Carbon Capture Construction Materials Market Trends, Global Report, 2025-2034

REPORT DETAILS

Market Statistics

Carbon Capture Construction Materials Market Overview

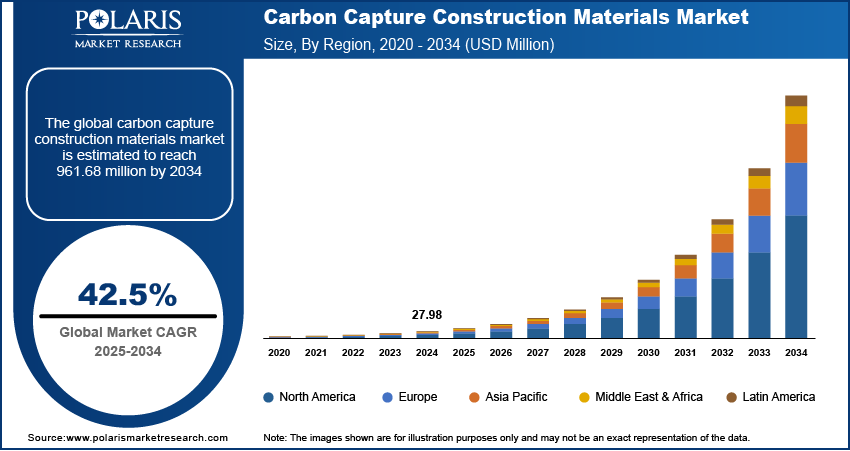

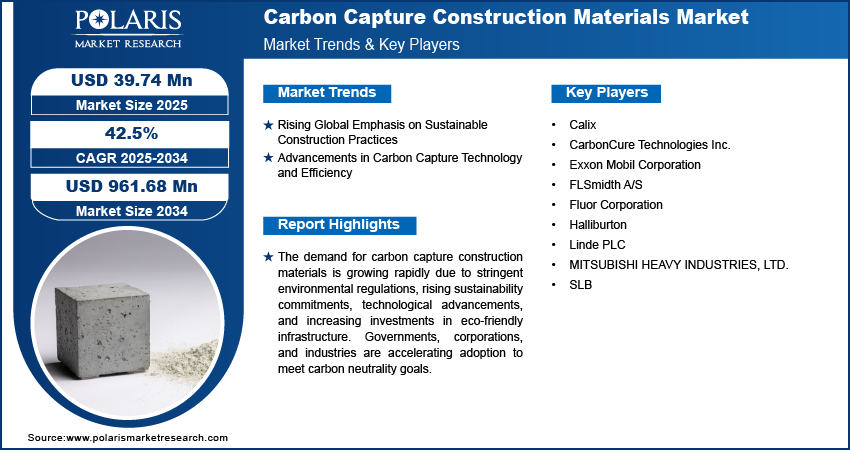

The global carbon capture construction materials market size was valued at USD 27.98 million in 2024. The market is projected to grow from USD 39.74 million in 2025 to USD 961.68 million by 2034, exhibiting a CAGR of 42.5% during 2025–2034.

Carbon capture construction materials (CCCM) refer to building materials that actively capture and store carbon dioxide (CO₂) during their production or lifecycle, reducing overall greenhouse gas emissions. These materials, including carbon-infused concrete, biochar-based composites, and recycled aggregates, are gaining traction due to their potential to mitigate climate change. The rising demand for sustainable solutions in the construction industry, driven by regulatory policies and corporate sustainability commitments, propels the carbon capture construction materials market growth.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The carbon capture construction materials (CCCM) market demand is rising as builders and developers prioritize eco-friendly alternatives over traditional high-carbon-emission materials such as cement and steel. Increasing awareness regarding the adverse impact of climate change and rising carbon reduction initiatives have encouraged governments and industries to invest in CCCM. The adoption of these materials is further fueled by innovations in carbon sequestration technologies and industrial-scale production, ensuring both cost-effectiveness and environmental benefits.

The growing preference for sustainable construction materials is driving demand for CCCM as consumers and businesses seek greener alternatives. The rise of green building certifications and standards, such as LEED and BREEAM, has created a favorable environment for carbon capture construction materials adoption. These certifications push builders to integrate low-carbon materials into their projects, boosting carbon capture construction materials market development.

Companies are pursuing various business expansion strategies, including strategic partnerships, investments in R&D, and innovating sustainable products, to take advantage of this trend. The carbon capture construction materials market is anticipated to experience significant growth as regulatory frameworks become stricter and environmentally conscious construction practices gain traction, establishing carbon capture construction materials as a crucial component in the future of sustainable building.

Carbon Capture Construction Materials Market Dynamics

Rising Global Emphasis on Sustainable Construction Practices

The rising global emphasis on sustainability is driving a significant shift in the construction industry, particularly in the demand for carbon capture construction materials. There is an increasing awareness among governments, organizations, and individuals about environmental impacts, leading to a rise in eco-friendly construction practices. The Paris 2024 Olympics is prioritizing sustainability by repurposing existing venues, utilizing bio-based materials, low-carbon concrete, solar energy, and integrating green spaces. These efforts aim to reduce the environmental footprint while ensuring long-term community benefits. This trend is contributing to the growing demand for carbon capture construction materials, as they offer a way to reduce carbon emissions during production. There are substantial growth opportunities in the carbon capture construction materials market as countries implement stricter environmental regulations and prioritize green infrastructure.

Advancements in Carbon Capture Technology and Efficiency

Advancements in carbon capture technology are driving demand for carbon capture construction materials as industries seek innovative ways to reduce emissions and enhance sustainability. Honeywell and UT Austin’s advanced solvent carbon capture technology is undergoing large-scale testing at Norway’s TCM facility, aiming to capture 95% of CO2 emissions from industrial sources. Such technological breakthroughs emphasize the potential for large-scale carbon capture, fueling interest in integrating captured CO2 into construction materials.

Technological advancements in carbon capture construction materials are enabling the development of low-carbon concrete and other sustainable building materials that effectively store captured CO2 driving the market revenue.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Carbon Capture Construction Materials Market Segment Analysis

Carbon Capture Construction Materials Market Assessment by Technology Outlook

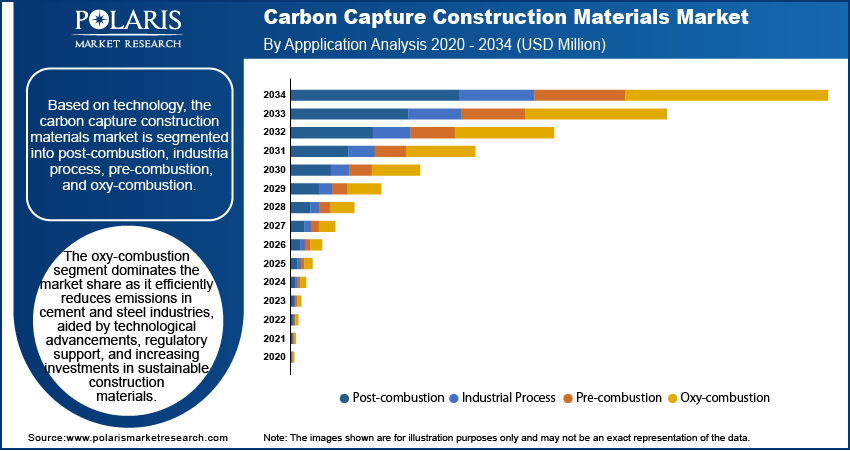

The global carbon capture construction materials market segmentation, based on technology, includes post-combustion, industrial process, pre-combustion, and oxy-combustion. The oxy-combustion segment is expected to hold a significant carbon capture construction materials market share during the forecast period due to its high efficiency in reducing carbon emissions. This process involves burning fuel with pure oxygen instead of air, producing a concentrated CO₂ stream that is easier to capture and store. Oxy-combustion offers a viable solution to lower their carbon footprint as industries, particularly cement and steel manufacturing, face stricter environmental regulations. Additionally, advancements in oxygen separation technologies and carbon utilization are making the process more cost-effective. Growing government support for carbon capture initiatives and increasing investments in sustainable construction materials further drive market demand. As a result, oxy-combustion is emerging as a key technology for achieving carbon neutrality in construction industries.

Carbon Capture Construction Materials Market Evaluation by Application Outlook

The global carbon capture construction materials market segmentation, based on application, includes commercial, residential, industrial, and others. The commercial segment held a significant carbon capture construction materials market revenue share in 2024 due to the rising demand for sustainable building solutions in offices, retail spaces, and commercial infrastructure. Stringent environmental regulations and corporate sustainability goals have driven businesses to adopt eco-friendly construction materials that reduce carbon emissions. Additionally, the growing trend of green buildings and LEED-certified structures has further fueled the use of carbon capture materials in commercial projects. Developers and investors increasingly prefer these materials to enhance energy efficiency, meet regulatory compliance, and improve long-term cost savings. This segment continues to expand the market due to rising urbanization and minimizing the carbon footprint of commercial buildings, which significantly contributes to the overall growth of the industry.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Carbon Capture Construction Materials Market Regional Analysis

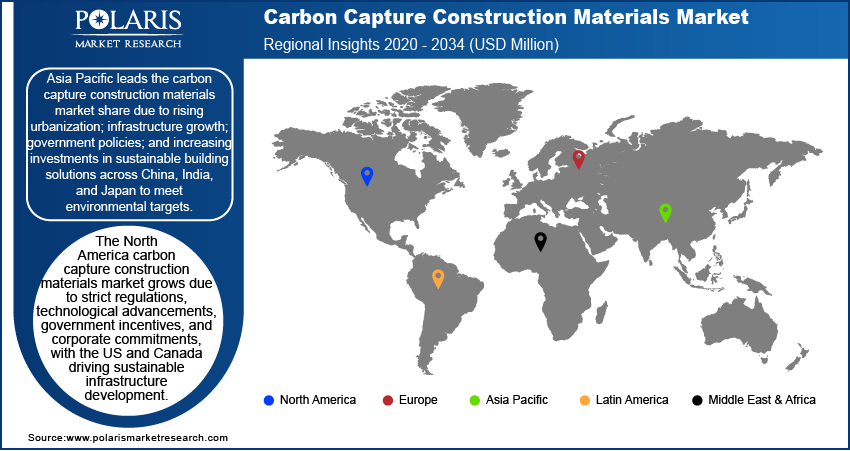

By region, the study provides carbon capture construction materials market insight into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific holds a substantial market share due to rapid urbanization, large-scale infrastructure development, and increasing government initiatives for sustainable construction. Countries such as China, India, and Japan are investing heavily in eco-friendly building materials to comply with stringent environmental regulations and reduce carbon emissions. The region’s growing population and rising demand for residential and commercial spaces have further driven the adoption of carbon capture materials across the region. Additionally, government policies promoting green buildings and carbon neutrality targets have accelerated the Asia Pacific carbon capture construction materials market expansion. The region continues to lead in adopting carbon capture construction materials with strong industrial expansion and increasing awareness of sustainable construction practices, making it a key player in the global market.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

The North America carbon capture construction materials market is experiencing a substantial growth due to strict environmental regulations, advancements in carbon capture technology, and increasing investments in sustainable infrastructure. The US and Canada are implementing policies to constrain carbon emissions, driving demand for low-carbon construction materials. Additionally, rising government fundings and incentives for carbon capture and utilization projects have encouraged manufacturers to develop innovative materials. The presence of key industry players and research institutions focused on sustainable construction solutions further supports market expansion. North America continues to witness substantial market growth with growing concerns over climate change and corporate commitments to carbon neutrality.

Carbon Capture Construction Materials Market – Key Players and Competitive Analysis Report

Leading market players are investing heavily in research and development to expand their product lines, which will boost the carbon capture construction materials market growth during the forecast period. Market participants are also undertaking a variety of strategic activities to expand their footprint across the world, with important market developments such as new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market scenario, the carbon capture construction materials market players must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the carbon capture construction materials market to benefit clients. A few major players in the market are CarbonCure Technologies Inc.; FLSmidth A/S; Calix; Exxon Mobil Corporation; Halliburton; Linde PLC; MITSUBISHI HEAVY INDUSTRIES, LTD.; SLB; and Fluor Corporation.

FLSmidth & Co. A/S, founded in 1882 and headquartered in Valby, Denmark, provides flowsheet technology and service solutions for the mining and cement industries across multiple regions. The company operates in three segments—mining, cement, and non-core activities. Its offerings include equipment and services for various processes such as crushing, grinding, filtration, and material handling. FLSmidth serves industries such as aggregates, cement, mining, and more. In September 2021, FLSmidth and Chart Industries scaled Cryogenic Carbon Capture, aiming for 95–99% CO₂ removal, with promising cement industry applications.

Halliburton, founded in 1919 and based in Houston, Texas, provides energy industry services through two segments—completion and production, and drilling and evaluation, offering a wide range of production, drilling, and digital solutions. In February 2024, Halliburton's CorrosaLock cement system enhanced CO₂ storage infrastructure by providing chemical resistance, corrosion protection, and improved mechanical integrity for CO₂ pipelines in water-present storage wells, minimizing cyclic loading impacts.

List of Key Companies in Carbon Capture Construction Materials Market

- Calix

- CarbonCure Technologies Inc.

- Exxon Mobil Corporation

- FLSmidth A/S

- Fluor Corporation

- Halliburton

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- SLB

Carbon Capture Construction Materials Industry Development

In December 2024, SLB Capturi completed the world’s first industrial-scale carbon capture plant at Heidelberg Materials' Brevik facility, set to reduce CO₂ emissions by 400,000 metric tons annually.

In September 2024, Heidelberg Cement and FLSmidth launched the first full-scale carbon capture project at Norcem Brevik, Norway, using solvent-based CO₂ removal and plant modifications to reduce emissions.

In September 2024, FLSmidth and Carbon8 Systems partnered to expand carbon capture in cement, using CO₂ and bypass dust to create lightweight construction aggregates, supporting FLSmidth’s MissionZero goal for zero-emission production by 2030.

Carbon Capture Construction Materials Market Segmentation

By Technology Outlook (Revenue, USD Million, 2020–2034)

- Post-Combustion

- Industrial Process

- Pre-Combustion

- Oxy-Combustion

By Application Outlook (Revenue, USD Million, 2020–2034)

- Commercial

- Residential

- Industrial

- Others

By End-Use Industry Outlook (Revenue, USD Million, 2020–2034)

- Steel

- Iron

- Cement

- Others

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Carbon Capture Construction Materials Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2024 | USD 27.98 Million |

| Market Size Value in 2025 | USD 39.74 Million |

| Revenue Forecast by 2034 | USD 961.68 Million |

| CAGR | 42.5% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Carbon Capture Construction Materials Market FAQ's

The global carbon capture construction materials market size was valued at USD 27.98 million in 2024 and is projected to grow to USD 961.68 million by 2034.

The global market is projected to register a CAGR of 42.5% during the forecast period.

Asia Pacific dominated the global market in 2024.

A few key players in the market are CarbonCure Technologies Inc.; FLSmidth A/S; Calix; Exxon Mobil Corporation; Halliburton; Linde PLC; MITSUBISHI HEAVY INDUSTRIES, LTD.; SLB; and Fluor Corporation.

The oxy-combustion segment is projected to grow rapidly in the market during 2025–2034.

The commercial segment held the significant market share in 2024.

Download Sample Report of Carbon Capture Construction Materials Market Trends, Global Report, 2025-2034

Please fill out the form to request a customized copy of the research report.