Overview

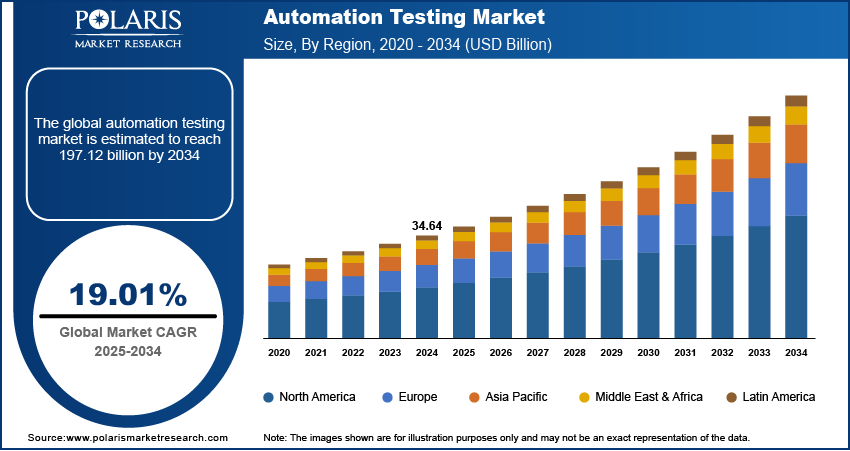

The global automation testing market size was valued at USD 36.44 billion in 2025. The market is projected to grow at a CAGR of 14.6% during 2026 to 2034. Key factors driving demand for automation testing include increasing software complexity, widespread use of mobile applications, and integration of artificial intelligence and machine learning.

Key Insights

- Based on the service segment, the implementation services segment is expected to be the most significant revenue contributor in the global market.

- North America had the largest revenue share in 2025, due to the widespread dispersion of technology suppliers.

- Asia Pacific is expected to witness the fastest CAGR in the global market during the forecast period, owing to the increasing adoption of mobile and web-based apps and cloud-based services.

Industry Dynamics

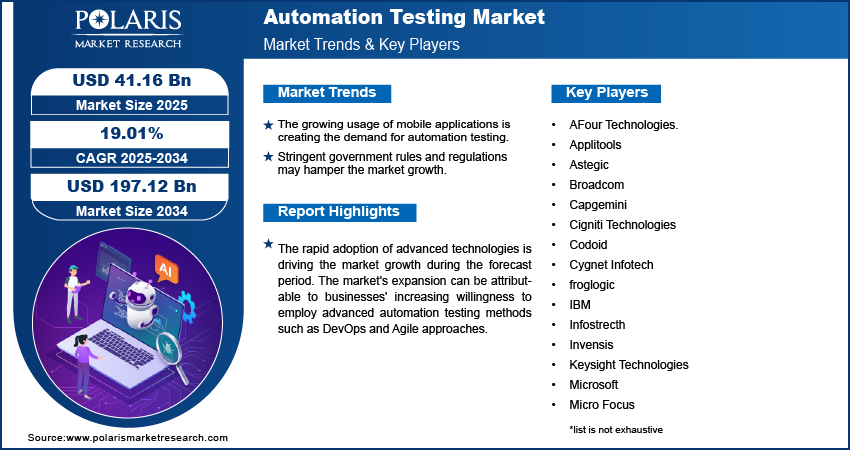

- The growing usage of mobile applications is creating the demand for automation testing.

- The increasing development of online gaming platforms is further propelling the market growth.

- The ongoing digital transformation across the globe will create lucrative automation testing market opportunities in the coming years.

- Stringent government rules and regulations hamper the market growth.

Market Statistics

- 2025 Market Size: USD 36.44 Billion

- 2034 Projected Market Size: USD 124.61 Billion

- CAGR (2026–2034): 14.6%

- North America: Largest Market Share

Impact of AI in Automation Testing Market

- AI helps in smarter test case generation and faster defect detection.

- The technology improves test coverage through predictive analytics.

- It allows testers to create scripts with minimal coding.

- The technology transforms the market through self-healing test automation, where scripts automatically adapt to UI changes without manual intervention

- AI-powered platforms enable intelligent test prioritization, reducing execution time while improving defect detection accuracy.

The rapid adoption of advanced technologies is driving the market growth during the forecast period. The market's expansion can be attributable to businesses' increasing willingness to employ advanced automation testing methods such as DevOps and Agile approaches. These approaches assist firms in shortening the time it takes to commercialize their software solutions by reducing the time it takes to automate analysis. Quick bug elimination, post-deployment debugging, and software integration of unforeseen changes are also provided by Agile, and DevOps approaches. These advantages are anticipated to increase demand for elegant and DevOps-based automated analysis across various sectors, including monetary services, telecommunications, automotive, government, and public. To stay competitive, different market competitors are focusing on building test automation solutions based on Agile and DevOps methodologies.

Each test cycle produces a large amount of data that can be utilized to discover and resolve test failures. The data from each test run can be sent back to the AI algorithms. With the growing benefits of incorporating AI into analysis, the need for technology has risen. With more AI being used in the development of test tools, the tools will self-heal at runtime. Self-healing test automation analysis is expected to be one of the most popular automation analysis trends in the coming years. Thus, market players are introducing new products into the automation testing market.

Modern technologies such as IoT, AI, and machine learning continue to expand. The automated analysis market has tremendous potential to evaluate advanced technical applications. The majority of the company's work is managed digitally and through rule-based software. When it comes to dealing with serious situations, this strategy is limited.

Automation Testing ROI & Cost Economics

Automation testing delivers a strong ROI by reducing manual effort, improving software quality, and accelerating release cycles. Although organizations face initial costs for tools, setting up frameworks, infrastructure, and training, these expenses are balanced by long-term savings. Agile test automation facilitates quick regression testing during short sprints. It reduces testing time by 40 to 70% and shortens release delays.DevOps automation testing enhances cost efficiency by incorporating automated tests into CI/CD pipelines. It reduces rework and defect-related costs after releases. As automation grows, the cost per test execution goes down. This enables wider test coverage across devices, browsers, and APIs without significant cost increases. Most companies see a return on investment within 6 to 18 months, especially in high-frequency release settings like SaaS and mobile apps. Overall, automation testing moves quality assurance away from labor-heavy methods to a more scalable and predictable cost model.

Automation Testing Market Drivers?

Rapid Adoption of Advanced Technologies

The use of technologies such as AI, machine learning, cloud computing, the Internet of Things, and big data analytics is increasing in many industries. Enterprises deploy complex, distributed applications that require faster release cycles and higher reliability. It makes manual testing impractical. DevOps automation testing has become essential as organizations integrate continuous integration/continuous deployment (CI/CD) pipelines to accelerate innovation while maintaining quality. For instance, AI-powered test automation tools help predict areas prone to defects, improve test coverage, and allow self-repairing test scripts. Similarly, cloud-native and microservices architectures need testing frameworks that can scale and automate. These frameworks should check APIs, performance, and security in various environments. Agile test automation helps with frequent code changes by allowing quick regression testing. This ensures that new technologies can be launched confidently and without delaying the time to market. Thus, the growing use of new technologies fuel the automation testing industry growth.

Increasing Adoption of Mobile and Web-Based Services

Numerous industries like banking, retail, healthcare, and media increasingly adopt mobile and web-based services. Users seek smooth performance across devices, browsers, and operating systems. This makes applications more complex and requires more testing. Agile test automation allows development teams to check frequent updates, user interface changes, and integrations during short sprint cycles. For example, digital banking apps need automated functional, security, and performance testing to maintain consistent service during feature updates. Likewise, e-commerce platforms depend on DevOps automation testing to validate web and mobile experiences during busy events like flash sales. Automation testing tools ensure compatibility across browsers, validate responsive designs, and find bugs more quickly. This enables the continuous delivery of reliable mobile and web-based services at scale. Thus, growing adoption of mobile and web-based services drives the market growth.

Automation Testing Market Restraints

Stringent Government Rules and Regulations

Governments establish data regulatory norms in various economies to protect data from unwanted access. Regulations such as GDPR in Europe, CCPA in the U.S., and emerging data protection laws in Asia require strict controls over how test data is accessed, stored, and processed. Other rules include the Health Insurance Portability and Accountability Act (HIPAA) in the U.S. and the Data Protection Directive in the European Union. Industry players must follow several regional rules regarding data storage, security, and privacy. Data stored on-premises is entirely secure/. However, data stored on the cloud is exposed to security risks. Ensuring data security in automation testing becomes more complex when organizations use production-like datasets for functional and performance testing. Automated test scripts often handle sensitive personal or financial information. This raises compliance risks if data masking, encryption, or access controls are not strong enough. These regulatory requirements can slow down DevOps automation testing efforts. Extra validation, audits, and approvals are necessary before launching automated frameworks. As a result, organizations may experience higher implementation costs and longer testing cycles. This undermines the speed and flexibility that agile test automation seeks to provide. Therefore, strict government rules about data protection and privacy hinder the growth of the automation testing market.

By Service

Automation testing by service is segmented into advisory and consulting, planning and development, support and maintenance, documentation and training, implementation, managed services, and others. The implementation services segment is expected to hold the global market revenue share in the coming years. With the help of implementation services, automation may be readily integrated into an existing software automation testing infrastructure. As a result, successful implementation of automated analysis solutions necessitates connecting the solutions with various hardware components and evaluating the overall system's functionality.

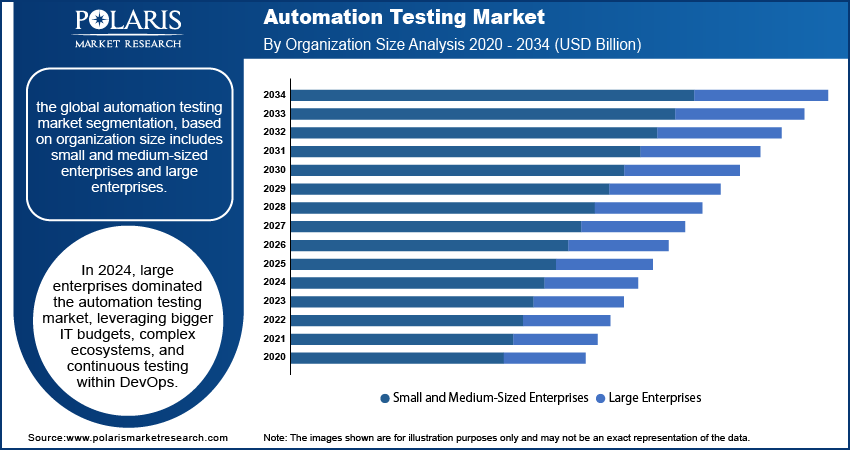

By Organization Size

Automation testing by organization size is segmented into small and medium-sized enterprises and large enterprises. The large enterprises segment dominated the revenue share in 2025. Large enterprises consist of complex systems, multiple applications, and a high volume of test cases. Thus, these enterprises adopt automation testing to enhance efficiency and reduce manual effort. Automation testing also help them increase test coverage and ensure the quality of software applications.

Automation Testing Adoption Patterns: Large Enterprises vs. SMEs

|

Parameter |

Large Enterprises |

SMEs |

|

Adoption Drivers |

Digital transformation, risk mitigation, regulatory compliance |

Faster time-to-market, cost efficiency, competitive pressure |

|

Automation Scope |

Enterprise-wide automation across web, mobile, API, and performance testing |

Focused automation for core applications and regression testing |

|

Approach |

Mature agile test automation and DevOps automation testing integration |

Selective automation aligned with agile teams |

|

Tool Preference |

Mix of commercial and enterprise-grade platforms |

Open-source and cloud-based subscription tools |

|

Investment Level |

High upfront investment with long-term ROI focus |

Lower initial spend with faster payback expectations |

|

CI/CD Integration |

Deep integration into complex CI/CD pipelines |

Basic CI/CD or partial pipeline integration |

|

Key Challenges |

Test maintenance at scale, data security in automation testing |

Skill gaps, budget constraints, limited infrastructure |

Geographic Overview

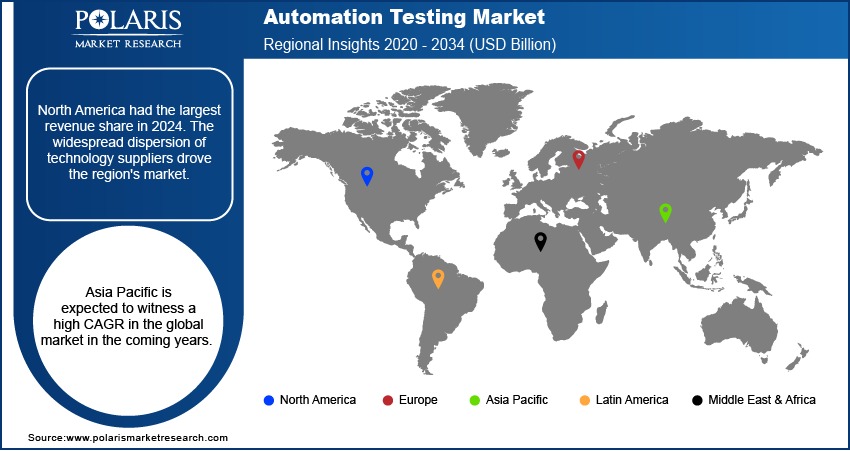

The automation testing market by region is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America held the largest revenue share in 2025. The widespread dispersion of technology suppliers drove the North America automation testing market. Smart consumer electronics such as smart TVs, home appliances, and laptops are becoming increasingly popular in the U.S. are fueling market demand. In smart consumer gadgets, software, web applications, and operating systems (OS) are intricately linked. As these smart consumer products become more generally accepted, the demand for test automation services in the region will increase.

The Asia Pacific automation testing market is expected to witness a high CAGR in the global market in the coming years. The Asia Pacific region is the most promising since it includes essential economies like Australia, Japan, Singapore, China, New Zealand, and Hong Kong, all of which have significant growth potential for automation analysis organizations. Governments in the region are implementing initiatives to fasten the adoption of new technologies such as artificial intelligence and machine learning, automation, the Internet of Things, mobile and web-based apps, cloud-based services, and other innovations, which is driving the demand for automation testing.

Competitive Insight

- Sauce Labs

- AFour Technologies.

- Invensis

- Keysight Technologies

- Broadcom

- Applitools

- Cygnet Infotech Astegic

- Mobisoft Infotech

- Parasoft

- ProdPerfect

- Microsoft

- Cigniti Technologies

- Infostrecth

- QA Source

- Codoid

- froglogic

- Capgemini

- Micro Focus

- IBM

- QA Mentor

- Ranorex

- Smartbear Software

- Testim.io

- Tricentis

- Thinksys

- Worksoft.

Recent Developments

- April 2025: ETSI announced the 11th UCAAT User Conference on Advanced Automated Testing, highlighting key themes such as model-based testing, cloud and mobile testing, and security-focused automation.

- March 2025: Cognizant unveiled a USD 1 billion AI enablement initiative aimed at boosting productivity in automated testing and embedded engineering.

- March 2025: SEALSQ Corp pivoted toward developing Quantum-Resistant chips, redefining security testing requirements for upcoming generations of applications.

- June 2023: Microsoft partnered with Leapwork to deliver advanced test automation solutions for users of Microsoft Dynamics 365 and Microsoft Power Platform. Leapwork’s AI-driven, visual, and codeless platform enables non-technical users to efficiently design and manage automated tests. This approach supports continuous, end-to-end testing across applications, minimizes disruptions during regular software updates, and ensures consistent delivery of high-quality software.

Automation Testing Market Segmentation

By Testing Type Outlook (Revenue – USD Billion, 2021–2034)

- Static Testing

- Dynamic Testing

- Functional

- Non-Functional

- Performance

- API

- Security

- Compatibility

- Compliance

- Usability

By Service Outlook (Revenue – USD Billion, 2021–2034)

- Advisory and Consulting

- Planning and Development

- Support and Maintenance

- Documentation and Training

- Implementation

- Managed Services

- Others

By Organization Size Outlook (Revenue – USD Billion, 2021–2034)

- Small and Medium-Sized Enterprises

- Large Enterprises

By Vertical Outlook (Revenue – USD Billion, 2021–2034)

- Banking

- Financial Services

- Insurance

- Automotive

- Defense and Aerospace

- Healthcare and Lifesciences

- Retail

- Telecom and IT

- Logistics and Transportation

- Energy and Utilities

- Media and Entertainment

- Other Verticals

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- France

- Germany

- UK

- Italy

- Netherlands

- Spain

- Austria

- Asia Pacific

- China

- India

- Japan

- Malaysia

- South Korea

- Indonesia

- Rest of Asia Pacific

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

- Rest of Middle East & Africa

Automation Testing Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 36.44 Billion |

|

Market Size in 2026 |

USD 41.74 Billion |

|

Revenue Forecast by 2034 |

USD 124.61 Billion |

|

CAGR |

14.6% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2022–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion, 2021–2034 and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global automation testing market is expected to reach USD 124.61 billion by 2034, at a CAGR of 14.6%.

AI and machine learning enable intelligent test case generation, predictive analysis, and adaptive testing. Integration of these technologies reduces maintenance time significantly and enhances test automation.

The banking segment leads automation testing adoption, driven by digital transformation requirements and regulatory compliance requirements.

Agile and DevOps adoption and cloud-based testing platforms drive automation testing demand. Also, increasing mobile applications and continuous deployment practices fuel the market growth.

Cloud-based automation tools offer scalability, cost-effectiveness, flexibility, and accessibility. These features make them attractive for SMEs and startups seeking efficiency.

Page last updated on:

Jan-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements