What is Bio-Lubricants Market Size?

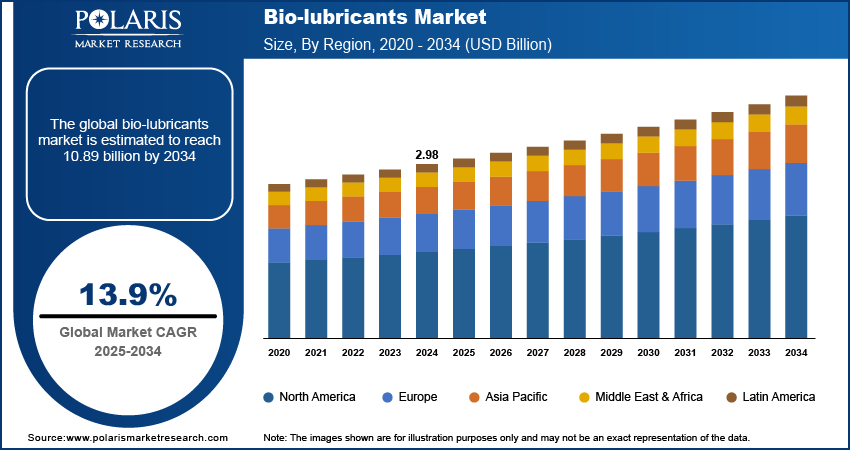

The global bio-lubricants market was valued at USD 3,738.15 million in 2025. It is expected to grow at a CAGR of 13.21% from 2026 to 2034. Rising environmental concerns and the expansion of end-use industries in developing countries such as India, Taiwan, and Brazil are driving the biodegradable lubricants market growth.

Key Insights

- The Europe bio-lubricants market dominated with over 37.39%revenue share in 2025 due to its various emission standards and the growing adoption of biodegradable products.

- The Asia Pacific bio-lubricants market is projected to witness rapid growth at a 14.40% CAGR. Growing demand from end-use industries contributes to the regional market growth.

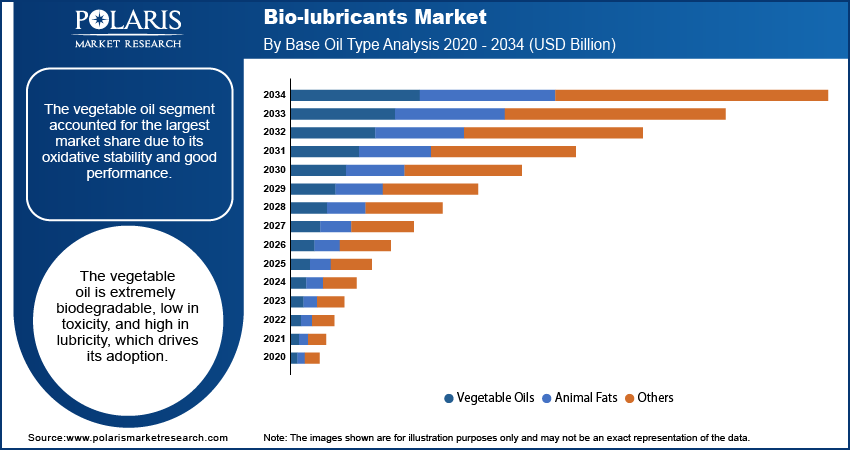

- The vegetable oils segment accounted for the largest market share of 76.80% in 2025. The segment’s dominance is driven by the oxidative stability and good performance of vegetable oil based lubricants.

- The hydraulic fluids segment is expected to witness significant growth at a 13.78% CAGR during the forecast period due to high demand for hydraulic elevators, sweepers, garage trucks, forklifts, motor graders, and front-end loaders.

Bio-Lubricants Market Statistics

- 2025 Market Size: 3,738.15 million

- Bio-Lubricants 2034 Market Forecast: 11,419.77 million

- CAGR (2026-2034): 13.21%

- Largest Market: Europe

Industry Dynamics

- There has been growth in applications that are sensitive to compliance, such as marine systems, forestry equipment, and off-highway machines. This has led to a strong long-term market for biodegradable lubricants.

- Innovation in product has been improving the performance characteristics of biodegradable lubricants. These characteristics include cold flow, oxidation resistance, and seal compatibility. It has enabled biodegradable lubricants to extend into other segments beyond the niche market.

- Technological advancements in extraction are expected to present several bio-lubricants market opportunities.

- High production costs and limited availability of raw materials may limit market growth.

To Understand More About this Research:Request a Free Sample Report

What Are Bio-Lubricants?

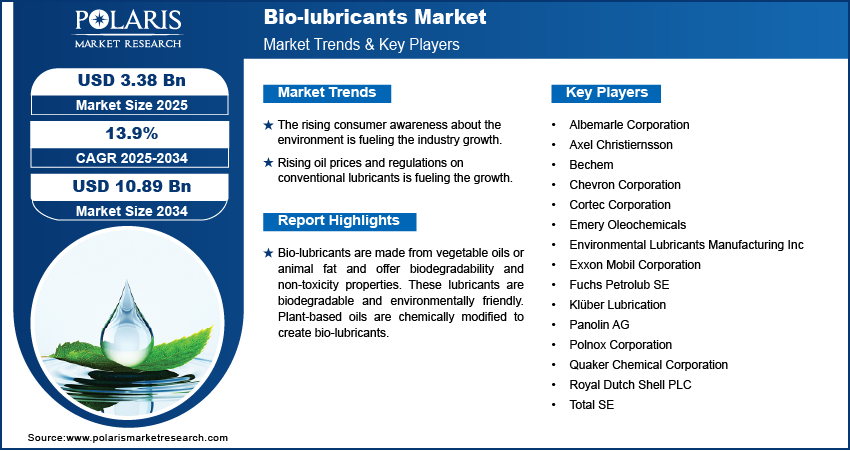

Bio-lubricants are made from vegetable oils, animal fats, and other renewable sources. Bio-lubricants are biodegradable and low toxicity, hence environmentally friendly. Bio-lubricants are used to reduce friction in heavy-duty machines, chainsaws, railway, two-stroke engines, hydraulic machines, and many others. Bio-lubricants are generally preferred to petroleum-based lubricants when they are exposed to the environment, leakage, and contact with humans.

Bio-lubricants are particularly valuable in industries where they may come into contact with soil, water, or an open environment. This includes agriculture, marine work, forestry, and construction equipment. The benefits of bio-lubricants extend beyond biodegradability. Bio-lubricants provide improved lubrication, toxicity reduction, and sustainability benefits to manufacturers and fleet operators.

It is important to differentiate between biobased, biodegradable, and environmentally acceptable lubricants. A lubricant, for instance, might be partially derived from renewable resources but still not meet all the criteria for biodegradability and toxicity to qualify for compliance or procurement. Biodegradable lubricant standards matter in this area. OECD Test Guideline 301 is often applied to test biodegradability. The EU Ecolabel sets environmental criteria for lubricants, and the USDA BioPreferred program identifies biobased products for procurement.

Bio-based lubricants have a number of benefits, such as lower toxicity, reduced environmental impact, and better worker safety, and in some instances, longer life of equipment. They also help in eliminating disposal issues. This is why demand for them is increasing across various industries.

End users are increasingly considering lubricants on a total lifecycle analysis lubricants basis. This includes not only performance but also sourcing, renewability, disposal, and environmental impacts. This approach supports the premium positioning of bio-lubricants. This is especially true when long-term costs and environmental compliance are more significant than initial costs.

The bio-lubricants market is benefiting from a shift towards lubricants that are less toxic, more biodegradable, and better suited to environmental standards. This is especially true for leakage-prone and environmentally sensitive applications. Buyers are not looking at lubricants solely in terms of price and performance; they are also considering environmental impact, disposal, worker safety, and total value.

Increased awareness of environmentally friendly lubricant solutions is projected to drive bio-lubricant demand in the near future. Bio-lubricants are more environmentally friendly than traditional lubricants. The increased use of these lubricants in the transportation and manufacturing industries is predicted to drive up global demand for bio-based lubricants. This is mostly due to increased environmental consciousness and understanding, stringent legislation, and market adoption of bio-based lubricants.

Market Dynamics

Growth Drivers

The global bio-lubricants market is expected to grow as awareness of environmental concerns and the depletion of crude oil resources in many developed countries increases. Bio-lubricants are viewed as viable alternatives to petroleum-based oils and are increasingly accepted for use in industrial and transportation applications.

Environmental compliance is emerging as one of the major bio-lubricants market drivers. Marine applications, hydraulic equipment in proximity to water, and outdoor heavy machinery require more stringent specifications related to leakage, spill risk, and biodegradability. This creates a greater opportunity for bio-based hydraulic oils, greases, and specialty lubricants in such environments. Regulatory initiatives such as EPA guidelines on environmentally acceptable lubricants and vessel discharge are driving this biodegradable lubricant demand, particularly in marine-related applications.

Automotive sector expansion is leading to an increase in automotive lubricants demand for engine oils, greases, transmission fluids, and other related applications. An increase in production of industrial and construction equipment is contributing to market expansion, as lubrication is a prerequisite for such equipment to operate efficiently.

Developing countries are also emerging as important demand centers due to the continued development in manufacturing activities, logistics, warehouse automation, and construction activities. Lubricant demand is also rising with the increasing number of machines, material handling equipment, off-highway vehicles, and industrial equipment. More opportunities are emerging for bio-lubricants, especially due to the increasingly stringent environmental regulations and export regulations.

The increase in oil prices and regulations on conventional lubricants is also expected to drive the market growth globally. Procurement programs supported by governments and sustainable sourcing systems are also helping to drive the long-term adoption of lubricants. The USDA BioPreferred lubricants program assists in identifying biobased products for procurement decisions. The EU Ecolabel for lubricants is a well-established environmental standard in Europe.

Market Restraints

The high production costs and limited raw material availability are major challenges to the bio-lubricants market. While bio-lubricants have several sustainability advantages, they also tend to have a higher production cost compared to conventional petroleum-based lubricants. The high cost of bio-lubricants could act as a major constraint.

Feedstock volatility is another major market constraint. The raw materials used in lubricants, such as vegetable and animal fats, are subject to agricultural cycles, other uses, regional availability, and price volatility. This could act as a constraint on the growth of certain types of bio-lubricants.

There are still performance limitations of bio-lubricants to be overcome in particular application areas. For example, oxidation stability, cold flow, compatibility, and longer service intervals are issues to be addressed to gain more market share. And here, strong R&D and lubricant additives are key to the supplier. Those who can demonstrate longer life and improved temperature performance are more likely to move beyond their current niche uses to expand into more industrial segments.

Bio-Lubricants Market Opportunities

One major opportunity is in the application-specific adoption. Not all lubricant types will shift at the same pace. But bio-lubricants are well-positioned in hydraulic oils, chainsaw oils, greases, metalworking fluids, and marine-related products, where environmental exposure is indeed a concern.

Another major opportunity lies in the circular economy, and new growth opportunities are arising from circular economy lubricants. For example, TotalEnergies’ EV3R range shows how re-refined base oils are being positioned as premium, more sustainable industrial fluids, extending the sustainability focus beyond just plant-based sources.

Bio-Lubricants Market Trends

Product innovations are becoming more visible and are increasingly being directed towards specific product applications. Renewable Lubricants has introduced biodegradable hydraulic fluids for use in low-temperature and environmentally critical applications. Klüber is also enhancing its sustainability efforts by using green electricity manufacturing and reducing emissions. These trends demonstrate that competition in the lubricants industry is no longer simply based on performance. Sustainability and product applications are increasingly being seen as key differentiators.

Report Segmentation

By Base Oil Type Analysis

Based on base oil type, the market is segmented into vegetable oils, animal fats, and others. The vegetable oils segment accounted for the largest market share of 88.4% in 2025. This is due to its biodegradability, low toxicity, good lubricity, and accessibility as a raw material. Vegetable oils are commonly used in lubricant formulations, particularly in industries where environmental issues are closely monitored.

Another major advantage is their strong positioning in sustainable procurement practices. Their renewability, performance, and market familiarity make them an easy starting point for bio-lubricant adoption. Moreover, the rising concern about environmental exposure, particularly in outdoor and leakage-prone equipment, supports the use of vegetable oils over conventional mineral oils.

However, vegetable oils are not universally applicable. In many cases, they have to be further formulated to enhance their oxidation stability and cold-weather performance. This creates opportunities for advanced bio-based blends, additives, and other feedstocks to expand in more specialized uses.

By Application Analysis

Based on application, the market is segmented into greases, hydraulic oils, gear oils, metalworking fluids, chainsaw oils, mold release agents, two-cycle engine oils, and others. The hydraulic fluids segment is expected to witness the fastest growth at a 14.6 % CAGR during the forecast period due to high demand for hydraulic elevators, sweepers, garage trucks, forklifts, motor graders, and front-end loaders. Bio-based lubricants are also commonly used as hydraulic fluids in a wide range of applications to improve operations such as harvesters, cranes, tractors, and load carriers.

Hydraulic systems present a major opportunity for the use of bio-lubricants. This is because hydraulic systems are commonly utilized in outdoor equipment and mobile machines, and leakage is a major problem in such systems. In these cases, the benefits of biodegradable hydraulic fluids are directly relevant to operators, municipalities, construction firms, and agricultural users.

Suppliers are also addressing performance issues in this segment. Renewable Lubricants, for instance, launched Bio-Ultimax 1200LT in early 2025 for use in cold temperatures, highlighting its better flow characteristics in cold temperatures, better resistance to oxidation, and compliance with EAL standards. Such developments are important because hydraulic fluid adoption is based on actual performance, not just sustainability benefits.

Other important application areas for these lubricants include industrial greases, metalworking fluids, gear oils, chainsaw oils, and mold release oils. Chainsaw oils and forestry lubricants are used in environmentally friendly operations. Metalworking lubricants provide benefits such as reduced toxicity and enhanced worker safety in industrial settings.

By End-Use Analysis

Based on end-use, the market is segmented into industrial, automotive and transportation, mining, building and construction, and others. The industrial segment is a key consumer of bio-lubricants due to the high demand for lubricants in the machines and equipment within the industry. Industries are evaluating their lubricants with a focus on sustainability, particularly for those that prioritize waste management and environmental and worker safety concerns.

Automotive and transportation are also growing areas for bio-lubricants. This is because fleets and operators are looking for lower-impact options and sustainable maintenance fluids. However, adoption of automotive bio-lubricants is more selective and depends on application needs, OEM requirements, and product approval standards.

Mining and building and construction are significant end-use segments, given the high usage of equipment, lubricant requirements, and the possibility of lubricant leakage or exposure to the environment. In addition, the increase in construction activity in emerging countries is driving the use of hydraulic and off-highway equipment, thereby supporting lubricant demand.

Regional Analysis

How Europe Captured Largest Market Share in 2025?

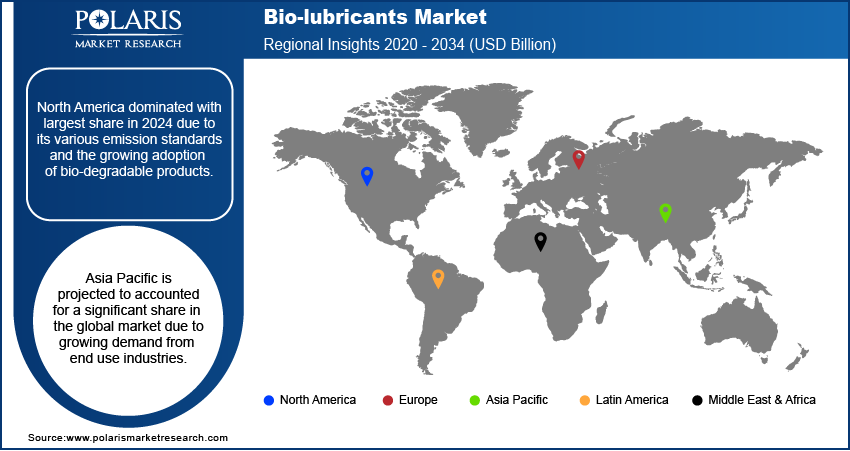

Europe accounted for the largest market share of 40% in 2025. This is due to the presence of stringent environmental regulations, high sustainability standards, and the widespread use of bio-lubricants. In addition, government policies and initiatives, along with the increasing demand for bio-lubricants among consumers, support the market's dominance.

The region benefits from high awareness of environmental compliance, a well-developed network of specialty lubricant suppliers, and widespread use of bio-lubricants. Moreover, programs such as the EU Ecolabel highlight the importance of environmental compliance and contribute to the market’s leading position.

What is Reason for Asia Pacific's Significant Growth?

The Asia Pacific bio-lubricants market is expected to witness strong growth at a 15.0 % CAGR during the forecast period. This is due to increasing industrialization in the Asia Pacific. This region is known to have a high level of manufacturing, and countries such as India, Taiwan, Vietnam, and Indonesia are adding to their manufacturing capabilities.

Growth is also fueled by an increase in vehicle production, infrastructure development, expansion in warehousing facilities, and an increase in the utilization of machinery. As the manufacturing sector grows, there are increasing lubricant requirements for various machinery and equipment, thereby increasing the potential for bio-lubricant uptake in the future.

Automotive sales and manufacturing in the region are increasing owing to a surge in demand for personal and public transport. This, in turn, is creating a need for engine oil, greases, and transmission fluids. Asia Pacific is likely to remain a high-opportunity region for suppliers that can balance costs and sustainability. Adoption may start in industrial and export-oriented sectors and eventually expand to a broader range of lubricant types.

North America, Latin America, and Middle East & Africa

North America is a major market for bio-lubricants. This is owing to the stringent environmental regulations and increasing awareness about the benefits of biodegradable products. This market is also fueled by government policies and regulations, as well as by consumers' increasing inclination towards bio-based products.

North America also benefits from high environmental compliance awareness, an established base of specialty lubricant suppliers, and even higher adoption in industrial, marine, and municipal applications. In the U.S., procurement trends related to biobased products and sustainability continue to support the argument for renewable lubricants. This is further enhanced by the USDA BioPreferred program and EPA environmental regulations related to environmentally acceptable lubricants, particularly in applications where leakage risk exists.

The renewed automotive sector in the U.S. and Canada, along with increased regulatory action on the use of conventional lubricants, is driving regional demand. North America also benefits from an excellent base of specialty lubricant suppliers, specialty formulators, and application-specific products, which aid in greater availability and awareness. This leads to increased usage in agriculture, forestry, and even in municipalities.

The Latin America bio-lubricants market offers significant market potential. This is due to rising use in agricultural activities, industries, and environmental concerns in this region. The Middle East and Africa region also has significant market potential. This is because of an increase in their use in industrial activities, mining, and fleet maintenance.

Competitive Landscape

The bio-lubricants market includes a wide range of participants. These range from large global oil companies to niche companies specializing in sustainability. An analysis of these companies' strategic focus can provide insight into the competitive landscape.

Diversified Global Lubricants Majors

Corporations such as Exxon Mobil Corporation, Chevron Corporation, Royal Dutch Shell PLC, and Total SE are global players with scale, distribution reach, and R&D expertise. Their approach to bio-lubricants is usually part of a larger portfolio and enables them to leverage existing strengths while gradually building up the sustainable segment.

Specialty Industrial Lubricant Providers

Firms such as Fuchs Petrolub SE, Klüber Lubrication, Bechem, and Quaker Chemical Corporation specialize in high-performance lubricants. These firms compete on the basis of technical expertise, tailored solutions, and established relationships in the industrial sector.

Sustainability-Focused/Bio-Based Specialists

Companies like Panolin AG, Environmental Lubricants Manufacturing Inc., Emery Oleochemicals, and Cortec Corporation are very much aligned with one of the key values of bio-lubricants. Their business models are centered on sustainability, renewability, biodegradability, and government regulations. They are also at the forefront of technology development in plant-based EALs.

Application-Led Innovators (Hydraulic & Marine Focus)

There are companies that specialize in application-specific innovation, especially in environmentally friendly applications such as hydraulic system innovation and marine environment application innovation. Axel Christiernsson and Polnox Corporation specialize in application-specific innovation in bio-lubricants that provide a competitive edge, particularly in spill-prone areas and marine environments.

List of Key Companies

- Albemarle Corporation

- Axel Christiernsson

- Bechem

- Chevron Corporation

- Cortec Corporation

- Emery Oleochemicals

- Environmental Lubricants Manufacturing Inc.

- Exxon Mobil Corporation

- Fuchs Petrolub SE

- Klüber Lubrication

- Panolin AG

- Polnox Corporation

- Quaker Chemical Corporation

- Royal Dutch Shell PLC

- Total SE.

Industry Developments

- February 2025: Renewable Lubricants introduced Bio-Ultimax 1200LT Hydraulic Fluids for cold weather applications. These hydraulic fluids provide pumpability to -40°C and have a pour point as low as -60°C. They are also resistant to oxidation and wear. In addition, these hydraulic fluids improve seal performance to reduce hydraulic fluid leaks. They meet EPA standards for Environmentally Acceptable Lubricants (EALs).

- February 2025: BP announced that it was evaluating options for its Castrol lubricants business, which could also include a potential sale. This move by BP is part of a process to rebalance the company’s portfolio.

- February 2025: Klüber Lubrication strengthened its sustainability commitments. The company emphasized its increased use of green electricity and stronger visibility at industry events. These actions align with its ESG positioning and resonate with its industrial customers’ need for bio-based lubricants.

- June 2024: TotalEnergies developed its first range of eco-designed lubricants: Quartz EV3R for passenger cars and Rubia EV3R for trucks. This range of eco-designed products has been developed from premium regenerated base oils to minimize environmental impact. In addition, the eco-designed bottles are made from 50% recycled plastic.

Market Segmentation

By Base Oil Type Outlook (Revenue, USD Million, 2021-2034)

- Vegetable Oils

- Animal Fats

- Others

By Application Outlook (Revenue, USD Million, 2021-2034)

- Greases

- Hydraulic Oils

- Gear Oils

- Metalworking Fluids

- Chainsaw Oils

- Mold Release Agents

- Two-Cycle Engine Oils

- Others

By End-Use Outlook (Revenue, USD Million, 2021-2034)

- Industrial

- Automotive and Transportation

- Mining

- Building and Construction

- Others

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Bio-Lubricants Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 3,738.15 million |

|

Market Size in 2026 |

USD 4,212.14 million |

|

Revenue Forecast by 2034 |

USD 11,419.77 million |

|

CAGR |

13.21% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD million, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Bio-Lubricants Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

A bio-lubricant refers to a lubricating oil that is made up of renewable sources, such as vegetable oil or animal fat, or other sustainable materials. A bio-lubricant is generally prized for being biodegradable, non-toxic, and environmentally friendly, as opposed to other petroleum-derived lubricants.

The global bio-lubricants market size stood at USD 3,738.15 million in 2025. It is projected to account for a CAGR of 13.21% between 2026 and 2034.

Market growth is supported by environmental concerns and industrial expansion. The market is also fueled by increased interest in sustainable materials.

The vegetable oils segment accounted for the largest market share in 2025. This is due to their eco-friendly characteristics and broad acceptance.

No. While adoption tends to begin in environmentally sensitive applications, bio-lubricants are also finding their way to hydraulic fluids, greases, metalworking fluids, chainsaw oils, and many other industrial applications.

North America is in the lead position due to stricter environmental oversight and increased awareness of biodegradable products. The region also has a strong procurement support for bio-based materials.

Asia Pacific is projected to witness rapid growth due to rising industrialization and manufacturing expansion.

The major challenges are increased production costs, limited availability of feedstock, performance limitations under specific operating conditions, and the need for formulation improvements.

A few of the key players in the market include Albemarle Corporation, Axel Christiernsson, Bechem, Chevron Corporation, Cortec Corporation, Emery Oleochemicals, Environmental Lubricants Manufacturing Inc., Exxon Mobil Corporation, Fuchs Petrolub SE, Klüber Lubrication, Panolin AG, Polnox Corporation, Quaker Chemical Corporation, Royal Dutch Shell PLC, and Total SE.

Not always. A lubricant may be biobased without meeting all biodegradability thresholds. Hence, buyers need to check the product claims, standards, and testing data.

Hydraulic equipment, marine systems, forestry, agriculture, construction, and some industrial operations are likely to adopt bio-lubricants more readily since environmental exposure is more relevant.

Page last updated on:

Jan-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements