CT Scanner Market Opportunity & Share, Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

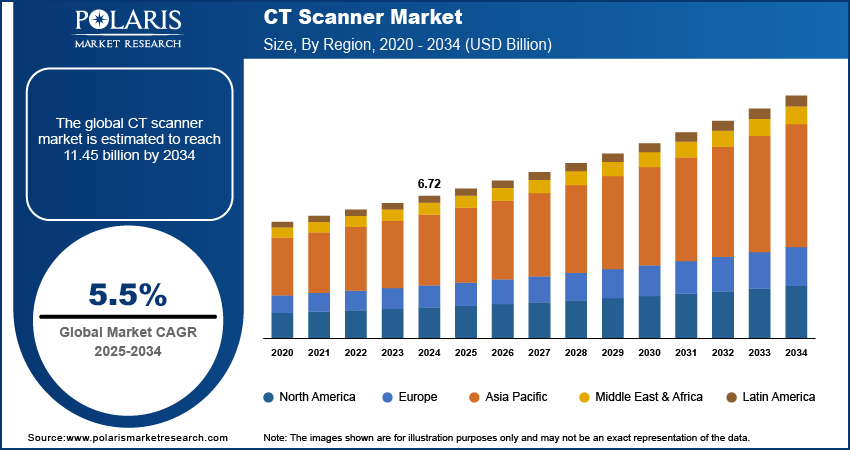

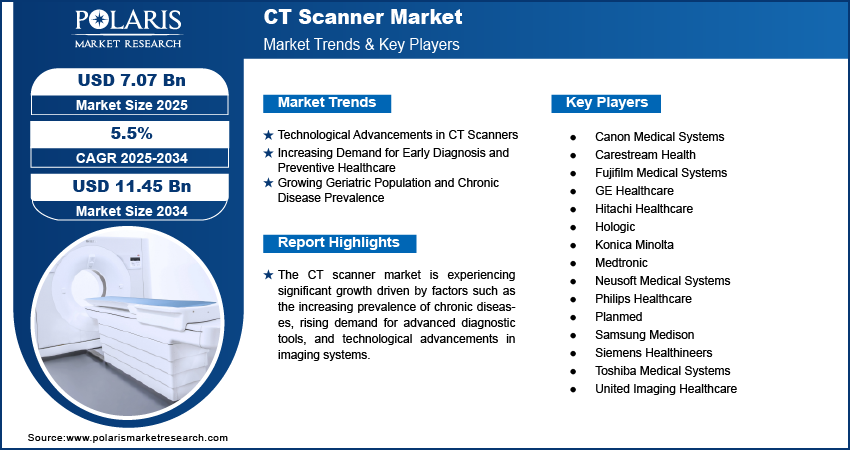

The global CT scanner market size was valued at USD 7.07 billion in 2025. The market is projected to account for a CAGR of 5.5% between 2026 and 2034. The market is driven by increasing cases of chronic diseases, a growing demand for early and accurate diagnostic tools, and improvements in imaging technologies. The market is also benefiting from investments in healthcare services, especially in developing economies and aging populations that require frequent diagnostic imaging. The computed tomography market is further fueled by the expansion of outpatient diagnostic imaging, increasing emergency and trauma imaging cases, and the replacement of older installed imaging systems. There is also a growing need for advanced CT imaging technologies that provide fast imaging, efficient workflow, and low patient dose in a fast-paced clinical environment.

Key Insights

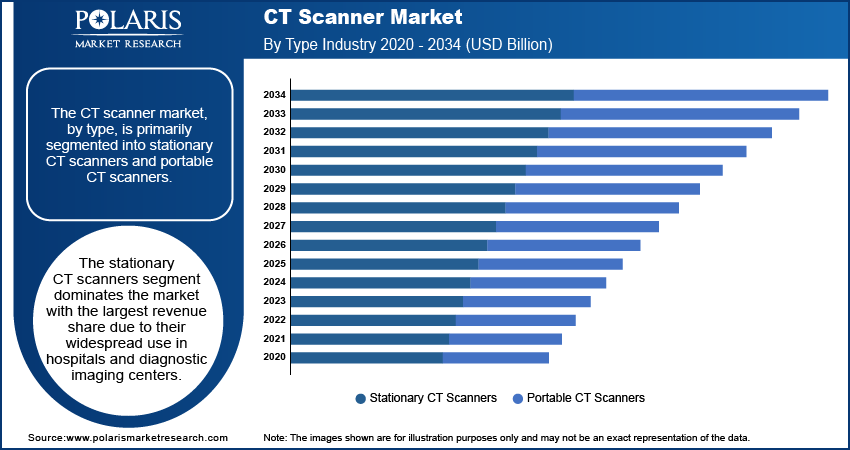

- The stationary CT scanners segment leads the market. This is due to their high adoption in hospitals and imaging centers.

- The O-arm CT scanners segment is witnessing the fastest growth. The segment’s growth is driven by its increasing application in spinal surgeries and other orthopedic procedures.

- North America holds the largest market share. The market dominance of North America is due to its advanced healthcare infrastructure and the presence of key manufacturers and research institutions.

- The Asia Pacific CT scanner market is registering the fastest growth. Rapid advancements in healthcare infrastructure, especially in emerging economies, drive the regional market growth.

Industry Dynamics

- The increased demand for CT scans is driven by the prevalence of chronic diseases, the aging population, and the need for precise, non-invasive diagnostic procedures.

- The market for CT scans is driven by technological advancements, healthcare investments, and the growing use of CT scans for emergency care, oncology, and cardiovascular diagnostics.

- Challenges such as high equipment costs and radiation exposure may affect market growth. The market development may also be affected by the shortage of skilled professionals in developing regions.

- Innovations in low-dose imaging, portable CT technology, and faster scanning are improving the efficiency of medical imaging.

Market Statistics

2025 Market Size: USD 7.07 billion

2034 Projected Market Size: USD 11.45 billion

CAGR (2026-2034): 5.5%

North America: Largest market in 2025

AI Impact on CT Scanner Market

- The analysis of medical imaging data by AI ensures improved accuracy and early detection of abnormalities. The use of AI helps in reducing errors in the analysis of CT scans.

- The integration of AI in medical imaging helps in the reconstruction and optimization of medical images in real time. This ensures that the quality of the medical image is improved while exposure to radiation is minimized.

- The use of AI in medical imaging improves the efficiency of a CT scanner by predicting its maintenance requirements. This ensures improved imaging operations in healthcare settings.

- The tools also aid in the automation of the workflow and prioritization of critical cases. Additionally, AI tools help in clinical decisions in radiology departments.

- Apart from image interpretation, AI technology is also being used in the CT scanner market for dose optimization, organ identification, scan selection, and workflow automation.

- AI in medical imaging helps healthcare facilities in the efficient use of the CT scanners, thus reducing the time taken for reporting and minimizing the waiting time.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

The computed tomography (CT) scanner market entails the creation and production of computed tomography scanners that are employed for imaging purposes. A computed tomography scanner uses X-rays to produce an image of the body’s inner structures. These images aid in diagnosis and treatment planning.

The advancements in technology, such as image resolution, scanning time, and integration with artificial intelligence for better diagnostic accuracy, are driving the growth of the CT scanners market. In addition to this, the need for timely diagnosis of diseases, the aging population, and the prevalence of chronic conditions such as cancer and cardiovascular diseases are also contributing to the market expansion. The trends that are expected to drive market development include the shift towards compact and portable CT scanners and the integration of hybrid imaging systems with CT scanners and other imaging modalities such as MRI and PET CT scanner.

Market Dynamics

Technological Advancements in CT Scanners

Significant advancements have been made in the hardware and software technology of CT scanners. The modern technology of the CT scanners provides better resolution and speed, as well as low exposure levels. For example, the multi-slice CT scanners that use multiple slices to produce clear images have become quite popular. Additionally, the use of AI and ML in the interpretation and diagnosis of images has also become quite effective. This is because AI and ML have the ability to recognize various patterns that might be missed by the radiologist. The recent advances in the technology of CT scanners have also led to the use of photon-counting CT, spectral CT, and AI-enabled reconstruction. They also make image acquisition processes easier. These technologies are particularly useful in cardiology, oncology, pediatrics, and trauma imaging. In these fields, speed, accuracy, and lower doses of radiation are a priority.

Increasing Demand for Early Diagnosis and Preventive Healthcare

Another important factor driving market growth is the emphasis on early disease detection and preventive healthcare. Early diagnosis of diseases like cancer, cardiovascular diseases, neurological problems, and others improves the chances of recovery. As the importance of early disease detection is recognized in the healthcare industry, there is a growing demand for diagnostic equipment such as CT scans. Low-dose CT scans are being employed within various screening programs, especially for patients at higher risk. This once again underlines the importance of CT scans as a diagnostic tool for various diseases as well as a means of preventive medicine. As a result, there is a growing emphasis within the healthcare industry to develop efficient and user-friendly equipment.

Growing Geriatric Population and Chronic Disease Prevalence

Older people are more susceptible to getting various health conditions, such as cardiovascular diseases, cancer, and neurological disorders. These health conditions require diagnostic imaging services. According to the World Health Organization, the global population of people aged 60 and above is projected to increase from 1.1 billion by 2023 to 2.1 billion by 2050. Chronic diseases, such as diabetes and hypertension, are common among older people. These conditions may require diagnostic imaging services for the monitoring of their associated complications. CT scanners are a common diagnostic tool for managing age-related health conditions. Therefore, the aging population is a significant driver of the CT scanner market.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Insights

By Type-Based Insights

The CT scanner market, by type, is primarily segmented into stationary CT scanners and portable CT scanners. Each of these types caters to different healthcare needs. Stationary CT scanners lead the market with the largest revenue share. This is because of their wide use in hospital settings and in diagnostic imaging clinics. Stationary CT scanners have high-resolution imaging and are used in more complex procedures. This makes them essential in cases where high-quality imaging is necessary. These devices have sophisticated features, including multi-slice and high-speed scanning. These help in quick diagnoses of serious health conditions. The demand for stationary CT scanners is expected to be high because of the increased need for high-quality imaging in cancer, cardiovascular, and neurological studies. Stationary CT systems continue to be the preferred choice for high-volume healthcare facilities. Such facilities demand systems that can perform large volumes of scans and meet various clinical needs. These hospital CT scanner systems are also used for advanced applications that include cardiac CT, oncology imaging, and procedure planning.

Portable CT scanners are expected to experience rapid growth in the forecast period. These CT scanners are becoming increasingly popular because they can provide imaging services in emergency rooms, intensive care units, and rural areas where larger CT scanners may not be available. Portable scanners also reduce the need to move patients, lowering transport risks and improving patient care. The increased emphasis on point-of-care diagnostics and trauma cases is expected to further boost the segment's growth. Their use is also on the increase in stroke care, postoperative monitoring, and critical care. Here, bedside imaging helps in reducing delays and enables doctors to meet the needs of patients more quickly.

By Device Architecture-Based Insights

The CT scanner market is segmented by device architecture into C-arm CT scanners and O-arm CT scanners. The C-arm CT scanners segment has the largest share in the global CT scanners market. This is mainly because C-arm CT scanners have been in use for a long time in interventional procedures and surgeries. C-arm CT scanners are often used in orthopedic, neurological, and trauma surgeries. These CT scanners offer real-time imaging during complex procedures. C-arm CT scanners are also very effective in minimally invasive surgeries, allowing doctors to obtain a clear view without large incisions. Their widespread adoption in hospitals and outpatient surgery centers has contributed to the dominance of this segment.

The O-arm CT scanners segment is growing at the fastest rate. This is due to the increased use of these devices in spinal surgeries and other orthopedic procedures. O-arm systems have the advantage of providing 3D imaging, which helps in improving the visualization of the surgery. Hence, these devices are very popular in operating rooms. Additionally, the segment's growth can be attributed to technological advancements that have improved the functionality and affordability of these devices. Hence, O-arm CT scanners are now available in a wider market. The growing focus on improving surgical outcomes and reducing patient recovery time is also contributing to the increased demand for these devices.

By Technology-Based Insights

The CT scanner market is segmented by technology into high-slice CT, mid-slice CT, low-slice CT, and cone beam CT (CBCT). The high-slice CT segment holds the largest market share because of its capacity to deliver high-resolution images at faster scan speeds. Such systems play an important role in complex diagnostic procedures that involve the use of cardiovascular imaging, oncology, and neurology. Here, detailed imaging is essential for the visualization of the body’s internal structures. The use of high-slice CT scanners is increasing in major hospitals and diagnostic centers. At the same time, interest is growing in the use of spectral imaging and photon-counting CT technology. This improves the visualization of lesions and allows doctors to better differentiate between various tissues. It increases diagnostic confidence in advanced imaging techniques.

The cone beam CT (CBCT) segment is witnessing the fastest growth rate. The growth of the segment is mainly attributed to the application of the segment in dental and orthopedic procedures. The segment offers a unique advantage over other CT scanners by delivering 3D imaging with lower radiation doses. CBCT scanners are mainly applied in dental imaging systems and maxillofacial procedures. They provide high-resolution imaging in a compact format. The advancements in cone beam CT technology, like better image quality and artificial intelligence in medical diagnostics, are contributing to the growth of this segment. The rising demand for compact specialty-focused imaging devices is also expected to increase the use of CBCT technology in ambulatory and specialty care settings.

By Application-Based Insights

The CT scanner market, by application, is segmented into human, veterinary, and research. The human application segment holds the largest market share. It is fueled by the increased use of CT scanners in the diagnosis and treatment of various diseases and health conditions. These conditions include cancer, cardiovascular diseases, and neurological disorders. CT scanners are an essential tool in healthcare, including hospitals and clinics. These devices provide essential services during routine health checks and in emergency medical situations. The rising need for advanced technology in diagnosis and the development of technology are contributing factors to the segment's dominance. Additionally, the segment benefits from the increased incidence of various health conditions in the global population.

The veterinary segment is experiencing the fastest growth, driven by the growing use of advanced imaging technologies in veterinary medicine. As the focus on animal health and well-being is increasing, the use of CT scanners in veterinary medicine is becoming more common. CT scanners are being used for the diagnosis and treatment of injuries, tumors, and neurological conditions in pets, livestock, and other animals. The use of CT scanners in veterinary medicine is fueled by the increase in pet ownership, advances in veterinary medicine, and the increasing requirement for non-invasive imaging solutions. In addition, the interest in research and development in animal health products is boosting the use of CT scanners in veterinary medicine.

By End-Use-Based Insights

The CT scanner market, by end-use, is segmented into hospitals & diagnostic centers, research laboratories & academic institutes, ambulatory care centers, and others. The hospitals & diagnostic centers segment has the largest share in the market. This is mainly because of the high demand for advanced diagnostic imaging. Hospitals and diagnostic centers are the primary places where CT scanners are used in routine and emergency patient diagnosis, including oncology, cardiology, and trauma cases. These centers benefit from the high-resolution imaging, fast scanning speed, and wide range of applications available in modern CT scanners.

The ambulatory care centers segment is growing at the fastest rate. This can be attributed to the rising trend of outpatient care. The need for effective, cost-efficient diagnostic services outside the hospital setting is also fueling demand for this segment. With the advent of mobile, smaller CT scanners, ambulatory care centers can now provide high-quality imaging services without hospital admission. The segment is also benefiting from the increasing demand for outpatient services, faster recovery rates, and reduced healthcare costs. These are providing a boost to ambulatory care centers as a solution for both patients and healthcare providers. New imaging modalities are also helping these centers provide services more accessibly.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

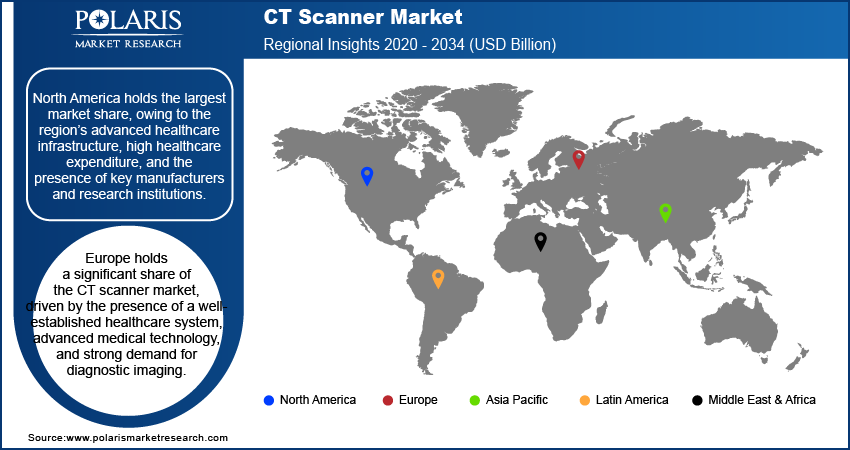

Regional Analysis

By region, the study covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The market for CT scanners is well diversified and covers various regions. Among these regions, the North America CT scanner market holds the largest market share. This is due to the better healthcare infrastructure and the higher healthcare spending in the region. Moreover, the presence of key players and research centers also drives market development in the region. The US contributes the most to the market share of North America due to the higher demand for diagnostic imaging in the country. Additionally, the incidence of chronic diseases and the growing geriatric population drive the regional market dominance. Replacement of older imaging systems, strong adoption of premium CT technologies, and continued investment in emergency and specialty care imaging are also supporting the region’s market leadership.

The Europe CT scanner market holds a significant share of the global market. The well-developed healthcare infrastructure, advanced healthcare technology, and demand for diagnostic imaging are some of the factors sustaining the market. The market is driven by high healthcare spending among the population, a major factor in countries like Germany, France, and the UK. This enables the population to access the latest diagnostic imaging technology. The importance of early diagnosis imaging and personalized medicine is creating a demand for CT scanners. Medical device manufacturers are contributing to market growth. The demand for hybrid imaging is creating a demand for CT scanners. Hybrid imaging combines CT with other imaging modalities.

The Asia Pacific CT scanner market is experiencing the fastest growth. The CT scanner market in this region is influenced by the rapid development of healthcare infrastructure, particularly in countries such as China, India, Japan, and South Korea. The increase in healthcare expenditure, along with greater awareness of early disease detection and the adoption of non-invasive diagnostic techniques, is fuelling demand for CT scanners. The prevalence of chronic diseases such as cancer and cardiovascular diseases is also creating a strong requirement for advanced diagnostic equipment. In addition, governments are spending more on healthcare infrastructure upgrades. The demand for compact, portable, affordable CT scanners is contributing to market growth in emerging economies. Asia Pacific also provides strong opportunities for vendors that offer cost-effective systems with scalable service options and portable imaging solutions suited for large and diverse patient populations.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

Some of the CT scanner market key players include Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, FUJIFILM, Samsung Medison, Carestream Health, Neusoft Medical Systems, United Imaging Healthcare, Konica Minolta, Medtronic, Hologic, Planmed, and other regional and specialty medical imaging OEMs. There are a number of companies that are engaged in the development, manufacturing, and distribution of CT scanners in various regions. Companies like Siemens Healthineers and GE HealthCare offer a variety of imaging solutions in several medical domains. There are other companies, such as Canon Medical Systems Corporation and Hitachi Healthcare, that offer advanced imaging solutions for specific purposes. The products developed by these companies are intended to ensure proper diagnosis, reduce radiation dose, and enhance efficiency during imaging procedures. These companies remain major players in this industry and are introducing various technologies to ensure non-invasive diagnostic procedures in the healthcare sector. Companies like Canon Medical Systems are also focusing on design innovations related to imaging devices, such as compact CT scanners that are portable.

Pricing and service also play important roles in competition. Organizations that offer full-service packages, including installations, maintenance, training, software updates, and workflow support, have a high chance of establishing long-term relationships with customers. Other factors that influence the competitive landscape in the CT scanner market include AI-enabled software platforms, dose management, scanner reliability, and serving large hospitals and cost-sensitive markets in emerging regions.

Siemens Healthineers is a prominent player in the industry. The company is recognized for its range of medical imaging technologies. Siemens Healthineers offers CT scanners with high imaging quality for a variety of diagnostic requirements. These range from routine exams to complex procedures. The company is focused on incorporating AI and software solutions in its products.

GE Healthcare is another leading player in the market. The company offers a range of imaging technologies, including CT scanners. GE Healthcare is recognized for its reliable and cost-effective solutions. These solutions are used in a variety of healthcare settings. The company is focused on making its imaging solutions more accessible. This is in line with its focus on developing imaging solutions with improved diagnostic capabilities.

List of Key Companies

- Canon Medical Systems

- Carestream Health

- FUJIFILM

- GE HealthCare

- Hologic

- Konica Minolta

- Medtronic

- Neusoft Medical Systems

- Philips Healthcare

- Planmed

- Samsung Medison

- Siemens Healthineers

- United Imaging Healthcare

CT Scanner Industry Developments

March 2025: Siemens Healthineers announced that it received FDA clearance for an expanded class of its Naeotom Alpha photon-counting computed tomography (PCCT) scanners. According to Siemens, the approval marked a major expansion of the premium imaging portfolio.

December 2024: Siemens Healthineers launched a significant upgrade for its SOMATOM CT scanner platform. The upgraded version is intended to deliver improved image performance, speed up scans, and lower doses of radiation for patients. This is part of the company’s ongoing commitment to developing more advanced medical imaging technologies.

November 2024: GE HealthCare launched a new version of Revolution CT. This upgraded version of the Revolution CT offers improved image quality and speed. It is part of the company’s commitment to providing clinicians with more efficient technologies for diagnosing complex diseases while keeping patients safe.

Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Stationary CT Scanners

- Portable CT Scanners

By Device Architecture Outlook (Revenue, USD Billion, 2021–2034)

- C-Arm CT Scanners

- O-Arm CT Scanners

By Technology Outlook (Revenue, USD Billion, 2021–2034)

- High-Slice CT

- Mid-Slice CT

- Low-Slice CT

- Cone Beam CT (CBCT)

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Human

- Veterinary

- Research

By End-Use Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals & Diagnostic Centers

- Research Laboratories & Academic Institutes

- Ambulatory Care Centers

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

CT Scanner Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 7.07 billion |

| Market Size in 2026 | USD 7.44 billion |

| Revenue Forecast by 2034 | USD 11.45 billion |

| CAGR | 5.5% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | CT Scanner Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

How is the report valuable for an organization?

Workflow/Innovation Strategy

The CT scanner market has been segmented into detailed segments of type, device architecture, technology, application, and end-use. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy

The growth strategy adopted in the CT scanner market is based on continuous innovation, expansion of product offerings, and customer accessibility. The major players are investing in advanced technology such as artificial intelligence, machine learning, and image resolution to improve diagnostic capabilities and reduce scanning times. Companies are also working to make these devices more accessible and cost-effective to serve emerging healthcare markets. Strategic partnerships, acquisitions, and expansion into developing markets are crucial to the marketing strategy for the CT scanner market. By providing customized solutions to diverse healthcare needs, these companies aim to reach a wider customer base and meet the growing demand for high-end diagnostic imaging equipment.

CT Scanner Market FAQ's

The CT scanner market stood at USD 7.07 billion in 2025. The market is projected to reach USD 11.45 billion by 2034.

The market is projected to account for a CAGR of 5.5% between 2026 and 2034.

North America holds the largest market share. This is due to its advanced healthcare infrastructure and high healthcare expenditure.

Some of the key market players include Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, FUJIFILM, Samsung Medison, Carestream Health, Neusoft Medical Systems, United Imaging Healthcare, Konica Minolta, Medtronic, Hologic, and Planmed.

The stationary CT scanners segment accounts for the largest market share. This is due to the widespread use of stationary CT scanners in hospitals and diagnostic imaging centers.

A computed tomography (CT) scanner is a medical imaging device that uses X-rays and computer technology to produce detailed cross-sectional images of the body. This helps healthcare providers view the inside of the body in a non-invasive way.

A few of the key market trends include the integration of artificial intelligence, the rising adoption of portable and compact CT scanners, and the development of hybrid imaging systems.

Download Sample Report of CT Scanner Market

Please fill out the form to request a customized copy of the research report.