Reports

Cancer Biomarkers Market Insight, Industry Share & Growth Driver, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

Cancer Biomarkers Market Overview

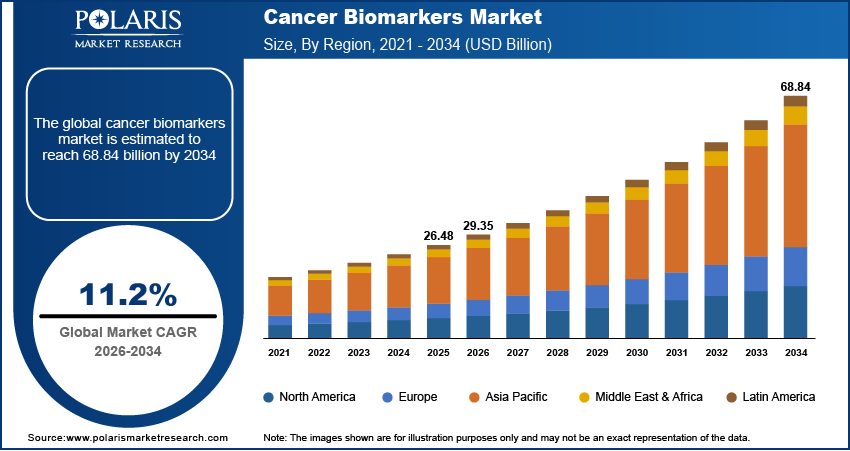

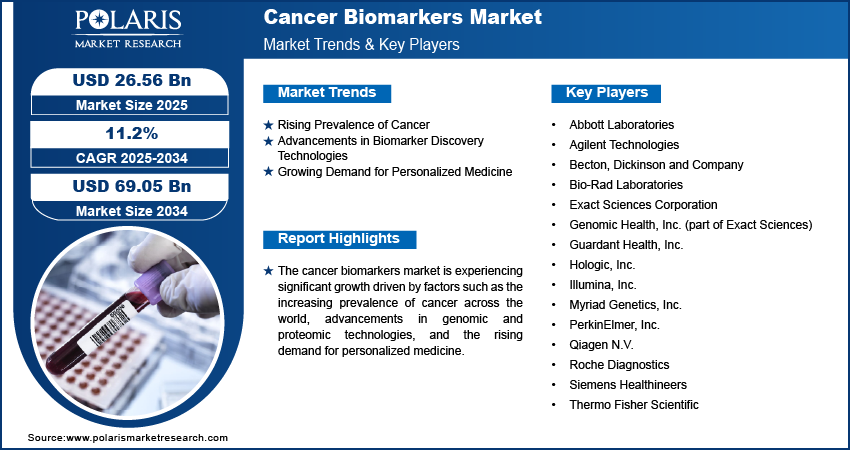

The cancer biomarkers market size was valued at USD 26.48 billion in 2025. The market is projected to account for a CAGR of 11.2% between 2026 and 2034. The market is driven by the global cancer epidemic, advancements in cancer biomarker discovery, increased investments in cancer research, rising demand for personalized cancer therapy and companion diagnostics market, and the combined potential of AI and liquid biopsy innovations for early cancer diagnosis.

Cancer biomarkers are measurable signals within DNA, RNA, or metabolic activity that assist in detecting cancer presence, prognosis level, and guiding and choosing therapy options and monitoring therapy reactions. The market includes tissue tests and non-invasive liquid biopsy tests, with adoption influenced by clinical validation standards and reimbursement policies.

Key Insights

- The genetic biomarkers segment leads the market. This is due to its key role in detecting cancer mutations and its use in personalized medicine, aided by advances in genomic technology.

- Proteomic biomarkers are experiencing the fastest growth. This is because they help understand cancer progression and develop targeted therapies.

- The diagnostics segment accounts for the largest market share. The growing demand for early and accurate cancer detection methods contributes to the segment’s leading market position.

- The North America cancer biomarkers market leads the global market with its strong healthcare infrastructure and high prevalence of cancer. The region also has major research investments and supportive regulations.

- The market has shown steady growth in the European region. The presence of various strong healthcare systems and an increased focus on precision oncology drives regional market growth.

- The Asia Pacific cancer biomarkers market is expected to see the highest growth rate. Rising cancer cases, better healthcare, and government support are contributing to market development in the region.

- Liquid biopsy technologies are becoming more common for non-invasive detection. Such aspects indicate the use of biomarkers beyond tissue analysis.

- Clear guidelines, strong clinical evidence, and reimbursement policies have a significant role in accelerating the expansion of biomarker tests across regions and providers.

Industry Dynamics

- Increasing rates of cancer create demand for early detection biomarkers and personalized treatment tools around the world.

- Advances in genomics and proteomics are accelerating the discovery of novel and precise cancer biomarkers.

- Growth in companion diagnostics helps in personalizing oncology therapeutics and putting biomarkers to better use.

- Biomedical and biomarker innovation are increased by the use of AI in biomarker discovery through rapid and accurate analysis.

- The expensive nature of these advanced techniques makes it difficult for emerging markets to access them.

- Apart from technology costs, adoption can also be influenced by challenges with data sharing and interoperability, variability in evidence, and the time required for standardization and validation.

Market Statistics

2025 Market Size: USD 26.48 billion

2034 Projected Market Size: USD 68.84 billion

CAGR (2026–2034): 11.2%

North America: Largest market in 2025

To Understand More About this Research: Download Sample Report

AI Impact on Cancer Biomarkers Market

- AI enables faster, more accurate biomarker discovery by analyzing larger volumes of data than conventional techniques allow.

- Machine learning algorithms help discover new cancer biomarkers by recognizing intricate patterns in genomic and protein data.

- AI-based software helps create more effective and personalized treatment plans. They do this by integrating patient-specific clinical information and biomarker data.

- Non-invasive and real-time monitoring of cancer progression and response to treatment using liquid biopsy analysis aided by AI technology.

- AI is increasingly used to group patients according to their biomarker profiles and identify those most likely to benefit from particular treatments. This increases the speed of oncology trials and supports the wider adoption of precision medicine.

- However, the success of these AI models depends upon the quality of data, the representation of various populations, and how explainable the results are. For this reason, strong oversight with proper validation is essentially required before such tools are used clinically.

The cancer biomarkers market focuses on the detection and use of biological markers, such as proteins, DNA, RNA, and other biomolecules, to identify cancer. Several factors that are driving the cancer biomarkers market include the rising incidence of cancer, advancements in biomarker discovery technologies, and increased government and private-sector investments in cancer research. In addition, the need to incorporate personalized medicine is significantly impacting the cancer biomarkers market. Emerging market trends include the use of artificial intelligence in biomarker discovery and the development of non-invasive liquid biopsy tests intended to aid in cancer detection.

Market Dynamics

Rising Prevalence of Cancer

The main driver of the cancer biomarkers market is the steady rise in the global burden of cancer. The WHO estimates that cancer is the second-leading cause of mortality worldwide, representing about 19.3 million cases and 10 million deaths in 2020. Growing cancer incidence necessitates improvements in diagnostic and therapeutic tools. This increases demand for biomarkers that facilitate early detection, prognosis, and personalized treatment strategies.

Advancements in Biomarker Discovery Technologies

Advancements in technology related to genomics and proteomics are contributing to the development of new cancer biomarkers. Next-generation sequencing technology and high-throughput screening technologies have transformed the field of cancer biomarker discovery. The traditional ways of finding biomarkers have given way to more accurate and faster identification of new biomarkers with the incorporation of next-generation sequencing technology. For instance, personal genomic profiles can be achieved in cancer diagnostics through the incorporation of next-generation sequencing technology, thereby identifying targeted therapy. Thus, the adoption of advanced technology contributes to the growth of the cancer biomarkers market.

Growing Demand for Personalized Medicine

Personalized medicine requires that medical treatments be tailored to each patient's individual characteristics. To achieve this, a lot of focus is placed on detecting specific biomarkers. According to a Personalized Medicine Coalition report, personalized medicine accounted for 42% of all new molecular entities approved by the US Food and Drug Administration (FDA) in 2021. Cancer biomarkers play an integral role in the development of specialized medical treatments. Thus, the emerging trend of personalized medicine biomarkers is boosting the growth of the cancer biomarkers industry.

High Cost and Complex Validation Pathways

While there remains a strong market need, the associated costs of NGS, multi-omics, and these sophisticated devices may impede market adoption, particularly in money-sensitive markets. Moreover, before tests can be widely accepted, they must demonstrate strong analytical/clinical validation. This process may also be associated with a certain degree of delay, which may impede or otherwise restrict test commercialization, particularly for new liquid biopsy tests using AI technology.

Segment Insights

Assessment – Cancer Type-Based Insights

The cancer biomarkers market segmentation, by cancer type, includes breast cancer, prostate cancer, colorectal cancer, cervical cancer, liver cancer, lung cancer, and others. The lung cancer segment is growing at the highest rate. It is mainly attributed to the rising incidence of lung cancer, particularly lung cancer that results from increasing smoking habits as well as rising environmental pollution. The introduction of non-invasive tests, including liquid biopsies and analysis of circulating tumor DNA, helps in the early detection and management of lung cancer. The introduction of novel therapies also contributes to the growth of the lung cancer segment.

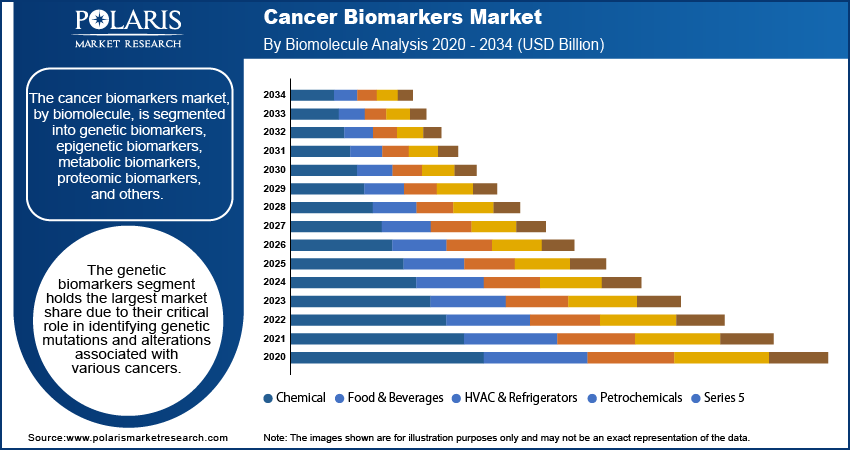

Outlook – Biomolecule-Based Insights

The cancer biomarkers market segmentation, by biomolecule, includes genetic biomarkers, epigenetic biomarkers, metabolic biomarkers, proteomic biomarkers, and others. The genetic biomarkers segment accounts for the largest share of the market due to its importance in detecting genetic mutations and changes associated with various cancer types. The widespread application of genetic tests in personalized medicine and the development of cancer-targeting drugs using genetic biomarkers are driving the dominance of the genetic biomarkers segment. In addition, the use of next-generation sequencing technologies helped identify the application of genetic biomarkers in cancer diagnosis and treatment. Genetic biomarkers remain fundamental to guiding therapy decisions in cases where targeted treatments depend on the identification of specific mutations, and they support companion diagnostics that help match patients with the most suitable treatment options.

The proteomic biomarkers segment has the highest growth rate, driven by increased emphasis on protein expression profiling and protein-based biomarkers for early cancer diagnosis and treatment. Proteomic biomarkers play an important role in understanding the mechanisms of cancer development. They are also essential for developing protein-targeted therapies to treat cancer. The development of mass spectrometry and other bioinformatics tools has helped researchers in proteomics discover new proteomic biomarkers, thereby driving this segment. Proteomic growth is also fueled by the need to improve understanding of pathway activity and resistance to therapy, which is not explained by genomics.

Evaluation – Application-Based Insights

The cancer biomarkers market, by application, is segmented into drug discovery & development, diagnostics, personalized medicine, and others. The diagnostics segment holds the largest share in the market due to the rising need for accurate cancer screening technologies. Biomarkers in diagnostics provide precision in cancer screening. Therefore, the use of biomarkers improves the results obtained with diagnostic technologies for cancer. The incidence of cancer in the population and advances in diagnostic technologies, such as liquid biopsy, are crucial factors driving the prominence of the diagnostics segment.

The personalized medicine segment is growing at the highest rate due to the increasing trend toward individualized treatment approaches and methods. Biomarkers play a crucial role in personalized medicine. They help doctors identify specific genetic or molecular profiles associated with individualized therapy approaches. The increasing trend toward precision medicine, combined with the application of biomarkers, is further increasing the acceptance of individualized treatment approaches.

Regional Insights

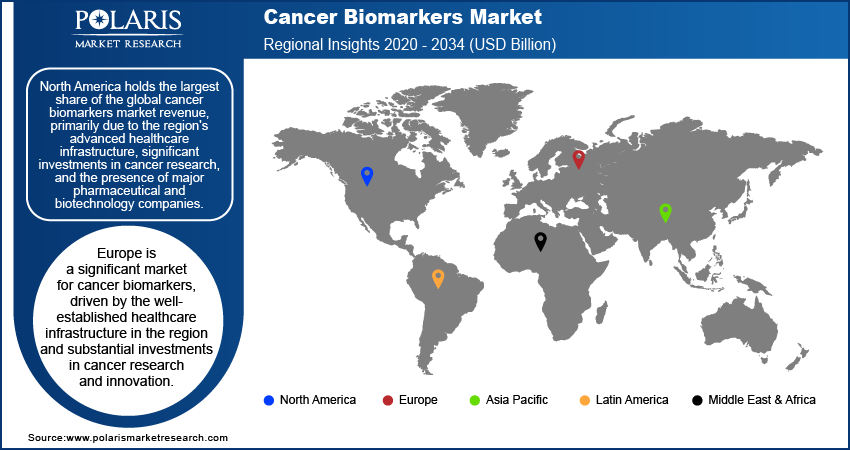

By region, the study provides cancer biomarkers market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America cancer biomarkers market accounts for the largest market share. This is due to advanced healthcare infrastructure, high investment in cancer research, and the presence of major pharmaceutical and biotechnology companies. High incidence rates of cancer and increased government support for research and development support the use of cancer biomarkers in diagnostics and personalized medicine. Also, favorable government regulations and the increased use of advanced diagnostic technologies contribute to North America's dominance in the global cancer biomarkers market. Moreover, the high level of testing penetration as well as clinical trial density would facilitate the swift commercialization of emerging biomarker tests. The market in other regions, including Europe and the Asia Pacific, is also witnessing growth. These regional markets are driven by rising healthcare expenditure and increased awareness of cancer early detection.

Europe is a major market for cancer biomarkers. This is due to the existing, well-established health infrastructure base, as well as investment in cancer research and innovation. Germany, the UK, and France are the top contributors to the field of cancer biomarkers. These countries focus on early detection and personalized medicine. The European Union’s initiative towards precision oncology and the integration of advanced diagnostic platforms further influence the use of cancer biomarkers in the region. The combined efforts of academic and biotech industry initiatives are driving research and development in the region. Precision oncology programs and cross-border research collaborations also support the adoption of cancer biomarkers in Europe.

The Asia Pacific cancer biomarkers market is expanding rapidly. It is driven by rising cancer incidence, improved healthcare infrastructure, and greater awareness of cancer biomarkers. Countries such as China, India, and Japan are investing heavily in improving their healthcare and biotechnology sectors. In addition, factors such as the increasing demand for personalized medicine and advancements in technologies like next-generation sequencing are significantly driving the Asia Pacific market for cancer biomarkers. Furthermore, the expanding pharmaceutical industry and growing clinical research activities contribute to the regional market growth. Other factors contributing to growth include increased access to genomic testing, expanding cancer screening, and greater biopharma R&D activity in countries such as China, Japan, and India.

Key Players and Competitive Insights

The market for cancer biomarkers comprises several major players that are driving growth and development. These major players include Roche Diagnostics, which specializes in diagnostics and personalized healthcare globally. Thermo Fisher Scientific is best known for its vast range of diagnostic tools and equipment. Abbott Laboratories, a major player in the diagnostics segment, is notable for its strong portfolio in molecular diagnostics. Qiagen N.V. specializes in sample preparation and diagnostic assays. Similarly, Illumina Inc. is known for its contributions to sequencing technologies. Bio-Rad Laboratories offers a range of diagnostic tools. Similarly, companies such as PerkinElmer Inc. and Hologic Inc. are contributing to cancer diagnostics and biomarker discovery.

Myriad Genetics, Inc. focuses on genetic testing and precision medicine. Exact Sciences Corporation is known for its innovative cancer screening products. Siemens Healthineers is a major provider of diagnostic imaging and laboratory diagnostics. Genomic Health, Inc., part of Exact Sciences, is influential in the personalized cancer care space. Other important contributors are Becton, Dickinson and Company, which provides a wide array of medical devices and diagnostic solutions, and Biocartis, which focuses on molecular diagnostics. Moreover, companies such as Foundation Medicine, Inc., a subsidiary of Roche, and Guardant Health, Inc., which specialize in liquid biopsy technologies, are key players driving market advancements.

Competitive differentiation strategies focused more on investing in additional biomarker tests. There is also increased investment in the NGS technology platform, including analytics software, and in engaging key stakeholders such as hospitals, pathology clinics, and pharma companies. There is investment in the development of liquid biopsy solutions with related artificial intelligence technologies.

Continuous innovations and strategic partnerships define the market's competitive landscape. Cancer biomarker companies are making significant investments in R&D to expand their biomarker portfolios and improve diagnostic accuracy. The integration of artificial intelligence with big data analytics creates advanced systems for delivering precise and customized cancer treatment. Companies use partnerships, acquisitions, and product development to achieve greater market visibility and technological advancement. The system delivers better patient outcomes and establishes new standards for cancer diagnostics and treatment.

Roche Diagnostics is one of the leading firms in the cancer biomarkers industry. The firm operates in the field of diagnostics and personalized health care services. It aims at delivering innovative diagnostics for the early detection of cancer.

Thermo Fisher Scientific is another major player in this field. It offers different products that can be used to diagnose diseases through different methods, such as sequencing. It is also an essential tool in cancer diagnosis.

List of Key Companies

- Abbott Laboratories

- Agilent Technologies

- Becton, Dickinson and Company

- Bio-Rad Laboratories

- Exact Sciences Corporation

- Genomic Health, Inc. (part of Exact Sciences)

- Guardant Health, Inc.

- Hologic, Inc.

- Illumina, Inc.

- Myriad Genetics, Inc.

- PerkinElmer, Inc.

- Qiagen N.V.

- Roche Diagnostics

- Siemens Healthineers

- Thermo Fisher Scientific

Cancer Biomarkers Industry Developments

- November 2024: Roche announced the launch of a new genomic profiling test. The test is designed to identify genetic mutations in cancer patients. With the new test, Roche aims to advance personalized treatment strategies.

- November 2024: Thermo Fisher Scientific expanded its collaboration with oncology research company Mainz Biomed. The company stated that the collaboration is focused on the development and commercialization of colorectal cancer screening products.

Cancer Biomarkers Market Segmentation

By Cancer Type Outlook (Revenue, USD Billion, 2021–2034)

- Breast Cancer

- Prostate Cancer

- Colorectal Cancer

- Cervical Cancer

- Liver Cancer

- Lung Cancer

- Others

By Biomarker Type Outlook (Revenue, USD Billion, 2021–2034)

- PSA

- HER-2

- EGFR

- KRAS

- Others

By Biomolecule Outlook (Revenue, USD Billion, 2021–2034)

- Genetic Biomarkers

- Epigenetic Biomarkers

- Metabolic Biomarkers

- Proteomic Biomarkers

- Others

By Profiling Technology Outlook (Revenue, USD Billion, 2021–2034)

- Imaging Technology

- OMICS

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Drug Discovery & Development

- Diagnostics

- Personalized Medicine

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Cancer Biomarkers Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 26.48 billion |

| Market Size in 2026 | USD 29.35 billion |

| Revenue Forecast by 2034 | USD 68.84 billion |

| CAGR | 11.2% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Cancer Biomarkers Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The cancer biomarkers market stood at USD 26.48 billion in 2025. The market is expected to reach USD 68.84 billion by 2034.

The market is projected to account for a CAGR of 11.2% between 2026 and 2034.

North America accounted for the largest market share in 2025. This is due to the region’s advanced healthcare infrastructure and significant investments in cancer research.

A few of the key players in the market are Abbott Laboratories; Agilent Technologies; Becton, Dickinson and Company; Bio-Rad Laboratories; Exact Sciences Corporation; Genomic Health, Inc. (part of Exact Sciences); Guardant Health, Inc.; Hologic, Inc.; Illumina, Inc.; Myriad Genetics, Inc.; andPerkinElmer, Inc.

The genetic biomarkers segment accounts for the largest share of the market due to its importance in detecting genetic mutations.

Cancer biomarkers are biological molecules found in blood, tissues, or other bodily fluids. They can indicate the presence of cancer or offer information about the disease progression and type.

A few of the major trends shaping the market include increased use of liquid biopsies and rising integration of artificial intelligence.

Diagnostic markers help detect or confirm cancer. Prognostic markers provide information about the course of cancer. Predictive markers reveal how well a patient will respond to a certain treatment.

Biomarkers need to be carefully tested to demonstrate their accuracy and usefulness in real-world patient care. Clear clinical evidence and acceptance by doctors are important for widespread adoption.

Companies manufacturing, distributing, or purchasing cancer biomarkers-related products and other consulting firms must buy the report.

Download Sample Report of Cancer Biomarkers Market

Please fill out the form to request a customized copy of the research report.