Construction Silicone Sealants Market Growth Trends, 2026-2034

REPORT DETAILS

Market Statistics

Overview

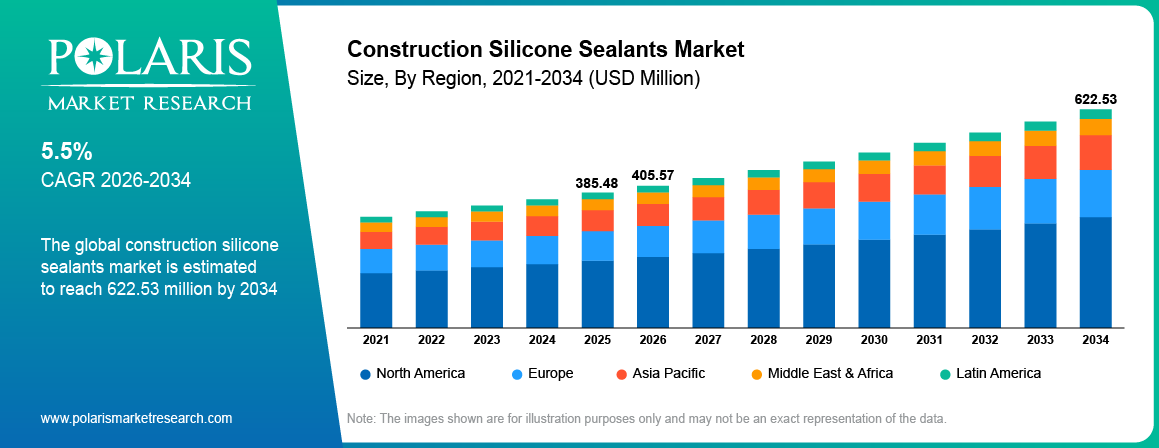

The global construction silicone sealants market is estimated around USD 385.48 million in 2025, with consistent growth anticipated during 2026–2034. Growth is driven by rapid urban construction and rising demand for low VOC sealants across modern building projects. The market is projected to grow at a CAGR of 5.5% during the forecast period.

Key Takeaways:

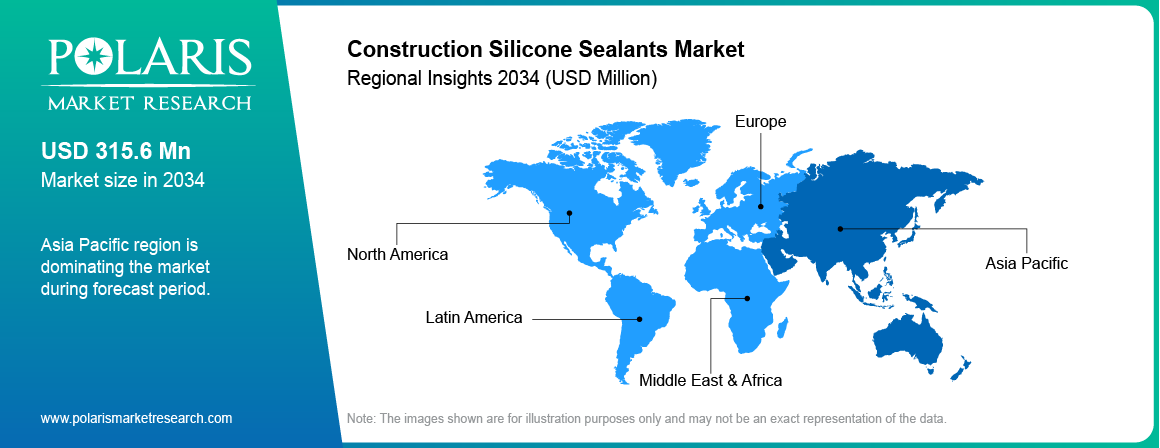

- Asia Pacific accounted for the largest regional share of around 45.6% in 2025, driven by large-scale residential construction, infrastructure development, and rapid urbanization across emerging economies.

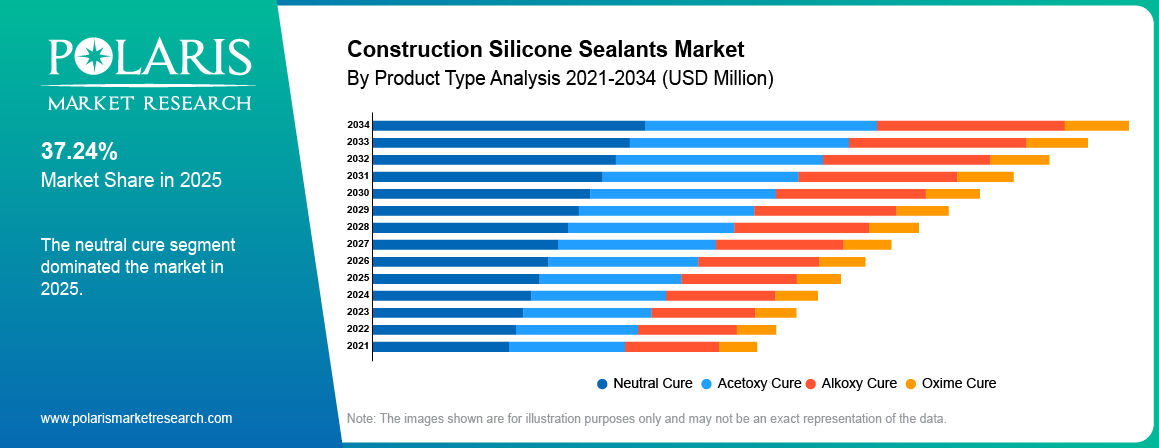

- By Type, Neutral Cure segment accounted for the largest share of approximately 52.3% in 2025, supported by extensive usage in glazing and façade applications due to strong adhesion and durability properties.

- By Application, Glazing segment accounted for the largest share of around 34.7% in 2025, driven by increasing use in commercial buildings, curtain walls, and façade sealing systems.

- By End Use, Commercial Construction segment accounted for the largest share of nearly 49.2% in 2025, supported by growing demand from office spaces, retail complexes, and high-rise infrastructure projects.

Market Statistics

- 2025 Market Size: USD 385.48 Million

- 2034 Projected Market Size: USD 622.53 Million

- CAGR (2026-2034): 5.5%

- Asia Pacific: Largest market in 2025

Industry Dynamics

- The high level of construction activity in urban environments drives the need for high-performance sealing materials in the built environment.

- Product innovation in low VOC materials will drive the adoption of low VOC materials in environmentally compliant construction projects.

- Fluctuation in raw material prices increases production costs for silicone sealant manufacturers.

- Increasing investment in smart city projects creates new demand for advanced construction sealing materials.

What is the Construction Silicone Sealants Market?

Construction silicone sealants is the term used to describe the creation and commercialization of silicone-based sealing materials for use in construction and infrastructure projects. The term includes chemical manufacturers, construction material providers, and construction contractors and developers. These materials are used in the built environment by architects, contractors, and maintenance staff for the sealing of structures, glazing, and facades.

The industry specializes in the supply and distribution of silicone sealants that find application in window glazing, curtain walling, expansion jointing, and sanitary sealing. Manufacturers develop advanced formulations to improve adhesion, weather resistance, and durability across different construction environments. Construction companies and infrastructure developers use these sealants to maintain structural integrity and prevent air and water leakage in buildings.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The construction silicone sealants industry differs from conventional sealant markets based on performance and durability requirements. Traditional sealants have poor resistance to temperature and environmental changes. Silicone sealants have high flexibility, UV stability, and long life in various construction applications. This is beneficial in the design of new constructions and the efficiency of construction project maintenance.

Drivers & Opportunities

Rapid urban construction activities: The rate of growth in new constructions of residential and commercial properties generates the need for construction materials in building structures. Silicone sealants support long term joint sealing across glazing systems, façade installations, and expansion joints. According to the United Nations, around 68% of the global population may live in urban areas by 2050, compared to about 55% in 2022. Expanding urban infrastructure projects increase the use of high-performance construction sealants. This is a growing trend that will fuel the construction silicone sealants market.

Product innovation in low VOC sealants: Manufacturers of construction silicone sealants have been focusing on the development of environmentally compliant products such as low VOC silicone sealants. Sustainable construction practices emphasize the use of environmentally friendly construction materials that have long-term life expectancy. Leadership in Energy and Environmental Design (LEED) green certification programs encourage the use of low emission construction materials in building construction.

Restraints & Challenges

Fluctuation in raw material prices: Silicone-based sealants require petrochemical-based raw materials like siloxane compounds and special additives. Fluctuations in the prices of chemical-based materials make the cost of producing silicone-based sealants high for manufacturers. Companies in the construction industry experience margin pressure due to the unstable prices of construction materials. These unstable prices are a major issue for the construction silicone-based sealant industry.

Opportunity

Increasing investment in smart city projects: Governments in many countries are investing more in the development of smart cities and urban infrastructures. For example, in the Union Budget 2024-25 of India, the Smart Cities Mission received a budget of USD 19.67 billion, with 7,502 of the 8,062 projects being completed by March 2025 and 560 in progress. New and innovative constructions require long-lasting materials for the facades of buildings, glass structures, and transport infrastructures. Smart buildings and integrated urban infrastructure increase the use of high-performance silicone sealants across construction projects.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report offers detailed coverage of the construction silicone sealants market by product type, application, and end-use industry to help readers identify the fastest expanding and most attractive demand segments.

By Product Type

-

Neutral Cure

Neutral cure dominated the market in terms of market share in 2025. This is because of high adoption rates in glazing, sealing of facades, and structural applications. High durability, low odor formulation, and adhesion properties across various substrates ensure high usage rates of neutral cure sealants in modern constructions.

-

Alkoxy Cure

The alkoxy cure segment is projected to grow at the fastest CAGR during the forecast period due to rising demand for low VOC and environmentally compliant sealing materials. Expanding green building standards and sustainable construction practices increase the adoption of alkoxy cure silicone sealants across residential and commercial construction.

By Application

-

Glazing

The glazing segment accounted for the largest market share in 2025, driven by rising installation of curtain wall systems and glass façade structures in commercial buildings. High performance sealing requirements in structural glazing systems increase the demand for silicone sealants across this application.

-

Roofing

The roofing segment is expected to experience the highest CAGR during the forecast period. This is attributed to the increasing rate of residential and commercial constructions. Silicon sealants ensure weather resistance and sealing properties in roof joints.

By End-Use Industry

-

Commercial

Commercial dominated the market in terms of market share in 2025. This is attributed to the expansion of office complexes, commercial centers, and high-rise constructions. High-scale constructions require durable sealing materials in glazing, sealing of facades, and structural applications.

-

Infrastructure

The infrastructure segment is expected to experience the highest growth rate during the forecast period. This is attributed to increasing investments in transportation infrastructure, public infrastructure, and smart city initiatives. Silicone sealants find application in joint sealing and structural protection in bridges, airports, and transportation infrastructure.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

Asia Pacific Market Assessment

Asia Pacific construction silicone sealants market dominated in 2025 driven by rapid urban construction across China, India, and Southeast Asia. Governments are increasing investments in housing, commercial buildings, and transport infrastructure. The Asian Development Bank estimates Asia requires over USD 26 trillion or USD 1.7 trillion per year in infrastructure investment between 2016 and 2030. Rising infrastructure projects increase demand for construction silicone sealants across the region.

North America Construction Silicone Sealants Market Insights

North America construction silicone sealants market is projected to grow at the fastest CAGR during the forecast period driven by strong renovation and commercial construction activities across the US and Canada. Demand for energy efficient buildings increases the use of high-performance sealants in glazing and façade systems. According to the U.S. Census Bureau, the U.S. construction spending in December 2025 reached an annual rate of USD 2.16 trillion, up 0.3% from prior month. This trend supports expansion of the regional market.

Europe Construction Silicone Sealants Market Overview

Europe construction silicone sealants market accounted for the second largest share driven by rising demand for sustainable construction materials. The European Commission’s Renovation Wave aims to renovate 35 million buildings by 2030 to improve energy efficiency and support 160,000 green construction jobs. Germany, France, and the UK are investing in green building projects and infrastructure renovation. This is boosting the application of silicone sealants in modern construction systems.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The competitive environment for the construction silicone sealants market is characterized by the emphasis that is laid on the performance of the product. Manufacturers are investing in the development of advanced silicones that provide durability and adhesiveness for construction projects. The collaboration of construction companies, distributors of construction materials, and infrastructure development helps the adoption of the product for modern construction projects.

The leading companies in the construction silicone sealants market are Dow Inc., Wacker Chemie AG, Shin‑Etsu Chemical Co., Ltd., Momentive Performance Materials Inc., Sika AG, Henkel AG & Co. KGaA, Arkema S.A., 3M Company, Soudal Group, H.B. Fuller Company, Bostik, Tremco CPG, and many more.

Key Players

- 3M Company

- Arkema S.A.

- Bostik

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco CPG

- Wacker Chemie AG

Industry Developments

- October 2025: Sika introduced a refreshed range of construction sealants that retain the same trusted performance and quality, now offered in updated and streamlined Sika packaging.

- March 2024: Dow launched the industry’s first carbon-neutral silicone adhesive for building façades, designed for structural glazing, insulating glass, and weather-sealing applications to support low-carbon construction materials.

Construction Silicone Sealants Market Segmentation

By Product Type Outlook (Revenue, USD Million, 2021-2034)

- Acetoxy Cure

- Neutral Cure

- Alkoxy Cure

- Oxime Cure

By Application Outlook (Revenue, USD Million, 2021-2034)

- Flooring

- Glazing

- Sanitary & Kitchen

- Roofing

- Gap Filling

- Windows

- Others

By End-Use Industry Outlook (Revenue, USD Million, 2021-2034)

- Residential

- Commercial

- Industrial

- Infrastructure

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Construction Silicone Sealants Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 385.48 Million |

| Market Size in 2026 | USD 405.57 Million |

| Revenue Forecast by 2034 | USD 622.53 Million |

| CAGR | 5.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Construction Silicone Sealants Market FAQ's

The global market size was valued at USD 385.48 million in 2025 and is projected to grow to USD 622.53 million by 2034.

Asia Pacific dominated due to rapid urban construction and expanding infrastructure development across China, India, and Southeast Asia.

Major applications include glazing, roofing, sanitary and kitchen sealing, windows, flooring joints, and gap filling across residential and commercial buildings.

A few of the key players in the market are Dow Inc., Wacker Chemie AG, Shin Etsu Chemical Co., Ltd., Momentive Performance Materials Inc., Sika AG, Henkel AG & Co. KGaA, Arkema S.A., 3M Company, Soudal Group, H.B. Fuller Company, Bostik, Tremco CPG, and others.

Key factors include rapid urban construction activities and rising investments in smart city infrastructure projects.

Download Sample Report of Construction Silicone Sealants Market

Please fill out the form to request a customized copy of the research report.