Air Traffic Management Market Size, Industry Report, 2026 - 2034

REPORT DETAILS

What is Air Traffic Management Market Size?

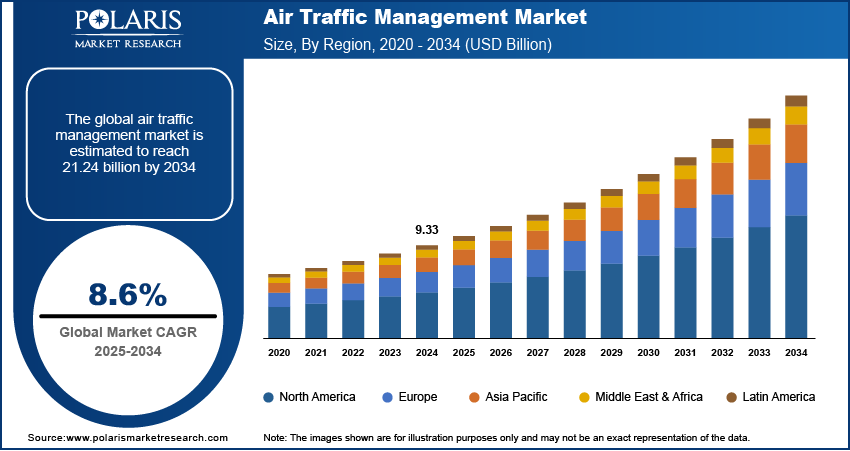

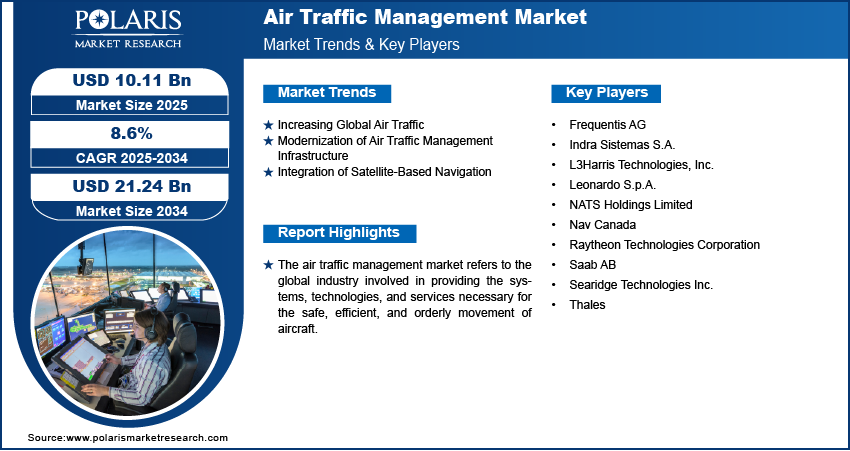

The global air traffic management market size was valued at USD 10.11 billion in 2025 and is expected to grow at a CAGR of 8.6% from 2026 to 2034. The market is driven by growing global air traffic, ongoing infrastructure modernization, and the integration of satellite-based navigation systems, all aimed at enhancing safety, efficiency, and capacity in air travel.

Market Statistics

Key Takeaways

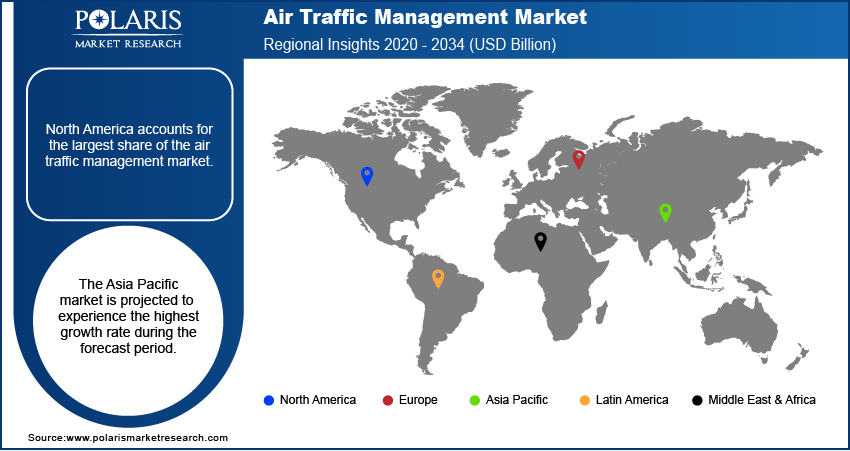

- North America has the largest market share of 34.85% due to a mature aviation industry, higher air traffic, and the relentless modernization of aviation infrastructure.

- Asia Pacific currently has the fastest growth rate of CAGR 8.9% market due to increased air travel in countries such as China and India, as well as large investments in airport construction.

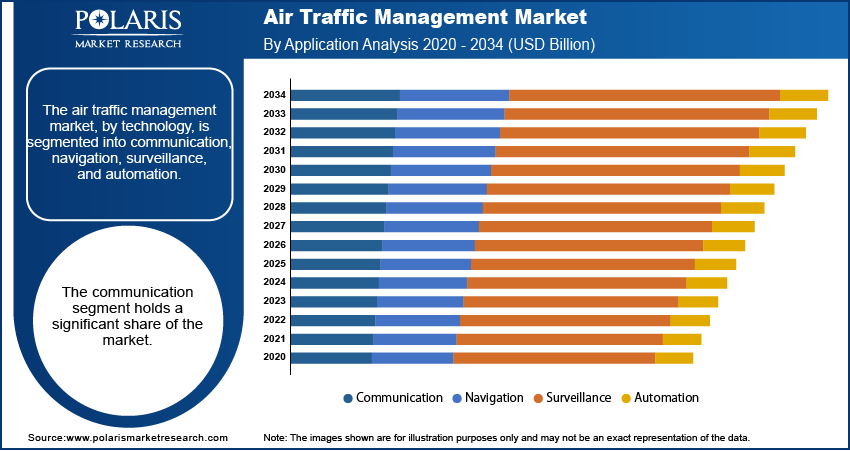

- The communication segment holds a major share of 33.65% due to its essential role in enabling safe, real-time information exchange between controllers and aircraft.

- The air traffic services sector dominates with 59.99% share due to its essential role in flight safety, including worldwide control, flight information, and alerting services.

- The commercial area is expected to grow at the highest rate of CAGR 8.7% due to increased traffic and expanded air routes, driving greater interest in advanced ATM technology.

Industry Dynamics

- Rising global air travel, driven by economic growth and disposable income, is increasing demand for advanced traffic management systems.

- Modernization efforts with new technologies, such as ADS-B and IP-based communication systems, are boosting the adoption of air traffic management systems.

- Satellite navigation, including GNSS and GBAS, enables accurate flight path planning and safer operations, supporting better traffic flow management.

- The increasing demand for efficient routes and safety in congested airspace creates scope for the global adoption of digital and satellite-based navigation.

- High implementation costs and complex infrastructure upgrades can limit adoption, especially in developing regions with limited financial and technical resources.

AI Impact on Air Traffic Management Market

- It enhances air traffic flow by predicting congestion and making real-time route adjustments.

- It assists air traffic controllers in several ways; first, by reducing manual tasks, thereby reducing human error.

- It increases safety by using data analysis to identify potential conflicts or issues before they escalate.

- It helps with predictive maintenance of systems and equipment, minimizing downtime.

- AI enables effective coordination among airports, air carriers, and control centers by optimizing data.

The introduction of artificial intelligence in air traffic management happens in a cascading manner. Most air traffic systems start as decision support systems that provide recommendations rather than full air traffic management automation, since air traffic management operations need well-validated, explainable, and highly trusted outcomes for air traffic managers or air traffic controllers. The most prominent areas of growth in air traffic management include congestion forecasting, arrival and departure sequencing, anomaly identification, and predictive maintenance.

The air traffic management (ATM) market enables integration between air navigation service providers (ANSPs), airports, airlines, and the defense sector. This enables the integration of operations such as air traffic control (ATC), flight information, and alerting, along with technology associated with communication, navigation, and surveillance (CNS) systems and automation. ATM modernization is an important area of focus because ATM expenditures are heavily influenced by factors such as growth in air traffic volumes, capacity constraints, and modernization requirements. The ATM market is anticipated to expand at a significant CAGR driven by these factors.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

What’s Included in Air Traffic Management (ATM Ecosystem Map)

The air traffic management market comprises solutions and services that ensure airplanes remain in motion while flowing smoothly through the global airspace. Air traffic management encompasses air traffic control solutions that direct aircraft movement throughout their journey and airspace management solutions that allocate the use of global airspace. Air traffic flow management solutions help prevent airport congestion and minimize potential delays.

The ATM ecosystem has four main areas of operation: ATS, supporting aircraft management, flight information, and notification; ATFM, managing demand and resources, flight planning, and management systems; and ASM, managing airspace efficiently. The four areas function within CNS systems, including communication systems, GNSS, GBAS, and ADS-B, which are located throughout the airspace for surveillance. The CNS systems are supported by automation that enables efficient air traffic management by reducing traffic flow, enhancing capacity, reducing delays, and minimizing risk.

The continuous rise in global air travel, driven by economic recovery and higher incomes, especially in developing nations, is the prime mover of the air traffic management industry. An increase in the number of flights also requires improved ATM systems to ensure air transport is both safe and efficient. On the other hand, modernization processes such as satellite navigation systems (GPS), ADS-B, and digital communication systems enable flight tracking, shorter routes, and greater capacity in the airspace. A focus on improving safety and making flight operations smoother also increases demand for modern ATM systems and services.

Air Traffic Management Systems: Benefits vs Challenges

| Aspect | Benefits | Challenges |

| Safety | Enhances aircraft separation, reduces collision risk, enables real-time monitoring and incident prevention | System failures, cybersecurity risks, and dependency on automation can impact safety if not managed properly |

| Efficiency | Optimizes flight routes, reduces fuel consumption, improves airspace utilization, and increases traffic handling capacity | Integration complexity, high implementation costs, and uneven adoption across regions can limit efficiency gains |

| Delays | Improves traffic flow management, minimizes congestion, and supports better scheduling and coordination | Weather disruptions, airspace congestion, and system limitations can still cause delays despite advanced systems |

| Interoperability | Facilitates seamless coordination between countries, supports global standards, and improves cross-border air traffic flow | Lack of standardization, legacy systems, and compatibility issues between regions hinder smooth interoperability |

Source: Polaris Market Research Analysis

Market Dynamics

Increasing Global Air Traffic

With the expansion of economies, traveling has become easier, leading to global air traffic growth and ultimately affecting the sector capacity and airspace. According to the Joint ACI World-ICAO Passenger Traffic Report, global passenger traffic totaled 9.5 billion in 2024 and would breach the 12-billion mark by 2030, fueled by rapid expansion in Asia Pacific and the Middle East. Pressure on this aspect, in turn, requires increased ATM automation. Purchasers seek solutions that would help reduce delays, increase predictability, and enhance runway and sector throughput, thereby accelerating the market for air traffic management.

Modernization of Air Traffic Management Infrastructure

Governments and airports globally are updating air traffic management infrastructure by implementing the latest technology in the sector. Some of the latest developments in India include the installation of IP-based voice communication control systems, an Aeronautical Message Handling System covering the entire country, ADS-B ground stations, a Performance-Based Navigation (PBN) system, and a Central Air Traffic Flow Management (C-ATFM) system. Such advancements in the air traffic management sector are thus driving growth in the Indian air traffic management industry.

Within the context of modernization of air traffic management systems, the following three considerations often apply to ATM system procurement. These considerations are interoperability, so that the systems can seamlessly share information. Then there's the matter of systems that are safe and meet the necessary standards. Finally, there's the matter of lifecycle support. Companies with strong system integration and lifecycle support capabilities will likely benefit the most from large-scale contracts and thus help advance the market.

Integration of Satellite-Based Navigation

Satellite navigation systems, such as GNSS, enable accurate positioning and timekeeping, ensuring flight safety and efficiency. In fact, satellite navigation has become standardized in the modern aircraft industry because it provides the accurate information required for flight management. This has enabled airline operators to plan their flights along accurate routes and adjust them in real time, especially at the point of landing. In this regard, the FAA also explains that satellite navigation technology, such as GBAS, has enhanced satellite navigation by expanding its support. This development has fuelled the growth of the air traffic management industry.

With the increasing use of GNSS and satellite navigation, greater importance is being placed on GNSS resilience. The aviation sector is thus incorporating redundancy into its systems through multi-sensor surveillance, backup navigation, and communication systems. This will, in effect, make aviation communication systems more secure, with minimal jamming or interference possible. Consequently, there is increasing expenditure on developing effective solutions, such as GBAS, surveillance, and automation systems, for the safe separation of aircraft, even in challenging environments.

What Limits Growth of Air Traffic Management Industry?

Higher Cost & Complexity in Implementation

One market restriction is the high cost of upgrades. An air traffic management system involves complex components, advanced hardware and software, and highly qualified personnel. Budget constraints, especially in developing countries, pose a significant challenge for most airports and aviation organizations. System integration is another factor that impedes the deployment of these air traffic management systems.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Insights

Market Assessment – By Technology Type

The market is segmented by technology into communication, navigation, surveillance, and automation. The communication segment accounted for a major share of 32.1% in 2025. Communication equipment plays a crucial role in smooth air traffic movement because communication between control and flights is conducted through it. Communication equipment includes voice and data communication services for flights and clearances, as well as other core networks. As flights increase every day, communication security keeps this segment prominent in the market.

It is projected that automation will be the fastest-growing category over the next few years, driven by its increasing adoption to enhance efficiency and alleviate the workload on air traffic controllers. It includes automated control tools, flow management solutions, and decision-support systems, each designed to enable controllers to make quick, accurate decisions. With increasing air traffic complexity and consequently greater demands for efficiency, advanced automation will grow.

Every form of technology has its specific use in air traffic management. The communication system includes voice, data links, and IP-based communication to ensure the safe transmission of information. The navigation system uses GNSS and ground-based systems for routing. The surveillance system relies on radar, ADS-B, and multilateration for effective aircraft monitoring and air traffic management. The automation segment encompasses conflict resolution, sequencing, and decision support for effective air traffic control.

Market Assessment – By Component

The market is segmented by component into hardware and software & solutions. The air traffic management hardware market comprises radars, radios, sensors, and tower equipment, which are critical for surveillance and communication coverage. The air traffic management software market comprises ATC automation platforms, flow management solutions, and data processing and analytics tools that help optimize efficiency and decision-making.

The air traffic management services market comprises system integration, maintenance, and managed services, which are critical for seamless operations. It has been observed that the software and services segments are expected to grow faster as older systems at airports and air traffic management organizations are modernized.

Market Evaluation– By Airspace

The market is segmented by airspace into air traffic services, air traffic flow management, airspace management, and aeronautical information management. The air traffic services segment has the largest market share. It comprises services such as air traffic control, flight information, and alerting services. These services ensure aircraft remain safe during transit. For these reasons, this segment holds the largest market share.

The air traffic flow management segment is projected to grow at the highest rate during the forecast period. This growth has been driven by the need to use the airspace efficiently and address congestion, particularly in busy areas. Air traffic flow management systems employ sophisticated technology to manage aircraft movement and optimize capacity and demand. This increases operational efficiency by reducing flight delays. With passenger traffic growing, the adoption rate of such systems will continue to rise.

Air traffic services ensure the safe separation of aircraft and provide necessary flight information and alerting. Air traffic flow management helps minimize delays by balancing demand and capacity across busy airspace. Airspace management aims to allocate airspace for both civil and military operations efficiently. Aeronautical information management aims to ensure that accurate and timely data are available to best support flight planning and other decisions that enhance safety, efficiency, and air traffic operations.

Market Assessment – By Airport Size

The market is segmented by airport size into small, medium, and large airports. The large airport market accounts for the largest market share. Large airports handle a high volume of flights, so they require sophisticated air traffic management solutions to operate efficiently. The extensive infrastructure and advanced technologies required by these major aviation and aviation analytics hubs contribute to the expansion of the large airport segment.

The large airport segment is also expected to grow the fastest over the forecast period. This may be attributed to increasing air travel and more passengers using major airports. Such demand encourages improvements in efficiency, safety, and capacity at large airports, therefore, inviting continued investment in advanced air traffic management systems and infrastructure upgrade programs.

There are growing line-of-sight opportunities in UTM (unmanned traffic management) and UAM (Urban Air Mobility) that are being developed to support ATM (Air Traffic Management) vendors in expanding their coverage of surveillance, communication, and ATM automation solutions for managing these traffic types. This will ensure that separation in traffic between traditional aircraft and new Air Mobility vehicles can be maintained. Though still evolving, they are shaping long-term investments.

Market Assessment – By End Use

The market is bifurcated by end use into commercial and military. The commercial segment holds a larger share. This is attributable to the significantly higher volume of air traffic and the extensive network of commercial and smart airports and airlines operating globally. The need for advanced air traffic management systems to handle the vast number of commercial flights, ensure passenger safety, and optimize operational efficiency contributes to the commercial segment's dominant position.

The commercial segment is also expected to grow faster during the forecast period. The ongoing increase in air passenger traffic, coupled with the worldwide expansion of airline fleets and airport infrastructure, necessitates further investment in advanced air traffic management technologies. The demand for enhanced safety, efficiency, and capacity to accommodate the growing commercial air travel sector will continue to drive significant adoption and advancement of air traffic management solutions in this end-use segment.

Use Cases of Air Traffic Management Across Stakeholders

| Stakeholder | Key Use Cases | Benefits / Impact |

| Airlines | Flight planning and optimization, fuel-efficient routing, real-time flight tracking, delay management, fleet coordination | Reduces fuel costs, improves on-time performance, enhances operational efficiency, and supports better passenger experience |

| Airports | Runway scheduling, ground movement control, gate allocation, congestion management, integration with airport operations systems | Optimizes airport capacity, reduces turnaround time, minimizes congestion, and improves overall operational flow |

| Defense/Military Aviation | Airspace surveillance, mission planning, secure communication, coordination with civil aviation, threat detection and response | Enhances national security, ensures safe integration of military and civilian airspace, improves situational awareness and rapid response capabilities |

| Commercial Aviation [Air Navigation Service Providers (ANSPs)] | Air traffic control operations, airspace management, conflict detection and resolution, flow management, cross-border coordination | Ensures flight safety, maximizes airspace utilization, reduces delays, and supports seamless international operations |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

The air traffic management market is segmented by geography. The North American and European markets for air traffic management are well-established, supported by extensive aviation-sector infrastructure and stringent safety regulations. However, the Asia/Pacific region is emerging as a fast-growing market due to rising air travel and large investments in new airports. Additionally, Latin America and the Africa & Middle East markets have growth potential as their aviation industries develop and upgrade their technology infrastructure.

North America currently has the largest market share in the air traffic management market. North America has a fully developed aviation sector, highly congested airspace, and major technology suppliers. There are also strong safety regulations in place, with ongoing improvements in air traffic control, which help to promote the air traffic management market.

Modernization initiatives are shifting their focus to upgrading ATMs, increasing automation, enhancing surveillance, and ensuring reliable communication. The goal is to achieve greater predictability and alleviate congestion for high-density routes. Investment is concentrated on flow management systems that increase capacity and minimize delays, thereby re-emphasizing leadership in the North American air traffic management market.

The Asia Pacific market is projected to experience the highest growth rate during the forecast period. Asia Pacific is expanding rapidly, driven by increased air transport in China and India, as well as significant investments in new airport construction and the modernization of existing air traffic management systems. A greater number of air transport users and aircraft operators require more advanced air traffic management solutions. Economic growth and increasing air transport connectivity are factors that are encouraging adoption in the region.

In Asia Pacific region, growing demand for passengers, as well as the development of airport infrastructure, propels the move to adopt scalable surveillance, communications, and automation in an expanding air space in order to ensure safety. Nations with advanced plans to improve their airports focus on the development of tower and approach systems, ATFM systems, and modern AIM in order to ensure uniformity in operations and drive the Asia Pacific air traffic management market.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

A few major players actively contributing to the air traffic management industry include Thales; Indra Sistemas S.A.; Leonardo S.p.A.; Frequentis AG; Saab AB; Raytheon Technologies Corporation; L3Harris Technologies, Inc.; Nav Canada (a key service provider with in-house technology development); NATS Holdings Limited (also primarily a service provider with technology innovation); and Searidge Technologies Inc. These companies offer air traffic management services, including communication, navigation, surveillance, and automation systems. They respond to the ever-growing demands posed by the aviation industry.

The air traffic management industry comprises a diverse set of established companies operating globally, as well as niche technology firms. Innovation, product quality, system integration, and adaptability to deliver customized solutions tailored to geographic and airport conditions are among the drivers in this industry. The focus on next-generation air traffic management systems based on AI, machine learning, cloud, and other technologies has intensified in this industry to make operations more efficient, safe, and sustainable.

A competition in the air traffic management industry market key players category usually comprises four categories. First, some companies specialize in communication, navigation, and surveillance. Second, the category comprises companies that provide flow management and decision support solutions. Third, those that offer solutions for ‘digital tower,’ ‘video analytics solutions,’ and so on. Lastly, a few ‘innovators operate under the umbrella of an ANSP for solution development.’ Not too long ago, the assessment of ATM system suppliers has widened from simply evaluating the performance of the system itself to encompassing the degree to which it is integrated, is resilient against cyber threats, supports the ‘long-term strategy,’ or has ‘long-term support capabilities.’

Thales, headquartered in Courbevoie, France, offers a comprehensive suite of air traffic management solutions. Thales deals with air traffic control automation, communication, and surveillance, as well as navigation systems and digital solutions for airspace management. The firm is crucial to modernizing air traffic management services to enhance safety, capacity, and efficiency for both civilian and military air services.

Indra Sistemas S.A., located in Alcobendas, Spain, is another prominent player in the air traffic management ecosystem. The company provides a wide array of air traffic management products and services, encompassing air traffic control systems, radar and surveillance technologies, communication platforms, and air navigation services. Indra's solutions are designed to optimize air traffic flow, improve safety, and reduce environmental impact, making them a relevant provider for air navigation service providers and airport authorities worldwide.

List of Key Companies

- Frequentis AG

- Indra Sistemas S.A.

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- NATS Holdings Limited

- Nav Canada

- Raytheon Technologies Corporation

- Saab AB

- Searidge Technologies Inc.

- Thales

Industry Developments

January 2026: The Qatar Civil Aviation Authority (QCAA) announced that it had awarded Bayanat Engineering Qatar the delivery of a display system provided by Frequentis. It is an advanced platform that transforms how air traffic controllers see, interpret, and manage the nation’s airspace. (Source: frequentis.com)

January 2026: the SkyBridge Alliance selected Thales’s AI-powered TopSky ATC. It is a cyber-secured advanced air traffic control solution that is expected to power Europe’s ATM modernization. Air Navigation Service Providers (ANSPs), Estonia (EANS), and Finland (FTANS) had launched SkyBridge Alliance. The alliance aims to strengthen cooperation and harmonize operations. It is expected to enable efficiency and innovation in European air traffic management. (Source: thalesgroup.com)

These air traffic management developments underline three key investment themes: First, regional innovation hubs support the Indo-Pacific ATM deployment and collaboration. Second, satellite communications are being used to advance ATM modernization programs. Third, improvements in airport automation enhance operational efficiency in busy, growing air traffic environments.

Market Segmentation

By Airspace Outlook (Revenue – USD Billion, 2021–2034)

- Air Traffic Services

- Air Traffic Flow Management

- Airspace Management

- Aeronautical Information Management

By Technology Type Outlook (Revenue – USD Billion, 2021–2034)

- Communication Systems

- Navigation

- Surveillance

- Others

By Component Outlook (Revenue – USD Billion, 2021–2034)

- Hardware

- Software & Solutions

By Airport Size Outlook (Revenue – USD Billion, 2021–2034)

- Small Airport

- Medium Airport

- Large Airport

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- Commercial

- Military

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Air Traffic Management Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.11 Billion |

| Market Size in 2026 | USD 10.96 Billion |

| Revenue Forecast by 2034 | USD 21.24 Billion |

| CAGR | 8.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Air Traffic Management Market FAQ's

The global air traffic management market will reach around USD 21.24 billion by 2034. The industry is expanding at a CAGR of CAGR 8.6% during 2026–2034. The significant factors fuelling the growth of thismarket are increasing air passenger traffic and the development of airport infrastructure.

The North American market has the largest share of the global market due to its mature aviation infrastructure and high air traffic. The Asia Pacific market has the second-fastest growth rate, driven by increased air travel in countries such as China and India.

It is buoyed by the regulatory requirements for ADS-B solutions, modernization initiatives such as NextGen and SESAR, and other developments in the use of commercial UAVs that must be integrated with UTM. The use of AI-driven automation also helps bolster airspace safety, efficiency, and traffic flow.

The leading providers of air traffic management solutions are Thales, Raytheon Technologies, L3Harris Technologies, Indra Sistemas, Saab AB, Honeywell, and Frequentis. Such firms are well-established, supporting their solutions with hardware and software and offering long-term support agreements with Air Navigation Service Providers.

Market drivers include technologies such as ADS-B, which accurately locate aircraft. Artificial Intelligence-based flow management optimizes traffic. Remote digital towers offer operational flexibility, while satellite surveillance enhances navigation. Cloud technology ensures scalability for ATM solutions, while drone traffic management ensures safe flights in the airspace.

ATM, or Air Traffic Management, refers to the larger picture encompassing ATC, ATFM, ASM, and AIM. All the procedures and systems that guarantee the safety and efficiency of air traffic fall under ATM. ATC, or Air Traffic Control, refers to the part of ATM that directs the aircraft in all stages of flight. This clears the confusion between the two terms: ATM and ATC.

ATFM or air traffic Flow management. It helps manage the flow between demand and capacity to minimize flight congestion and delays. As air traffic increases, particularly in route congestions, ATFM plays a crucial role in maintaining flights on schedule.

Today, ATMs depend on software platforms and automation tools. Airports and ANSPs require continuous improvement and the integration of systems. This boosts demand for ATM software and services, such as flow management and decision support.

As more technologies, such as digital communications, satellite navigation, and automation, are incorporated in the ATM system, this also has implications for its potential exposure to threats. Cybersecurity in the aviation sector is paramount to ensuring flights take place in a safe and reliable environment.

Download Sample Report of Air Traffic Management Market

Please fill out the form to request a customized copy of the research report.