Market Overview

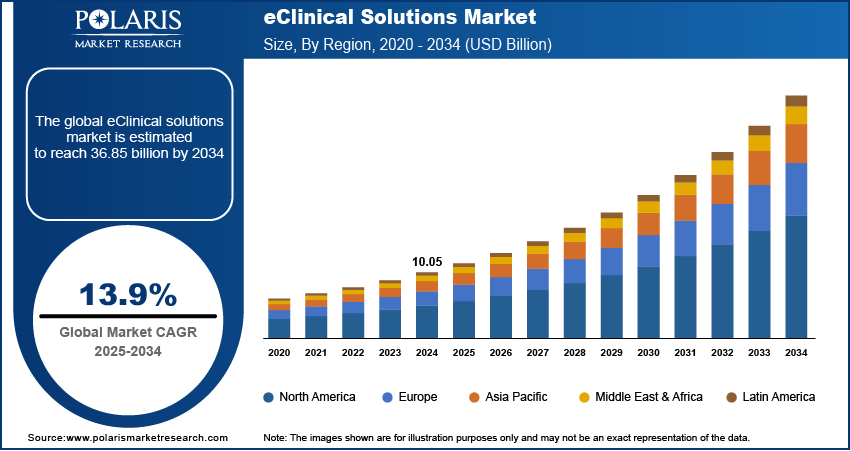

The global eClinical solutions market size was valued at USD 11.41 billion in 2025. According to our eClinical solutions market forecast, it is projected to account for a CAGR of 13.9% between 2026 and 2034. The rising adoption of digital technologies, increased complexity of clinical trials, and the need for efficient data management and regulatory compliance are driving the market forward.

Key Insights

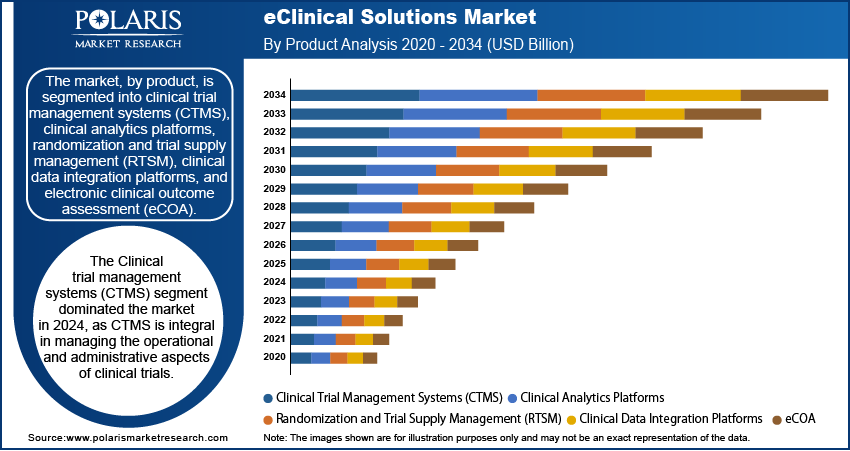

- The clinical trial management systems (CTMS) segment led the market with a 25.84% revenue share in 2025. This is because CTMS is integral in managing the operational and administrative aspects of clinical trials.

- The pharma & biotech organizations segment is anticipated to experience significant growth during the forecast period. Substantial investments in drug development and approvals are driving robust growth of the segment.

- The North America eClinical solutions market held the largest market share of 49.80% in 2025. Advanced healthcare infrastructure and significant R&D investments contribute to the region’s leading market share.

- The Asia Pacific eClinical solutions market is projected to witness the fastest growth during the forecast period. Large patient population and an increase in clinical research activities contribute to the region’s robust growth.

- Sponsors and CROs increasingly prefer to work on platforms that combine trial operations, patient engagement, data visibility, and compliance, rather than individual tools.

- Advanced technologies and AI-powered clinical trial software are now being used for day-to-day activities like patient matching, protocol design support, and data review.

Industry Dynamics

- The use of electronic data capture systems, clinical trial management systems, and electronic clinical outcome assessment instruments is expected to increase data accuracy and improve trial efficiency, thereby driving market growth.

- The increasing complexity of clinical trials is also driving demand for data management solutions.

- The market is expected to grow as pharmaceutical companies and contract research organizations seek to increase efficiency and reduce the costs of trials.

- Data security and privacy issues may limit the eClinical solutions market growth.

Market Statistics

- 2025 Market Size: USD 11.41 billion

- 2034 Projected Market Size: USD 36.77 billion

- CAGR (2026-2034): 13.9%

- North America: Largest market in 2025

AI Impact on eClinical Solutions Market

- AI assists in speeding up clinical trials by enhancing the matching of patients and reducing waiting time in the recruitment process.

- It facilitates faster and more accurate data review to help identify problems at an early stage to prevent costly mistakes.

- AI also aids in enhanced decision-making by offering clearer insights based on large quantities of data collected in clinical trials.

- It helps in reducing workload by automating processes to enable more time to be devoted to trial quality and patient experience.

The eClinical solutions market includes software platforms and associated services used to manage clinical trials digitally. These eClinical platforms support clinical trial management, including planning, coordination, patient data collection, randomization, supply chain management, outcome measurement, analysis, and documentation throughout the clinical development lifecycle.

Some of the emerging trends in the market include the incorporation of artificial intelligence and machine learning in data analysis, the increased use of decentralized clinical trial software, and the increased use of virtual trials and cloud-based eClinical solutions. The market is also expected to grow as more pharmaceutical companies and contract research organizations seek to increase efficiency and reduce the costs of trials.

To Understand More About this Research:Request a Free Sample Report

Market Dynamics

Adoption of Digital Technologies in Clinical Research

The integration of electronic data capture (EDC) technologies, clinical trial management systems (CTMS), and electronic clinical outcome assessment (eCOA) tools improves the accuracy and efficiency of the research process. For instance, the integration of cloud computing technologies enables researchers and clinicians to access their data anywhere. Moreover, the technologies have enhanced security features to ensure that the research process complies with current regulations. This reduces the risk of data breaches. The current eClinical technologies can be used to support different functions such as tracking the study protocol, remote monitoring, patient engagement, data collection, and analysis. They can be integrated with other technologies such as imaging, ePRO, and site technologies. Therefore, the integration of digital technologies into the clinical research process is driving the growth of the eClinical solutions market.

Growing Complexity of Clinical Trials

The complexity of clinical trials has driven the need for advanced data management solutions, thereby necessitating eClinical tools. Currently, a lot of data is being generated from various sources, including genomics, images, and wearable devices. The complexity of clinical trials is further increased by regulatory requirements, which necessitate the use of comprehensive clinical solutions. Fragmented systems may cause delays in database lock, data reconciliation bottlenecks, and decreased visibility between the sponsor, CRO, and site. This has created the need for integrated eClinical solutions that help minimize manual processes and improve audit readiness.

Rising Emphasis on Regulatory Compliance and Data Security

Stringent clinical trial regulations are encouraging buyers to look beyond data security and focus on the compliance features of eClinical systems. Regulations like 21 CFR Part 11 have been a driving force behind the implementation of clinical software. Clinical sponsors and CROs have been increasingly adopting clinical software with enhanced functionality. The functionality includes access controls, change history, validated workflow, data traceability, data storage, and audit trails. They help maintain the integrity of electronic records and signatures. They also ensure data reliability throughout the clinical trial process. In addition to this, the updated FDA guidance emphasizes data security and decentralized clinical trials, creating a need for compliance-focused eClinical solutions.

Decentralized and Hybrid Trial Adoption

The shift towards decentralized and hybrid clinical trials is becoming a long-term trend. Sponsors are utilizing remote visits, telehealth, and home-based procedures to improve patient access and reduce patient burden. With regulators' support, patient-centric models are making a growing case for patient engagement technologies, such as eCOA, remote data capture, and eConsent in clinical trials. At the same time, a growing volume of data is being generated from a wide range of sources. There is a growing need for effective oversight and control, driving demand for technologies that maintain accurate, well-managed data. As a result, sponsors are selecting eClinical solutions that can manage distributed workflows and integrate data effectively.

Integration, Standardization, and Data Silos

Companies are using multiple eClinical tools. This is the reason integration is becoming a challenge. Disconnected systems can result in data silos in clinical trials, inconsistent data, as well as duplication of efforts. They can also result in slower data processing, which can reduce the overall visibility of the trial operation. These interoperability challenges can limit the benefits of the digital systems, especially when the systems do not integrate well or when they are poorly managed. Thus, there is greater emphasis on standard data formats, integration, and the use of unified platforms to reduce manual effort and promote integrated trial operations.

Segment Insights

By Product Insights

The eClinical solutions market, by product, is segmented into clinical trial management systems (CTMS), clinical analytics platforms, randomization and trial supply management (RTSM), clinical data integration platforms, and electronic clinical outcome assessment (eCOA). The clinical trial management systems (CTMS) segment led the market with a 25.84% revenue share in 2025. CTMS plays an integral role in the administration and management of the operational aspects of the clinical trials process, which includes financial and project management. The widespread use of CTMS by research sites, sponsors, and contract research organizations (CROs) underscores its importance in streamlining clinical trial processes.

The electronic clinical outcome assessment (eCOA) segment is expected to experience the fastest growth between 2026 and 2034, driven by the growing importance of high-quality clinical data. eCOA solutions enhance the quality of the data collection process by evaluating the outcomes provided by clinicians, patients, and observers. The effectiveness of eCOA solutions in streamlining the data collection process is what makes them important in clinical research.

Trials are becoming more spread out and data-heavy. This has created a need among sponsors for trial dashboards, alerts, risk signals, and real-time data review tools to help teams spot issues early and make better decisions. This is driving increased demand for clinical analytical platforms. The importance of RTSM software solutions is particularly relevant in clinical studies where randomization, supply, and patient allocation are critical. At the same time, clinical data integration platforms are becoming more important to sponsors who are seeking a unified trial data view from systems like EDC, CTMS, safety, and outcome systems.

By Delivery Mode Insights

The eClinical solutions market, by delivery mode, is segmented into cloud & web-based and on-premise. The cloud & web-based segment led the market in 2025. The importance lies in various benefits, such as ease of access, usability, and low investment requirements. In addition, web and cloud-based eClinical solutions provide service providers with better interoperability and customization capabilities to meet user group information presentation needs. Cloud solutions support collaboration across sponsors, CROs, sites, and external partners. They improve rollout flexibility and better align with decentralized and multi-regional trial software. These benefits have led to the popularity of clinical research among various stakeholders.

The on-premise delivery mode, although having a smaller market share, is considered a preferred option by organizations that place a high value on data security. This is because services and solutions installed on servers within the organization's internal network ensure complete access to information and complete control within the organization's premises. Although the on-premise clinical trials software requires installation within the organization's internal network, the services and solutions installed can also be accessed remotely. This delivery mode is beneficial to organizations in terms of cost savings resulting from power consumption and maintenance costs. It is favored by entities that manage sensitive data and need stringent security measures.

At the same time, hybrid deployment is becoming a promising solution. The hybrid deployment allows organizations to retain control over key systems while taking advantage of the flexibility offered by cloud-based systems. The shift is gaining popularity because it has the potential to address compliance, performance, and efficiency issues in a changing clinical-trials environment.

By Clinical Trial Insights

The clinical trial phase segmentation covers Phase I, Phase II, Phase III, and Phase IV. The role of the trial phase is critical to eClinical solution selection and application. Phase I clinical trials emphasize speed, close monitoring, and early safety tracking. As such, they require basic data-collection capabilities and fast, efficient decision-making tools. Phase II and Phase III studies have more patients and often multiple study sites. As a result, they require effective site management, patient management, and result tracking. On the other hand, Phase IV trial platforms and post-marketing studies are more focused on collecting real-world data. As such, they require tools that are effective for long-term patient management. The various phases of clinical trials have shown the need for flexible platforms that are effective for different study needs.

By End Use Insights

The eClinical solutions market, by end use, is segmented into hospitals/healthcare providers, contract research organizations (CROs), academic institutes, pharma & biotech organizations, and others. The contract research organizations (CROs) segment dominated the market in 2025. This dominance is attributed to the increasing collaboration between biopharmaceutical companies and CROs, as firms seek to reduce overall expenditures and enhance research efficiency. CROs require platforms that are able to operate across different sponsors, protocols, regions, and site networks. As a result, they prefer platforms that are scalable, flexible, and easy to integrate. The outsourcing of clinical trials to CROs offers benefits such as specialized expertise and streamlined processes. This further drives the adoption of CRO eClinical solutions.

The pharma & biotech organizations segment is expected to witness substantial growth during the forecast period. The growth of the segment is attributed to substantial investments in drug development and approvals, as well as the number of clinical trials conducted across the globe. The need to efficiently manage clinical trial data and adhere to regulatory norms is also boosting the adoption of eClinical solutions in these organizations.

Though the major users of eClinical solutions are pharmaceutical companies, biotech firms, and CROs, there has been an increasing trend of usage from medical device companies, academic bodies, and government research bodies. They use eClinical solutions in various studies, which include device, investigator-initiated, and public health studies. This has led to an increase in the demand for eClinical solutions, thus contributing to the growth of the industry.

Regional Analysis

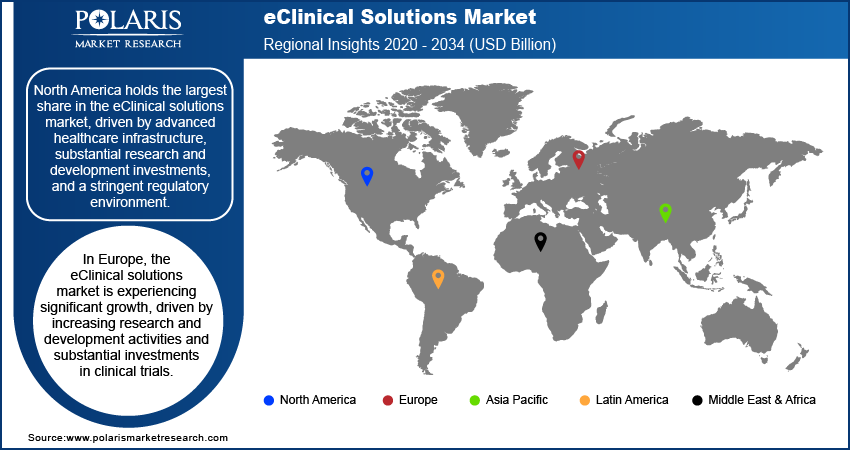

By region, the study provides eClinical Solutions market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America eClinical solutions market led the market with a 49.80% revenue share in 2025. It is driven by advanced healthcare infrastructure, substantial research and development investments, and a stringent regulatory environment. The leadership in this region is also aligned with strict regulations, such as FDA 21 CFR Part 11, as well as decentralized clinical trials guidance. This indicates not only increased spending but also a focus on digital compliance. The presence of major pharmaceutical companies conducting extensive clinical trials further fuels the regional market dominance.

The Europe eClinical solutions market is experiencing continuous growth. The region has robust biopharma research, high-quality healthcare, and increasing investment in digital operations in clinical trials. In addition, Europe is taking a more structured approach to decentralized trials, with the European Medicines Agency (EMA) focusing on patient safety, quality, and coordination in trials. This is encouraging the use of eClinical solutions to enable compliant, patient-centric trials with consistent quality and oversight in different regulatory environments.

The Asia Pacific eClinical solutions market is anticipated to exhibit the fastest growth during the projection period. The regional market is driven by a large patient population and increased clinical research activity. The market is also fueled by the rapid adoption of advanced technologies in countries like Japan, South Korea, and Australia.

Latin America is slowly growing as a viable region for conducting clinical research. An increase in the number of clinical trials is being carried out in countries like Brazil and Mexico because of the diverse population. An increase in the number of clinical trials is also being witnessed due to an improving regulatory environment. This is resulting in more interest in eClinical solutions to support multi-site clinical trials.

The Middle East & Africa eClinical solutions market is also gaining traction because of the improving healthcare infrastructure and digitalization. Governments are increasingly investing in clinical research. This offers an opportunity for eClinical solutions to support data management and monitoring of clinical trials.

Key Players and Competitive Insights

The eClinical solutions market has several major players that are contributing to the development of clinical trial technologies. The eClinical solutions market is influenced by key strategy trends that affect both the vendors’ positions and the customers’ choices. For instance, there is a focus on unified clinical platform solutions, with Medidata, Veeva Systems, and Oracle being some of the companies that provide integrated platforms to eliminate gaps between systems.

In addition, there is a growing need for AI-enabled eClinical platform capabilities, with companies such as IQVIA improving trials through design, recruitment, and analysis. Furthermore, there is a focus on decentralized trials and patient engagement through companies such as Signant Health and Clario. Interoperability remains a key priority, with companies such as eClinical Solutions and Anju Software improving data integration and standardization. Additionally, there is a focus on acquisition strategies, with companies such as Signant Health acquiring CRF Health and Clario acquiring ERT Clinical. Overall, customers are looking for vendors that align with these trends.

Medidata Solutions, which is a subsidiary of Dassault Systèmes, offers cloud-based software to the clinical trial industry. Its software covers data capture, clinical studies, and analytics. This platform caters to different aspects of clinical research. It improves data quality and makes operations efficient.

Veeva Systems specializes in offering cloud-based services to the life science sector. Its services include clinical data management, regulatory affairs, and quality control. They aim to streamline processes and ensure compliance with industry standards.

|

Company |

Enterprise Breadth |

Endpoint Expertise |

Analytics Depth |

DCT Support |

AI Capabilities |

Best Fit |

|

Medidata (Dassault Systèmes) |

High |

Medium |

High |

High |

Medium–High |

Large sponsors |

|

Veeva Systems |

High |

Low–Medium |

Medium |

Medium |

Medium |

Sponsors (end-to-end) |

|

Oracle |

High |

Medium |

High |

Medium |

High |

Large enterprises |

|

IQVIA Inc. |

High |

Medium |

High |

High |

High |

Sponsors & CROs |

|

ICON plc |

Medium |

Low |

Medium |

Medium |

Low–Medium |

CRO-led delivery |

|

PAREXEL International |

Medium |

Low |

Medium |

Medium |

Low–Medium |

CRO-led delivery |

|

Signant Health |

Medium |

High |

Medium |

High |

Medium |

Patient-focused trials |

|

Clario (incl. ERT Clinical) |

Medium |

High |

Medium |

High |

Medium |

Endpoint-heavy studies |

|

eClinical Solutions LLC |

Medium |

Low |

High |

Medium |

Medium |

Data/analytics focus |

|

Anju Software |

Medium |

Low |

Medium |

Medium |

Low–Medium |

Mid-size orgs |

|

ArisGlobal LLC |

Medium |

Low |

Medium |

Low–Medium |

Medium |

Safety/regulatory focus |

|

DATATRAK International |

Low–Medium |

Low |

Low–Medium |

Low |

Low |

Small–mid trials |

|

Medrio, Inc. |

Low–Medium |

Low |

Low–Medium |

Medium |

Low |

Mid-market sponsors |

|

CRF Health (Signant) |

Low |

High |

Low–Medium |

High |

Low |

eCOA specialization |

|

ERT Clinical (Clario) |

Low |

High |

Low–Medium |

High |

Low |

Endpoint specialization |

List of Key Companies

- Anju Software

- ArisGlobal LLC

- Clario

- CRF Health (now part of Signant Health)

- DATATRAK International, Inc.

- eClinical Solutions LLC

- ERT Clinical (now part of Clario)

- ICON plc

- IQVIA Inc.

- Medidata Solutions (a subsidiary of Dassault Systèmes)

- Medrio, Inc.

- Oracle Corporation

- PAREXEL International Corporation

- Signant Health

- Veeva Systems

Industry Developments

In February 2025, Medidata showcased new study experience capabilities for sites and sponsors at the SCOPE 2025 conference. These advancements were intended to reduce study design and execution timelines.

In January 2025, Medidata (A Dassault Systèmes Company) (France) launched Clinical Data Studio, an AI-powered software platform designed to modernize clinical trial data management.

Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Clinical Trial Management Systems (CTMS)

- Clinical Analytics Platforms

- Randomization and Trial Supply Management (RTSM)

- Clinical Data Integration Platforms

- Electronic Clinical Outcome Assessment (eCOA)

By Delivery Mode Outlook (Revenue, USD Billion, 2021–2034)

- Cloud & Web-Based

- On-Premise

- Hybrid

By Clinical Trial Outlook (Revenue, USD Billion, 2021–2034)

- Phase I

- Phase II

- Phase III

- Phase IV

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals/Healthcare Providers

- Contract Research Organizations (CROs)

- Academic Institutes

- Pharma & Biotech Organizations

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

eClinical Solutions Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 11.41 billion |

|

Market Size in 2026 |

USD 12.97 billion |

|

Revenue Forecast by 2034 |

USD 36.77 billion |

|

CAGR |

13.9% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

eClinical Solutions Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market for eClinical solutions stood at USD 11.41 billion in 2025. The market is projected to reach USD 36.77 billion by 2034.

The market is projected to account for a CAGR of 13.9% between 2026 and 2034.

North America led the market in 2025. This is due to its advanced healthcare infrastructure and substantial research and development investments.

A few of the key players in the market include Anju Software; ArisGlobal LLC; Clario; CRF Health (now part of Signant Health); DATATRAK International, Inc.; eClinical Solutions LLC; ERT Clinical (now part of Clario); ICON plc; IQVIA Inc.; Medidata Solutions (a subsidiary of Dassault Systèmes); Medrio, Inc.; Oracle Corporation; PAREXEL International Corporation; Signant Health; and Veeva Systems.

The clinical trial management systems (CTMS) segment accounted for the largest market share in 2025. CTMS plays an integral role in the administration and management of the operational aspects of the clinical trials process.

The pharma & biotech organizations segment is expected to witness substantial growth during the forecast period. The growth of the segment is attributed to substantial investments in drug development and approvals.

eClinical solutions are software and technology platforms used to streamline and manage various aspects of clinical trials. These solutions encompass tools for data collection, clinical trial management, analytics, regulatory compliance, patient monitoring, and outcome assessments.

A few of the key market trends include the adoption of cloud-based solutions and the increasing integration of artificial intelligence and machine learning. Adoption of Cloud-Based Solutions: Growing shift towards cloud-based platforms for better scalability, data accessibility, and cost efficiency. Decentralized Clinical Trials: Increase in the adoption of decentralized trials, driven by the need for more flexible and patient-centric approaches. Artificial Intelligence (AI) and Machine Learning (ML) Integration: Use of AI and ML for optimizing trial design, patient recruitment, data analysis, and predictive modeling. Patient-Centric Solutions: Development of solutions that focus on improving patient engagement, real-time monitoring, and data collection.

eClinical solutions improve trial efficiency by reducing manual workflows and improving coordination across stakeholders. They also enhance compliance readiness across global studies.

Clinical trials rely on trustworthy electronic records, traceable electronic workflows, and securely handled data. FDA Part 11 remains a major reference point for electronic records and signatures.

This report is valuable to pharma and biotech companies, CROs, investors, healthcare IT strategy teams, and vendors looking at market expansion.

AI supports patient matching and trial design support. It also enables workflow prioritization and faster data analysis.

Page last updated on:

Apr-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements