Reports

Electric Submersible Pump for Oil & Gas Market Growth Report 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

Overview

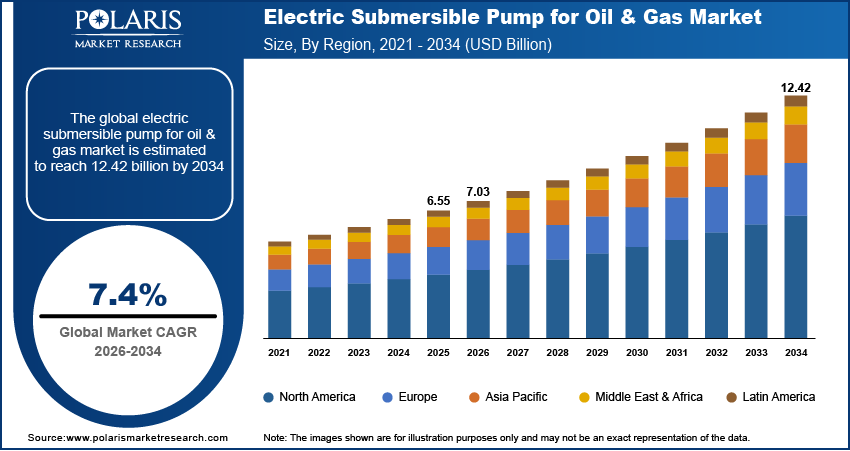

The global electric submersible pump for oil & gas market is estimated around USD 6.55 billion in 2025, with consistent growth anticipated during 2026–2034. This is driven by expanding ESP use in mature oilfields and deepwater projects supports stable and efficient production. The market is projected to grow at a CAGR of 7.4% during the forecast period.

Industry Dynamics

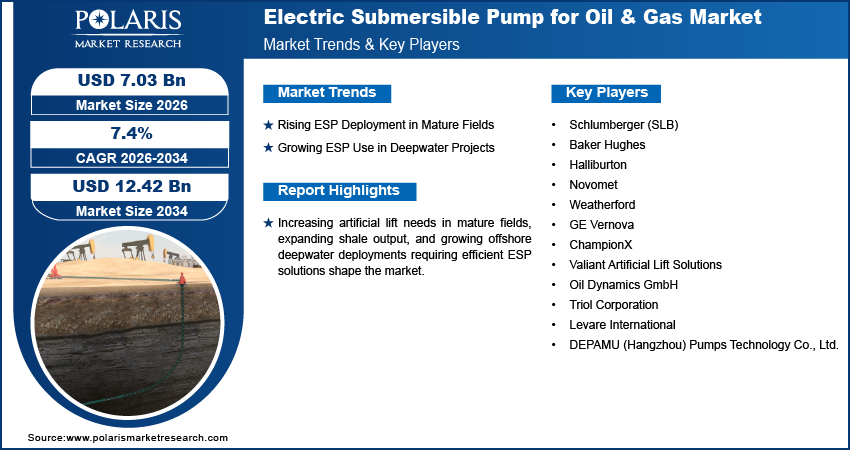

- Rising ESP deployment in mature fields supports stable long-term production.

- Growing deepwater adoption strengthens efficiency across offshore portfolios.

- Harsh downhole conditions create reliability and run life challenges.

- Shale growth and Middle East redevelopment create strong opportunities for advanced ESP upgrades.

Market Statistics

- 2025 Market Size: USD 6.55 billion

- 2034 Projected Market Size: USD 12.42 billion

- CAGR (2026-2034): 7.4%

- North America: Largest market in 2025

What is an ESP and Why It Matters for Oil & Gas

An electric submersible pump (ESP) is a high-capacity artificial lift system used to increase production from oil and gas wells with declining reservoir pressure. In many producing fields, natural reservoir energy falls over time, which reduces flow rates and affects overall asset productivity. ESPs help sustain production by pushing large volumes of fluid to the surface, making them essential in mature onshore and offshore fields where natural lift no longer supports commercial output.

Across the oil and gas sector, ESPs hold strategic importance as they address the core challenge of maximizing recovery from aging assets. Operators use ESPs in brownfield redevelopment programs, waterflooding operations, and extended-reach wells where traditional lift solutions do not deliver required efficiency. Adoption continues to rise in offshore environments as ESPs handle higher water cut, deeper installations, and variable operating conditions compared with conventional pumping systems.

The technology also plays an important role in the development of shale and tight oil. Horizontal wells in unconventional basins often see early peak output followed by rapid decline. In such wells, ESPs stabilize production through high lift performance, support a longer production plateau, and improve recovery factors. In consideration of this perspective, operators are optimizing artificial lift selections to meet economic targets across volatile price cycles, thereby driving additional momentum into the electric submersible pump for oil & gas market.

In addition, digital monitoring and variable speed drives strengthen the reliability of modern ESP systems. The crucial improvements contribute to better failure rates and improved run life, while supporting predictive maintenance strategies, in line with the operational priorities of major producers.

Strategic Importance for Mid to Senior Level Stakeholders

- ESPs allow for steady production from mature and unconventional wells with better long-term production visibility.

- Lower lifting costs and longer run life strengthen asset efficiency across big field portfolios.

- High horsepower ESPs in deepwater projects support faster production ramp up and higher recovery.

- Advanced monitoring and variable speed drives improve performance enhancement with the reduction of operational risk.

- Upgrades in technology correspond to digital field priorities and enhance the overall continuity of production.

Drivers & Opportunities

Rising ESP Deployment Across Mature Oilfields Driving Long-Term Production Stability: The growing dependence on artificial lift systems in most declining reservoirs continues to strengthen the demand drivers for ESPs across major producing regions. Increasingly, the mature fields around the Middle East, China, and South America are all turning to high-capacity ESPs in order to try to dampen the effects of falling reservoir pressure and increasing water cuts. In this regard, SLB announced two new artificial lift systems last April 2024, providing enhanced reliability, expanded operating range, and reduced power use that enabled operators to increase well performance while reducing operating costs. Efforts like this underscore the strategic role of ESPs in offering a stabilizing force to output from maturing assets, enhancing recovery efficiency, and facilitating field redevelopment strategies aimed at extending operational life.

Accelerating Use of ESPs in Deepwater and Ultra-Deepwater Projects Enhancing Production Efficiency: Growth in offshore investments is continuously increasing the offshore ESP adoption for deepwater wells where gas lift systems have limited applicability due to poorer reservoir conditions. According to Rystad Energy, offshore activity is growing at a rapid clip, with global spending led by key projects in the Middle East-set to increase from USD 33 billion in 2023 to USD 41 billion in 2025. Advanced subsea ESP installations across the Gulf of Mexico and offshore Brazil have marked the shift toward artificial lift technologies that deliver reliable performance under high-temperature and high-pressure conditions. These lifting systems have operational advantages in wells with limited availability of gas injection. Therefore, they are preferred for difficult subsea conditions. Strong adoption in the offshore portfolios reflects the growing operator confidence in high-efficiency lifting solutions that improve flow assurance and support long-term continuity of production.

Restraints & Challenges

Operational Challenges Related to ESP Reliability in Harsh Downhole Environments: Application in the marketplace has been strong; however, operators continue to experience notable ESP reliability issues due to abrasive solids, corrosive fluids, and elevated downhole temperatures. Wells in unconventional shale formations and high-water-cut reservoirs frequently encounter sand-related wear, motor overheating, and reduced run life. These ESP deployment challenges raise intervention frequency and increase operational costs mainly at remote offshore and deep drilling locations. Operators are investing in enhanced metallurgy, improved cooling systems, and advanced gas-handling technology to address these barriers and strengthen long-term system performance.

Opportunity

Expanding Opportunities from Shale Development, Middle East Redevelopment, and Brownfield Optimization: Growing shale development continues to accelerate unconventional wells ESP use-especially in basins such as the Permian, Montney, Vaca Muerta, and Sichuan. Horizontal wells in these areas are dependent on ESPs to stabilize output following steep early decline rates. Simultaneously, Middle Eastern producers are moving ahead with brownfield redevelopment efforts focused on reservoir improvement and high-volume lift optimization. Throughout 2024, a number of regional projects involved large-scale ESP upgrades to mitigate rising water cut and achieve stable production. All these trends continue to provide strong long-term opportunities for ESP vendors and service providers, as global operators look to prioritize production efficiency and field life extension across both conventional and unconventional portfolios. For example, Saudi Aramco's Q3 2025 update confirmed that the Jafurah Phase 1 development remains on track for completion by the end of this year with the early wells demonstrating good commercial flow rates as it targets 2.0 billion scf/d in 2030 with its 80% gas output increase.

Segmental Insights

This report offers detailed coverage of the electric submersible pump for oil and gas market by type and application to help readers identify the fastest expanding and most attractive demand segments.

By Type

-

Horizontal ESP Systems

The horizontal ESP segment accounted for the largest market share in 2025, mainly due to its crucial role in making production from long horizontal laterals stable in shale and tight reservoirs. Its capability of sustaining uniform drawdown and handling gas interference hence positions it strongly in the unconventional basins where early decline rates remain steep and lift requirements are high.

-

Vertical ESP Systems

The vertical ESP segment grew at the highest CAGR due to its wide prevalence in mature conventional fields that have high-volume artificial lift requirements. Compatibility with deep vertical wells and rising water cut conditions reinforces its dominance across global redevelopment programs.

-

Multistage Electric Submersible Pumps

The medium-stage multistage ESP segment is growing due to its optimum performance for conventional onshore wells with moderate lift capacity requirements. Its balance of cost, scalability, and operational reliability keeps it the most widely deployed configuration.

Key Components & Functions

In modern ESP systems, performance, reliability, and suitability for different reservoir settings are determined by several integrated components.

ESP Motor: The motor is the foundation of the system and drives the pump assembly. The ESP motor market continues to advance through the use of high-temperature insulation, improved cooling pathways, and corrosion-resistant alloys. Motors must withstand elevated downhole temperatures, pressure variations, and fluid-induced stress.

ESP Power Cables: ESP power cables transmit surface power to the motor across long vertical depths. Durability of cables, especially under high-temperature corrosive and mechanically strained conditions are very important. Cable failure is one of the main sources of downtime; hence, adequate insulation and armoring are of vital importance for long-term performance.

Seal/Protector Section: The seal section serves to equalize the pressure between the wellbore fluids and the internal motor oil without contaminating it. It protects the motor from gas ingress and fluid intrusion, enhancing system run life.

Pump Stages: The pump module contains multiple impeller-diffuser pairs that lift fluids to the surface. Stage configuration varies depending on fluid viscosity, sand concentration, and water cut. High-stage designs support deeper wells and variable reservoir conditions.

Control Panel & Variable Speed Drive (VSD): The surface control system regulates motor speed, startup sequences, and power supply. VSDs optimize pump performance under changing reservoir conditions and reduce electrical load variations.

Downhole Sensors: These sensors monitor temperature, pressure, vibration, and motor load. They enable performance optimization and the early detection of operational anomalies for better longevity.

Digital Innovation

Smarter monitoring systems and automation-driven workflows are reshaping the operations of ESP.

Real-Time Monitoring & Remote Connectivity: In modern times, ESP installations have integrated remote monitoring of ESP performance. Operators see in real time the status of the pump health, vibration patterns, fluid levels, and pressure changes. These capabilities reduce the frequency of intervention and improve overall system reliability, especially for offshore and remote assets.

Smart ESP Systems & IoT Integration: Smart ESP systems offer situational awareness round the clock using IoT-enabled sensors with cloud-based communication. They detect abnormal conditions, such as gas slugging, voltage fluctuations, or overheating, enabling timely operational adjustments.

Predictive Maintenance & AI-Driven Automation: Artificial intelligence enables pattern recognition, anomaly detection, and production optimization. AI automation in oil wells enables the early detection of failure symptoms on gas lock, scale buildup, or pump degradation. Predictive models proactively lead to maintenance planning and improve run life at such wells, with minimum unplanned shutdowns. The described capabilities provide special value to deepwater and unconventional wells as intervention costs are very high in those wells.

Operational Constraints Analysis

| Parameter | Typical ESP Systems | HPHT / Deepwater ESP Systems | Operational Notes |

| Depth Rating | 2,000 to 8,000 ft | Up to 12,000+ ft | Higher stage count required for deeper wells; cable strength influences maximum deployable depth. |

| Temperature Range | Up to 120°C | 150–200°C | Elevated temperatures impact motor insulation, lubricant stability, and seal system performance. |

| Pressure Environment | Up to 8,000 psi | 10,000–15,000 psi | Deepwater reservoirs require reinforced metallurgy and high-pressure protector systems. |

| Fluid Conditions | Moderate sand, medium water cut | High sand load, high water cut, corrosive fluids | Gas handlers, abrasion-resistant stages, and corrosion-resistant alloys extend run life. |

| Well Deviation | Vertical and mild deviations | Highly deviated and horizontal laterals | Horizontal wells require optimized intake design and improved gas handling. |

The report evaluates each ESP sub-segment by market size, share, growth rate, and indicative performance differentials across operating environments.

By Application

-

Onshore

The onshore ESP segment held the largest share of the market in 2025, due to its reliability in the reservoir, the fluid composition, and stresses in the downhole environment. Onshore ESP systems operate in wells where intervention access is easier and the production variability is more predictable. These environments support faster cycles of installation and reduced maintenance costs, especially for more mature onshore oil fields that are going through upgrades for artificial lift.

-

Offshore

The onshore shale ESP segment is expected to witness the fastest growth during the forecast period. This is due to its operation under considerably harsher conditions: higher pressures, deeper pump settings, and elevated temperatures. The complication heightens in subsea wells where workover vessels or rig-assisted intervention becomes necessary for retrieval operations. However, most operators persist with high-pressure deepwater ESPs for their capability to keep flow rates stable and make an impact on water-cut escalation in deep reservoirs.

Conventional vs Unconventional Wells

In conventional reservoirs, the inflow performance is generally predictable; therefore, ESP installation is usually not too complicated. Wells with natural pressure decline or increasing water cut normally see an immediate positive effect on recovery rates after their conversion to artificial lift for oil fields. ESP replacements in mature wells of Middle Eastern carbonate reservoirs have resulted in average production increases from 500 to 1,200 barrels per day, depending on fluid properties and the number of stages.

Unconventional formations introduce different challenges. ESP for shale wells is used to stabilize output after the sharp decline following initial peak production. Horizontal wells regularly present gas interference and variable fluid properties in the Permian Basin, which demands advanced gas-handling pump stages. Nevertheless, ESPs remain the preference of shale operators for mid-life production enhancement. A case in point, presented by a US shale operator in 2023, showed that production increased from 120 barrels a day to close to 300 barrels a day after ESP deployment and extended the economic life of the horizontal well by several months.

Another major segment of deployment are found in heavy oil reservoirs. High-viscosity fluids require special intake designs, abrasion-resistant pump stages, and enhanced motor cooling systems. ESP for heavy oil production in Canada and South America demonstrates consistent performance gains when deployed in combination with thermal stimulation or chemical treatment programs.

Market Use-Cases

Case 1: ESP Optimization in the Permian Basin

One such Permian Basin operator was experiencing chronic ESP failures in a gassy, unconventional well. The pump cannot handle the high gas content and unstable inflow, and resulting shutdowns were driving workover costs upward. To solve this, a redesigned ESP system featuring an extended-life motor, enhanced gas-handling technology, and a sand control intake was installed by the operator. The new system was set deeper in the well to improve drawdown and create more stable operating conditions.

After installation, the results were clear. The ESP run life increased from about 105 days to around 550 days. Well uptime improved from roughly 85% to 96%. This upgrade provided better cumulative production with fewer shutdowns. Remote monitoring for ESP contributed to the operator's early detection of unusual behavior and prevention of unexpected failures.

This real-world example effectively illustrates how advances in today's ESP design, together with superior monitoring tools, enable better performance in demanding shale wells. It highlights the value of tailored artificial lift solutions in wells that experience high gas, solids, or changing reservoir behavior.

Case 2: Offshore Deepwater ESP in High-Gas Environment (Brazil)

The 2025 technical publication indicated that a multistage electric submersible pump system was deployed in a deepwater Brazilian field, which featured high gas content and fluctuating downhole pressures. It mentioned that an ESP specially designed for high gas fraction, enhanced fluid separation, and strong boosting performance in deepwater operations was developed.

This revised pump configuration allowed for continuous and stable production in the previously mentioned environments where conventional gas-lift systems normally face performance constraints. The installation of ESPs had demonstrated reliable lifts despite high gas-liquid mixing and increased reservoir pressure, with no frequent shutdowns due to gas interference.

These next-generation ESP designs, therefore, support high-volume lift capacity, improved fluid handling systems efficiency, and extended operational run life in deepwater reservoirs. These systems help to contribute to better asset productivity and long-term field management in offshore wells exposed to harsh production conditions.

Regional Analysis

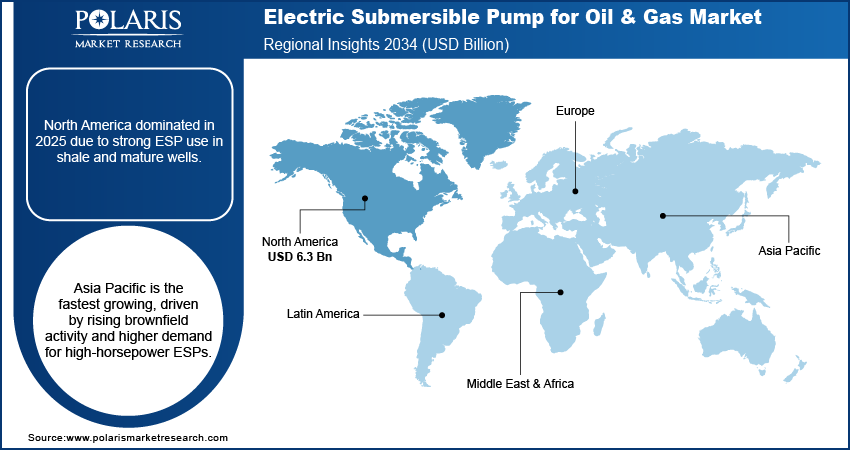

North America Market Assessment

The North America dominated the market in 2025, due to accelerating ESP installation in shale basins where steep early decline rates require stable artificial lift. Shale producers prioritize high-efficiency ESP systems to maximize drawdown. Moreover, digital ESP integration expands rapidly across the Permian and Eagle Ford. In addition, operators focus on maximizing well uptime with predictive automation tools.

Asia Pacific Electric Submersible Pump for Oil & Gas Market Insights

Asia Pacific is anticipated to witness the highest growth. This is owing to increasing ESP deployment across China and Southeast Asia where brownfield redevelopment drives lift requirements. Regional fields face rising water cut and pressure decline. Moreover, high-viscosity and deep onshore assets demand reliable high-horsepower ESP units. In addition, national oil companies invest in long-life artificial lift programs.

Middle East Electric Submersible Pump for Oil & Gas Market Overview

The Middle East growth in the electric submersible pump for oil & gas market is attributed to its strong adoption across mature high-volume fields positions the Middle East as the leading regional market. The increasing redevelopment activity in the across countries, including Saudi Arabia, the UAE, and Oman, bolsters continuous ESP deployment amid rising water cut. Besides, offshore expansion programs consolidate the long-term outlook for high-capacity lift systems.

Heat Map Analysis

| Region | Demand Intensity | Production Strength | Industrial Consumption | Regulatory Influence | Growth Momentum |

| North America | High | High | High | Medium | Very High |

| Asia Pacific | High | Medium–High | High | Medium | High |

| Middle East | Very High | Very High | Medium–High | Medium | High |

Key Players & Competitive Analysis Report

The global electric submersible pump for oil and gas market is moderately consolidated, with major oilfield service companies dominating system supply, installation, and lifecycle management. Competition is driven to innovate in high-efficiency ESP systems, digital monitoring tools, and integrated artificial lift portfolios for extended run life and production stability. Motor, cable, pump stage, and seal system controls are the focus of players to ensure reliable operations in mature fields, shale wells, and offshore reservoirs.

Major companies operating in the ESP for oil & gas industry include Schlumberger (SLB), Baker Hughes, Halliburton, Novomet, Weatherford, GE Vernova, ChampionX, Valiant Artificial Lift Solutions, Oil Dynamics GmbH, Triol Corporation, Levare International, Novomet, DEPAMU (Hangzhou) Pumps Technology Co.,Ltd., and others.

Key Players

- Schlumberger (SLB)

- Baker Hughes

- Halliburton

- Novomet

- Weatherford

- GE Vernova

- ChampionX

- Valiant Artificial Lift Solutions

- Oil Dynamics GmbH

- Triol Corporation

- Levare International

- DEPAMU (Hangzhou) Pumps Technology Co., Ltd.

Market Share Analysis

The market share landscape shows strong positioning for SLB and Baker Hughes, supported by high performance standards and consistent technology investments. Novomet strengthens its position through competitive cost structures and strong reliability in challenging wells. Halliburton and Weatherford maintain medium shares driven by balanced performance and steady innovation.

| Company | Market Share Position | Performance | Cost Competitiveness | Innovation Strength |

| SLB | High | High | Medium | High |

| Baker Hughes | High | High | Medium | Medium |

| Halliburton | Medium | Medium | Medium | Medium |

| Weatherford | Medium | Medium | Medium | Medium |

| Novomet | Medium | High | High | Medium |

Industry Developments

- July 2025: Sawafi Levare opened a new ESP manufacturing and service center at SPARK aimed at expanding the local production capacity in supporting more than 1,000 wells and reinforcing Saudi Vision 2030 goals.

- September 2024: Halliburton has introduced a new TrueSync hybrid PMM motor for ESP operations to enhance production performance, increase power efficiency, and reduce overall operating cost.

- April 2024: SLB introduced two new artificial lift systems that increase operating range, improve reliability, and decrease power consumption and emissions.

- March 2024: INTECH was awarded a project for the Middle East to automate more than 10 ESP power-supply skids with SIL-3 safety controls to improve reliability and ensure lower operation costs.

Cost Analysis & ROI

A detailed capital and operating cost comparison explains why ESPs remain a commercially viable means of artificial lift for wells of medium to high productivity. Although the upfront expenditure is higher than conventional rod pumping systems, ESPs deliver a lower cost per lifted barrel when deployed in wells with strong flow potential, water-rich conditions, or deeper production zones.

Capital & Operating Cost Breakdown

| Cost Category | Typical share of total |

| ESP hardware & downhole system | 45–55% |

| Installation + well intervention | 20–25% |

| Power consumption | 15–20% |

| Monitoring & maintenance | 10–15% |

Although these proportions vary by well depth, fluid composition, and system size, operators constantly look at ESPs as a higher-CAPEX solution compared to rod lift. However, faster production acceleration, higher drawdown efficiency, and fewer interventions support stronger long-term economics.

ESP vs Gas Lift: Economic Considerations

A comparison with gas lift indicates clear differences concerning production performance and cost behavior. ESPs deliver higher production volumes, especially in deeper or deviated wells where gas lift efficiency declines. In water-rich environments, ESPs maintain lower OPEX, whereas gas lift incurs additional compression and fuel gas costs. Energy efficiency is generally better in high-pressure, high-temperature settings as ESPs convert electrical power to hydraulic lift with greater consistency. Also, with digital monitoring, operating ESPs result in less downtime, as issues can be addressed before failure. On the other hand, gas lift systems still present a high frequency of intervention due to valve and flow instabilities.

| Metric | ESP | Gas Lift |

| Production Volume | Higher | Moderate |

| OPEX | Lower in water-rich wells | Higher gas compression costs |

| Energy Efficiency | Better in HPHT wells | Variable |

| Downtime | Lower (with digital monitoring) | Higher intervention frequency |

ROI Drivers for ESP Deployment

Three key levers underpin return on investment. Energy-efficient motors and optimized pump designs provide up to 10-20% power consumption savings, directly reducing the cost of operations. Real-time sensors enabling predictive maintenance reduce the frequency of repair events by extending running life.

Operators in shale plays, brownfield redevelopment projects, and deep-water fields commonly achieve returns on investment in as little as 9-18 months, depending on reservoir conditions, fluid properties, and production targets. In scenarios where rapid production uplift is a strategic priority, ESPs remain one of the economically compelling artificial-lift solutions available today.

Future Outlook & Strategic Recommendations

The ESP landscape is advancing into a more digital, resilient, and sustainability-aligned operating model. In the next decade, high-temperature and ultra-deep ESP deployment expected to define activities, increasing the adoption of electric lift in wells where thermal or pressure conditions have previously prohibited it. Digital autonomy is set to rise as SCADA-integrated ESP systems, allowing continuous optimization, automated intervention alerts, and improved production stability, become standard in all new installations. Meanwhile, environmentally conscious lift strategies are reducing energy intensity to prominence for operators, forming an important strand of any wider ESG commitment.

Emerging Growth Themes Through 2034

| Theme | Impact |

| AI-driven pump control | Higher uptime and lower OPEX |

| Energy-efficient motors | ESG alignment and potential carbon credit gains |

| Field redevelopment | Strong retrofit and replacement cycles |

| Deepwater opportunities | Meaningful revenue expansion |

These themes indicate a shift toward efficiency-centric and technology-led decision-making. Improved material science, components with high endurance, and advanced control systems expected to enable ESPs for supporting more complicated well architectures.

Recommendations for Stakeholders

| Stakeholder | Action Strategy |

| Operators | Transition to digital ESP platforms to extend run-life and improve efficiency |

| OEMs | Focus on corrosion- and sand-resistant design to improve system reliability |

| Investors | Prioritize capital allocation toward brownfield redevelopment and mid-life field optimization |

| Service providers | Build performance-based contracting models to demonstrate measurable value |

Thus, ESP technology projected to grow to anchor economic and sustainable production strategies across global oil and gas portfolios, reinforcing its importance in a transitioning energy environment.

Electric Submersible Pump for Oil & Gas Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021-2034)

- Horizontal ESP

- Vertical ESP

- Multistage ESP configurations

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Onshore

- Offshore

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Electric Submersible Pump for Oil & Gas Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 6.55 Billion |

| Market Size in 2026 | USD 7.03 Billion |

| Revenue Forecast by 2034 | USD 12.42 Billion |

| CAGR | 7.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 6.55 billion in 2025 and is projected to grow to USD 12.42 billion by 2034.

North America dominates due to high ESP installation in shale basins and strong adoption of digital lift optimization.

ESPs are used in mature wells, shale reservoirs, heavy oil fields, and offshore deepwater projects to maintain stable production.

A few of the key players in the market are Schlumberger (SLB), Baker Hughes, Halliburton, Novomet, Weatherford, GE Vernova, ChampionX, Valiant Artificial Lift Solutions, Oil Dynamics GmbH, Triol Corporation, Levare International, Novomet, and DEPAMU (Hangzhou) Pumps Technology Co.,Ltd.

Growth is driven by shale development, rising mature field interventions, and increasing offshore deepwater deployment.

Download Sample Report of Electric Submersible Pump for Oil & Gas Market

Please fill out the form to request a customized copy of the research report.