Battery Energy Storage System Market Size, Share Report 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

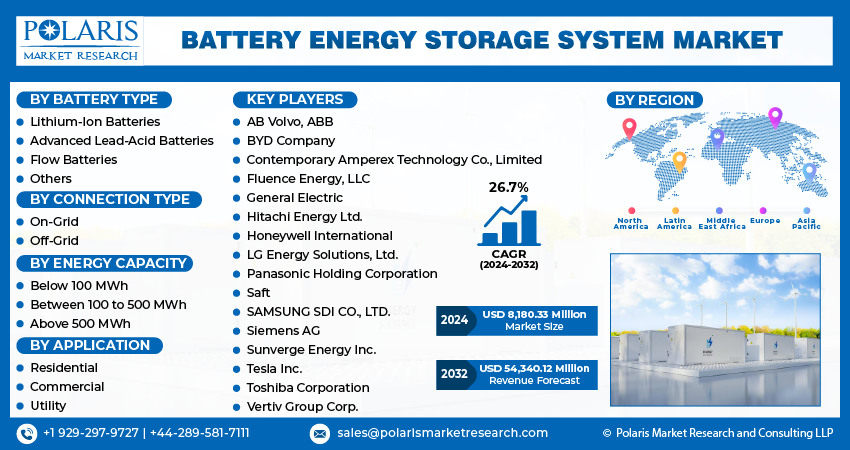

The global battery energy storage system market size was valued at USD 103.80 billion in 2025. It is projected to grow at a CAGR of 26.8% from 2026 to 2034. Growing renewable energy integration and grid modernization initiatives are driving demand.

Battery energy storage systems (BESS) are stationary storage devices designed for electricity storage and subsequent discharge to meet reliability needs. They facilitate the integration of renewable power sources, reduce the cost of power use during peak hours, and address other needs at the utility, commercial, industrial, and residential levels. Most of these installations are based on 2-hour and 4-hour systems, which are quite instrumental in determining their usage needs, project returns, and other aspects.

Key Insights

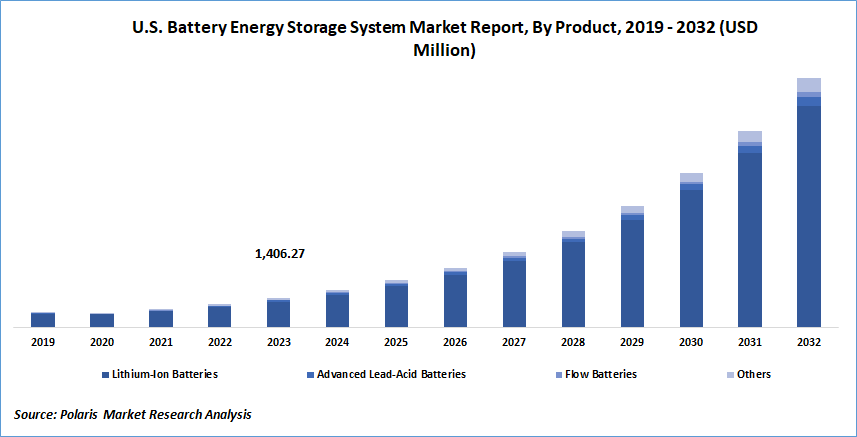

- The lithium-ion batteries segment accounted for the largest battery energy storage system market share in 2025. This is due to the extensive application of lithium-ion BESS in residential, commercial, and utility-scale usage.

- In 2025, the above 500 MWh segment dominated the market due to increasing deployment rates of utility-scale battery storage to enhance grid stability and meet the requirements of mega factories and other high-load scenarios. There is also an increasing need for 4+ hour configurations to meet the needs of grids that require a high degree of flexibility to achieve deeper reductions in renewable curtailment rates.

- The Asia Pacific market has grown rapidly, driven by the expansion of renewable energy, demand for grid stability, and government policies that promote clean energy.

- The North America region is also expected to grow as industrial demand for power backup installations rises.

Industry Dynamics

- Cost savings for the mass-scale BESS projects can be achieved through mass procurement and optimal manufacturing, leading to higher demand in the global market.

- The shift of the world towards low-carbon power has resulted in rapid growth of the market, driven by investment in green energy dreams.

- The increasing need to integrate renewable energy sources represents a major market opportunity.

- High capital and support infrastructure costs and production complexities may limit market expansion.

Market Statistics

2025 Market Size: USD 103.80 billion

2034 Projected Market Size: USD 881.46 billion

CAGR (2026-2034): 26.8%

Asia Pacific: Largest Market Share

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The rise in demand for BESS is driven by ongoing grid upgrades, the growing adoption of lithium-ion battery systems, and the shift toward fossil-fuel-free economies. Moreover, the revolution in renewable energy is also contributing to the growth of the battery energy storage system market. Expected growth in home electricity use is attributed to rising disposable incomes and the global rise in remote work.

Key trends shaping this market include the rapid increase in revenue-enabled BESS use cases, such as frequency regulation, ancillary services, energy arbitrage, and peak shaving, which improve project economics, enhance investment visibility, and speed up procurement cycles. Increased restrictions in safety and compliance are driving greater adoption of standard test tools and codes, such as UL 9540/UL 9540A and NFPA 855. This is influencing permitting timelines and system design choices.

Energy storage systems are crucial for ensuring an uninterrupted power supply during peak hours. They receive help through government financial incentives, which include the California Self-Generation Incentive Program (SGIP). The initiatives aim to improve the technology used in residential energy storage systems. Residential energy storage systems will see growing demand due to reduced costs and the rising adoption of renewable energy sources. Solar has been instrumental in the development of residential BESS.

The implementation of large BESS projects enables manufacturers to achieve cost savings through their extensive production operations and project implementation processes. The major projects require substantial quantities of batteries and components. This results in cost savings through bulk purchasing and efficient manufacturing operations, thereby boosting worldwide BESS market demand. For instance, in November 2022, Harmony Energy Income Trust plc, a UK-based investment company, successfully commissioned the Bumpers Battery Energy Storage System (BESS) project in Buckinghamshire. The project has a capacity of 99 MW / 198 MWh. The accomplishment establishes the project as the largest battery energy storage system in Europe.

The dual power system of the project represents a major step forward in clean energy technology development, adding to Harmony Energy Income Trust's total power capacity of 277.5 MW/555 MWh from its five operational projects. The system is one of Europe's principal BESS installations, capable of supplying electricity to around 300,000 homes in the United Kingdom for 2 hours. The Bumpers BESS system will function as an essential component that provides balancing services to support the U.K. electricity grid, using a Tesla 2-hour Megapack. The project was developed by Harmony Energy, while Tesla took charge of building it, and Autobidder will handle project operations through its algorithmic trading system, which belongs to Tesla. NHOA, previously known as Engie EPS , secured a contract in May 2022 to create a 30MWh Battery Energy Storage System in Peru. The BESS project will be established at the Chilca thermal power plant, which has an 800MW capacity, located in Peru. The system operates to deliver vital primary frequency regulation support required by Peru's national grid.

The energy storage system deployments demonstrate that grid-scale battery storage technology enhances operational flexibility by storing surplus renewable energy and delivering additional electricity during peak demand. The projects show how system integrators and energy management systems enable organizations to participate effectively in grid services.

What’s Driving Battery Energy Storage Systems Demand?

Rising Shift Towards Low-Carbon Energy Generation

The world is increasingly transitioning to low-carbon energy. There have been investments in green energy objectives. This is supporting the growth of the BESS market. Its use in residential, non-residential, and utility segments for storing energy from solar and wind power is evident. Major technologies used in BESS, such as flow batteries, solid-state batteries, pumped hydro, and thermal energy, are facilitating energy storage. The initiatives taken by various organizations to build new energy plants with low emissions, using large-scale infrastructure for BESS, are expected to boost the industry in a positive manner.

For example, in March 2021, a global clean energy technology firm, Pacific Green, announced a contract with the infrastructure project developer TUPA Energy to construct a 1.1 GW battery energy storage system in the U.K. as part of the TUPA contract. Furthermore, Pacific Green also secured rights to 100MW BESS for Kent, U.K., with the goal of completing the remaining 1,000MW by 2023. This demonstrates the increased drive for sustainable energy solutions and will continue to propel the uptake of battery energy storage systems in the energy market.

Increased focus on grid reliability and resiliency is a major growth driver for the BESS market, especially in regions where high demand peaks, extreme weather, and grid reliability are key issues. Battery energy storage systems help achieve fast response for backup power, shave peak demand for large commercial and industrial consumers, and support grid stability as the proportion of solar and wind increases.

What’s Restraining Market Development?

High Initial Installation Costs

Battery energy storage technologies, including lithium-ion batteries, flow batteries, and lead-acid batteries, need substantial investment capital due to the batteries’ ability to hold a charge relative to their density. Challenges are also noted regarding flow batteries. These batteries are limited due to their capital-intensive nature. In addition, supporting infrastructure contributes to the cost of system investment. This is particularly true for small- and medium-sized enterprises. Energy Subsidy Reform Facility's (ERSF) activities have been under scrutiny to enhance the effectiveness of subsidy reforms, including the issuing of topical reports and developing a database on the energy subsidy reforms conducted in 77 countries.

Apart from the initial investment costs, BESS project schedules are limited by interconnection queue, permitting, and safety compliance, which are jurisdiction-dependent. There are further costs involved in fire protection design, site layout optimization, and safety testing and validation, which can increase the total installed costs and commissioning schedules, especially for utility-scale BESS systems.

Despite the shortcomings facing BESS technologies, R&D efforts of companies have focused on improving their functionality to counter the challenges that affect their battery energy storage system market growth.

What Are the Emerging Technologies in the Market?

The driving factors for the BESS market include renewable energy systems and technological innovations. The increasing adoption of alternative chemistries is emerging as a new trend for the market. The trend of large-scale grid-scale storage systems powered by long-duration storage is increasing rapidly. The digitalization of battery systems enabled by AI and IoT is increasing operational efficiency in the industry. The incentives for grid-scale storage systems, along with the stringent policies of emerging markets, are driving large-scale adoption of BESS by key players worldwide.

The process of choosing technology now depends more on battery chemical trade-offs, which exist between LFP and NMC batteries. LFP batteries are widely favored in stationary energy storage due to their cost stability, longer cycle life, and stronger safety profile, while NMC continues to be used in select cases where higher energy density or specific supply chain considerations apply. The adoption of second-life EV batteries in mission-critical BESS applications becomes restricted because their performance shows variability, their warranty system is complex, and their safety standards require thorough testing.

| Trends | Description | Key Drivers Significance |

| Technology/chemistry diversification | Chemistries like solid-state batteries, sodium-ion batteries, and flow batteries are increasing in demand. |

|

| Scale-up of grid-scale & long-duration storage | The number of deployments of utility scale battery storage is rising quickly. There is need for longer-duration (4+ hour) storage. |

|

| Behind-the-meter (BTM) & distributed storage growth | Growth in residential, commercial, and industrial storage applications, colocated with solar, as well as for peak shaving/energy independence. |

|

| Digitalization, AI, and IoT integration | Advanced battery management systems, IoT technology, and cloud technology are increasingly integrated with BESS. |

|

| Cost declines & supply-chain evolution | Battery costs are reducing. There has been an expansion of manufacturing and supply chains worldwide. |

|

| Second-life batteries & circular economy | Retired EV batteries are being used for stationary storage. Recycling and reuse programs are growing. |

|

| Emerging markets & regulatory support | Expansion in Asia Pacific, Latin America, Africa. Governments are offering incentives and setting mandates for storage integration. |

|

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Report Segmentation

The market is primarily segmented based on battery type, connection type, energy capacity, application, and region. For stakeholders assessing the BESS market, battery type BESS segmentation shows chemical composition; connection type (on-grid or off-grid) defines the operational environment and system reliability needs; and energy capacity determines project size and operational economic aspects.

By Battery Type Insights

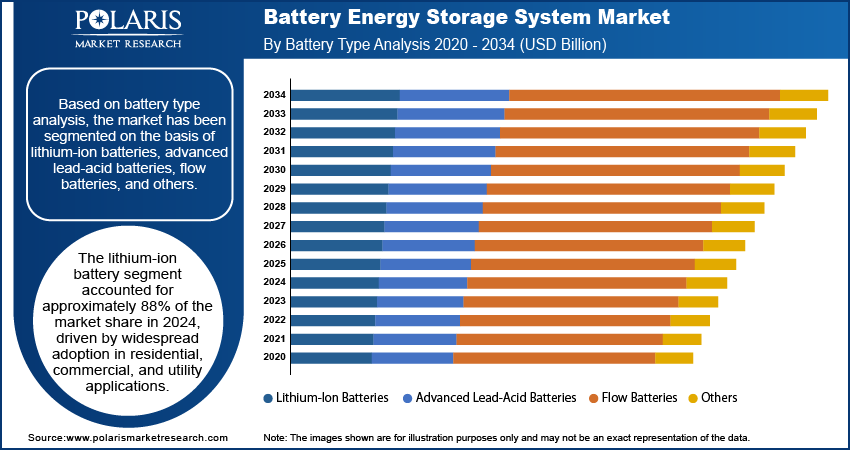

Based on battery type analysis, the market has been segmented on the basis of lithium-ion batteries, advanced lead-acid batteries, flow batteries, and others. The lithium-ion batteries segment held the largest battery energy storage system market share of around 88% in 2025. Lithium-ion (Li-ion) batteries are metal- or polymer-based batteries. These batteries find usage in residential areas, commercial spaces, and utility services. Their applications include small appliances, electronic devices, and electric vehicles. The technology exists in storage systems that handle medium to large energy capacities. The increasing need for Li-ion batteries comes from their ability to deliver high energy density and fast power discharge capabilities. The primary function of Li-ion batteries as energy storage systems includes a vital backup power supply that assists in solving microgrid power supply problems.

By Energy Capacity Insights

Based on energy capacity category analysis, the market has been segmented into below 100 MWh, between 100 to 500 MWh, and above 500 MWh. The above 500 MWh segment accounted for the largest battery energy storage system market share of around 56% in 2025. The installation of battery systems with capacities exceeding 500 MWh mainly occurs in locations that require exceptional energy output, including major manufacturing plants, oil and gas exploration companies, and utility facilities. The battery above capacity is a convenient form to obtain a constant power supply for industrial applications. The batteries provide essential advantages, which improve grid stability and reliability and result in long-term cost savings and support the use of renewable energy sources.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

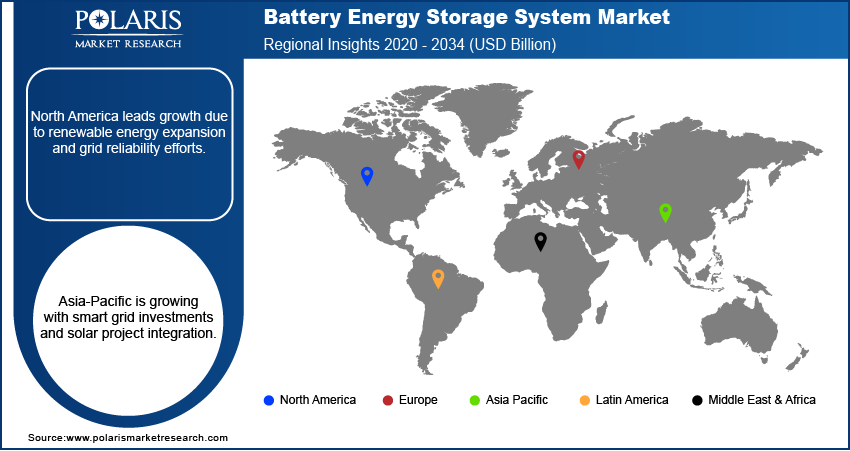

Asia Pacific

The Asia Pacific BESS market has experienced significant growth due to renewable energy integration, grid stability issues, and government clean energy programs. China, Japan, South Korea, and Australia currently lead the region's market expansion. The combination of economic development and urban expansion creates demand for dependable energy storage solutions. Supportive policies promoting renewable energy and improvements in battery technologies have made systems more market-efficient. They have also made them more cost-effective. China has made significant financial commitments to both renewable energy sources and energy storage systems. The country's dominant position as the top battery manufacturer has reduced production costs while enabling advancements in battery technology. The government establishes ambitious targets that lead to increased financial support from both public and private sectors. For instance, the Ming Yang Smart Energy-Tong Liao Hybrid Project and the Baotang Battery Energy Storage System, both located in China, each have a power capacity of 320,000kW and 300,000kW, respectively. Both of them use lithium-ion battery storage technology. The battery manufacturing capacity improvements, renewable energy expansion, and ongoing grid modernization projects in the Asia Pacific further enhance its leadership position.

North America

The North America battery energy storage system market will expand as industries need a reliable power supply during emergency situations. The market receives additional support from government funding for lithium-ion battery manufacturing facilities and initiatives, such as the U.S. Department of Energy's commitment of USD 2 million. The large-scale integration of renewable energy sources into the U.S. economy serves as a driver of deployment to address intermittency issues, in line with environmental regulations. The demand of U.S. manufacturers is growing through applications in electric vehicles and energy storage. Other developments in the area include solid-state lithium-ion batteries intended for off-grid applications, home backup, and small industrial machinery, such as those by Yoshino Technology. In addition, they are complemented by compatibility with solar PV panels, further enhancing market prospects.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Landscape

The fragmentation of the battery energy storage system market and the presence of several players are likely to drive competition. Major service providers in the market are upgrading their technologies regularly, ensuring efficiency, integrity, and safety. These players focus on partnerships, product upgrades, and collaboration as key strategies to gain a competitive advantage over peers and secure a notable market share.

The competitive ecosystem includes cell and module suppliers, system integrators that provide complete BESS solutions, and software and control vendors that deliver EMS/BMS optimization and dispatch services. Buyers choose to assess vendors based on their warranty protection capabilities, performance decline management and system expansion abilities, safety certifications, power conversion efficiency, and track record of success with comparable grid-scale battery energy storage projects.

Some of the key companies in the market include:

- AB Volvo

- ABB

- BYD Company

- Contemporary Amperex Technology Co., Limited

- Fluence Energy, LLC

- General Electric

- Hitachi Energy Ltd.

- Honeywell International

- LG Energy Solutions, Ltd.

- Panasonic Holding Corporation

- Saft

- SAMSUNG SDI CO., LTD.

- Siemens AG

- Sunverge Energy Inc.

- Tesla Inc.

- Toshiba Corporation

- Vertiv Group Corp.

Recent Developments

- May 2025: CATL introduced a 9 MWh ultra-large energy storage system, TENER Stack. The company stated that the new system is created for high-density and mobile use. It offers improved efficiency and supports diverse applications, including AI data centers and industrial electrification.

- April 2025: Honeywell installed a 1.4 MWh microgrid BESS system for SECI in the Lakshadweep Islands. The new microgrid is India’s first operational solar-plus-storage system that connects to the main power grid. The system uses Honeywell’s Energy Management and microgrid control technologies to reduce carbon emissions from Kavaratti remote microgrid operations.

- September 2024: GE Vernova was chosen by Quinbrook Infrastructure Partners as the integration provider for stages 1 and 2 of the Supernode BESS project in Queensland, Australia. The 500 MW/1,500 MWh system will support large-scale wind and solar storage.

- January 2024: Vertech announced its plan to build ten grid-scale battery storage facilities across the United States in January 2024. The company stated that the aim behind the project is to achieve a total battery storage capacity of 10 gigawatt-hours.

- January 2024: BYD reached an agreement with Spain's Grenergy to deliver renewable energy power facilities, which will use its blade-shaped batteries for a $1.4 billion energy storage project in Chile's Atacama Desert.

- September 2023: Tesla introduced its newest home battery backup system, Powerwall 3. The new system delivers increased power capacity and includes an integrated solar inverter.

Report Coverage

The battery energy storage system market report emphasizes key regions across the globe to provide users with a better understanding of the product. The report also provides market insights into recent developments and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, battery type, connection type, energy capacity, application, and futuristic growth opportunities.

Market Segmentation

By Battery Type Outlook (Revenue, USD Billion, 2021– 2034)

- Lithium-Ion Batteries

- Advanced Lead-Acid Batteries

- Flow Batteries

- Others

By Connection Type Outlook (Revenue, USD Billion, 2021– 2034)

- On-Grid

- Off-Grid

By Energy Capacity Outlook (Revenue, USD Billion, 2021– 2034)

- Below 100 MWh

- Between 100 to 500 MWh

- Above 500 MWh

By Application Outlook (Revenue, USD Billion, 2021– 2034)

- Residential

- Commercial

- Utility

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Battery Energy Storage System Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 103.80 billion |

| Market Size in 2026 | USD 131.51 billion |

| Revenue Forecast by 2034 | USD 881.46 billion |

| CAGR | 26.8% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Battery Energy Storage System Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Battery Energy Storage System Market FAQ's

The battery energy system market stood at USD 103.80 billion in 2025. It is projected to account for a CAGR of 26.8% between 2026 and 2034.

A battery energy storage system stores electrical energy in batteries for later use. It manages renewable energy fluctuations and provides backup power. It also stabilizes grids and enables peak shaving.

The market is driven by the integration of renewable energy and grid modernization initiatives. It also benefits from the reduced costs of lithium-ion batteries.

The lithium-ion batteries segment leads the market. This is because lithium-ion (Li-ion) batteries find usage in residential areas, commercial spaces, and utility services.

The Asia Pacific battery energy storage system market has experienced significant growth due to renewable energy integration and government clean energy programs.

Download Sample Report of Battery Energy Storage System Market

Please fill out the form to request a customized copy of the research report.