Market Overview

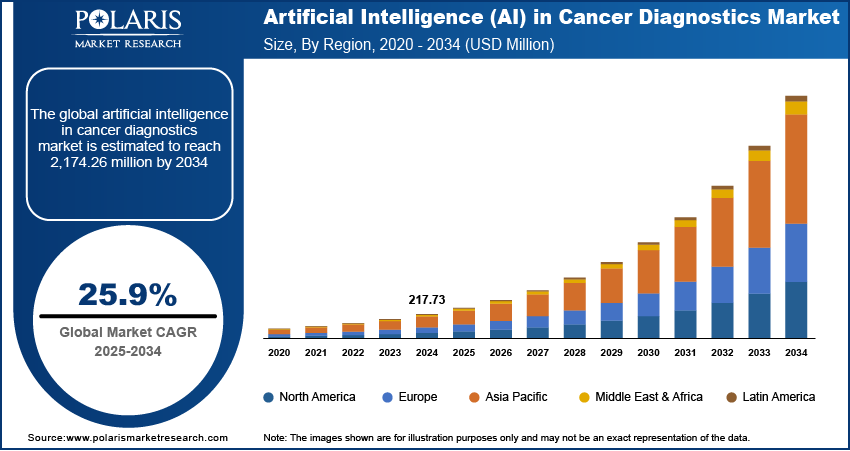

The artificial intelligence (AI) in cancer diagnostics market size was valued at USD 217.73 million in 2024, growing at a CAGR of 25.9% during 2025–2034. The rising incidence of cancer and increasing demand for precision medicine are a few of the key factors fueling the market growth.

Key Insights

- The screening and diagnosis segment accounted for the largest market share. The segment’s dominance is primarily attributed to the rising integration of AI technologies in pathology and medical imaging.

- The lung cancer segment is registering the highest growth rate. The growing incidence of cancer, along with increased demand for precise diagnostic methods, drives the robust growth of the segment.

- The hospital segment dominates the market, owing to the widespread integration of AI algorithms into hospital workflows.

- North America led the market in 2024. The regional market dominance is primarily fueled by its advanced healthcare infrastructure and major investments in healthcare IT solutions.

- Asia Pacific is registering robust growth, driven by growing healthcare investments and the rapid adoption of AI technologies in the region.

Industry Dynamics

- The rising prevalence of cancer worldwide has fueled the need for advanced diagnostic tools that allow for early detection and improve patient outcomes, driving market growth.

- Advancements in deep learning and machine learning, which have improved the efficiency and accuracy of cancer diagnostics, are fueling market expansion.

- The expansion of AI-based diagnostic solutions in emerging economies is expected to boost market development in the coming years.

- Lack of standardized protocols may hinder market growth.

Market Statistics

2024 Market Size: USD 217.73 million

2034 Projected Market Size: USD 2,174.26 million

CAGR (2025-2034): 25.9%

North America: Largest Market in 2024

AI Impact on Artificial Intelligence in Cancer Diagnostics Market

- Advanced AI systems process complex imaging and clinical datasets to identify cancer cases with high accuracy.

- Deep learning models uncover minute abnormalities and early-stage signs that conventional approaches may overlook.

- AI-driven diagnostic tools support oncologists in tailoring treatment strategies by integrating diverse patient health information.

- With continuous algorithm refinement, AI enhances diagnostic precision and contributes to improved survival rates and care quality.

To Understand More About this Research: Request a Free Sample Report

The artificial intelligence in the cancer diagnostics market demand is rising due to the increasing adoption of AI-driven technologies in oncology. AI-powered diagnostic tools enhance early cancer detection, improve diagnostic accuracy, and reduce human error, contributing to better patient outcomes.

Key drivers of AI in the cancer diagnostics market growth include the rising prevalence of cancer, the growing demand for precision medicine, and advancements in machine learning and deep learning algorithms. Additionally, the integration of AI with medical imaging and pathology is streamlining cancer diagnosis. A few artificial intelligence in the cancer diagnostics market trends include the expansion of AI-based diagnostic solutions in emerging economies, regulatory advancements supporting AI adoption in healthcare, and increasing investments in AI-driven oncology research.

Artificial Intelligence in Cancer Diagnostics Market Dynamics

Increasing Prevalence of Cancer

The rising incidence of cancer globally is a significant driver for the adoption of artificial intelligence in cancer diagnostics. According to the World Health Organization, approximately 20 million new cancer cases were reported in 2022, leading to 9.7 million deaths. This escalating burden necessitates advanced diagnostic tools to facilitate early detection and improve patient outcomes. AI technologies offer the potential to analyze complex medical data efficiently, aiding in the early detection of cancerous conditions, thereby propelling AI in cancer diagnostics market development.

Advancements in AI Algorithms and Imaging Technologies

Recent advancements in AI algorithms, particularly in machine learning and deep learning, have enhanced the accuracy and efficiency of cancer diagnostics. The integration of AI with advanced imaging technologies, such as MRI and CT scans, has improved the precision of cancer detection, which encourages the adoption of these advanced integrated devices. For instance, AI-powered platforms are being deployed to assist radiologists in interpreting scans, thereby accelerating diagnosis and reducing the workload on healthcare professionals. Hence, rising advancements in AI algorithms and imaging technologies are expected to offer artificial intelligence in the cancer diagnostics market opportunities during the forecast period.

Government Initiatives and Funding

Government support through funding and policy initiatives plays a crucial role in driving artificial intelligence in cancer diagnostics market expansion. The US government's Cancer Moonshot initiative aims to reduce cancer mortality by investing in AI data analysis to establish a nationwide ecosystem for data sharing among patients, doctors, and researchers. Such initiatives encourage the development and implementation of AI-driven diagnostic tools, fostering innovation in the cancer diagnostics.

-in-cancer-diagnostics-market-infographic.webp)

Artificial Intelligence in Cancer Diagnostics Market Segment Insights:

AI in Cancer Diagnostics Market Assessment by Application

The artificial intelligence in cancer diagnostics market, by application, is segmented into screening & diagnosis, tumor identification, surveillance, and treatment. The screening and diagnosis segment held the largest market share in 2024. This prominence is attributed to the integration of AI technologies in medical imaging and pathology, which enhances early cancer detection and diagnostic accuracy. AI algorithms assist in analyzing complex imaging data, facilitating the identification of malignancies at initial stages, thereby improving patient outcomes. The demand for AI-driven screening and diagnostic tools is further propelled by the increasing global cancer incidence and the need for efficient diagnostic solutions.

The tumor identification segment is experiencing the highest growth rate within this market. Advancements in machine learning and deep learning algorithms have significantly improved the precision of tumor detection and characterization. AI applications in tumor identification aid in distinguishing between benign and malignant tumors, assessing tumor boundaries, and evaluating metastatic spread. This rapid growth is driven by the continuous development of AI models capable of processing vast datasets to provide accurate tumor assessments, thereby supporting personalized treatment planning and monitoring.

Artificial Intelligence in Cancer Diagnostics Market Evaluation by Cancer Type

The artificial intelligence in cancer diagnostics market, by cancer type, is segmented into breast cancer, prostate cancer, lung cancer, colorectal cancer, cervical cancer, and others. The breast cancer segment dominated the market share in 2024. This is attributed to the high incidence of breast cancer globally, necessitating advanced diagnostic tools for early detection and treatment. AI technologies have been instrumental in enhancing the accuracy of mammography interpretations, leading to improved patient outcomes. According to the World Health Organization, approximately 2.3 million women were diagnosed with breast cancer in 2020, underscoring the critical need for effective diagnostic solutions.

The lung cancer segment is experiencing the highest growth rate within this market. This rapid expansion is driven by the increasing prevalence of lung cancer and the demand for precise diagnostic methods. AI applications in lung cancer diagnostics, such as the analysis of imaging data from CT scans, have shown promise in early detection and accurate tumor characterization. The integration of AI in these processes aids in identifying malignancies at earlier stages, thereby facilitating timely interventions and improving survival rates.

Artificial Intelligence in Cancer Diagnostics Market Outlook by End Use

The artificial intelligence in cancer diagnostics market, by end use, is segmented into hospitals, diagnostic centers, medical research institutes, contract research organizations, and others. The hospital segment holds the largest market share. This dominance is attributed to the widespread integration of AI algorithms into hospital workflows, addressing the shortage of healthcare professionals and enhancing the speed and accuracy of cancer diagnoses. Hospitals are increasingly adopting AI-powered diagnostic tools to improve patient outcomes and streamline operations. For instance, Addenbrooke’s Hospital in the UK implemented Microsoft's InnerEye, a deep-learning solution that significantly reduced CT processing time and treatment planning by 90%.

-in-cancer-diagnostics-market-segment.webp)

Artificial Intelligence in Cancer Diagnostics Market Regional Outlook

By region, the report provides AI in cancer diagnostics market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America held the largest market share in 2024. This dominance is attributed to the region's advanced healthcare infrastructure, significant investments in healthcare IT solutions, and the presence of key industry players. The increasing adoption of AI technologies in oncology, supported by substantial funding for AI development, further propels market growth in North America. Additionally, the rising prevalence of cancer and heightened patient awareness contribute to the expanding utilization of AI-driven diagnostic tools in the region.

The Europe AI in cancer diagnostics market is experiencing substantial growth, driven by significant investments and technological advancements. For instance, the European Investment Bank recently provided a €15 million loan to Spanish biotech company Amadix to develop innovative blood tests for early cancer detection. Additionally, institutions such as CERN are adapting AI models to revolutionize cancer treatment, collaborating with hospitals across Europe to enhance diagnostic accuracy and patient outcomes.

The Asia Pacific artificial intelligence in the cancer diagnostics market is rapidly expanding due to increasing healthcare investments and the adoption of AI technologies. Countries such as China and Japan are at the forefront of integrating AI into medical diagnostics to improve early cancer detection rates. The growing prevalence of cancer in the region, coupled with supportive government initiatives, is propelling the adoption of AI-driven diagnostic solutions. This trend is expected to continue, contributing significantly to advancements in cancer diagnostics and patient care.

-in-cancer-diagnostics-market-region.webp)

Artificial Intelligence in Cancer Diagnostics Market – Key Players and Competitive Analysis Report:

In the artificial intelligence in the cancer diagnostics market, several companies are actively contributing to advancements in early detection and treatment. Notable entities include Microsoft Corporation, IBM Corporation, Siemens Healthineers, GE Healthcare, and Tempus Labs, Inc. These organizations are at the forefront of integrating AI into healthcare to enhance diagnostic accuracy and patient outcomes.

Other significant contributors such as PathAI; Paige.AI, Inc.; and Kheiron Medical Technologies Limited specialize in developing AI-powered pathology solutions to improve cancer diagnosis. Additionally, companies such as Aidoc and Zebra Medical Vision are focusing on AI applications in medical imaging, aiding in the early detection of various cancers. Furthermore, Flatiron Health and Guardant Health are leveraging AI to analyze real-world oncology data and develop liquid biopsy technologies, respectively. These efforts collectively aim to revolutionize cancer diagnostics by providing more precise and less invasive testing options.

Microsoft Corporation and IBM Corporation are prominent entities in AI in the cancer diagnostics market. The company has been actively developing AI solutions to enhance cancer detection and treatment. In collaboration with Paige, a digital pathology provider, Microsoft is working on creating the world's largest image-based AI model for cancer detection. This model is being trained on up to four million digitized microscopy slides across various cancer types, utilizing Microsoft's advanced supercomputing infrastructure. The initiative aims to improve the accuracy and efficiency of cancer diagnosis, potentially leading to earlier detection and treatment for patients.

IBM Corporation has also made significant strides in applying AI to healthcare, particularly in oncology. IBM's Watson for Oncology and Watson for Genomics platforms assist physicians in providing personalized, evidence-based cancer care by analyzing vast amounts of medical data to identify tailored treatment options. These tools support clinical decision making by offering insights into various treatment possibilities based on extensive medical literature and patient data.

List of Key Companies in Artificial Intelligence in Cancer Diagnostics Market

- Aidoc Medical Ltd.

- DeepMind Technologies Limited

- Enlitic, Inc.

- Flatiron Health, Inc. (A subsidiary of Roche)

- GE Healthcare Technologies Inc.

- Guardant Health, Inc.

- IBM Corporation

- Kheiron Medical Technologies Limited

- Microsoft Corporation

- Paige.AI, Inc.

- PathAI, Inc.

- Qure.ai Technologies Private Limited

- Siemens Healthineers AG

- Tempus Labs, Inc.

- Zebra Medical Vision Ltd.

Artificial Intelligence in Cancer Diagnostics Industry Developments

- March 2025: Philips revealed an expanded partnership with Ibex to fast-track the use of AI-powered digital pathology, addressing the worldwide shortage of pathologists and the increasing cancer patient population.

- September 2024: PathAI, Inc. launched MET Predict on the AISight Image Management System (IMS). This AI-driven algorithm assists pathologists in detecting non-small cell lung cancer (NSCLC) tumors that may present MET exon 14 skipping (METex14) or MET amplification using H&E whole slide images.

- September 2023: Microsoft announced a partnership with Paige to develop the world's largest image-based AI model for cancer detection. The model is being trained on up to four million digitized microscopy slides across multiple cancer types, utilizing Microsoft's advanced supercomputing infrastructure. Once deployed, it is expected to enhance the accuracy and efficiency of cancer diagnosis, potentially leading to earlier detection and treatment for patients.

Artificial Intelligence in Cancer Diagnostics Market Segmentation

By Application Outlook (Revenue – USD Million, 2020–2034)

- Screening & Diagnosis

- Tumor Identification

- Surveillance

- Treatment

By Cancer Type Outlook (Revenue – USD Million, 2020–2034)

- Breast Cancer

- Prostate Cancer

- Lung Cancer

- Colorectal Cancer

- Cervical Cancer

- Others

By End Use Outlook (Revenue – USD Million, 2020–2034)

- Hospitals

- Diagnostic Centers

- Medical Research Institute

- Contract Research Organization

- Other

By Regional Outlook (Revenue – USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Artificial Intelligence (AI) in Cancer Diagnostics Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 217.73 million |

|

Market Size Value in 2025 |

USD 273.58 million |

|

Revenue Forecast by 2034 |

USD 2,174.26 million |

|

CAGR |

25.9% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market size was valued at USD 217.73 million in 2024 and is projected to grow to USD 2,174.26 million by 2034.

The market is projected to register a CAGR of 25.9% during the forecast period.

North America held the largest share of the market in 2024.

Several companies in the market are actively contributing to advancements in early detection and treatment. A few notable entities include Microsoft Corporation, IBM Corporation, Siemens Healthineers, GE Healthcare, and Tempus Labs, Inc. These organizations are at the forefront of integrating AI into healthcare to enhance diagnostic accuracy and patient outcomes.

The screening & diagnosis segment accounted for the largest share of the market in 2024.

Artificial intelligence in cancer diagnostics refers to the use of AI technologies, including machine learning, deep learning, and computer vision, to improve the accuracy, efficiency, and speed of cancer detection and diagnosis. AI-powered algorithms analyze medical imaging, pathology slides, and genomic data to identify cancerous cells, predict tumor progression, and assist healthcare professionals in making informed clinical decisions. These AI solutions help reduce diagnostic errors, enhance early detection, and personalize treatment plans by processing vast amounts of medical data. The integration of AI in cancer diagnostics aims to improve patient outcomes and streamline healthcare workflows.

A few key trends in the market are described below:

Page last updated on:

Aug-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements