Market Overview

The global agricultural adjuvants market size was valued at USD 4.32 billion in 2025. According to our agricultural adjuvants market forecast, the industry is projected to account for a CAGR of 4.9% between 2026 and 2034. The growth can be attributed to the need for efficient crop protection products and increased focus on sustainable agriculture practices.

Key Insights

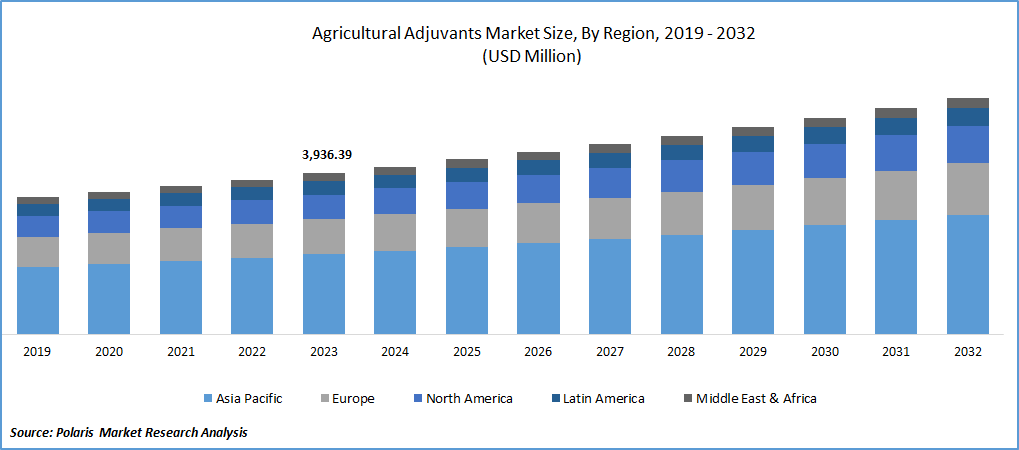

- Asia Pacific led the market with a 39.1% revenue share in 2025. This is due to the high level of pesticides and agricultural activity within this region.

- The North America agricultural adjuvants market is expected to grow at 5.1% CAGR, owing to the increasing use of advanced application technology.

- In 2025, the herbicides segment dominated the market with a 49.1% revenue share. The segment’s dominance is driven by the extensive use of glyphosate adjuvants and glufosinate in farming.

- The utility adjuvants segment is expected to account for a 4.9% CAGR, as they help improve spray quality and reduce drift.

Market Statistics

- 2025 Market Size: USD 4.32 billion

- 2034 Projected Market Size: USD 6.63 billion

- CAGR (2026–2034): 4.9%

- Asia Pacific: Largest Market in 2025

Industry Dynamics

- The growing use of agrochemicals has created an increased demand for agricultural adjuvants to enhance the properties of these chemicals.

- The rising demand for sustainable agricultural adjuvants is projected to boost market demand.

- Increased need to manage herbicide resistance is projected to create several market opportunities.

- Limited awareness and education among farmers may hinder market growth.

To Understand More About this Research:Download Sample Report

Agricultural adjuvants are additives used with herbicides, insecticides, fungicides, and other biological crop protection additives. The use of these products helps to enhance spreading, wetting, penetration, retention, and drift control. This makes them important for conventional and precision farming systems.

Agricultural adjuvants are now viewed not only as supporting agents. They are also seen as value-adding chemicals that enhance the performance of costly crop protection chemicals, minimizing losses and maximizing application efficiency in both conventional and specialty crops. In the face of growing demands to produce more from already scarce land resources, adjuvants are gaining greater importance in precision spraying, drift reduction, biological compatibility, and variable-rate application programs.

The market is also driven by the rise of crop protection product use with increasingly complex spray conditions. Agricultural adjuvants are known to alter the physical and chemical characteristics of the spray solution, thereby enhancing droplet spread, adhesion, canopy penetration, rainfastness, and the uptake of active ingredients. Adjuvants are crucial, especially in herbicide-intensive applications, drone-based spraying, and harsh climate and crop conditions.

The agricultural adjuvants market is also supported by the increasing pressure on global agriculture. The global cropland area per capita was 0.2 hectares in 2021, 18% less than in 2000, according to the Food and Agriculture Organization (FAO). This shows the need to improve crop productivity from the available land. In this respect, adjuvants are gaining more importance as they help farmers to improve agricultural efficiency without increasing the amount of the active ingredients.

Market Dynamics

Rising Demand for Sustainable Agricultural Adjuvants

The agricultural adjuvants market is being driven by the increasing impact of the shift to sustainable agricultural adjuvants. There is growing interest in biodegradable, low-residue, bio-based agricultural adjuvants that improve sprayability while reducing environmental impact. The trend is particularly relevant in high-value crops and biological crop protection programs. It can also be seen in regions where residue levels, spray drift, and regulatory approval are critical to the purchasing decision.

Sustainble crop protection technologies are now a part of product development, not marketing. Companies are now developing adjuvants that can be used in combination with biological pesticides, low-dose chemicals, and precision applications. This is relevant as new crop protection agents generally have more specific adjuvants than conventional ones. The recent developments include the launch of BASF's Agnique BioHance product in May 2024, as well as the partnership between Rovensa Next and the Biocontrol Coalition in April 2024. These developments show the market's focus on biological efficacy and regulatory activity.

Increasing Use of Agrochemicals

The agricultural adjuvants market is growing rapidly due to increasing agrochemical demand, especially for crops that require repeated and targeted control of weeds, diseases, and pests. According to FAO, global pesticide use reached 3.73 million tonnes of active ingredients in 2023, following several years of growth. With this increase in pesticide use in agriculture, the demand for adjuvants is also increasing. They help to increase efficiency, reduce reapplication, and boost pesticide efficacy in field conditions.

The increased use of agrochemicals has also meant that there has been a corresponding increase in the use of agricultural surfactants, oil adjuvants, spreaders, compatibility agents, and water conditioners. These agents are useful for improving wetting, mixing, deposition, droplet retention, and leaf retention. Adjuvants are not merely optional for the interests of the commercial grower. Rather, they are boosters for maximizing the return on investment for pesticide and fertilizer applications.

The demand for herbicides remains strong. According to USDA-based statistics, 84% of glyphosate is used in crops such as soybeans, corn, and cotton. This implies that it is highly used in large-scale farming activities, in which adjuvants play a significant role. In this case, herbicide adjuvants are used to boost the spreadability and absorption of glyphosate application. It also helps in its rainfastness and resistance management.

Precision Agriculture, Drone Spraying, and Digital Farming

GPS-guided sprayers, drone-based sprayers, sensor-based mapping, and variable-rate application sprays need better control over droplet size, spray drift, deposition, moisture retention, and canopy penetration. In this scenario, precision agriculture adjuvants can serve as a link between modern equipment, such as AI-guided spray systems, and field performance.

The role of drone spraying is becoming increasingly important in markets where there is demand for labor-saving, quick field coverage, and operations in difficult terrain. In this case, adjuvants that help reduce drift, evaporation, and deposition are very important for the spray. For example, Evonik has highlighted the role of Evonik adjuvants like BREAK-THRU MSO MAX 522 and TEGO XP 11134, which are used in drone farming. These drones focus on reduced drift, canopy penetration, and deposition.

Restraints and Challenges

Although the agricultural adjuvants market has strong drivers, it also has some limitations. Obtaining regulatory clearances for surfactants, oils, polymers, and specialty co-formulants approvals can be challenging. This can impact the progress of product development. The performance of the product can also differ across crops, climates, and tank-mix combinations. This presents a challenge, especially for newer crop protection technologies such as biological or precision crop protection solutions.

Technology and Innovation Outlook

The technology profile of the agricultural adjuvants industry is changing from simple surfactants to more specialized products for biologicals, drones, and digital farming. Some industry product innovations reflect an increased focus on precision application, biologicals, and digital farming. The partnership between BASF and Agmatix, announced in March 2025, to develop an AI in agriculture solution for soybean cyst nematode detection is an example of how precision application is combined with digital technology. While it is not an adjuvant product, it is an example of how precision application is driving crop protection more broadly, where adjuvants will become even more important.

The market is also being driven by developments in bio-based crop protection methods. With more biological fungicides, insecticides, and pest management products being used, there is a growing requirement for adjuvants to enhance distribution and tackiness without affecting the stability of the active ingredients. Hence, formulation compatibility, low toxicity, and longer shelf-life are more important than in traditional adjuvant systems.

Segmental Insights

By Function Outlook

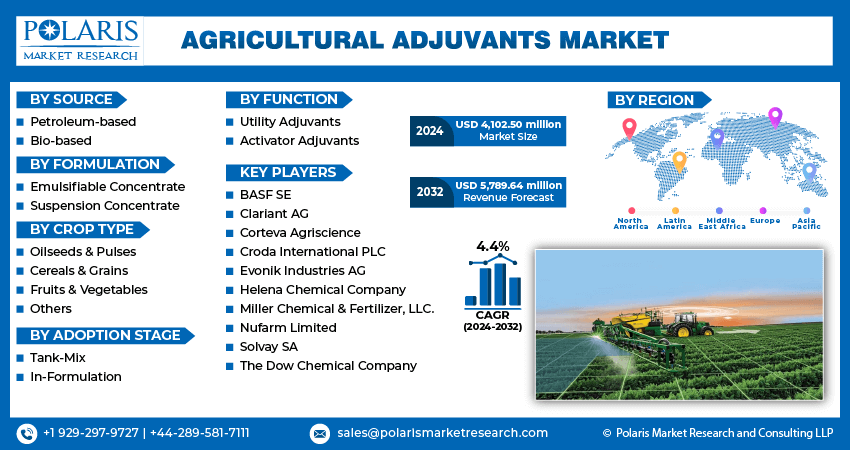

The agricultural adjuvants by function market segmentation includes activator adjuvants and utility adjuvants. The utility adjuvants segment is expected to grow at a 4.9% CAGR during the forecast period. This is mainly because utility adjuvants alter the physical and chemical properties of spray solutions, thereby improving spray quality, reducing drift, and enhancing adhesion to plant surfaces. Utility adjuvants help deliver crop protection chemicals more accurately, a factor gaining increasing importance in precision spray applications. For example, Clariant has launched Synergen DT, which is an antidrift agent for drone spraying. This demonstrates the role of utility adjuvants in the development of newer application systems like drone technology. These adjuvants assist in the control of drift and evaporation, thus becoming suitable for both sustainable and technology-based farming practices.

At the same time, the activator adjuvants remain relevant, as they enhance spray application by directly improving its effectiveness. Utility adjuvants are growing in popularity due to an increasing need for advanced application technology, while activator adjuvants remain an essential category as they play an important role in herbicide and pesticide performance.

By Application Outlook

Based on application, the agricultural adjuvants market includes herbicides, fungicides, insecticides, and others. In 2025, the herbicides segment dominated the market with a 49.1% revenue share, driven by the extensive use of glyphosate adjuvants and glufosinate in farming. The effectiveness of herbicides depends on their spreading, retention, canopy coverage, and absorption. According to USDA data, the major crops that use the most herbicides are soybeans, corn, and cotton, indicating a strong association between herbicides and adjuvants. Adjuvants are used in these crops to control resistance and cover leaves. Their use also helps maintain crop protection performance.

Fungicides and insecticides are another area of increasing interest, especially in specialty crops and high-value horticulture. Fungicide and insecticide adjuvants enhance canopy penetration, uniformity of canopy coverage, and the efficient use of active ingredients. This is especially true in the high-value crops of fruit and vegetable farming. Here, the quality of the products and the efficiency of the inputs can impact the grower's profitability.

By Source Outlook

The market, by source, is segmented into petroleum-based and bio-based. Petroleum-based adjuvants are favored due to their long history of use, reliability, and compatibility with conventional crop protection systems. However, bio-based adjuvants are becoming increasingly important as companies react to the push for sustainability. Their demand is also on the rise due to the need for biodegradable products, and the growing interest in environmentally friendly spray programs. Bio-based formulation additives are expected to see increased adoption in applications related to biological pesticides, sustainability-focused markets, and regions where environmental factors play a role in buying decisions.

By Adoption Stage Outlook

By adoption stage, the market is segmented into tank-mix and in-formulation. In-formulation adjuvants led the agricultural adjuvants market in 2025. This is due to the need for ready-to-use formulations, as well as the increasing concern for spray drift and environmental safety. Crop protection manufacturers prefer in-formulation adjuvants due to the built-in compatibility, handling, and performance advantages. Tank mix adjuvants remain important at the distributor and grower levels because of their flexibility in local farming needs, crop-specific programs, and customized spray performance.

By Crop Type Analysis

By crop type, the agricultural adjuvants market covers oilseeds & pulses, cereals & grains, fruits & vegetables, and others. The cereals & grains segment led the market in 2025, driven by the large-scale cultivation of crops such as wheat, rice, corn, and others. These crops are expected to remain a significant driver of the market due to the large area under cultivation and the use of herbicides and pesticides in row crop production. Fruits & vegetables are also another high-value segment in adjuvants as there is an increased focus on product quality, disease control, precision in spraying, and residues.

Regional Analysis

By region, the study covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

The Asia Pacific agricultural adjuvants market dominated the global market with a 39.1% revenue share in 2025. The high level of pesticide and agricultural activity within this region makes it a significant contributor to the global market. According to the FAO, pesticide consumption levels in 2023 were high, at 218 kilotons in China and 40.1 kilotons in India. Adjuvants play a crucial role in the effectiveness of pesticides and other crop protection agents. This level of pesticide activity supports the high growth rate of this region.

The region also has strong long-term growth potential, driven by the combination of extensive farming and increasing demand for crop protection efficiency-enhancing products. In India and China, the need to enhance crop yields, the rising cost of inputs, and the adoption of more advanced crop protection techniques are the Asia Pacific market trends expected to sustain adjuvants' demand.

North America

The North America agricultural adjuvants market is expected to record a 5.1% CAGR during the forecast period. This is attributed to the use of advanced application technology, strong awareness of spray performance, and the high level of herbicides used in large-scale row crop cultivation. The region also benefits from regulatory pressure on spraying and demand for higher pesticide efficiency.

The Canada agricultural adjuvants industry and the U.S. agricultural adjuvants market are significant due to the scale of commercial farming activities and the presence of robust distribution infrastructure. In addition, there is significant demand for technologies that minimize drift and maximize deposition. The recent introduction of Liberty ULTRA Herbicide with Glu-L Technology by BASF is a significant development in the region. The region is also a significant center for innovation in biological support adjuvants, digital farming technologies, and precision spray technologies. This further reinforces its importance beyond current market volumes.

Europe

The Europe agricultural adjuvants market accounts for a substantial market share due to the need for better crop yield, high production of high-value crops, and an emerging focus on sustainability. The shift to fruits, vegetables, and specialty crops is boosting demand for adjuvants to improve spray efficiency without negatively impacting the environment and to optimize resource use. The partnership formed in April 2024 between Rovensa Next and the Biocontrol Coalition is an example of the region’s focus on developing even more sustainable crop protection products. Europe is an important region in terms of demand as well as the regulatory environment, in which sustainability is driving next-generation adjuvants.

Latin America

The Latin America agricultural adjuvants market is an important sector for agrochemicals because of its production of soybeans, corn, and other agricultural products on a large scale. Countries like Brazil, Argentina, and Colombia are major contributors to this region’s market. Brazil is experiencing high agrochemicals demand because of its high soybeans production. This creates a favorable environment for adjuvants that enhance the efficiency of herbicides and pesticides across broad-acre programs.

Middle East & Africa

The Middle East & Africa agricultural adjuvants market is expected to grow gradually due to the rise in food security concerns and the use of controlled environment farming and advanced crop protection techniques. In this region, there is also an increase in the use of pesticides and the interest in controlled-environment farming techniques in countries like Saudi Arabia. Even though this region is smaller in comparison to Asia Pacific and North America, there are opportunities in greenhouse agriculture, horticulture, and water-sensitive farming, where spray efficiency is important.

Key Market Players & Competitive Analysis

Key agricultural adjuvants market players are focusing on research and development activities to increase their portfolios and improve performance for conventional and sustainable crop protection products. Market participants are increasingly focusing on product portfolio expansion, collaborations, acquisitions, and application development to increase geographical reach and improve category positioning.

Key agricultural adjuvants companies include BASF SE, Clariant AG, Corteva Agriscience, Croda International PLC, Evonik Industries AG, Helena Chemical Company, Miller Chemical & Fertilizer, LLC, Nufarm Limited, Solvay SA, and The Dow Chemical Company.

The agricultural adjuvants market competitive landscape is increasingly characterized by four major themes. These are compatibility of products with biological products, drift control innovation of modern spray systems, support of precision agriculture inputs, and sustainability-led formulation development.

BASF is one of the most prominent innovators in the industry. In May 2024, the company launched the Agnique BioHance range to enhance the performance of biological pesticides. This BASF crop protection innovation is in line with the overall trend of products that enhance adhesion, spreading, and compatibility in crop protection agents.

Evonik’s footprint is enhanced by developing adjuvant innovations in drone-assisted farming applications. BREAK-THRU MSO MAX 522 and TEGO XP 11134 provide Evonik’s customers with advantages in reduced drift, better deposition, and improved canopy penetration. This is an example of how the focus of the industry is shifting to application-specific performance additives.

Similarly, Corteva, Croda, Clariant, and other key industry players are competing in terms of differentiated formulation support, crop protection integration, and access to channels. The next phase of competition is seen to be more about application intelligence, biological compatibility, and spray system relevance.

List of Key Companies

- BASF SE

- Clariant AG

- Corteva Agriscience

- Croda International PLC

- Evonik Industries AG

- Helena Chemical Company

- Miller Chemical & Fertilizer, LLC.

- Nufarm Limited

- Solvay SA

- The Dow Chemical Company

Industry Developments

- June 2025: BASF commissioned a world-scale hexamethylenediamine unit in France. The strategic move boosted polyamide 6.6 intermediates for packaging films.

- May 2025: Corteva partnered with NEVONEX to integrate sensor data and precision software for real-time adjuvant optimization.

- March 2025: BASF and Agmatix launched an AI tool to detect soybean cyst nematode stress via aerial imagery. According to BASF, the tool enables targeted adjuvant-supported sprays.

- March 2025: Sell Agro launched its first new product, Oleum Sell. Oleum Sell is a high-purity mineral oil free of sulfur, aromatics, and naphtha.

Agricultural Adjuvants Market Segmentation

By Source Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Petroleum-based

- Bio-based

By Formulation Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Emulsifiable Concentrate

- Suspension Concentrate

By Crop Type Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Oilseeds & Pulses

- Soyabean

- Others

- Cereals & Grains

- Rice

- Wheat

- Corn

- Others

- Fruits & Vegetables

- Others

By Adoption Stage Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Tank-Mix

- In-Formulation

By Function Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Utility Adjuvants

- Buffers/Acidifiers

- Water conditioners

- Compatibility agents

- Antidrift agents

- Antifoam agents

- Others

- Activator Adjuvants

- Oil-based Adjuvants

- Surfactants

By Application Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Herbicides

- Fungicides

- Insecticides

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Agricultural Adjuvants Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 4.32 billion |

|

Market Size in 2026 |

USD 4.52 billion |

|

Revenue Forecast by 2034 |

USD 6.63 billion |

|

CAGR |

4.9% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Agricultural Adjuvants Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The agricultural adjuvants market was valued at USD 4.32 billion in 2025 and is projected to reach USD 6.63 billion by 2034.

The market is expected to grow at a CAGR of 4.9% from 2026 to 2034.

Asia Pacific accounted for the largest market share in 2025. This is supported by large agricultural output and high pesticide consumption in the region.

North America is expected to witness the fastest growth. Rising adoption of precision agriculture and herbicide resistance management are driving the regional market growth.

A few of the key players in the market include BASF SE, Clariant AG, Corteva Agriscience, Croda International PLC, Evonik Industries AG, Helena Chemical Company, Miller Chemical & Fertilizer, LLC., Nufarm Limited, Solvay SA, and The Dow Chemical Company.

The utility adjuvants segment is projected to grow fastest owing to the rising demand for drift control and spray-quality enhancement.

The herbicides segment accounts for the largest market share. The widespread use of herbicides in large-scale crop production contributes to the segment’s leading market share.

They are used to improve the performance of crop protection applications. They do so by enhancing wetting, spreading, and drip control.

They are gaining popularity due to the growing preference for sustainable, biodegradable, and biologically compatible crop protection products by growers, regulators, and manufacturers.

Precision agriculture increases the need for high-performance adjuvants, as the technology requires tighter control of droplets and spray coverage.

Page last updated on:

Apr-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

Market size estimates (USD Mn/Bn)

Segment-wise distribution (%)

Growth metrics (CAGR %)

Final Outputs

Structured tables and charts

Segment-level datasets

Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements