Automotive Camera Market Size, Share Global Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Overview

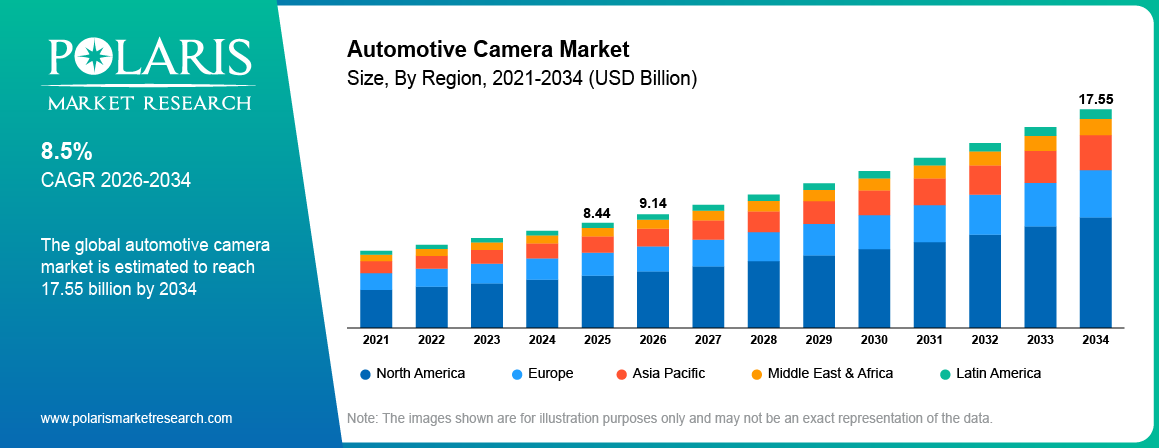

The global automotive camera market is estimated around USD 8.44 Billion in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by increasing vehicle safety regulations and rising ADAS adoption. The market is projected to grow at a CAGR of 8.5% during the forecast period.

Key Takeaways:

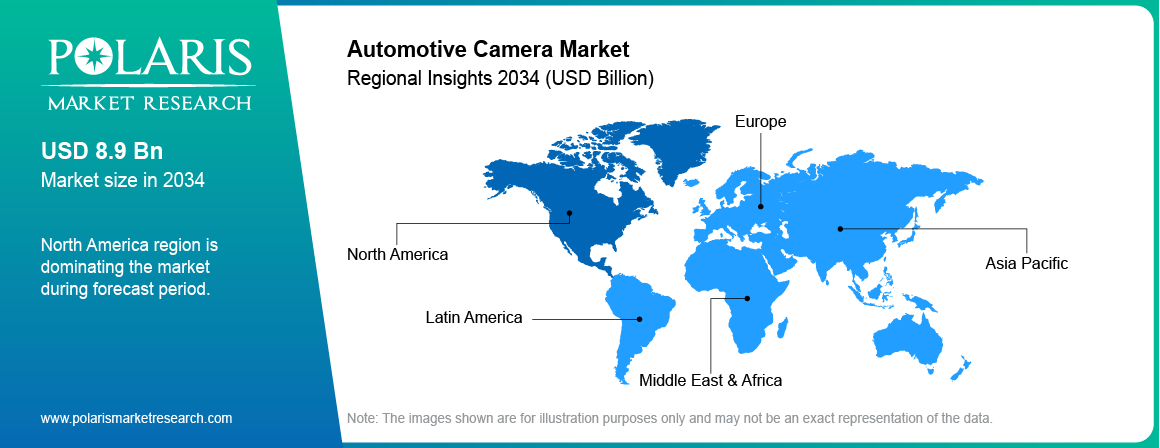

- North America accounted for the largest regional share of around 36.9% in 2025, driven by strong ADAS adoption, regulatory mandates for safety features, and increasing integration of automotive vision technologies.

- Asia Pacific is projected to grow at a CAGR of 8.2%, driven by large-scale vehicle production, EV expansion, and increasing adoption of ADAS technologies across China and Japan.

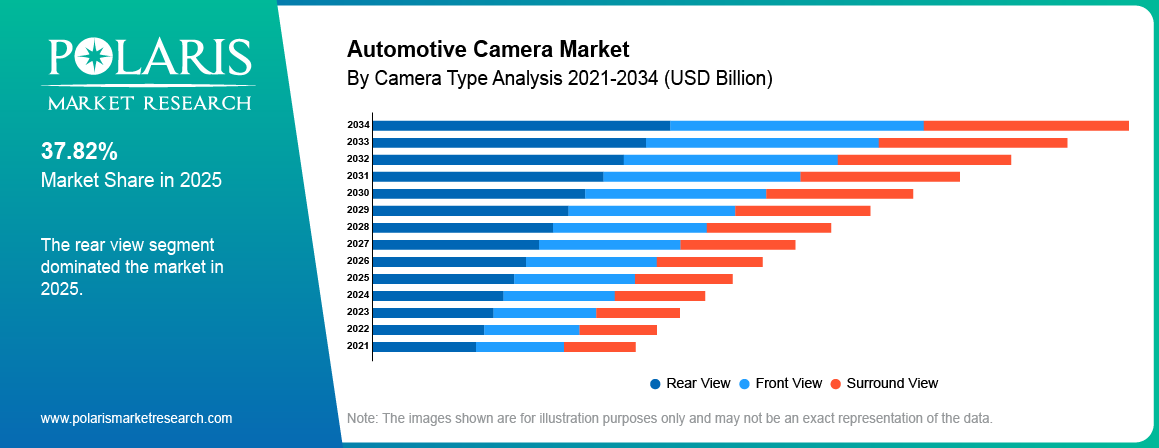

- By Camera Type, Rear View segment accounted for the largest share of approximately 48.6% in 2025, supported by mandatory safety regulations and widespread integration in passenger vehicles.

- By Vehicle Type, Commercial Vehicles segment is projected to grow at a CAGR of 7.9%, driven by increasing focus on fleet safety, driver monitoring, and expansion of logistics and transportation services.

- By Technology, Infrared Cameras segment is projected to grow at a CAGR of 8.7%, driven by rising demand for night vision, driver monitoring, and AI-enabled safety systems.

- By Application, Parking Assist segment accounted for the largest share of approximately 39.5% in 2025, supported by increasing adoption of rear and surround view systems for improved vehicle safety.

Market Statistics

- 2025 Market Size: USD 8.44 Billion

- 2034 Projected Market Size: USD 17.55 Billion

- CAGR (2026-2034): 8.5%

- North America: Largest market in 2025

Industry Dynamics

- Increasing vehicle safety regulations are expanding adoption of automotive cameras across passenger and commercial vehicles.

- Rising development of autonomous and ADAS enabled vehicles is increasing demand for automotive vision technology.

- Performance limitations in adverse weather conditions restrict reliability of camera-based sensing systems.

- Advancements in AI automotive camera systems create long term opportunities in the global automotive camera market.

What is the Automotive Camera Market?

The automotive camera industry refers to the structured production and supply of imaging systems used in vehicles for safety and monitoring applications. The ecosystem comprises camera sensors, lenses, electronic control units, and software that provide integration for the camera. The market comprises various types of vehicles, including passenger cars and commercial vehicles that require improved visibility.

The market comprises rearview cameras, surround view cameras, frontview cameras, interior monitoring cameras, and sideview cameras. These systems combine image sensors, lenses, processors, and embedded software to support driver assistance and vehicle monitoring functions. Manufacturers provide integrated camera modules through OEM supply chains and aftermarket distribution channels.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The automotive camera industry differs from radar, LiDAR, and ultrasonic sensing systems. Radar measures distance through radio signals, while LiDAR uses laser scanning to map surroundings. Ultrasonic sensors support short range obstacle detection. Automotive cameras capture visual information that supports lane monitoring, parking assistance, and driver monitoring functions.

Drivers & Opportunities

Increasing vehicle safety regulations: Stricter vehicle safety regulations are increasing the demand for automotive cameras in modern vehicles. Governments in the US, Europe, and Asia are mandating safety features such as rear-view cameras and driver monitoring systems. These policies are supporting the adoption of ADAS camera market technologies and strengthening automotive camera market growth.

Growth of autonomous vehicles: The development of autonomous and semi-autonomous vehicles is increasing the need for advanced imaging systems. Automotive cameras support lane detection, object recognition, and traffic monitoring functions. For instance, in February 2026, Uber introduced Uber Autonomous Solutions, a platform that offers infrastructure, fleet management, and operational support for the commercialization of autonomous mobility and delivery services worldwide. This trend is growing the market for automotive camera technology for self-driving vehicles.

Restraints & Challenges

Performance Limitations in Adverse Weather: The performance of automotive camera technology is limited in adverse weather. Rain, fog, snow, and low light environments reduce image clarity and detection accuracy. These limitations affect the performance of ADAS camera market systems that depend on visual data.

Opportunity

AI vision systems in automotive cameras: Artificial intelligence is creating new opportunities for AI automotive camera systems in modern vehicles. AI in image processing enables better object detection, pedestrian detection, and traffic sign recognition. For example, in March 2026, Nexar announced its partnership with Vay to integrate Vay’s remotely driven vehicle fleet with its BADAS predictive AI model. This enables better risk detection, ensuring better safety in remote driving and autonomous services. The technologies help in real-time decision-making in ADAS and autonomous driving.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report offers detailed coverage of the automotive camera market by camera type, vehicle type, technology, and application to help readers identify the fastest expanding and most attractive demand segments.

By Camera Type

-

Rear view

Rear View Cameras dominated the market in terms of market share in 2025, due to mandatory safety regulations for rear view cameras in passenger cars. The government of the US, Europe, and Asia has implemented regulations that require rear view cameras in newly manufactured vehicles. This regulatory support is increasing the demand for ADAS cameras in modern vehicles.

-

Surround view

Surround view cameras segment is projected to grow at the fastest CAGR during the forecast period, due to increasing adoption of advanced driver assistance systems in premium and mid-range vehicles. These systems provide a 360-degree view around the vehicle and improve parking safety.

By Vehicle Type

-

Passenger vehicles

The passenger vehicles segment has the highest market share in 2025, due to the increased adoption of safety features in personal mobility vehicles. The automotive industry is increasingly using multiple cameras for ADAS and driver monitoring. Increasing consumer preference for vehicle safety features is strengthening demand for automotive cameras in this segment.

-

Commercial vehicles

Commercial vehicles segment is projected to grow at the fastest CAGR during the forecast period, due to increasing focus on fleet safety and driver monitoring systems. The logistics sector is increasingly using camera technology to prevent accidents and monitor vehicles. Growth in transportation and delivery services is supporting expansion of the segment.

By Technology

-

CMOS cameras

The CMOS camera technology has the highest market share in 2025, due to low power consumption and cost-effectiveness in automotive camera technology. These sensors provide high resolution image capture required for ADAS camera market applications. Increasing integration in passenger vehicles is supporting segment dominance.

-

Infrared cameras

Infrared cameras segment is projected to grow at the fastest CAGR during the forecast period, due to rising demand for improved night vision and driver monitoring systems. These cameras can be used to detect objects and improve driver vision in low-light conditions. Increased R&D in AI automotive camera technology is driving the market.

By Application

-

Parking assist

Parking assist had the highest market share in 2025. This is due to the adoption of rear view and surround view cameras in passenger vehicles. The rear view and surround view cameras help to increase the driver’s visibility, thus minimizing the chances of collision while parking. The increasing demand for ADAS safety features is contributing to this market segment’s growth.

-

Driver monitoring systems

Driver monitoring systems segment is projected to grow at the fastest CAGR during the forecast period, due to increasing focus on driver safety and fatigue detection technologies. Automakers are integrating interior automotive vision technology to track driver attention and alertness. Safety regulations and autonomous vehicle development are supporting the growth of this segment.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

North America Market Assessment

North America automotive camera market dominated in 2025, driven by strong adoption of ADAS technologies across the US and Canada. In January 2026, Teledyne FLIR OEM announced the launch of its Tura, the industry’s first ASIL-B automotive-grade thermal infrared camera, designed to improve night vision capabilities and pedestrian detection for ADAS and autonomous vehicles. Rear view cameras and driver monitoring systems must be integrated into new vehicles, as mandated by safety regulations. This regulatory push is strengthening the US automotive camera market and supporting demand for automotive vision technology.

Asia Pacific Automotive Camera Market Insights

Asia Pacific automotive camera market is projected to grow at the fastest CAGR during the forecast period, owing to large scale vehicle production and EV expansion. The International Energy Agency reported that China accounted for over 70% of global electric car production in 2024, while Chinese OEMs represented more than 80% of the country’s domestic EV manufacturing, rising from around two-thirds in 2021. China and Japan are major automotive manufacturing hubs that are increasing adoption of ADAS cameras. This trend is strengthening the China automotive camera market and the Japan automotive camera market.

Europe Automotive Camera Market Overview

Europe was the second-largest market for automotive cameras driven by strict vehicle safety regulations and OEM innovation. Countries like Germany, France, and the UK are moving towards the integration of ADAS and automated driving systems. For example, the EU’s General Safety Regulation (EU) 2019/2144, effective from July 2022, has been updated in 2024 to include the integration of advanced driver assistance systems like intelligent speed control, autonomous emergency braking, and driver monitoring in all new vehicles to ensure road safety and the integration of automated driving.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The competitive landscape is affected by the development of automotive vision technology that is integrated with ADAS systems. Companies are focusing on delivering high-quality image sensors and AI-based object detection capabilities in camera modules. Partnerships with automotive manufacturers are boosting the adoption of automotive camera systems.

Leading companies in the automotive camera market are Robert Bosch GmbH, Continental AG, Magna International Inc., Valeo SA, Denso Corporation, Aptiv PLC, Mobileye Global Inc., OMNIVISION Technologies Inc., ON Semiconductor Corporation, Sony Semiconductor Solutions Group, Samsung Electro-Mechanics Co., Ltd., ZF Friedrichshafen AG, and many more.

Future of Automotive Camera Technology

AI automotive camera systems are improving perception capabilities in modern vehicles. Machine vision automotive technology supports object detection, traffic sign recognition, and pedestrian identification through advanced image processing. Automakers are using AI-based camera modules to improve decision accuracy in ADAS systems as well as driver monitoring systems.

Autonomous vehicle camera technology is evolving with the development of next generation imaging systems. Increasing high resolution sensors and multi-camera architectures help to increase environmental awareness in vehicles. Continuous investment in machine vision automotive platforms is strengthening the role of cameras in autonomous driving systems.

Key Players

- Aptiv PLC

- Continental AG

- Denso Corporation

- Magna International Inc.

- Mobileye Global Inc.

- OMNIVISION Technologies Inc.

- ON Semiconductor Corporation

- Robert Bosch GmbH

- Samsung Electro-Mechanics Co., Ltd.

- Sony Semiconductor Solutions Group

- Valeo SA

- ZF Friedrichshafen AG

Industry Developments

- February 2026: MCNEX launched automotive-grade QHD front and rear cameras powered by Valens’ VA7000 A-PHY chipsets that transmit high-resolution video over unshielded or low-cost cables, reducing vehicle wiring complexity and cost for ADAS applications.

- October 2025: OMNIVISION released the OX08D20, an 8MP CMOS image sensor using TheiaCel Technology for exterior automotive camera applications. The camera is designed for low light, motion, and high dynamic range imaging for ADAS and autonomous driving.

- January 2024: Leopard Imaging introduced their Hyperlux LP camera products using the LI-AR0830-YUV-MIPI and LI-AR2020-MIPI at CES 2024. The camera provides high-quality image capture, increased dynamic range, and ultra-low power consumption for automotive applications.

Automotive Camera Market Segmentation

By Camera Type Outlook (Revenue, USD Billion, 2021-2034)

- Rear View

- Front View

- Surround View

By Vehicle Type Outlook (Revenue, USD Billion, 2021-2034)

- Passenger vehicles

- Commercial vehicles

By Technology Outlook (Revenue, USD Billion, 2021-2034)

- CMOS Cameras

- HDR Cameras

- Infrared Cameras

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Lane Departure Warning

- Blind Spot Detection

- Parking Assist

- Driver Monitoring Systems

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automotive Camera Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 8.44 Billion |

| Market Size in 2026 | USD 9.14 Billion |

| Revenue Forecast by 2034 | USD 17.55 Billion |

| CAGR | 8.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Automotive Camera Market FAQ's

The global market size was valued at USD 8.44 Billion in 2025 and is projected to grow to USD 17.55 Billion by 2034.

North America dominates due to strong adoption of ADAS technologies and strict vehicle safety regulations.

Major applications include lane departure warning, blind spot detection, parking assist, and driver monitoring systems.

A few of the key players in the market are Robert Bosch GmbH, Continental AG, Magna International Inc., Valeo SA, Denso Corporation, Aptiv PLC, Mobileye Global Inc., OMNIVISION Technologies Inc., ON Semiconductor Corporation, Sony Semiconductor Solutions Group, Samsung Electro-Mechanics Co., Ltd., ZF Friedrichshafen AG, and others.

The factors propelling growth include increasing vehicle safety regulations and rising development of autonomous vehicles.

Download Sample Report of Automotive Camera Market

Please fill out the form to request a customized copy of the research report.