Data Center Cooling Market Forecast 2026-2034

REPORT DETAILS

Market Statistics

Data Center Cooling Market Overview

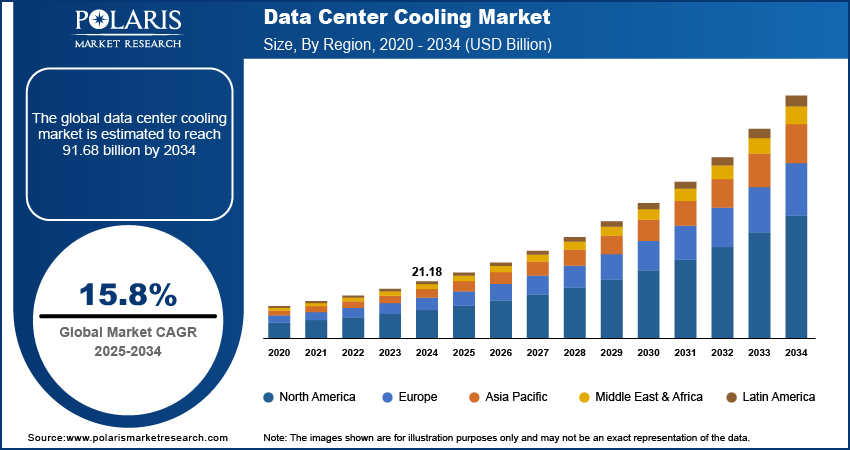

The global data center cooling market size was valued at USD 24.44 billion in 2025, growing at a CAGR of 15.8% during 2026–2034. Rapidly growing data traffic and cloud service expansion is driving the demand for the data center cooling.

Key Takeaways

- North America held the largest revenue share of 38.85% in 2025. The high degree of digitalization and advanced data infrastructure contribute to the region’s leading market position.

- Asia Pacific is forecasted to emerge as the fastest-growing regional market with a CAGR of 16.7%. The driving forces behind the rapid growth of this region include digitalization and stringent data localization regulations.

- Precision air conditioners have become the key product segment of the market with a 33.2% revenue share in 2025. This is attributed to their capability to maintain temperature and humidity at very precise levels.

- The small scale segment is predicted to record the highest CAGR of 16.4%. The increasing need for localized data processing and edge computing will fuel the growth of this segment.

- Air cooling emerged as the dominant cooling technique. It accounted for 58.9% of revenue share in 2025. This is due to the low initial investment required in installing these systems.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Market Statistics

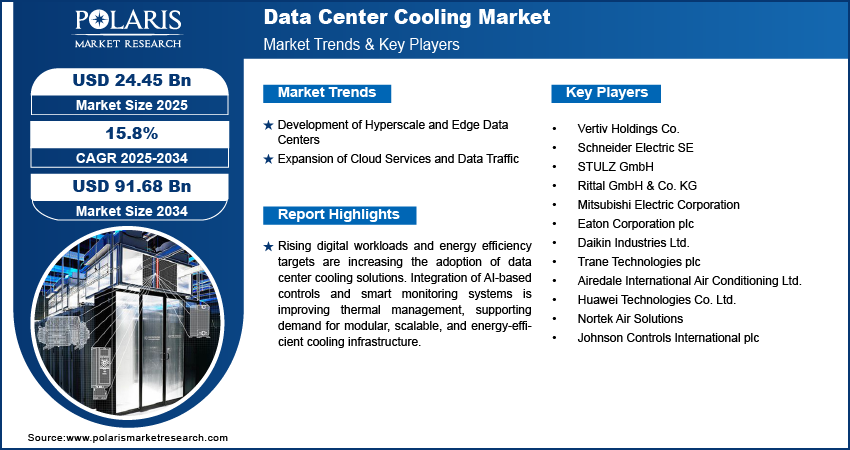

- 2025 Market Size: USD 24.44 Billion

- 2034 Projected Market Size: USD 91.50 Billion

- CAGR (2026–2034): 15.8%

- North America: Largest Market in 2025

Industry Dynamics

- The growing adoption of online services and cloud platforms is increasing the number of data centers across key regions.

- The development of hyperscale and edge data centers is another factor contributing to the rapid market expansion.

- The rising focus on the integration of IoT sensors and AI algorithms into data center infrastructure management (DCIM) tools is expected to create several market opportunities.

- High energy consumption and strict sustainability goals may present market challenges.

AI Impact on Data Center Cooling Market

- AI enables optimizing cooling by regulating temperatures and airflow based on live data from data centers.

- The technology reduces energy use by regulating cooling only where it's needed.

- AI boosts equipment performance through predictive maintenance by anticipating risks of overheating.

- AI also facilitates savings through efficient cooling practices.

Data center cooling systems help manage heat generated by servers and equipment, ensuring consistent performance and reducing energy waste. These systems include air-based and liquid-based technologies that support both traditional and modular infrastructure. The focus on reducing power usage effectiveness (PUE) and meeting energy efficiency standards is encouraging operators to adopt precision cooling solutions. Data centers across banking, telecommunications, and technology sectors are integrating energy-efficient cooling systems to support continuous operations. Compact system design, reduced water usage, and remote monitoring capabilities are helping operators improve cooling performance in both new and retrofitted facilities.

The adoption of data center cooling is also driven by regulations focused on environmental impact and sustainability. Efficient cooling helps lower electricity consumption, reduce carbon emissions, and extend equipment life. Developments in direct-to-chip liquid cooling, immersion cooling, and AI-based thermal management are expected to support long-term industry growth. These technologies are helping operators achieve better thermal control, reduce operational costs to meet global efficiency targets.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Rising demand for energy-efficient infrastructure and growing complexity in IT workloads are pushing the adoption of advanced data center cooling systems. For instance, in July 2024, researchers at the University of Missouri-Columbia are developing an advanced two-phase cooling system that uses phase change to dissipate heat efficiently, potentially reducing energy use in data centers amid growing Artificial Intelligence computing demands. Global data centers are upgrading their thermal management strategies to meet environmental regulations and performance requirements. Regulatory frameworks and corporate sustainability goals are driving operators to lower carbon emissions and reduce energy consumption. Efficient cooling techniques help to maintain ideal operating temperatures, reduce energy waste, and support high-density computing environments. These systems improve overall data center performance by enhancing airflow, lowering power usage, and ensuring equipment stability under heavy loads.

Urban and high-growth digital regions are seeing steady demand for next-generation cooling solutions due to rising investments in hyperscale facilities, edge data centers, and cloud computing infrastructure. Advanced cooling systems offer space efficiency, low water usage, and reduced maintenance needs that comply with evolving design and operational standards. Operators prefer these solutions for their reliability, adaptability, and long-term cost benefits. Public and private investments in green data centers and smart thermal management support the integration of these technologies. As data processing needs expand, advanced cooling systems are becoming essential for building sustainable and future-ready digital infrastructure.

Industry Dynamics

Expansion of Cloud Services and Data Traffic

Rising adoption of cloud platforms and online services is increasing the number of data centers across key regions. Businesses are expanding digital operations, which led to higher demand for continuous data processing and storage. Cloud-based software, e-commerce, video platforms, and enterprise applications are generating large data volumes that require stable and secure infrastructure. According to the Cybersecurity Ventures, global data storage is projected to surpass 200 zettabytes by 2025, this includes data across private and public IT systems, utility infrastructures, cloud data centers, personal devices such as PCs, laptops, tablets, and smartphones, as well as IoT devices. These conditions raise the need for efficient thermal control to prevent hardware stress and maintain system reliability in high-load environments.

Higher processing activity leads to greater heat output from computing equipment. Cooling systems are essential to maintain safe operating temperatures and reduce the risk of hardware failure. Consistent thermal management improves uptime, extends equipment life, and supports performance under constant workloads. Operators are investing in advanced cooling technologies that help maintain system stability while reducing energy use. As data usage continues to grow, thermal efficiency remains a priority in data center planning and operation.

Development of Hyperscale and Edge Data Centers

Deployment of hyperscale and edge data centers across key regions is increasing due to growing digital activity and demand for low-latency services. Hyperscale data center facilities are designed to manage large-scale computing and storage needs, while edge centers focus on delivering localized data processing closer to end-users. For instance, in February 2025, CtrlS Datacenters announced construction of a new hyperscale data center in Chennai with a planned capacity of 72 MW. The facility aims to support growing digital infrastructure needs with enhanced scalability and efficiency. These facilities require reliable thermal systems to maintain equipment stability and avoid performance disruption under varying operational conditions. Construction in diverse environments and rapid deployment timelines are encouraging the use of modular and adaptable cooling solutions.

Edge data centers often operate in space-limited locations, requiring compact cooling units that support energy efficiency. Hyperscale centers contain dense hardware that generates significant heat, making high-capacity cooling systems necessary for long-term reliability. Efficient thermal control supports continuous operations and reduces maintenance risks. Scalable and remote-managed systems are being integrated to handle increasing computing volumes while optimizing energy use. Expansion of digital infrastructure continues to drive demand for advanced cooling technologies that align with the operational needs of modern data centers.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

Product Analysis

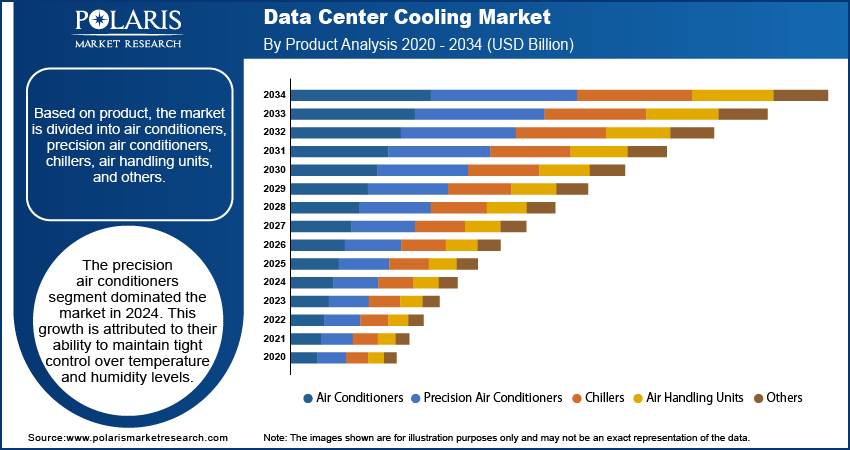

The global segmentation, based on product includes, air conditioners, precision air conditioners, chillers, air handling units, and others. The precision air conditioners segment dominated the market in 2025. This growth is attributed to their ability to maintain tight control over temperature and humidity levels. These systems are designed specifically for data center environments, where consistent cooling is necessary to avoid thermal disruptions. High demand from enterprise and hyperscale facilities supports the continued use of precision air conditioning units in both new and retrofitted setups. These units offer accurate environmental control and help avoid energy waste by adjusting to thermal loads. Their operational reliability makes them suitable for data centers requiring uninterrupted performance.

The chillers segment is projected to grow at a robust pace in the coming years, as data centers expand capacity and shift toward scalable cooling infrastructure. These systems provide centralized cooling and are increasingly used in large and modular setups for cost efficiency. Rising construction of high-density facilities is contributing to the accelerated adoption of water-cooled and air-cooled chiller units. As an example, in March 2024, Carrier launched the AquaForce 30XF chiller range, designed specifically to meet the cooling demands of modern data centers. The new series offers high efficiency, low environmental impact, and reliable performance. It helps to lower the overall temperature more effectively in large server rooms where traditional systems face limitations. Their ability to support long operating hours with steady output is encouraging wider deployment.

Size Analysis

The global segmentation, based on size includes, large scale, medium scale, and small scale. The large scale segment accounted for substantial market share in 2025, owing to extensive computing workloads and global cloud infrastructure development. These facilities operate on a 24/7 basis and require advanced thermal systems that can handle high-density server configurations. High investment from technology companies supports this segment’s continued leadership. These facilities often host mission-critical workloads, making precise thermal management essential for long-term operations. The need to meet service-level agreements further supports investment in robust cooling systems.

The small scale segment is projected to grow at a significant pace during the assessment phase, due to the rising demand for edge computing and localized data processing. These setups require compact, energy-efficient cooling systems that can be deployed quickly across urban and remote locations. Growth in smart city infrastructure and IoT applications is supporting this trend. These facilities help reduce network congestion and enhance data speed by operating closer to the user. The demand for decentralized infrastructure across regions is boosting small-scale installations.

Cooling Technique Analysis

The global segmentation, based on cooling technique includes, air cooling, liquid cooling, immersion cooling, evaporative cooling, and free cooling. The air cooling segment was valued at significant share in 2025, due to its low setup cost and ease of maintenance. It is commonly adopted in traditional data centers where moderate density levels are present. Use of raised floor systems and contained airflow solutions further supports efficient cooling across multiple racks. Operators favor air cooling due to its minimal structural changes and easy integration. Its cost-effectiveness continues to make it a popular choice for standard workloads.

The liquid cooling segment is estimated to hold a substantial market share in 2034, as operators look to manage heat in high-performance computing environments. This technique provides higher cooling efficiency and is suitable for dense workloads such as AI, machine learning, and graphics processing. Shift toward sustainable operations and reduced power usage is driving adoption. In October 2024, KAYTUS unveiled its all-liquid cooling solutions at DCWA 2024, designed to meet the high-performance demands of AI-driven data centers. The technology enhances energy efficiency and thermal management for next-gen computing environments. Liquid-based systems reduce energy consumption by transferring heat more effectively than air. These systems also support compact server designs by reducing the need for bulky airflow components.

| Cooling Technology | Description | Level of Efficiency | Main Features | Common Uses |

| Air Cooling | Cools computers through the use of fans, vents, and HVAC to circulate cold air and dissipate heat from servers | Moderate | Commonly used technology, affordable to install and manage | Mid-range data centers, company IT spaces |

| Liquid Cooling | Direct heat dissipation by immersing computer components or racks in liquid coolant | High | Has superior heat dissipation characteristics than air, allows higher density computing operations | Artificial intelligence applications, HPC systems, hyperscale centers |

| Immersion Cooling | Cools server hardware by submerging them completely into dielectric liquid coolant | Very High | Highest heat dissipation characteristics, consumes less power than other methods | Advanced AI data centers, hyperscale computing, research labs |

| Evaporative Cooling | Cools incoming air by making use of evaporating water before it enters a data center environment | Moderate to High | Consume less energy compared to mechanical air conditioning systems | Large scale data centers in appropriate climate |

| Free Cooling | Taking advantage of ambient air and water sources to lower temperatures | High | Economical in operation, consumes low energy compared to others | Cloud data centers, green data centers, northern countries |

Source: Polaris Market Research Analysis

Service Type Analysis

The global segmentation, based on service type includes, installation & deployment, support & consulting, and maintenance services. The installation and deployment segment is projected to grow during the forecast period, due to the growing number of data center construction projects. These services include equipment setup, integration, and testing to ensure proper thermal control across all operational zones. Demand for expert handling during infrastructure expansion supports this segment’s strength. Professional installation helps minimize errors and ensures systems run at peak efficiency. Rising adoption of advanced equipment requires specialized support during the setup phase.

The maintenance services segment is estimated to witness fastest growth during the forecast period, due to the need for regular system checks and performance optimization. Service providers offer cleaning, inspection, and repair solutions to prevent system downtime. Higher focus on equipment lifespan and thermal efficiency is supporting market growth across this segment. These services help identify early signs of system fatigue and avoid emergency shutdowns. Predictive maintenance tools are also being adopted to lower long-term operational risks.

End User Analysis

The global segmentation, based on end user includes, BFSI, IT and telecom, manufacturing, retail, healthcare, energy and utilities, and others. The IT and telecom segment growth is driven by the high dependency on data storage, cloud applications, and communication services. Large server farms and data hubs operated by technology firms require continuous cooling support to maintain service uptime and prevent operational risks. Thermal stability remains a key requirement in meeting strict uptime targets. Operators in this segment consistently invest in modern cooling to manage dynamic computing loads.

The healthcare segment is estimated to grow at a significant CAGR from 2026-2034, due to increasing reliance on digital health systems, telemedicine platforms, and patient data management. Rising installation of data centers across hospitals and diagnostic centers is creating demand for stable and efficient cooling solutions tailored to sensitive data environments. These centers must operate under strict temperature control to ensure data accuracy and compliance. Expansion of electronic medical records and AI-driven diagnostics is raising the need for reliable thermal systems.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

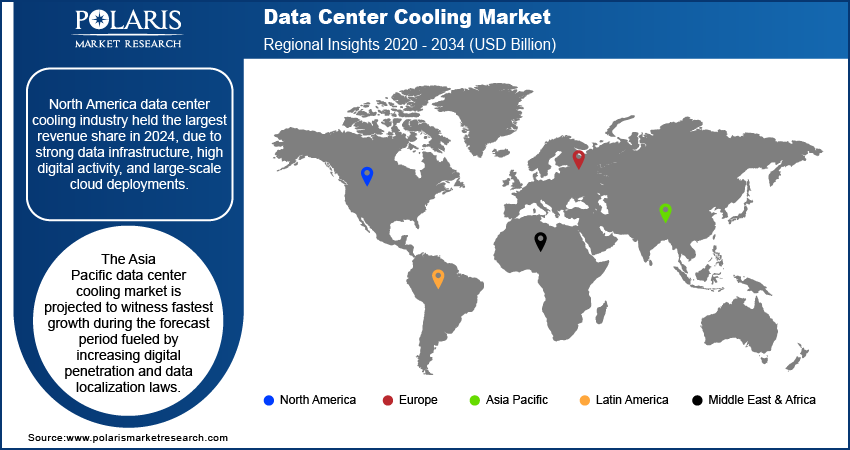

North America data center cooling industry held the largest revenue share in 2025, due to strong data infrastructure, high digital activity, and large-scale cloud deployments. The US remained the key contributor with continued expansion in hyperscale campuses and enterprise data hubs. States including Virginia, Texas, and California supported steady demand for scalable cooling systems. For instance, in January 2025, Major tech companies including OpenAI, SoftBank and Oracle announced to invest over USD 500 billion in global data center infrastructure by 2030 to meet rising AI and cloud computing demands. This surge reflects the growing need for high-performance, energy-efficient digital ecosystems. Federal energy programs promote use of efficient thermal solutions to manage power usage. AI workloads and 5G rollout are increasing cooling requirements across core and edge locations. A well-developed supply chain further supports adoption of precision and liquid-based systems.

US Data Center Cooling Market Insight

The US dominated the regional market in 2025. This dominance is attributed to the growing investment in hyperscale, colocation, and enterprise data centers. High energy costs and increasing server densities are pushing operators toward precision cooling and modular solutions. Digital infrastructure strategies are supporting deployment of sustainable systems, aligned with evolving building standards. Regional climate variations require site-specific cooling approaches. Data center growth across Chicago, Phoenix, and Virginia is supported by tax benefits, strong utility access, and available land. Collaborations between technology providers, utilities, and public agencies help streamline adoption of advanced systems while maintaining operational efficiency and environmental compliance.

Asia Pacific Data Center Cooling Market

The Asia Pacific data center cooling market is projected to witness fastest growth during the forecast period fueled by increasing digital penetration and data localization laws. China, India, Japan, and Singapore are expanding data center capacity to meet rising cloud usage and digital service demand. National programs support sustainable infrastructure with emphasis on efficient cooling. Singapore’s green data center framework and Japan’s energy reforms boost the use of liquid and evaporative cooling. Recently, in February 2025, the government of Singapore targets for data centers to achieve a water usage effectiveness of 2.0m3/MWh or less within the next 10 years. Thus, the demand for data center cooling is projected to increase steadily over the coming years. High-density urban centers drive demand for compact and energy-saving systems. Edge deployment for smart cities and industrial applications further supports regional expansion. Cooling solutions with lower power usage are preferred due to rising electricity costs.

Europe Data Center Cooling Market Overview

Europe data center cooling market accounted for significant revenue share in 2025, due to strong regulations and digital infrastructure development. Regional operators follow strict energy efficiency standards, promoting widespread use of advanced cooling systems. Countries including Germany, Netherlands, and Ireland host major data center clusters. For example, in February 2025, DreamHost launched its first international data center in Amsterdam, expanding its global footprint to better serve customers across Europe with enhanced performance and data sovereignty. Moreover, the EU’s Green Deal and new server eco-design rules promote deployment of liquid and free cooling solutions. Operators are modernizing existing sites to meet environmental targets. Cold regional climates support partial use of natural cooling. Availability of renewable energy and improved connectivity further enhances infrastructure resilience and cooling adoption.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The data center cooling industry is highly competition, due to increasing demand for thermal efficiency, regulatory compliance, and scalable infrastructure. Leading providers are offering modular, energy-efficient cooling systems that reduce power usage and support high-density environments. Market participants are focusing on product innovation, regional capacity expansion, and customized solutions suited for hyperscale and edge deployments. Partnerships with data center operators and technology integrators support service coverage and customer retention. Emphasis on reliability, real-time monitoring, and integration with facility management platforms contributes to strong positioning across global and regional markets.

Key companies in the industry include Vertiv Holdings Co., Schneider Electric SE, STULZ GmbH, Rittal GmbH & Co. KG, Mitsubishi Electric Corporation, Eaton Corporation plc, Daikin Industries Ltd., Trane Technologies plc, Airedale International Air Conditioning Ltd., Huawei Technologies Co. Ltd., Nortek Air Solutions, and Johnson Controls International plc.

Key Players

- Vertiv Holdings Co.

- Schneider Electric SE

- STULZ GmbH

- Rittal GmbH & Co. KG

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Daikin Industries Ltd.

- Trane Technologies plc

- Airedale International Air Conditioning Ltd.

- Huawei Technologies Co. Ltd.

- Nortek Air Solutions

- Johnson Controls International plc

Industry Developments

- April 2026: Johnson Controls showcased the new YORK absorption chillers at the Data Center World 2026. These chillers are created to reduce the chiller power consumption by 90 percent through the use of waste heat for cooling. Johnson Controls also highlighted the Silent-Aire CDU Platform, with capacities ranging from 500kW to 10MW. (source: johnsoncontrols.com)

- March 2026: Ecolab entered into a definitive agreement for the acquisition of CoolIT Systems. According to Ecolab, the acquisition will enhance its portfolio in advanced liquid cooling for AI-driven data centers. The acquisition is expected to close in the third quarter of 2026. (source: ecolab.com)

- June 2025: Shell introduced its latest Direct Liquid Cooling (DLC) fluid designed to enhance thermal management in high-performance data centers. The solution supports energy-efficient operations and aligns with sustainability goals for advanced digital infrastructure. (Source: shell.com)

- May 2025: Chemours and DataVolt partnered to advance liquid cooling technologies for AI-driven data centers. The collaboration aims to enhance energy efficiency and enable scalable, future-ready infrastructure. (Source: chemours.com)

- April 2025: LG launched a comprehensive end-to-end cooling solution tailored for high-capacity data centers, addressing rising thermal management demands. The system enhances efficiency and reliability across large-scale digital infrastructure. (Source: lg.com)

Future Outlook for Data Center Cooling Market

It is anticipated that the market for data center cooling will grow rapidly due to increased AI computing demand, higher server density, and the expansion of hyperscale and edge data centers. The use of liquid and immersion cooling methods will become more widespread as organizations emphasize energy savings and sustainability. The future cooling systems are expected to incorporate the use of artificial intelligence-based thermal management systems and green cooling systems

Data Center Cooling Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Air Conditioners

- Precision Air Conditioners

- Chillers

- Air Handling Units

- Others

By Size Outlook (Revenue, USD Billion, 2021–2034)

- Large Scale

- Medium Scale

- Small Scale

By Cooling Technique Outlook (Revenue, USD Billion, 2021–2034)

- Air cooling

- Liquid cooling

- Immersion cooling

- Evaporative cooling

- Free cooling

By Service Type Outlook (Revenue, USD Billion, 2021–2034)

- Installation & Deployment

- Support & Consulting

- Maintenance Services

By End User Type Outlook (Revenue, USD Billion, 2021–2034)

- BFSI

- IT and Telecom

- Manufacturing

- Retail

- Healthcare

- Energy and Utilities

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Data Center Cooling Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 24.44 Billion |

| Market Size in 2026 | USD 28.23 Billion |

| Revenue Forecast by 2034 | USD 91.50 Billion |

| CAGR | 15.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

data center cooling market FAQ's

The global data center cooling market was valued at USD 24.44 billion in 2025 and is projected to reach USD 91.50 billion by 2034, growing at a CAGR of 15.8%.

Precision air conditioners dominated in 2025 due to their ability to maintain tight temperature and humidity control, specifically designed for data center environments, offering accurate environmental control and preventing energy waste.

Liquid cooling is estimated to hold substantial share by 2034, suitable for high-performance computing environments like AI and machine learning, providing higher efficiency and supporting compact server designs effectively.

IT and telecom segment leads due to high dependency on data storage, cloud applications, communication services, large server farms, and continuous cooling support to maintain service uptime and prevent operational risks.

North America held the largest share in 2025 due to strong data infrastructure, high digital activity, large-scale cloud deployments, hyperscale campuses, enterprise hubs, and federal energy efficiency programs.

Maintenance services segment is estimated to witness fastest growth during forecast period, driven by need for regular system checks, performance optimization, cleaning, inspection, repair solutions preventing downtime, and predictive maintenance tools.

AI is transforming data center cooling through intelligent thermal management systems that monitor real-time temperature data, predict heat patterns, and automate cooling adjustments. AI-driven cooling reduces energy consumption, lowers power usage effectiveness (PUE), and improves overall operational efficiency, making it a key innovation driving the market forward.

Download Sample Report of data center cooling market

Please fill out the form to request a customized copy of the research report.