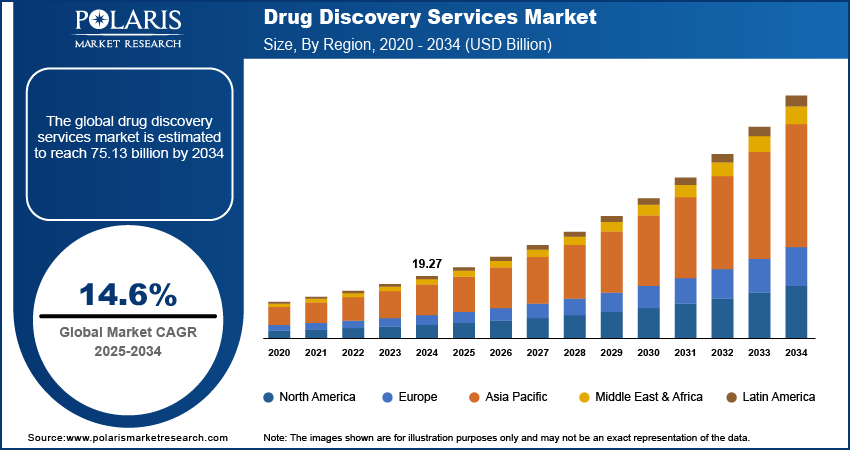

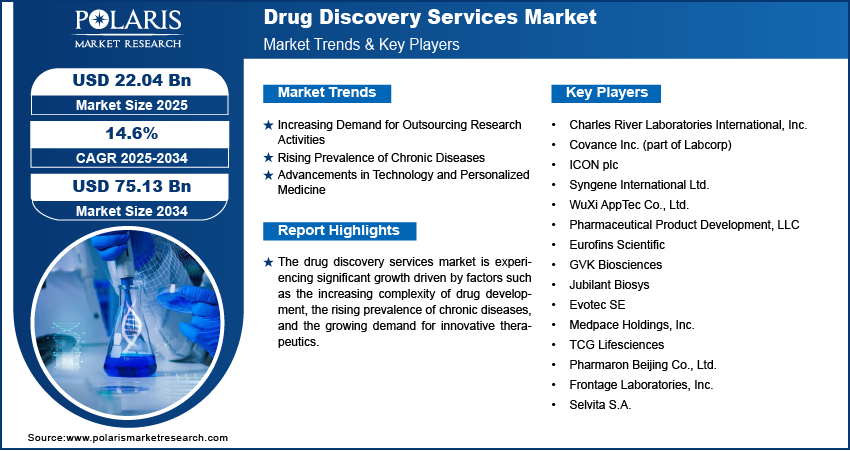

The drug discovery services market size was valued at USD 22.04 billion in 2025, growing at a CAGR of 14.6% during 2026–2034. Market growth is primarily driven by the increasing complexity of drug discovery processes and the growing demand for outsourcing research activities.

In this report, drug discovery services encompass research and development support conducted externally or within facilities and research institutions for early-stage discovery. Early-stage drug discovery services typically include target validation and selection, hit identification, hit-to-lead, lead optimization, and lead candidate validation. It excludes later-stage clinical trials or commercial manufacturing, unless they are directly linked to preclinical discovery support.

Key Insights

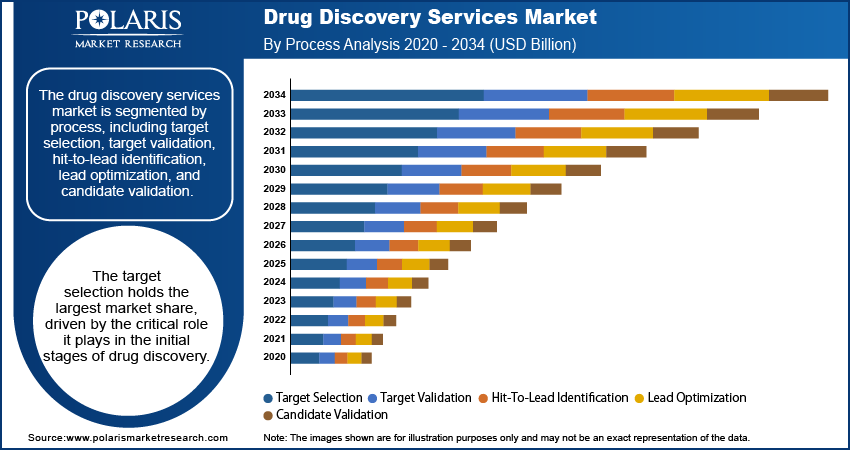

- The target selection segment leads the drug discovery services market share, owing to its crucial role in initial drug discovery stages.

- The biology services segment is registering the fastest growth. The segment’s growth is largely fueled by the shift towards more complex biological drugs.

- The pharmaceutical & biotechnology companies segment accounts for the largest market share. Increased investment in drug delivery for the development of new therapies drives the segment’s leading market position.

- North America dominates the market. The regional market dominance is attributed to the presence of key market participants and significant investments in R&D.

- Asia Pacific is witnessing rapid growth. This is due to the shift towards outsourcing research activities in the region.

- Oncology remains a prominent area of demand in the outsourced drug discovery market. Oncology drug discovery services are driven by active development pipelines and the emergence of novel targets in solid tumors and hematological malignancies.

- The service mix is shifting due to the growing prominence of biologics and more sophisticated treatments. This creates a growing need for biology-driven discovery work in addition to more standard chemistry-driven programs. This, in turn, supports the transition to biologics discovery service offerings and to more fully integrated discovery models.

Industry Dynamics

- The growing trend of outsourcing research activities across biotechnology and pharmaceutical companies is a key factor fueling the drug discovery services market growth.

- The rising prevalence of chronic conditions such as cardiovascular diseases and cancer is fueling the demand for drug discovery services.

- Increasing focus on emerging therapeutic areas like personalized medicine is expected to provide market growth opportunities.

- High costs of drug discovery may present market challenges.

- Apart from cutting costs, more companies have started outsourcing to access specialized platforms such as high-throughput screening, advanced cell models, and bioinformatics. Additionally, outsourcing helps companies accelerate discovery timelines and run multiple programs at the same time.

- The execution risks lie in dealing with data consistency issues as well as vendor issues. Managing IP rights as well as data could be a challenge. Thus, picking the right CRO as well as managing quality well are essential in the successful outsourcing of drug discovery.

Market Statistics

- 2025 Market Size: USD 22.04 billion

- 2034 Projected Market Size: USD 75.13 billion

- CAGR (2026-2034): 14.6%

- North America: Largest Market in 2025

AI Impact on Drug Discovery Services Market

- AI in drug discovery services supports target identification through the analysis of genomic, proteomic, and clinical data to identify new drug targets.

- Predictions of interactions between compounds and of toxicity are made using machine learning. Such predictions aid in eliminating a trial-and-error aspect in preclinical research.

- Artificial intelligence-based platforms enhance virtual screening and molecular design, significantly reducing development costs.

- Advanced analytics support personalized drug discovery methods, helping match therapies to patients' biometric markers to improve success rates.

- Increasingly, AI is being employed at different levels in drug discovery. This can include aiding target selection and validation by analyzing biological data, discovering leads through virtual screening, and enhancing leads with predictive methods and new-molecule design.

- However, to a certain extent, performance depends on the training dataset, the standardized assay, and the strength of the validation steps. Thus, companies that stand out in integrity, governance, and data reproducibility will have a stronger advantage in securing high-value research programs.

How to Choose a Drug Discovery Services Provider?

Organizations typically evaluate drug discovery CRO services on a variety of key parameters. These are:

- Specific therapeutic area and treatment type expertise

- Assay development and validation experience

- Strong integration of chemistry and biology for hit-to-lead and lead optimization

- Capacity and turnaround time of screening workflows

- Strong quality systems and data integrity standards

- Clear IP and data rights provisions within contract structures

A way to focus on vendor choice would be to align them with the appropriate stage of discovery. For example, early target validation may require strong biological expertise and disease models. In contrast, lead-optimization expertise relies on medicinal chemistry to design-make-test analyses and to predict compound biodistribution properties.

To mitigate execution risk, buyers should request sample deliverables. These include the hit triage report and questions regarding reproducibility and various forms of governance, such as science reviews, milestone-based releases, and clear change-control processes.

The drug discovery services market provides research and development support to pharmaceutical and biotechnology companies in the identification and development of new drugs. Key services include target identification, assay development, lead identification, and optimization, as well as preclinical studies.

The market is driven by factors such as increasing demand for outsourcing research activities, the rising prevalence of chronic diseases, and the growing complexity of drug discovery processes. Trends shaping the drug discovery services market include the adoption of artificial intelligence and machine learning for drug discovery, a focus on personalized medicine, and increased collaborations between pharmaceutical companies and contract research organizations (CROs).

Market Dynamics

Increasing Demand for Outsourcing Research Activities

One of the key drivers of the drug discovery services market is the increasing outsourcing trend among pharmaceutical and biotech industry players. The need to contain costs and to make the drug discovery process more efficient are the key reasons for this outsourcing activity. Outsourcing enables these industry players, pharma, or biotech companies, to tap the expertise of the contract research organization, thus increasing efficiency. According to a 2024 report by the Association of Clinical Research Organizations, outsourcing can accelerate drug development by 30%, making it a preferable choice for companies seeking accelerated research.

Rising Prevalence of Chronic Diseases

The growing need for treating chronic illnesses like cancer, diabetes, and cardiac conditions is the other major factor propelling the market for drug discovery services. The global toll of chronic illnesses is on the rise, leading to increased calls for new pharmaceuticals. According to the World Health Organization, chronic illnesses contributed to about 71% of all global mortality in 2021, marking the need for innovative pharmaceutical solutions. The demand for new pharmaceuticals drives the market, with pharmaceutical manufacturers aiming to meet new medical requirements through innovative pharmaceutical solutions.

Advancements in Technology and Personalized Medicine

Technological innovations, especially in fields like AI, machine learning, and genomics, are bringing a paradigm shift to the drug discovery and development industry. These innovations make it possible to be more accurate and time as well as cost-efficient when it comes to finding possible candidates for developing medications with a much shorter timeline compared to existing methods of drug discovery and development. Further, with a rise in personalized medicine approaches for developing drugs according to individual genetic expression, there is a substantial requirement for specialized drug discovery services. A 2023 study published in Nature Reviews Drug Discovery revealed that AI-assisted drug discovery services can cut costs by as much as 20%. This highlights the transformative impact of these technological innovations on the market.

Segment Insights

Assessment by Process

The market for drug discovery services is divided on the basis of process into target selection, target validation, hit-to-lead identification, lead optimization, and candidate validation. The target selection process has the largest market share, mainly because of its importance in the early stages of drug discovery. This process includes identifying and validating biological targets with the highest likelihood of being medically significant. This is very important for the later stages of drug development. The increasing adoption of bioinformatics and computational biology to improve the accuracy and efficiency of target selection is further driving the dominance of target selection services. Common outputs at this point include ranked lists of priority targets, documents outlining why each target was selected, and early validation packages that facilitate the program's progression from hit identification.

The lead optimization segment is also experiencing the fastest growth rate in the market. This segment is focused on the optimization of lead compounds to make them more effective, safe, and pharmacokinetics before moving on to clinical trials. The rising interest in developing high-quality lead compounds and in improving screening and structure-based drug design is contributing to the segment’s growth. The requirement for more targeted and effective drug candidates is driving the interest in this process, making it a significant growth area in the market. The lead optimization services are increasingly supported by predictive ADME/Tox modeling, design-make-test cycles, and DMPK support. The acquisition of lead optimization services is sometimes carried out through drug discovery outsourcing services.

Evaluation by Type

The market for drug discovery services is divided by type into chemistry services and biology services. The chemistry services market currently holds the largest share in drug discovery, mainly because of the pivotal role chemistry services play in the process. Chemistry drug discovery services include medicinal, synthetic, and analytical chemistry, which are necessary for the synthesis and optimization of drug candidates. The demand for chemistry services is also driven by the need for high-throughput screening and the development of new chemical entities, both of which are important in the early stages of drug discovery. For many programs, drug discovery CRO services integrate chemistry with design and screening to accelerate hit identification and the hit-to-lead phase.

Biology services register the highest growth rate in the drug discovery services market. This segment includes services such as target identification, cell-based assays, and preclinical testing. These services are being increasingly recognized as biologics and personalized medicines advance. The shift towards more complex biological entities, including monoclonal antibodies and gene therapies, is driving growth in biological services. The integration of advanced technologies such as CRISPR and next-generation sequencing is further supporting this segment.

Outlook by End User

The drug discovery services market segmentation, based on end user, includes pharmaceutical & biotechnology companies, academic institutes, and others. Pharmaceutical & biotechnology firms have the largest market share due to their high investment in drug discovery to develop new drugs and maintain a competitive edge. Pharmaceutical & biotechnology firms are increasingly outsourcing to improve research productivity and reduce the time-to-market for new drugs. The complexity of the drug development process and the rising costs of in-house research and development also contribute to this segment's market share.

Academic institutes are also growing at the fastest rate in the drug discovery services market. This is due to the growing emphasis on collaborative research and the rise in public-private partnerships. These institutes are a crucial part of early-stage drug development. They often rely on grants and funding from government and private institutions to support their research. The emphasis on translational research and the growing use of advanced technologies in academic institutions are major drivers of this segment's growth. The role of academic research in developing innovative therapies is also on the rise. All of this supports the growth of this end-user segment.

Assessment by Drug Type

By drug type, the demand is being split increasingly between small molecule and biologics drug discovery services, including monoclonal antibodies and more advanced approaches. Small molecule drug discovery services remain dependent on strong medicinal chemistry and high-throughput approaches, whereas biologics-driven discovery is increasingly based on biology-centric platforms, advanced cell models, and validation by disease mechanism.

Assessment by Therapeutic Area

By therapeutic area, demand is driven by oncology drug discovery services, due to strong pipelines and high unmet medical needs. On the other hand, cardiovascular-metabolic, CNS, infectious disease, and rare disease conditions are increasingly supported by specialized outsourcing models. CROs are likely to differentiate themselves by providing disease-related assays, translational models, and biomarker strategies that better align with the objectives of a sponsor study.

Regional Insights

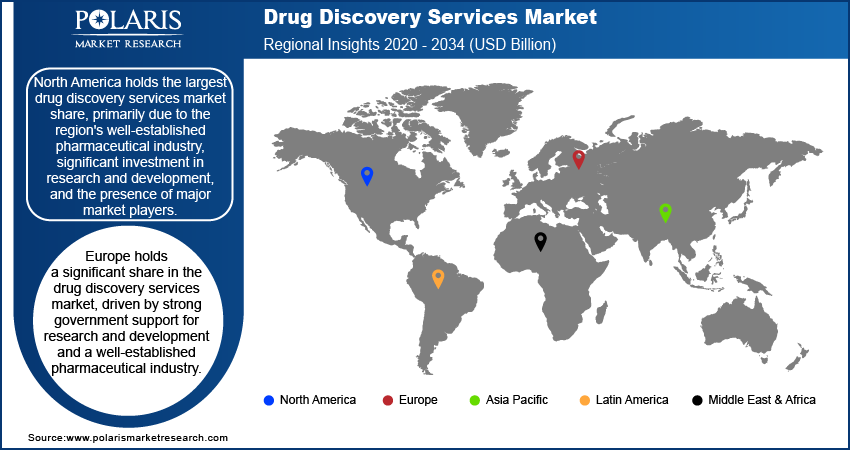

By region, the study provides drug discovery services market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America drug discovery services market currently has the largest market share, mainly due to the well-established pharmaceutical industry in this region, along with substantial investments in research and development, and the presence of major market players. The US currently leads the market due to its well-developed infrastructure for drug discovery, substantial government support, and access to advanced technologies. In addition, the rising incidence of chronic diseases and the need for innovative drugs are driving market growth in this region. A strong concentration of biotech companies, venture capital investments in new pipelines, and the early adoption of AI-enabled discovery platforms by drug discovery service providers enhance the region’s market position.

Europe is a significant market for drug discovery services. This is due to strong government support for R&D and a well-established pharmaceutical industry. Countries like Germany, the UK, and France are significant in this market. They have substantial investment in drug discovery and innovation. The region offers a favorable research environment. Many public-private partnerships and academic institutions are engaged in developing drug discovery services. In addition, the increasing prevalence of chronic diseases and the aging population are driving demand for innovative drugs, thereby contributing to market growth in the European region. The collaborative environment in Europe, founded on public-private partnerships and a collaborative relationship between academia and industry, is supportive of early discovery outsourcing. This is especially true for specialized biology services and translational research models.

The Asia Pacific market for drug discovery services is growing rapidly due to increasing investments in healthcare infrastructure and the rising trend of outsourcing research to countries such as China and India. The low costs, a qualified workforce, and the growing pharmaceutical industry in the Asia Pacific region are major factors contributing to the market's growth. Governments across the Asia Pacific region are also making significant investments in research and development to enhance the region's drug discovery capabilities. The role of India is growing in chemistry services, data analytics, and integrated discovery support, while the China ecosystem is facilitating large-scale biological research and platform expansion. The combined strengths of these ecosystems are thus helping to accelerate CRO competitiveness in the region.

Key Players and Competitive Insights

The competitive environment in the drug discovery services market is dominated by several major players with extensive experience and global presence. These players compete based on their service offerings, technological expertise, and ability to deliver cost-effective solutions. They have also formed long-term relationships with major pharmaceutical players. This allows them to gain business and utilize their expertise in different therapeutic areas.

Analysis of the market indicates a trend of consolidation and acquisition. Large drug discovery service providers are expanding their services and reach by acquiring smaller companies with niche expertise. Companies are also increasingly using new technologies, such as artificial intelligence and machine learning, to improve their drug discovery capabilities. In addition, they are investing in the latest research and development to differentiate themselves and have a larger share of the growing market.

Key players in the drug discovery services market include companies such as Charles River Laboratories International, Inc.; Covance Inc. (now part of Labcorp); ICON plc; Syngene International Ltd.; WuXi AppTec Co., Ltd.; Pharmaceutical Product Development, LLC (PPD, now part of Thermo Fisher Scientific); Eurofins Scientific; GVK Biosciences; Jubilant Biosys, Evotec SE; Medpace Holdings, Inc.; TCG Lifesciences; Pharmaron Beijing Co., Ltd.; Frontage Laboratories, Inc.; and Selvita S.A. These companies provide a range of drug discovery services, including target identification, lead optimization, and preclinical development. They serve pharmaceutical and biotechnology firms worldwide.

Charles River Laboratories International, Inc. is a prominent player in the drug discovery services market. The company provides a comprehensive range of services to support early-stage drug research and development, including target identification, lead optimization, and preclinical testing.

Covance Inc., now part of Labcorp, is another key player offering extensive drug discovery and development services. Covance provides integrated solutions, including preclinical and clinical research, to pharmaceutical and biotechnology companies.

Differentiation on the competitive frontier is increasingly driven by four key areas: high-end-to-end integration between biology and chemistry, expertise in a particular modality, such as biologics or small molecules, the application of AI-enabled discovery workflows, and quality and reproducibility systems that reduce execution risk.

Vendors are typically categorized into three groups. These are large integrated CROs that provide end-to-end discovery-to-development services, boutique firms that specialize in specific areas of biology or chemistry, and AI-native discovery companies that partner with wet lab vendors to deliver hybrid discovery programs.

List of Key Companies

- Charles River Laboratories International, Inc.

- Covance Inc. (part of Labcorp)

- ICON plc

- Syngene International Ltd.

- WuXi AppTec Co., Ltd.

- Pharmaceutical Product Development, LLC (PPD, part of Thermo Fisher Scientific)

- Eurofins Scientific

- GVK Biosciences

- Jubilant Biosys

- Evotec SE

- Medpace Holdings, Inc.

- TCG Lifesciences

- Pharmaron Beijing Co., Ltd.

- Frontage Laboratories, Inc.

- Selvita S.A.

Drug Discovery Services Market Sizing Methodology

The Polaris market estimates have been built by use of a triangulation approach that combines discovery services revenues, service lines, assumptions regarding outsourcing by sponsor type, and industry validation by factors such as pipeline data, R&D spend, and growth of CRO capacity. All of these assumptions have been stress-tested to align with past trends (2021-2024) and the drivers for 2026-2034.

Drug Discovery Services Industry Developments

November 2024: Charles River Laboratories announced the expansion of its gene therapy capabilities through the acquisition of a new facility. The company revealed that the expansion will enhance its capacity to support clients in the growing field.

September 2024: Covance expanded its digital and decentralized clinical trial capabilities to streamline drug development processes and improve patient engagement. The move reflects its commitment to using technology to improve service delivery.

Drug Discovery Services Market Segmentation

By Process Outlook (Revenue, USD Billion, 2021–2034)

- Target Selection

- Target Validation

- Hit-To-Lead Identification

- Lead Optimization

- Candidate Validation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Chemistry Services

- Biology Services

By Drug Type Outlook (Revenue, USD Billion, 2021–2034)

- Small Molecules

- Biologics

By Therapeutic Area Outlook (Revenue, USD Billion, 2021–2034)

- Oncology

- Infectious Diseases

- Cardiovascular Diseases

- Neurological Diseases

- Immunological Diseases

- Digestive & Gastrointestinal Diseases

- Genitourinary & Women’s Health

- Respiratory Diseases

- Endocrine & Metabolic Diseases

- Other Therapeutic Areas

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Pharmaceutical & Biotechnology Companies

- Academic Institutes

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Drug Discovery Services Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 22.04 billion |

|

Market Size in 2026 |

USD 25.21 billion |

|

Revenue Forecast by 2034 |

USD 75.13 billion |

|

CAGR |

14.6% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Drug Discovery Services Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the Report Valuable for an Organization?

Workflow/Innovation Strategy: The drug discovery services market has been segmented into detailed segments of process, type, and end user. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy: The expansion and marketing plan in the drug discovery services market includes developing their services, advancing their technology, and establishing partnerships with other companies. Companies are investing in effective technologies such as AI and machine learning to improve the efficiency of their drug discovery services. Partnerships with pharmaceutical and biotechnology companies, as well as the acquisition of specialized companies, help expand their market. Also, their emphasis on emerging disciplines such as gene and personalized medicine provides them with opportunities for expansion. They are also paying attention to customer-centric strategies and adapting to the needs and requirements of customers at different development phases.

FAQ's

The drug delivery services market stood at USD 75.13 billion in 2034. It is projected to account for a CAGR of 14.6% between 2026 and 2034.

Drug discovery services include target identification and validation, hit-to-lead identification, lead optimization, candidate validation, chemistry services, biology services, assay development, and preclinical testing.

The major users of this technology are pharmaceutical and biotech companies. They are followed by research institutes and contract research organizations (CROs) working on new drug development.

AI speeds up target identification, models compound interactions and toxicity, optimizes virtual screening and molecular design, shortens development time, and enables personalized medicine strategies much more effectively.

North America leads the market. This is due to the region's established pharmaceutical infrastructure, significant R&D investments, and the presence of major industry players.

Drug discovery services refers to the range of research and development services provided to pharmaceutical, biotechnology, and life sciences companies to assist in the process of discovering new drug candidates. These services support various stages of drug development, including target identification, lead discovery, hit-to-lead optimization, preclinical testing, and candidate validation. Drug discovery services aim to identify potential therapeutic compounds, assess their effectiveness, and optimize their properties before moving into clinical trials. Companies offering these services use advanced technologies, specialized expertise, and scientific methodologies to help accelerate the drug discovery process, reduce costs, and improve the likelihood of developing successful drugs

A few key trends in the market are described below: Adoption of AI and Machine Learning: Increased use of artificial intelligence (AI) and machine learning for data analysis, drug design, and predicting drug efficacy, reducing time and cost in drug discovery. Outsourcing of Research Activities: Pharmaceutical and biotech companies are increasingly outsourcing drug discovery services to contract research organizations (CROs) to lower costs and access specialized expertise. Growth of Personalized Medicine: The rise of personalized medicine is driving demand for more targeted drug discovery services based on individual genetic profiles. Technological Advancements: Integration of cutting-edge technologies such as CRISPR gene editing, next-generation sequencing, and 3D printing in drug discovery.

A new company entering the drug discovery services market could focus on leveraging advanced technologies such as artificial intelligence (AI) and machine learning to optimize drug discovery processes, reducing time and cost for clients. Specializing in emerging therapeutic areas, such as gene therapy, personalized medicine, and biologics, could also differentiate the company, as these fields are experiencing rapid growth. Additionally, offering tailored services and building strong partnerships with pharmaceutical and biotechnology companies, academic institutions, and contract research organizations (CROs) could help establish credibility and foster long-term relationships. Focusing on efficient, data-driven solutions and staying at the forefront of technological advancements will enable the company to compete effectively.

Page last updated on:

Nov-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements