thermal systems. The company focuses on reliability, efficiency, and lightweight designs. Its engineering expertise and broad product offerings make it suitable for both commercial and defense aviation platforms.

Parker Hannifin Corporation is a global leader in motion and control technologies. Its product offerings include aerospace valves and fluid control systems for different aircraft systems. Parker serves prominent OEMs and benefits from a broad product range, a global footprint, and years of industry experience.

List of Key Companies

- AeroControlex Group, Inc.

- Circor International, Inc.

- Crane Aerospace & Electronics, Inc.

- Eaton Corporation plc

- Honeywell International Inc.

- ITT Aerospace Controls Inc.

- Liebherr-International Deutschland GmbH

- Meggitt PLC

- Moog Inc.

- Parker Hannifin Corporation

- Porvair plc

- Precision Fluid Controls, Inc.

- Safran S.A.

- Sitec Aerospace GmbH

- Triumph Group, Inc.

Aerospace Valves Industry Developments

January 2025: Aerolloy Technologies commissioned its first Vacuum Arc Remelting furnace to domestically produce aerospace-grade titanium alloys. According to Aerolloy Technologies, the move strengthens local manufacturing of lightweight and high-performance materials. It also reduces reliance on imports and improves supply chain resilience in the aerospace components market.

October 2022: Triumph Group acquired a contract from Lockheed Martin to produce brake valve assemblies for the F-16 Fighting Falcon aircraft. Triump Group provides production hardware and operational support for the F-16 program under this contract.

August 2022: Marsh Brothers Aviation signed a four-year deal with Aviation Fabricators (AvFab) to provide aircraft seat actuator valves. The alliance came after Marsh Brothers helped fix AvFab's supply chain issues, and the company is expected to provide customized actuator valves for the MRO of private and commercial aircraft seats.

February 2022: ITT Inc. subsidiary ITT Aerospace Controls added five new valves and actuators to its portfolio of aircraft components. The revamped line of products strengthens the company's presence in fluid handling applications within fuel, hydraulic, water, and environmental control systems utilized in aerospace and defense applications.

Aerospace Valves Market Segmentation

By Product Type Outlook (Revenue, USD Million, 2021–2034)

- Butterfly Valves

- Rotary Valves

- Solenoid Valves

- Flapper-nozzle Valves

- Poppet Valves

- Gate Valves

- Ball Valves

- Others

By Aircraft Type Outlook (Revenue, USD Million, 2021–2034)

- Commercial Aviation

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional Aircraft

- General Aviation

- Defense Aviation

- Defense Aviation

- Helicopter

- Military Aircraft

- Spacecraft

- UAVs

By Material Outlook (Revenue, USD Million, 2021–2034)

- Stainless Steel

- Titanium

- Aluminum

- Others

By Application Outlook (Revenue, USD Million, 2021–2034)

- Fuel System

- Hydraulic System

- Environmental Control System

- Pneumatic System

- Lubrication System

- Water & Wastewater System

By End Use Outlook (Revenue, USD Million, 2021–2034)

- OEM

- Aftermarket

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Aerospace Valves Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 13,353.7 Million |

| Market Size in 2026 | USD 13,849.1 Million |

| Revenue Forecast by 2034 | USD 19,121.4 Million |

| CAGR | 4.2% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Aerospace Valves Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Aerospace Valves Market FAQ's

The aerospace valves market was valued at USD 13,353.7 million in 2025. The market is projected to reach by USD 19,121.4 million in 2034.

The market is projected to account for a CAGR of 4.2% between 2026 and 2034.

North America led the market in 2025. This is due to the increasing demand for commercial aircraft and the modernization programs of the fleet.

A few of the key players in the market include AeroControlex Group, Inc., Circor International, Inc., Crane Aerospace & Electronics, Inc., Eaton Corporation plc, Honeywell International Inc., ITT Aerospace Controls Inc., Liebherr-International Deutschland GmbH, Meggitt PLC, Moog Inc., Parker Hannifin Corporation, Porvair plc, Precision Fluid Controls, Inc., Safran S.A., Sitec Aerospace GmbH, and Triumph Group, Inc.

The butterfly valves segment accounted for the largest market share in 2025. This is due to their long life and capacity to control high-flow fluids with high efficiency.

The hydraulic system segment is projected to register the fastest growth. This is because newer airplanes increasingly depend on automated fluid control technology to improve efficiency.

Download Sample Report of Aerospace Valves Market

Please fill out the form to request a customized copy of the research report.