Ethylene Market Business Growth, Development Factors, 2026-2034

REPORT DETAILS

Market Statistics

Ethylene Market Overview

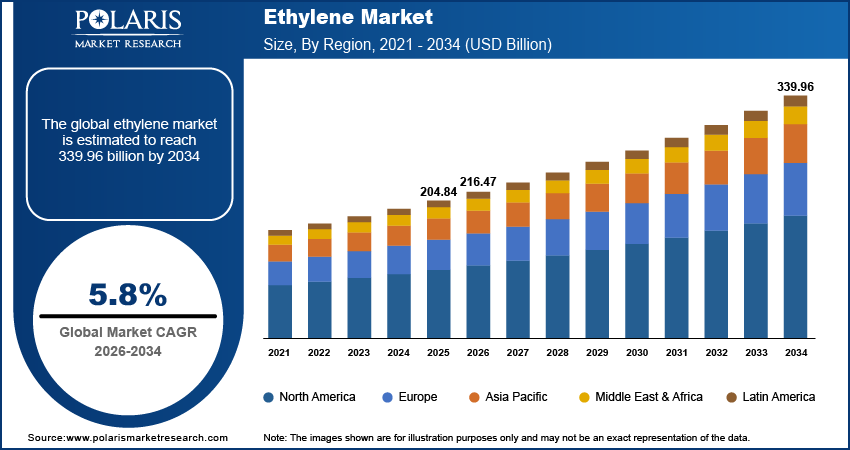

The global ethylene market size stood at USD 204.84 billion in 2025. It is projected to account for a CAGR of 5.8% between 2026 and 2034. The ethylene market growth is driven by the expansion of the automotive industry and the construction sector.

Key Insights

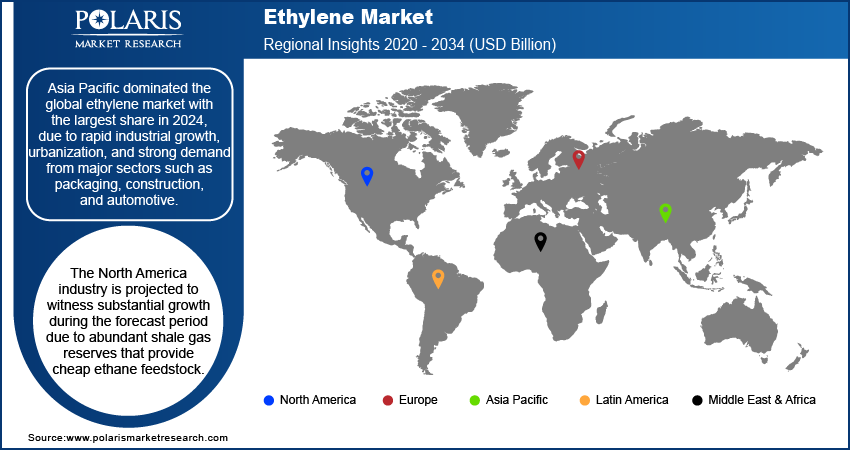

- Asia Pacific held the largest market share of 51.12% in 2025. This is due to the rapid growth of industries and urbanization.

- The North America ethylene market is expected to register substantial growth rate of CAGR 6.1% during the forecast period. This is due to the abundance of shale gas resources, which provide a cheap source of ethane, thereby increasing the production of ethylene.

- The U.S. market is expected to register substantial growth rate of CAGR 6.4% in the coming years. This is due to the abundance of shale gas resources, which provide an economical source of ethane for steam cracking.

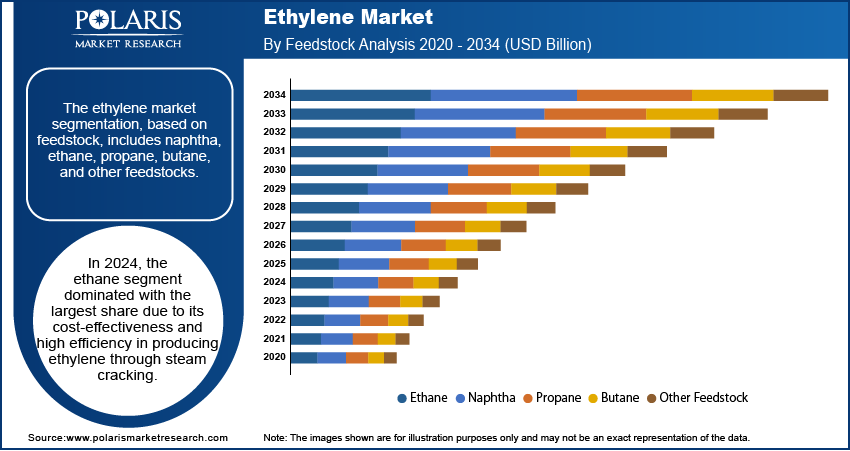

- In 2025, the ethane segment held the largest market share of 48.57%. This is due to its cost efficiency and high ethylene yield in steam cracking.

- The automotive industry is expected to register substantial growth rate of CAGR 5.9% during the forecast period. This is due to the application of ethylene in the production of lightweight materials that improve fuel efficiency and reduce emissions.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Ethylene Industry Dynamics

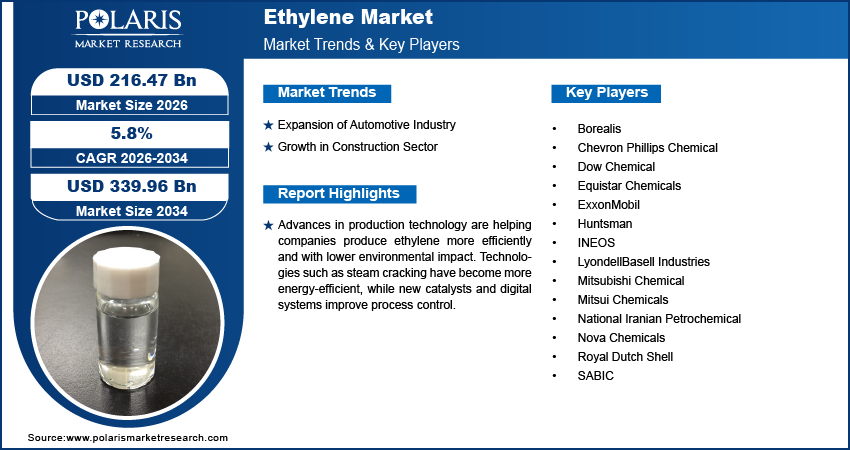

- Expansion of the automotive industry drives the demand for ethylene.

- Growth in the construction sector is fueling the industry's growth.

- Advances in production technology are allowing companies to produce ethylene in a more efficient way. Companies can also have a lower environmental impact.

- High environmental concerns and strict regulations on plastic production and waste management are ethylene market restraints that limit the growth of the industry.

Market Statistics

- 2025 Market Size: USD 204.84 billion

- 2034 Projected Market Size: USD 339.96 billion

- CAGR (2026–2034): 5.8%

- Asia Pacific: Largest market in 2025

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

AI Impact on Ethylene Market

- AI in ethylene production analyzes process variables and feedstock quality. That way, it improves yield and plant throughput.

- The integration of AI allows for adaptive process control. Parameters can be dynamically adjusted based on actual input and forecasted demand.

- AI-based analytics help in the early detection of equipment degradation and catalyst degradation. It also reduces downtime across ethylene production plants.

- AI enhances operator decision-making. It provides real-time information and notifications. It enhances safety and efficiency in ethylene production facilities.

- AI also enhances the quality of operators in controlling production rates and adhering to regulations. Additionally, digital twins created using artificial intelligence and process analytics are being employed to optimize cracking processes and lower energy consumption.

What is Ethylene?

Ethylene is a colorless and highly flammable hydrocarbon gas. It is widely used as a basic raw material for the production of various downstream chemicals and plastics

Ethylene is a key raw material in the manufacturing of plastics, particularly polyethylene, which is used in packaging, containers, and bags. The use of plastic products is increasing with the rise in consumer goods, food packaging, and e-commerce packaging. In addition, the developing nations are experiencing an increase in disposable income, which is resulting in the consumption of packaged goods. This has led to increased demand for polyethylene, thereby directly increasing the need for ethylene. In addition to the increase in volumes, there is a shift towards recyclable packaging and circular plastics, which is impacting the balance between virgin and recycled content polyethylene demand over the forecast period.

Innovation in production technology is also enabling firms to produce ethylene more effectively and with less negative impact on the environment. Steam cracking technology, for example, has become more energy-efficient, and new catalysts and digital technologies have enhanced process control. There is a trend towards the use of bio-based ethylene and recycling technologies to produce more sustainable ethylene products. Innovations have made production cheaper and more environmentally friendly, and this has encouraged firms to increase their ethylene production capacities using new and cleaner production technologies. The focus of innovation in the industry is shifting towards lowering carbon intensity, as companies are experimenting with electrified processes, enhanced heat recovery, and the use of advanced catalysts.

Ethylene Pricing & Cost Structure

Ethylene prices vary by region and are driven by feedstock prices, energy prices, plant operating rates, and downstream demand for polyethylene. Ethane-based producers have a potential cost advantage because of their higher production rates and better access to feedstocks. Naphtha-based producers can offset their costs because of their valuable co-products. In the short term, prices are influenced by turnarounds, unplanned outages, and changes in margins for key derivatives.

Drivers and Opportunities

Expansion of Automotive Industry

Ethylene-derived products are widely used in the automotive sector. These products include synthetic rubber, plastics, and glycol antifreeze. The demand for light, strong plastic materials is increasing as global car production, including electric and hybrid models, rises. As per the International Organization of Motor Vehicle Manufacturers, in 2024, the number of passenger cars produced worldwide was 67.67 million. Lighter plastic materials are used to reduce vehicle weight, which is essential for meeting environmental regulations. Ethylene-derived plastics are used in the manufacture of car dashboards, bumpers, wiring, and engine components. The increase in the number of middle-class consumers in developing countries is driving demand for cars. This is boosting sales of ethylene and its derivatives. The development of electric vehicle platforms is also supporting demand. As EVs need light materials and thermal management, there has been an increase in the use of polymers and ethylene-based chemicals in interior, exterior, and under-the-hood applications.

Growth in Construction Sector

The construction industry is on the rise globally. According to the Government of Canada, in 2023, there were 596,000 people employed in the construction industry in Ontario, Canada. Ethylene serves as a fundamental material for manufacturing pipes, insulation, flooring, paints, and adhesives. These materials form the basis of construction activities across the entire construction industry. The construction industry is experiencing significant growth in many countries due to urbanization and governments' efforts to develop infrastructure. Developing countries such as India and China are making infrastructure investments in smart cities, affordable housing, and transportation infrastructure. The construction activities require large quantities of ethylene-based materials. The construction industry has increased its use of ethylene-based materials because energy-efficient, durable building materials have become essential to modern construction solutions. Infrastructure development and the need for corrosion-resistant materials have also led to increased demand for ethylene-based products such as polyethylene pipes and insulation.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

Feedstock Analysis

Based on ethylene feedstock analysis, the market is segmented into naphtha, ethane, propane, butane, and other feedstock. The ethane segment accounted for the largest ethylene market share in 2025. Ethane is cost-effective and provides a higher ethylene yield in steam cracking. The availability of ethane, particularly in North America due to shale gas, has made it the preferred feedstock. It has better ethylene conversion rates than other feedstocks, such as naphtha or propane. Regions that have natural gas resources are also investing in ethane-based crackers to make production cheaper. The trend of using ethane as a major raw material, particularly in the U.S. Gulf and the Middle East regions, is also contributing to the growth of this category.

On the other hand, naphtha remains in use in areas where refinery integration is strong and ethane availability is low. Propane and butane are also used as alternative feedstocks, depending on regional availability, cost structure, and the ability of cracking units.

Application Analysis

The ethylene market segmentation, based on application, includes polyethylene, ethylene oxide, ethyl benzene, ethylene dichloride, and others. Polyethylene is the largest downstream application for ethylene. It is due to the demand for flexible and rigid packaging, consumer products, and industrial goods. The expansion of HDPE, LDPE, and LLDPE production capacity has a direct impact on the consumption of ethylene, especially in the Asia Pacific region, where the production of packaging, infrastructure, and manufacturing is strong.

The ethyl benzene segment registered substantial growth because ethyl benzene is mainly used in the production of styrene, which is further converted into plastics, resins, and synthetic rubbers. The growing demand for styrene-based products in packaging, electronics, insulation, and consumer goods is directly driving demand for ethyl benzene. The application of styrene in construction and automotive components is rising due to the acceleration of industrialization and urbanization processes in developing nations. Consequently, the demand for ethylbenzene and, therefore, ethylene is rising. Moreover, the rising global manufacturing base and the growing use of durable consumer goods are driving the ethyl benzene market.

Together with ethylbenzene and styrene, the demand for ethylene is also fueled by ethylene oxide and ethylene dichloride, which are used in the production of ethylene glycol, used in the manufacture of textiles and polyester, as well as PVC, used in construction and industrial sectors.

Real-World Applications of Ethylene

| End-Use Industry | Application | Benefits |

| Plastic Packaging | Polyethylene films, bottles, and food containers | Widely used in packaging due to flexibility, durability, and low cost |

| Construction Pipes | PVC and HDPE pipes for water supply and drainage | Essential in infrastructure projects for corrosion resistance and long service life |

| Automotive Components | Fuel tanks, dashboards, interior trims | Lightweight plastic parts help improve fuel efficiency and vehicle performance |

| Textiles | Polyester fibers for clothing and home furnishings | Ethylene derivatives such as ethylene glycol are used in polyester production |

| Antifreeze Production | Engine coolants and industrial heat transfer fluids | Ethylene glycol derived from ethylene is used to prevent freezing and overheating |

Source: Polaris Market Research Analysis

End Use Analysis

The ethylene market segmentation, based on end use, includes building & construction, automotive, packaging, textiles, agrochemicals & agriculture, and others. The packaging industry had the largest market share because of the extensive use of polyethylene films, bottles, and containers. The rise in online shopping, food delivery, and consumer goods globally has driven demand for flexible, lightweight, and durable packaging. The demand for food safety, shelf life, and convenience packaging is further increasing the use of ethylene-based plastics. The development of the retail industry in developing countries is further increasing the demand for ethylene in the packaging segment.

The automotive industry is projected to register substantial growth during the forecast period due to the extensive use of ethylene as a weight-reducing agent, fuel-efficient material, and a means to achieve emission norms. The increasing use of light materials for the production of auto parts such as bumpers, dashboards, and engine components by automakers is a result of the rising demand for electric and fuel-efficient vehicles. Ethylene is also employed in the production of antifreeze solutions (ethylene glycol), which is a crucial component in the cooling systems of vehicles. The rapid growth of the automotive industry in China, India, and Mexico is fueling the segmental expansion.

The growing use of protective and medical packaging, as well as industrial transit packaging, is boosting polyethylene consumption. This keeps ethylene demand relatively stable even during economic downturns.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

Asia Pacific Ethylene Market Trends

Asia Pacific led the global market with the largest share in 2025. This is due to the fast-growing industries, urbanization, and high demand from key industries like packaging, construction, and automotive. Countries such as China, India, South Korea, and Japan are key consumers and producers of ethylene. The increasing disposable income, rising middle-class populations, and surging e-commerce business are fueling the demand for ethylene-based plastics and packaging. Moreover, the governments are investing in setting up large-scale petrochemical plants to develop domestic manufacturing. The availability of low-cost labor and the increasing demand for consumer goods make the Asia Pacific a key hub for ethylene production and consumption. The area is also extending integrated refinery and petrochemicals facilities to enhance self-sufficiency in petrochemicals. This is contributing to increased production of ethylene in the region and changing regional ethylene trade flows in polyethylene and other derivatives.

China Ethylene Market Insights

The market in China is expected to experience substantial growth during the forecast period, owing to the country’s large manufacturing base and developing infrastructure. The high demand for packaging materials, construction materials, and automotive parts drives the consumption of ethylene. The Chinese government’s initiative to achieve self-sufficiency in the petrochemicals sector has resulted in substantial investments in integrated ethylene production facilities and refinery expansion. Moreover, the fast-growing e-commerce industry and the urbanization trend create demand for plastics and packaging, which rely heavily on ethylene, thereby driving the industry's growth in China.

North America Ethylene Market Analysis

The North America industry is expected to register significant growth over the forecast period due to the abundance of shale gas resources that ensure a cheap supply of ethane feedstock. The region has seen significant investment in ethane crackers, leading to an increase in production capacity, making North America a significant exporter of ethylene. The demand from the packaging, automotive, and construction sectors is high, and advancements in production technology ensure efficient and low-cost production. The U.S. and Canada are also seeing the benefit of increased exports of polyethylene and other derivatives of ethylene to Asia and Latin America. This makes operating rates and logistics capacity important variables for regional growth.

U.S. Ethylene Market Overview

The U.S. industry is expected to register significant growth over the forecast period owing to its massive shale gas resources, which offer ethane for steam cracking on a low-cost basis. In the previous decade, several world-scale ethylene production units have been commissioned in Texas and Louisiana. As a result, the U.S. has emerged as a prominent player in the global market. Domestic demand from the packaging, automotive, and industrial sectors sustains a high level of consumption in the U.S., while a substantial amount goes as polyethylene exports. The U.S. benefits from state-of-the-art infrastructure, innovation, and a favorable regulatory framework, which attracts steady investment.

Europe Ethylene Market Insights

The Europe market is expected to see substantial growth in the coming years. This is due to increasing demand from the packaging, automotive, and construction industries. The region is highly focused on sustainability and the circular economy, which promotes innovation in ethylene production and recycling. The stringent environmental regulations are pushing firms to invest in cleaner production methods and move towards bio-based or recycled feedstocks. Production costs in Europe are higher than in other regions, such as North America and Asia. However, the region has good research and infrastructure, and it is well integrated into the petrochemical value chain. Furthermore, the focus on green plastics and the EU climate goals is increasing demand and development in ethylene. The EU’s initiatives for a circular economy and decarbonization policies are fueling investments in mechanical and chemical recycling. Such investments are influencing the demand for ethylene derivatives. They are encouraging producers to opt for more sustainable production technologies.

Germany Ethylene Market Outlook

The market in Germany is expected to witness substantial growth due to the country’s robust manufacturing sector and advanced chemical industry. The country uses ethylene for high-end applications such as automotive components and building materials. Germany promotes innovation through research and sustainable solutions. Germany is home to top-tier chemical companies like BASF and Covestro. The automotive industry is one of the main drivers for light ethylene-based plastics. Germany also focuses on energy efficiency and low-emission production. This is in sync with the EU’s sustainability targets.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Analysis

The global ethylene industry is highly competitive. The industry is dominated by large and integrated companies. The companies compete based on their proximity to low-cost feedstocks, the size of their cracking facilities, and their strong connections with downstream products like polyethylene. Large companies concentrate on enhancing capacity, strategic partnerships, and efficiency to remain competitive. Sustainability projects, such as low-emission production and circular polymer solutions, are also beginning to emerge as a new factor that differentiates companies in the industry. Technology licensors and integrated petrochemical companies drive the new capacity and the conversion of ethylene into different derivative products.

List of Key Companies

- Borealis

- Chevron Phillips Chemical

- Dow Chemical

- Equistar Chemicals

- ExxonMobil

- Huntsman

- INEOS

- LyondellBasell Industries

- Mitsubishi Chemical

- Mitsui Chemicals

- National Iranian Petrochemical

- Nova Chemicals

- Royal Dutch Shell

- SABIC

Industry Developments

- October 2025: Dow and MEGlobal expanded an agreement. Dow will supply an additional equivalent of 100 KTA of ethylene from its Gulf Coast operations. (Source: corporate.dow.com)

- In February 2025, S-Oil’s Shaheen petrochemical project in Ulsan, South Korea, with a cost of USD 7 billion, achieved 55% completion and is expected to be fully operational by the first half of 2026. This project is the largest single foreign investment in South Korea. It is supported by Saudi Aramco, which owns a 63.4% stake in S-Oil. (Source: icis.com)

Future of Ethylene Market

The market is expected to report rapid growth in the coming years. The expansion will be shaped by increasing adoption of sustainable production methods. Also, there is a rising demand for bio-based ethylene derived from renewable feedstocks, such as bioethanol. Advanced recycling technologies, including chemical recycling, are supporting the development of a circular plastics economy. They help reduce plastic waste and improve material reuse. Industries are focusing on emission reduction. Thus, low-carbon production processes, including carbon capture and energy-efficient cracking technologies, are gaining importance. Rising demand for eco-friendly packaging, lightweight automotive materials, and green construction solutions will further drive innovation and long-term market growth.

Ethylene Market Segmentation

By Feedstock Outlook (Volume Kilotons; Revenue, USD Billion, 2021–2034)

- Naphtha

- Ethane

- Propane

- Butane

- Other Feedstock

By Application Outlook (Volume Kilotons; Revenue, USD Billion, 2021–2034)

- Polyethylene

- Ethylene Oxide

- Ethyl Benzene

- Ethylene Dichloride

- Others

By End Use Outlook (Volume Kilotons; Revenue, USD Billion, 2021–2034)

- Building & Construction

- Automotive

- Packaging

- Textiles

- Agrochemicals & Agriculture

- Others

By Regional Outlook (Volume Kilotons; Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 204.84 billion |

| Market Size in 2026 | USD 216.47 billion |

| Revenue Forecast by 2034 | USD 339.96 billion |

| CAGR | 5.8% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Volume in kilotons, revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Ethylene Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Ethylene Market FAQ's

The prices of ethylene differ in different regions depending on the availability and cost of feedstocks. Energy prices and demand-supply conditions also affect price trends.

Ethane-based production is more economical and gives a higher production of ethylene. Naphtha-based cracking gives a variety of co-products like propylene and aromatics.

The automotive segment is expected to witness significant growth during the forecast period. This is due to the extensive use of ethylene as a weight-reducing agent and fuel-efficient material.

The ethane segment accounted for the largest market share in 2025. Ethane is cost-effective and provides a higher ethylene yield in steam cracking.

The ethylene market stood at USD 204.84 billion in 2025. It is projected to grow to USD 339.96 billion by 2034.

The market for ethylene is projected to account for a CAGR of 5.8% between 2026 and 2034.

A few of the key players in the market are Borealis, Chevron Phillips Chemical, Dow Chemical, Equistar Chemicals, ExxonMobil, Huntsman, INEOS, LyondellBasell Industries, Mitsubishi Chemical, Mitsui Chemicals, National Iranian Petrochemical, Nova Chemicals, Royal Dutch Shell, and SABIC.

The ethane segment accounted for the largest market share in 2025. Ethane is cost-effective and provides a higher ethylene yield in steam cracking.

Asia Pacific led the global market with the largest share in 2025. This is due to the fast-growing industries and rising urbanization in the region.

The ethylene market stood at USD 204.84 billion in 2025. It is projected to grow to USD 339.96 billion by 2034.

The market for ethylene is projected to account for a CAGR of 5.8% between 2026 and 2034.

Ethane-based production is more economical and gives a higher production of ethylene. Naphtha-based cracking gives a variety of co-products like propylene and aromatics.

The prices of ethylene differ in different regions depending on the availability and cost of feedstocks. Energy prices and demand-supply conditions also affect price trends.

Polyethylene is the largest consumer of ethylene. This is due to its extensive use in packaging, consumer goods, and industrial applications.

Capacity additions help in improving supply and thus aid in long-term market growth, while shutdowns may affect supply and thus lead to short-term price fluctuations.

Stringent plastic regulations and recycling rates may moderate the demand for virgin ethylene, but growth is expected in the healthcare, infrastructure, and high-performance plastics markets.

A few of the key players in the market are Borealis, Chevron Phillips Chemical, Dow Chemical, Equistar Chemicals, ExxonMobil, Huntsman, INEOS, LyondellBasell Industries, Mitsubishi Chemical, Mitsui Chemicals, National Iranian Petrochemical, Nova Chemicals, Royal Dutch Shell, and SABIC.

Polyethylene is the largest consumer of ethylene. This is due to its extensive use in packaging, consumer goods, and industrial applications.

Capacity additions help in improving supply and thus aid in long-term market growth, while shutdowns may affect supply and thus lead to short-term price fluctuations.

Stringent plastic regulations and recycling rates may moderate the demand for virgin ethylene, but growth is expected in the healthcare, infrastructure, and high-performance plastics markets.

The Asia Pacific and Middle Eastern regions are projected to add the most ethylene capacity. This is due to robust downstream demand growth and the availability of cost-effective feedstocks.

Download Sample Report of Ethylene Market

Please fill out the form to request a customized copy of the research report.