Global Diabetes Drug Market Size, Share & Industry Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

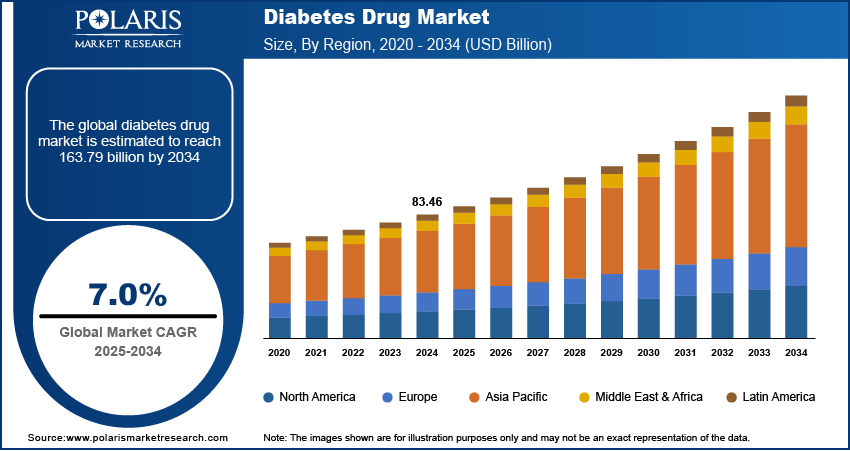

The diabetes drug market size was valued at USD 89.09 billion in 2025 and is expected to register a CAGR of 7.0% from 2026 to 2034. Growth is being driven by the rising global diabetes prevalence, the increasing burden of type 2 diabetes, expanding obesity-linked metabolic disorders, and the growing adoption of advanced oral antidiabetic drugs. The diabetes therapeutics market is also benefiting from stronger physician preference for multi-benefit therapies that support glycemic control while improving cardiovascular, renal, and weight-management outcomes. However, diabetes drugs pricing pressure and reimbursement variability hinder the industry growth. In addition, uneven healthcare access across developing economies restrains market penetration. Diabetes care evolves from glucose control alone toward broader cardiometabolic management. Thus, the market is shifting toward high-efficacy drug classes, connected care models, and more personalized treatment pathways.

Key Insights

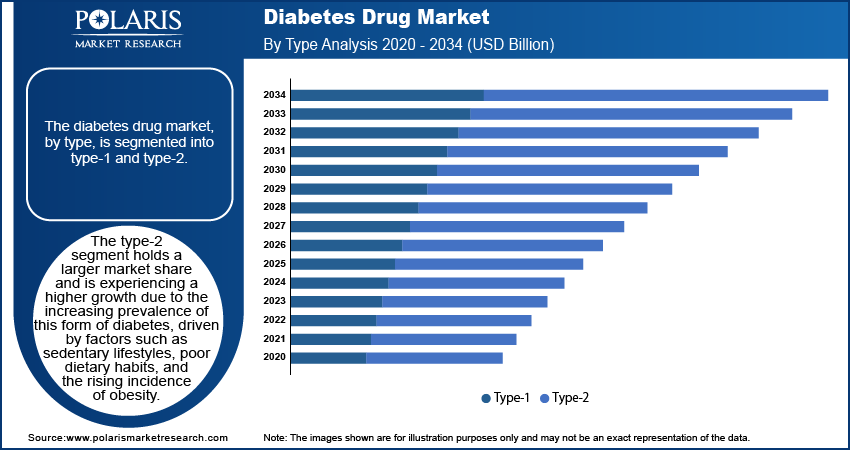

- The type-2 segment held the largest share in 2025. It is due to the increasing prevalence of this form of diabetes, driven by sedentary lifestyles and poor dietary habits.

- The intravenous (IV) segment is registering notable growth. The growth is driven by the increasing adoption of advanced therapies such as insulin infusions and biologic treatments.

- The insulin segment held the largest revenue share in 2025. Insulin is the primary treatment for type 1 and type 2 diabetes. This drives the dominance of the segment.

- North America held the largest share of the diabetes drug industry in 2025. The high prevalence of diabetes and advanced healthcare infrastructure fuel the regional market growth.

- The market in Asia Pacific is witnessing the fastest growth. It is propelled by the rising prevalence of diabetes, particularly in countries such as China, India, and Japan.

Industry Dynamics

- Continued development and adoption of Glucagon-like peptide-1 (GLP-1) receptor agonists in the management of type-2 diabetes drive the market growth.

- The rise of genetic testing and the increase in use of continuous glucose monitors (CGMs) are expected to boost the industry expansion in the coming years.

- Rapid integration of digital health technologies into diabetes management is expected to create lucrative opportunities for the market during the forecast period.

- High cost of diabetes drugs hinders the growth of the industry.

Market Statistics

2025 Market Size: USD 89.09 billion Source: Polaris Market Research Analysis Source: Polaris Market Research Analysis Source: Polaris Market Research Analysis

AI Impact on Diabetes Drug Market

- Artificial intelligence (AI) algorithms analyze massive datasets, including clinical trials, patient records, and genomic data, to find promising compounds and predict drug efficacy.

- AI in diabetes drug discovery helps find genetic markers connected to different diabetes types. It enables personalized treatments for various populations.

- AI-powered models suggest new uses for existing drugs. This reduces development time and costs.

- There is an increased use of AI in diabetes management. This is driven by innovations in diagnostics and the growing need for personalized treatment.

The diabetes drug industry emphasizes the development, production, and commercialization of diabetes medicines. The increasing prevalence of diabetes, the rising aging population, and the growing awareness of diabetes management drive the market growth. Innovative drug formulations and a growing focus on personalized medicine support the industry. Further, the use of digital health technologies is helping the market grow. Current diabetes drug market trends, like the move toward biologics, continuous glucose monitoring devices, and new treatments such as GLP-1 receptor agonists and SGLT2 inhibitors, will support the market in the coming years.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Market Dynamics

Increasing Adoption of GLP-1 Receptor Agonists

Glucagon-like peptide-1 (GLP-1) receptor agonists are gaining significant traction in the treatment of type-2 diabetes due to their ability to improve glycemic control, promote weight loss, and broader cardiometabolic outcomes. Medications like semaglutide and liraglutide are becoming the first choice for many patients. These drugs mimic the effects of GLP-1. They increase insulin secretion and block glucagon release in response to meal. According to the American Diabetes Association, GLP-1 analogues have shown good results in controlling blood sugar and reducing weight. Thus, more healthcare providers prefer them. Their continued development and adoption are expected to drive the diabetes drug market demand as patient requirements for more effective, multi-benefit treatments rise.

Shift Toward Personalized Diabetes Treatments

The shift toward personalized diabetes treatment is strengthening the advanced diabetes drugs market. Therapy selection increasingly reflects patient phenotype, real-time glucose data, co-morbidities, kidney function, weight profile, cardiovascular risk, and lifestyle patterns. Biomarker-led care, pharmacogenomic exploration, and CGM-informed treatment optimization are helping clinicians match patients with more suitable drug classes and dosing strategies. This evolution is improving adherence, reducing avoidable therapy switching, and encouraging the adoption of more targeted therapeutics in both specialist and primary-care settings.

Personalized treatments provide individualized care plans. The treatment helps optimize efficacy and minimize side effects. For example, genetic testing helps find patients who are more likely to benefit from specific types of drugs. The method enables better patient outcomes, lower healthcare costs, and increased patient adherence. The rising use of genetic testing and continuous glucose monitors (CGMs) will support this trend in the future.

Growth in Digital Health Integration

The integration of digital health technologies into diabetes management is rapidly expanding. It is driven by the increasing prevalence of diabetes and the demand for effective disease management tools. A few digital tools are continuous glucose monitors, wearable devices, connected insulin pens, smart delivery devices, remote diabetes monitoring platforms, mobile adherence applications, and AI-enabled decision support systems. These tools help manage blood sugar levels, medication adherence, and lifestyle choices. They provide real-time monitoring, personalized feedback, and data-driven insights. This information assists patients and healthcare providers in making informed decisions. A study published in Diabetes Care found that using CGMs in people with type 1 diabetes significantly lowered A1C levels and improved glycemic control. Use of digital health tools gives patients more control over their condition and improve treatment outcomes.

Pharmaceutical companies are teaming up with device and digital health platform companies. This makes the connection between diabetes drugs and diabetes care technology stronger. It is creating a broader and more defensible market ecosystem. Thus, the growing focus on digital diabetes care will boost the diabetes management market expansion.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmentation Analysis

Type-Based Insights

By type, the market is segmented into type-1 and type-2. The type-2 segment holds a larger share in 2025. The type 2 diabetes treatment market growth is fueled by the increasing prevalence of this form of diabetes. Various factors such as sedentary lifestyles, poor dietary habits, and the rising incidence of obesity boost the type-2 diabetes cases. Type-2 diabetes accounts for approximately 90–95% of all diabetes cases globally. This contributes to the strong demand for medications to managing blood sugar levels and reduce weight. They are also used to reduce complications associated with the disease. The market for type-2 diabetes drugs is expanding with the adoption of new therapies such as GLP-1 receptor agonists, SGLT2 inhibitors, and DPP-4 inhibitors. These therapies have shown efficacy in improving glycemic control and managing cardiovascular health and weight. Furthermore, the shift toward personalized treatment options and the growth of digital health tools are supporting the segment's growth.

The type-1 segment is growing because of better insulin treatments and an increase in diagnosed cases. Insulin remains the primary treatment for type-1 diabetes. The type-1 diabetes therapy market is evolving with new insulin pumps, continuous glucose monitors, and other treatments. Although this segment is smaller, it is gaining attention as the focus shifts to improving patients' quality of life through new technology and more effective insulin delivery systems. Increased awareness of type-1 diabetes management and new therapy developments support the growth of this segment.

Route of Administration-Based Insights

The diabetes drug industry is segmented into oral, intravenous, and subcutaneous. The oral segment dominated revenue share. The leading position is attributed to its benefits, such as convenience, and ease of use. Rising preference for noninvasive options also fuels the segment growth. Oral medications like metformin, DPP-4 inhibitors, and SGLT2 inhibitors are commonly prescribed for managing type 1 and type 2 diabetes. The increasing use of these oral therapies comes from their effectiveness in controlling blood sugar levels and their known safety profiles. Oral drugs are especially favored in type 2 diabetes treatment, where patients often need long-term care to manage their condition. The segment's leading position is also reinforced by the ongoing development of new oral medications that provide additional benefits like weight management and heart protection.

The intravenous (IV) segment is registering notable growth driven by the increasing adoption of advanced therapies such as insulin infusions and biologic treatments. IV therapies are mainly used in hospitals for patients with severe or uncontrolled diabetes. This is particularly true in emergencies or during the beginning stages of treatment. This area is improving due to new technology in insulin delivery systems, like insulin pumps and smart infusion devices that offer better control of blood sugar levels. Furthermore, the rise of biologic drugs and other injectable diabetes medications, along with the increasing number of diabetes-related complications, is driving the greater use of intravenous treatments in hospitals and clinics.

Drug Class-Based Insights

The market, by drug class, is segmented into insulin, sensitizers, SGLT-2 inhibitors, alpha-glucosidase inhibitors, and others. The insulin segment holds the largest market share. The insulin market is expanding since it has been the primary treatment for both type 1 and type 2 diabetes. Insulin therapies, including rapid-acting, long-acting, and premixed forms, are vital for managing blood sugar levels in patients with insulin deficiency or resistance. The segment leads the market due to the high number of type 1 diabetes patients who depend on insulin for everyday management. There is also a rising demand for insulin therapy in more advanced type 2 diabetes cases. New technologies, like insulin pumps and continuous glucose monitoring systems, are making insulin administration easier and more effective, which supports the ongoing growth of this segment. The category remains commercially significant due to product differentiation across rapid-acting, long-acting, biosimilar, and device-compatible formulations, as well as its central place in intensive glucose management.

The SGLT-2 inhibitors segment is registering the highest growth. The SGLT2 inhibitors market is driven by their dual benefits of improving blood glucose control and offering cardiovascular and renal protection. Drugs like empagliflozin and canagliflozin are becoming more popular, especially for managing type-2 diabetes. They lower blood sugar by blocking sodium-glucose co-transporter-2 in the kidneys, , which promotes glucose excretion. SGLT-2 inhibitors help with weight loss and heart health. It matches rising emphasis on overall diabetes care. As more clinical evidence shows the long-term benefits of SGLT-2 inhibitors, this group of drugs is likely to grow significantly in the coming years. This dual clinical and commercial value is increasing the class’s relevance among physicians, payers, and manufacturers focused on high-value therapy segments.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

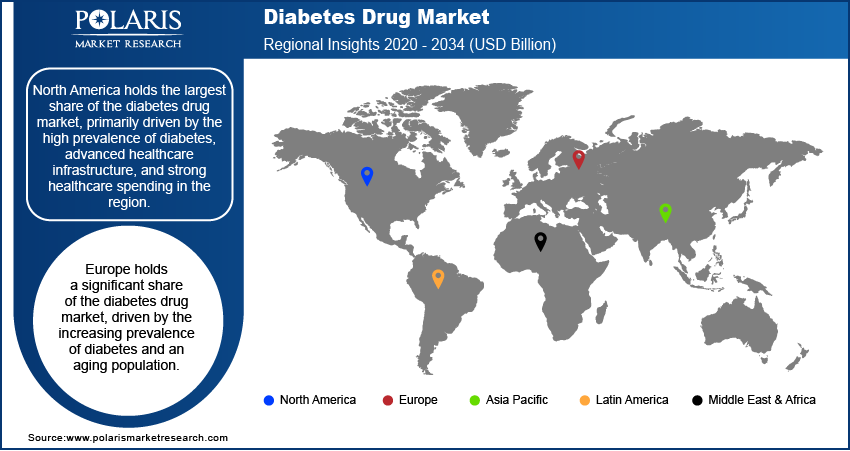

Regional Market Insights

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America has the largest share of the global market. This is mainly due to the high number of diabetes cases, strong healthcare infrastructure, and significant spending on healthcare in the region. The region also has many leading pharmaceutical companies and ongoing improvements in diabetes devices. Innovative treatments like GLP-1 receptor agonists and SGLT-2 inhibitors are available as well. Established reimbursement policies and broad access to healthcare services boost the North America diabetes drug market share. The U.S. holds the largest market share. The increasing diabetes cases, especially type-2 diabetes, fuel the dominance. Factors like obesity and an aging population contribute to this rise.

Europe holds a significant share of the global market revenue share. Rising number of diabetes cases and increasing aging population boost the market growth. In the region, there is a steady increase in diabetes cases, especially type-2 diabetes. The incidence is rising due to lifestyle changes, sedentary habits, and unhealthy diets. European countries with strong healthcare systems, such as Germany, the UK, and France, are at the forefront of adopting new diabetes treatments. These treatments include insulin therapies, GLP-1 receptor agonists, and SGLT-2 inhibitors. The region is also experiencing an increase in personalized medicine and digital health tools for managing diabetes. This trend is boosting growth in the Europe diabetes drug market. In addition, strong regulatory support and public health programs that focus on managing diabetes are contributing to the growth of the Europe diabetes therapeutics market.

The Asia Pacific diabetes drugs market is growing rapidly. It is fueled by the rising number of diabetes cases, especially in countries like China, India, and Japan. The region is reporting major demographic changes, including urbanization and an aging population. These factors boost the higher rates of type-2 diabetes. Besides lifestyle changes, factors like rapid economic growth and improved access to healthcare boost the demand for diabetes medications. Greater awareness of diabetes management and the launch of newer, more effective drug therapies accelerate the market expansion. However, challenges such as differences in healthcare infrastructure between countries and affordability concerns may affect market growth. Still, Asia Pacific is likely to keep expanding due to its large patient population and the growing use of better diabetes treatments.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

Major pharmaceutical companies such as Novo Nordisk, Sanofi, Eli Lilly, Merck, and Boehringer Ingelheim operate in the diabetes drug market. Diabetes drug companies are involved in developing, producing, and distributing various diabetes treatments. A few therapies are insulin therapies, GLP-1 receptor agonists, and SGLT-2 inhibitors. Other important players include AstraZeneca, Johnson & Johnson, Novartis, Bayer, GlaxoSmithKline, and Takeda. Companies like AbbVie, Bristol Myers Squibb, Pfizer, and Roche are contributing with their innovative diabetes treatments. Companies such as Insulet Corporation emphasize insulin delivery systems and devices. It helps them expand their presence in the market. Competitive intensity is increasing as manufacturers seek to differentiate on glucose-lowering efficacy, as well as on weight-management outcomes, cardiovascular and renal value, ease of administration, and connected-care compatibility.

In terms of competition, market players are constantly striving to innovate and introduce new therapies. They emphasize treatments that offer better control of blood glucose levels, improved patient outcomes, and fewer side effects. Large players such as Novo Nordisk and Sanofi dominate the insulin market. The rise of new therapies like GLP-1 receptor agonists and SGLT-2 inhibitors is increasing competition. Companies such as Eli Lilly, Boehringer Ingelheim, and AstraZeneca are particularly involved. As more patients look for treatments that offer multiple benefits, including cardiovascular protection and weight management, the race to develop effective drugs and cardiovascular devices is becoming intense.

Despite increased competition, industry players highlight the importance of partnerships, acquisitions, and collaborations. The strategies assist them in strengthening their market position. Many are investing in research and development to explore new drug classes and improve the effectiveness of existing therapies. Companies are increasingly using personalized medicine approaches. They focus on digital health tools and growing their presence in emerging markets. It helps them fulfil the rising demand for diabetes medications. Pricing pressures, especially in areas with strict healthcare regulations, and the challenge of managing diverse patient needs shape the competitive landscape.

List of Key Companies

- AbbVie

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol Myers Squibb

- Eli Lilly

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Novo Nordisk

- Pfizer

- Roche

- Sanofi

- Takeda

Industry Developments

- In March 2025, Eli Lilly announced plans to launch Mounjaro in China, India, Brazil, and Mexico by 2026. It aims to address the unmet demand for dual diabetes and obesity treatments in these countries.

- In August 2024, Novo Nordisk launched a new insulin therapy. It aims to provide better blood sugar control with fewer injections.

- In November 2023, Sanofi announced a global collaboration with Glooko to integrate SoloSmart, a connected device for SoloStar and DoubleStar insulin injection pens, with Glooko's digital platform.

Market Segmentation

By Type Outlook

- Type-1

- Type-2

By Route of Administration Outlook

- Oral

- Intravenous

- Subcutaneous

By Drug Class Outlook

- Insulin

- Sensitizers

- SGLT-2 Inhibitors

- Alpha-Glucosidase Inhibitors

- Others

By Distribution Channel

- Retail Pharmacies

- Online Pharmacies

- Hospital Pharmacies

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Diabetes Drug Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 89.09 billion |

| Market Size in 2026 | USD 95.15 billion |

| Revenue Forecast in 2034 | USD 163.79 billion |

| CAGR | 7.0% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Why to Buy the Diabetes Drug Market Research Report?

- Workflow/Innovation Strategy: The diabetes drug market has been segmented on the basis of type, route of administration, drug class, and distribution channel. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

- Growth/Marketing Strategy: The diabetes drug market growth and marketing strategies focus on innovation, expanding access to treatment, and enhancing patient outcomes. Companies are investing heavily in research and development to introduce new therapies, such as GLP-1 receptor agonists and SGLT-2 inhibitors, that offer additional benefits such as weight loss and cardiovascular protection. Strategic partnerships and acquisitions help increase product offerings and market reach. Also, making digital health solutions, like continuous glucose monitors and mobile apps, help companies improve patient engagement and adherence. Market players are working to grow their presence in emerging markets to take advantage of the increasing rates of diabetes worldwide.

Diabetes Drug Market FAQ's

The global market was valued at USD 89.09 billion in 2025. The market is projected to reach USD 163.79 billion by 2034. It is expected to register a CAGR of 7.0% during 2026-2034.

Insulin, GLP-1 Receptor Agonists, DPP-4 Inhibitors, and SGLT2 Inhibitors are a few drug classes. They target mechanisms of blood glucose management.

North America leads the global market. Rising investments in R&D, increasing geriatrics population, and advanced healthcare access boost the dominance.

Rising diabetes prevalence globally and a growing geriatrics population fuel the market growth. Also, lifestyle changes, obesity rates, and continuous innovation in drug formulations are key market growth drivers.

AbbVie, AstraZeneca, Bayer, Boehringer Ingelheim, Bristol Myers Squibb, Eli Lilly, GlaxoSmithKline, Johnson & Johnson, Merck, Novartis, Novo Nordisk, Pfizer, Roche, Sanofi, and Takeda are among the top players.

Download Sample Report of Diabetes Drug Market

Please fill out the form to request a customized copy of the research report.