Market Overview

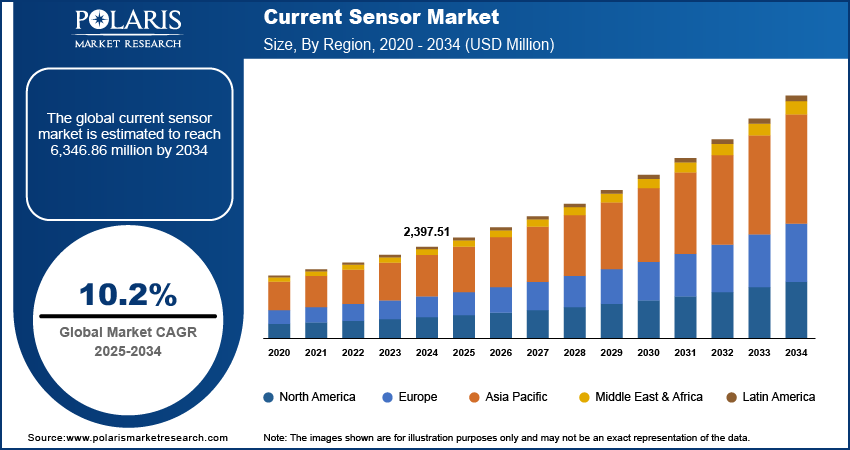

The current sensor market size was valued at USD 2.72 billion in 2025. According to our current sensor industry analysis, the market is projected to grow at a CAGR of 10.2% from 2026 to 2034. A CAGR of indicates that the market is growing on a structural level and is not experiencing short-cycle growth. This is because the market is driven by major trends such as the adoption of electric vehicles, Industry 4.0, renewable energy, and semiconductor advancements. Compared with other markets such as voltage sensors and power semiconductors, the current sensor market is growing faster due to its applications in battery management systems, motor drives, and inverter systems.

Market growth is primarily driven by increasing demand for industrial automation and the need for real-time current measurement in smart grid systems. The trend toward high-efficiency power electronics in electric vehicles, solar inverters, data centers, and robotics is also fueling demand for small, accurate current-sensing solutions.

Key Insights

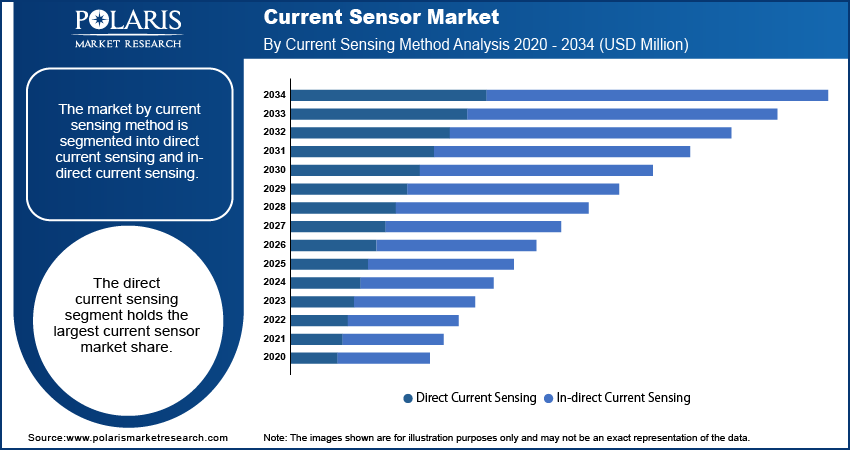

- The direct current sensing segment accounts for the largest market share. This is due to its high accuracy and simplicity.

- The open loop segment is witnessing notable growth, owing to its significant price benefit over closed-loop sensors.

- The Hall effect segment accounted for the largest market share in 2025. The segment’s dominance is attributed to the ability of these sensors to measure both AC and DC currents.

- Asia Pacific led the market in 2025. This is attributed to the high rate of urbanization as well as the adoption of electric vehicles in the region.

- The Europe market is expected to experience significant growth. This is attributed to the focus of the region on automating industries, as well as the adoption of renewable energy sources.

Industry Dynamics

- The increasing use of electric vehicles has driven the demand for advanced current sensors.

- The adoption of strict energy efficiency policies by governments worldwide is influencing the market dynamics.

- The increasing use of artificial intelligence for energy efficiency and predictive maintenance is presenting several market opportunities.

- Inaccuracies in extreme environmental conditions may restrain market growth.

Market Statistics

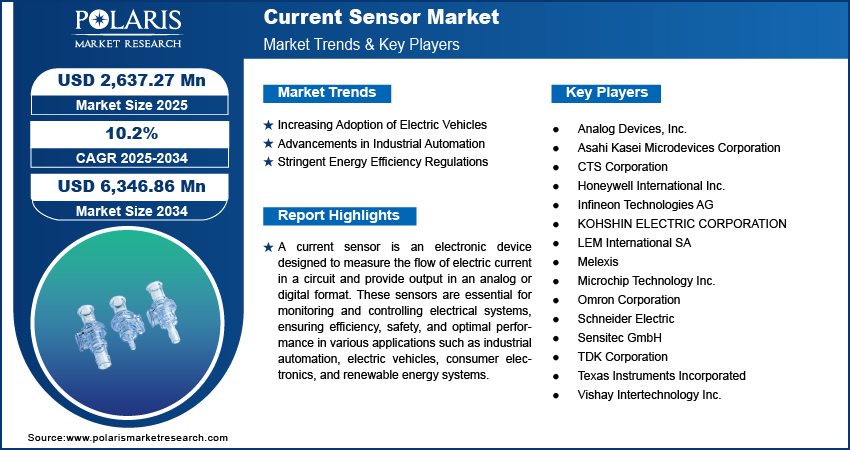

2025 Market Size: USD 2.72 billion

2034 Projected Market Size: USD 6.49 billion

CAGR (2026-2034): 10.2%

Asia Pacific: Largest Market in 2025

To Understand More About this Research:Request a Free Sample Report

AI Impact on the Current Sensor Market

- AI-based calibration methods enhance sensor accuracy, thereby minimizing current measurement errors in automotive, industrial, and consumer applications.

- In addition to the fundamental calibration process, integrating AI in current sensors technology enables the system to identify potential errors in the EV battery pack and the industrial motor configuration before they occur. By analyzing patterns and anomalies in the current waveform, the AI system can detect signs of overheating, insulation degradation, and power instability.

- Machine learning algorithms enable self-diagnosis and anomaly detection, which assist sensors in predicting faults.

- AI-powered current sensors assist in the efficient management of electricity flow in a smart grid network. It does so by supporting dynamic load balancing and grid stabilization. This enhances grid robustness, particularly when handling voltage instability and the intermittent nature of renewable energy sources like solar and wind.

- The integration of edge computing and digital current sensors is making conventional hardware intelligent sensing units that are capable of processing data and making decisions in real time. These units are not only capable of measuring current but also analyzing patterns, identifying problems, and making decisions quickly, making them ideal for use in the IoT industrial environment.

- Integration with AI control systems enhances real-time monitoring and energy efficiency in the ecosystems.

The rising need for energy-saving solutions, along with the increasing adoption of automation technologies in industrial settings, is driving the current sensor market. The market growth is also fueled by the rising adoption of electric vehicles. Current sensors are essential devices for detecting and controlling the flow of electrical current. Market development is fueled by technological advancements, which integrate Hall-effect sensors with Rogowski-coil sensors to provide better accuracy and reliability. The growing need for government regulations on energy usage and safety is pushing various industries to adopt current sensors.

A qualitative analysis of the current state of the sensor market indicates a rising trend toward contactless, high-accuracy sensing technology. The rising demand for real-time current measurement in smart grids and renewable energy sources is also driving the market. In addition, the miniaturization of current sensors and their integration into compact electronic devices are driving the demand in the consumer electronics market. The R&D activities are expected to improve sensor efficiency, making them more cost-effective.

Market Dynamics

Increasing Adoption of Electric Vehicles

The rising trend of electric vehicles is a major factor that contributes to the growth of the market. In China, electric vehicles accounted for more than 35% of the total domestic car sales in 2023, meeting the country’s 2025 target for new energy vehicles earlier than expected (International Energy Agency, 2023). Likewise, the US experienced a 40% rise in electric vehicle sales in 2023, which covered about 10% of the car market. The adoption of electric vehicles demands the use of advanced current sensors for efficient battery management and monitoring, thus driving the growth of the market.

Advancements in Industrial Automation

The field of industrial automation is changing. This has resulted in a growing need for accurate current-sensing solutions. The adoption of advanced automation technologies across industries has driven a growing need for accurate current measurement. This is to ensure efficiency and safety. The government's smart manufacturing and Industry 4.0 initiatives have also contributed to this growing need for current sensors.

Stringent Energy Efficiency Regulations

Governments around the world are also enforcing strict energy-efficiency policies to address environmental impacts, thereby affecting the current sensor market. For example, India's pledge to achieve net-zero emissions by 2070 includes policies that have increased EV adoption from 0.7% in 2020 to 6.3% in 2024. This has resulted in nearly 5 million registered EVs (World Resources Institute, 2025). The policies require accurate current measurement and control. They have increased the use of high-quality current sensors across sectors.

Pricing & Supply Chain Dynamics

The market for current sensors is closely tied to the semiconductor supply chain, the availability of rare-earth elements, and semiconductor wafer fabrication capacity. The Hall effect and magneto-resistive sensor technologies require semiconductor-grade silicon and rare magnetic materials. This makes them vulnerable to semiconductor shortages and trade policies.

During the recent semiconductor shortages, the lead times for current sensor ICs rose dramatically. The semiconductor shortage impact on sensors created pricing pressures in the automotive and industrial sectors. In response to the increasing adoption of electrification, companies are resorting to supply contracts and vertical integration to counter risks and ensure supply.

The current sensor cost structure also differs depending on the technology used. Open-loop sensors are less costly and are used when cost is a consideration. Closed-loop and fluxgate sensors are expensive because of their high accuracy, temperature stability, and resistance to harsh environments.

Technology Benchmarking Analysis

Hall-effect sensors are currently the most popular due to their ability to detect both AC and DC currents. Magneto-resistive sensors are gaining popularity in applications that need compactness and low power consumption. Fluxgate sensors are used in high-end applications because of their high accuracy and stability. Shunt sensors remain a cost-effective alternative, but they lack the electrical isolation offered by other technologies.

When compared across factors such as accuracy, temperature stability, cost, isolation capability, and ease of integration, the market is moving towards digital, highly integrated sensor IC designs that are better compatible with smarter systems.

Segment Insights

Assessment by Current Sensing Method

The current sensor market is segmented by current sensing method into direct current sensing and in-direct current sensing. The direct current sensing segment has the largest market share in the current sensor market. This is because the method is simple, reliable, and accurate. The rising demand for battery-driven products, low-power consumption, and the increasing adoption of renewable energy sources are contributing to the growth of the segment.

The in-direct current sensing segment is experiencing significant growth. Its ability to sense the current without direct electrical access enhances safety and extends the component's lifespan. This is particularly useful for electric vehicles, automation, and power distribution.

Evaluation by Loop

The current sensor market segmentation, based on loop, includes open loop and closed loop. The closed loop segment accounts for the largest market share. These sensors are commonly used to offer an output proportional to the measured current, making them ideal for applications that demand quick response, high linearity, and low temperature drift. Their widespread use in variable-speed drives, ground-fault detectors, robotics, and power supplies contributes to their market dominance.

The open loop segment is also experiencing considerable growth. Open loop sensors have a substantial price advantage over the closed loop sensors. These sensors are most suited due to their compact design and low power consumption. This makes them suitable for battery-powered applications. Further, open-loop sensors offer cost advantages in high current ranges (above 100 A). They usually consume constant power, irrespective of the current being measured.

Outlook by Technology

The current sensor market is segmented by technology into Hall effect, shunt, flux gate, and magneto-resistive. The Hall effect segment accounted for the largest market share in 2025. Hall effect sensors can measure both AC and DC currents without making contact. This makes Hall effect sensors rugged and reliable. They are also very small and affordable. Furthermore, they can withstand harsh environmental conditions, such as high temperatures and strong electromagnetic interference. Advances in semiconductor technology have improved the sensitivity and integration of these sensors. They are widely used for current measurement in industries such as industrial automation, automotive, and consumer electronics.

The magneto-resistive segment is expanding at the fastest rate. This is due to the excellent performance characteristics of magneto-resistive current sensors. Magneto-resistive current sensors have high sensitivity, high accuracy, and a compact design. These characteristics make them suitable for use in advanced applications such as wearables, robots, and drones. Magneto-resistive sensors are finding applications in consumer electronics, especially in true wireless stereo (TWS) earbuds. Technological advancements in magneto-resistive sensors, such as the development of tunnel magneto-resistance (TMR) technology, have ensured high sensitivity and ultra-low power consumption.These advancements are also expected to drive increased use of magneto-resistive sensors.

Assessment by Output

The current sensor market segmentation, based on output, includes analog and digital. The analog segment had the largest share in the current sensor market. This is because analog sensors can provide continuous and real-time signals. These signals are important for applications that need immediate and accurate current readings. Industries such as industrial automation and process control rely heavily on these sensors for their high accuracy and reliability. In addition, there has been an improvement in the development of analog sensors with higher accuracy and lower power consumption. This has made them compatible with advanced control systems.

The digital segment is witnessing considerable growth in the current sensor market. Technological advancements and the rising demand for IoT-enabled devices drive the growth in this segment. Digital sensors have several advantages. They offer noise immunity and can transmit signals over long distances without any degradation. Digital sensors are increasingly used in applications that require fast, accurate data acquisition. These uses include smart grids and battery management systems. The integration of digital sensors with advanced data analytics systems makes them an essential part of modern electronic infrastructure.

Evaluation by Application

The current sensor market is segmented by application into motor drive, converter inverter, battery management, UPS & SMPS, starter & generators, grid infrastructure, and others. The motor drive segment holds the largest market share. This is because of the extensive application of electric motors in different sectors such as the automotive industry, industrial automation, and consumer electronics. Current sensors are an essential part of motor performance measurement. Their use ensures efficient functioning and protection against damage due to overload. The growing use of electric vehicles has been a major contributor to this market share, as accurate current measurement is critical for efficient motor control and energy conservation in electric vehicles. Moreover, the rising focus on automation and the implementation of smart technology in manufacturing processes has increased the requirement for current sensors in motor drives, ensuring efficient functioning and energy conservation.

The starter & generators segment is currently growing at the fastest rate in the current sensor market. This is driven by a significant emphasis on improving energy efficiency and lowering emissions in the automotive and aerospace industries. Current sensors are a critical part of ensuring optimal performance and safety in starter motors and generators, which are essential components in these industries. The current trend of sustainability and government regulations has further driven the adoption of current sensing technology in this segment. The application of current sensors assists in meeting performance needs while enabling the integration of cleaner and more efficient power systems.

Regional Insights

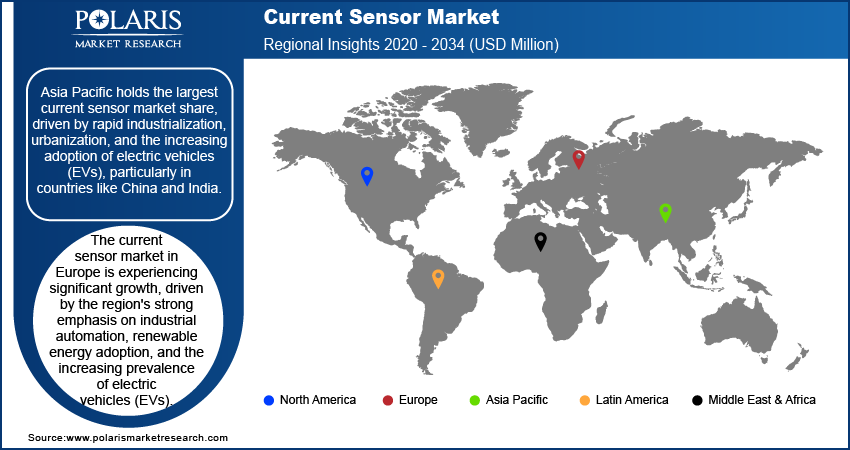

By region, the study provides current sensor market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region had the largest market share in 2025. The Asia Pacific market is fueled by the fast-growing industrialization and urbanization in the region. The region is also fueled by the rising adoption of electric vehicles, especially in China and India. The region has a robust manufacturing base and government plans to implement renewable energy and smart grid solutions, which in turn boost the demand for efficient current-sensing solutions. The region is also witnessing growing interest in energy management and infrastructure.

The current sensor market in Europe is experiencing significant growth. The regional market is driven by its strong emphasis on industrial automation, renewable energy adoption, and the increasing prevalence of electric vehicles (EVs). Germany is one of the most important players. The country has a strong industrial base and is a leader in automotive technology. The emphasis on Industry 4.0 and smart manufacturing has increased the need for high-quality sensors in robotics and predictive maintenance. Likewise, the French market is experiencing significant growth due to heavy investment in renewable energy infrastructure and smart grids. These technologies require accurate current measurement solutions. The UK is also an important player. The country's strong automotive industry and the government's efforts to promote EV infrastructure and carbon emissions reduction have increased the need for efficient current sensing solutions.

Key Players and Competitive Insights

The competitive environment in the current sensor market is marked by fast-paced technological development, collaborative efforts, and geographical expansion. Organizations are heavily investing in R&D activities to improve the accuracy of sensors, lower power consumption, and miniaturize them to meet the demands of the electric vehicle, automation, and renewable energy sectors. The market is experiencing consolidation trends through mergers and acquisitions to enhance technological and geographical reach. The Asia Pacific region holds the largest market share. This is because of the region’s growing automotive production and consumer electronics market. The North America and European markets are also growing due to the adoption of electric vehicles and the integration of renewable energy. However, pricing pressures continue to pose a challenge. This is due to stiff competition that impacts profit margins. Another challenge is the ability to ensure accuracy at different temperatures. Opportunities in the industry are increasing due to the adoption of electric mobility, smart grid systems, and the integration of artificial intelligence.

Honeywell International Inc. is a diversified technology and manufacturing firm that provides a broad portfolio of products and services to different industries such as aerospace, building technologies, performance materials, and safety solutions. In the current sensor industry, Honeywell offers innovative sensing solutions for use in industrial automation, automotive, and energy management applications. The sensors are engineered to provide precise and reliable data to enable efficient system operation across industries.

Texas Instruments Incorporated is a global semiconductor firm. The company specializes in the design and production of analog and embedded processing chips. In the current sensor industry, Texas Instruments has a broad portfolio of current sensing solutions. The solutions are essential in power management and control systems. The company’s products are used in different applications. These include consumer electronics, automotive, and industrial applications. They have accurate measurement functions that are vital for optimal functionality.

List of Key Companies

- Analog Devices, Inc.

- Asahi Kasei Microdevices Corporation

- CTS Corporation

- Honeywell International Inc.

- Infineon Technologies AG

- KOHSHIN ELECTRIC CORPORATION

- LEM International SA

- Melexis

- Microchip Technology Inc.

- Omron Corporation

- Schneider Electric

- Sensitec GmbH

- TDK Corporation

- Texas Instruments Incorporated

- Vishay Intertechnology Inc.

Regulatory & Compliance Landscape

The international regulations regarding energy efficiency, vehicle safety, and smart grid development are propelling the adoption of modern current sensing technology. The standards defined by bodies such as the International Electrotechnical Commission and vehicle safety regulations defined by the International Organization for Standardization mandate precise and temperature-stable current measurement, particularly in electric vehicles and battery management systems.

Government policies regarding net-zero goals and electrification are indirectly driving the demand for current sensors in the transportation, renewable energy, and smart grid sectors.

Current Sensor Industry Developments

March 2025: Honeywell International Inc. acquired Sundyne LLC for USD 2.2 billion. Sundyne LLC is based in Arvada, Colorado, and focuses on the development of highly engineered pumps and compressors for the petrochemical industry, as well as for the liquefied natural gas (LNG) and renewable fuel industry. The acquisition is part of Honeywell's strategy to improve its Energy and Sustainability business by diversifying its product portfolio in energy security solutions.

January 2025: Allegro MicroSystems introduced the ACS37030MY and ACS37220MZ current sensor ICs for accurate sensing in a compact, rugged package. They take 40% less space than 16-pin devices. Their use offers increased isolation and lower resistance to reduce power dissipation.

January 2025: Infineon Technologies AG launched the Sensor Units & Radio Frequency (SURF) business unit by combining its Sensor and RF operations. The move strengthens competitiveness. It also addresses the rising demand for sensors and RF solutions across automotive, consumer, and industrial markets. It is aligned with energy-efficient and electrification trends.

January 2025: Honeywell and NXP Semiconductors announced an expanded partnership. The partnership aims to accelerate the development of next-generation aviation technology. This collaboration focuses on integrating NXP's high-performance computing architecture into Honeywell's Anthem avionics. It will enable AI-driven aerospace technology to improve operational efficiency and safety.

February 2024: Asahi Kasei Microdevices (AKM) introduced the CZ39 series of coreless current sensors for electric vehicle applications. The sensors enable more compact and highly accurate on-board charging systems in EVs.

Current Sensor Market Segmentation

By Current Sensing Method Outlook (Revenue, USD Billion, 2021–2034)

- Direct Current Sensing

- In-Direct Current Sensing

By Loop Outlook (Revenue, USD Billion, 2021–2034)

- Open Loop

- Closed Loop

By Technology Outlook (Revenue, USD Billion, 2021–2034)

- Hall Effect

- Shunt

- Flux Gate

- Magneto-Resistive

By Output Outlook (Revenue, USD Billion, 2021–2034)

- Analog

- Digital

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Online

- Offline

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Motor Drive

- Converter Inverter

- Battery Management

- UPS & SMPS

- Starter & Generators

- Grid Infrastructure

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Current Sensor Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 2.72 billion |

|

Market Size in 2026 |

USD 2.99 billion |

|

Revenue Forecast by 2034 |

USD 6.49 billion |

|

CAGR |

10.2% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Current Sensor Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market for current sensors stood at USD 2.72 billion in 2025. The market is projected to reach USD 6.49 billion by 2034.

The market is projected to account for a CAGR of 10.2% between 2026 and 2034.

Asia Pacific accounted for the largest market share in 2025. This is due to rapid industrialization and growing adoption of EVs in the region.

A few of the key market players include Analog Devices, Inc.; Asahi Kasei Microdevices Corporation; CTS Corporation; Honeywell International Inc.; Infineon Technologies AG; KOHSHIN ELECTRIC CORPORATION; LEM International SA; Melexis; Microchip Technology Inc.; Omron Corporation; Schneider Electric; Sensitec GmbH; TDK Corporation; Texas Instruments Incorporated; and Vishay Intertechnology Inc.

A current sensor is an electronic device that detects and measures electric current in a circuit. The measured electric current is converted into a readable output signal, which can be analog or digital.

The direct sensing method accounts for the largest market share. This is due to the simplicity and accuracy of the method.

Page last updated on:

May-2025

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements