Insulation Market Demand, Share & Industry Analysis Report, 2026-2034

REPORT DETAILS

Insulation Market Summary

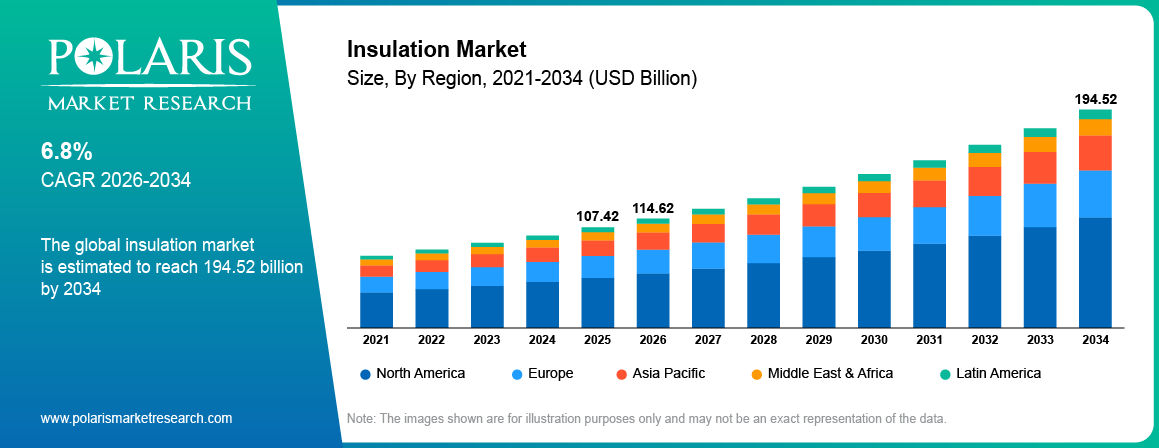

The insulation market size was valued at USD 107.42 billion in 2025. The market is projected to exhibit a CAGR of 6.8% during 2026 to 2034. The insulation materials market plays a pivotal role in increasing energy efficiency, thermal protection, and temperature management in buildings, industry, and transportation services.

Market Statistics

Key Takeaways

- Asia Pacific led global market in 2025, holding 33.95% of the revenue share. This is due to a surge in new construction and growing energy-efficiency concerns across the region.

- The North America insulation market is anticipated to show significant growth, registering a CAGR of 6.6% during 2026–2034, owing to stricter building standards and increasing adoption of eco-friendly building material.

- The expanded polystyrene (EPS) segment led the market in 2025, accounting for over 40.97% of the revenue share. EPS is cost-efficient, recyclable, and has strong thermal insulation properties. This makes it well-suited for large-scale construction and cold storage applications.

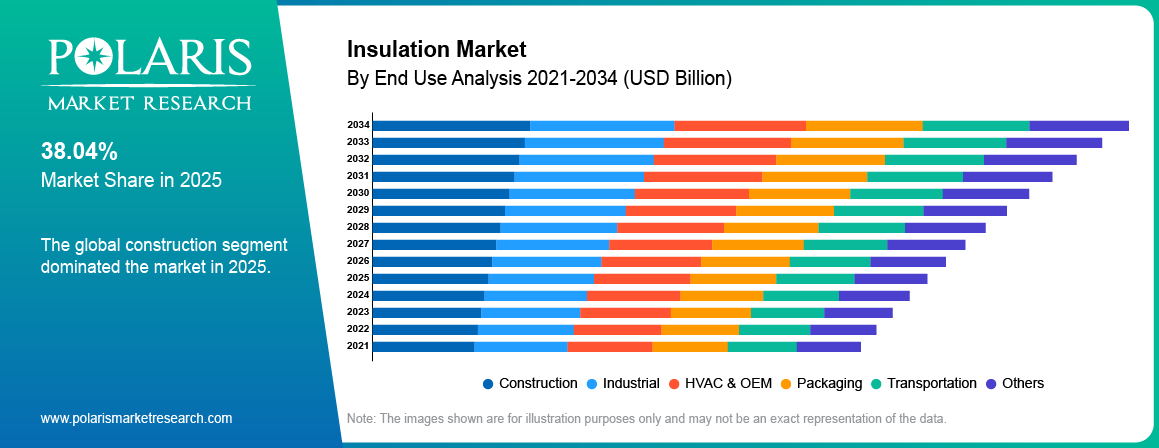

- The construction segment held the largest market revenue share in 2025, accounting for 29.88% of total revenue. This is backed by urbanization and infrastructure expenditure across regions.

Industry Dynamics

- Tax credits, subsidies, and fiscal incentives provided by governments and regulatory bodies encourage homeowners, businesses, and industries to invest in insulation solutions that improve energy efficiency and reduce ecological impact, thereby driving market expansion.

- The production of electric and hybrid vehicles is growing rapidly. This is creating demand for advanced acoustic and EV thermal insulation solutions. These materials are essential for battery thermal management, noise reduction, and passenger comfort.

- Rising energy prices and the requirement to decrease the energy intake are pushing the acquisition of insulation materials.

- Elevated production prices linked with insulation substances emerge as a restraining factor.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

What is Insulation?

Insulation, a material or system, is used to reduce the movement of heat, sound, or electricity between spaces or surfaces. It supports maintain stable temperatures and improves energy efficiency in buildings, equipment, and vehicles. Insulation materials act as barriers that limit heat loss or gain, ensuring better comfort, safety, and controlled operating conditions across different applications

The insulation market includes products that help efficiently manage temperature by reducing heat transfer. The insulation products allow temperature regulation in buildings, industries, and transportation sectors. Many types of insulation products are available in the market. These insulation products include fiberglass, mineral wool, polyurethane foam, cellulose, and expanded polystyrene, among others. Each insulation product has different applications, such as thermal, acoustic, or electrical insulation.

The application of insulation in industrial equipment, pipeline insulation, and HVAC insulation for optimal temperature retention and energy conservation is driving the insulation market. In addition, increasing consumer demand for eco-friendly, biodegradable, and recyclable insulation materials meets global sustainability requirements. The market is witnessing the development of eco-friendly insulation materials, including natural fibers and biodegradable insulation foams.

Rising energy costs and the need to reduce energy use are boosting demand for insulation materials. Increased energy efficiency in buildings and processes reduces power costs and meets strict energy-use standards. In addition, R&D activities related to high-performance insulation materials, such as aerogels, vacuum insulation panels, and phase-change materials, have contributed to the development of the market.

Technology and Innovation in Insulation Market

The insulation sector is undergoing a transition driven by technological advancements. Today, manufacturers' focus includes high-performance insulation and green products. Emerging innovations like aerogel insulation, vacuum insulation panels, and phase-change materials provide greater thermal resistance with reduced thickness.

These advanced insulation materials have found increasing uses in electric vehicles and cold chain logistics. They are also used in high-temperature industrial environments, where conventional materials are unable to meet performance requirements.

Types of Insulation Materials

| Insulation Type | Key Features | Common Application |

| Fiberglass | Lightweight, cost-effective, good thermal control | Walls, roofs, ceilings |

| Mineral Wool | Fire-resistant, soundproof, durable | Industrial equipment, walls, piping |

| Polyurethane Foam | High insulation efficiency, moisture resistant | HVAC systems, refrigeration, buildings |

| Cellulose | Eco-friendly, made from recycled materials | Wall cavities, attics, residential buildings |

Source: Polaris Market Research Analysis

How Insulation Works?

Insulation functions by slowing down the transfer of heat between surfaces or spaces. It reduces heat transfer through conduction, convection, and radiation. Most insulation materials contain trapped air or low-conductivity substances that limit heat movement. This keeps indoor spaces warm in winter and cool in summer. By maintaining consistent temperatures, insulation minimizes the need for heating and cooling systems, which helps energy savings and improves overall efficiency

Market Dynamics

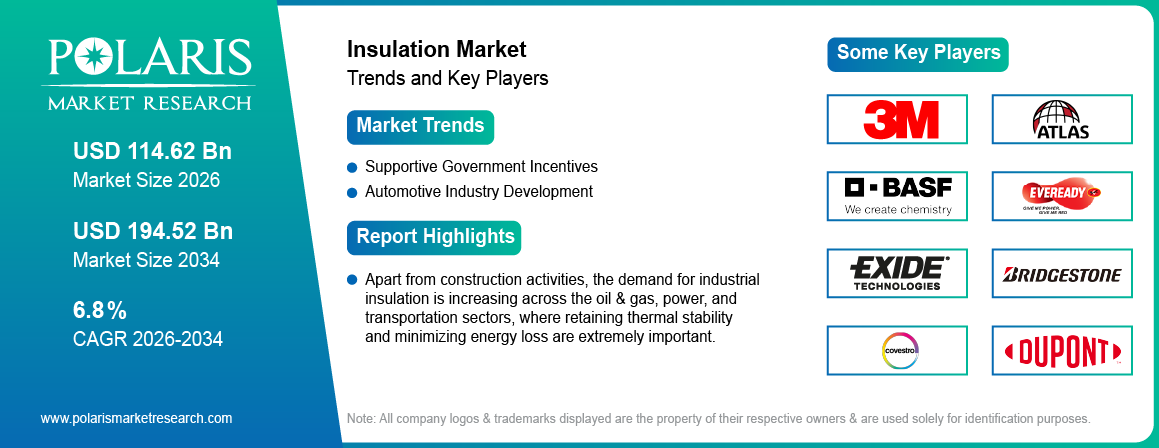

Supportive Government Incentives

Government programs focus on the importance of sustainability and energy-efficient practices. Tax credits, grants, and other kinds of economic incentives initiated by the government or other regulatory institutions encourage people and industries to go for insulation that enhance energy-saving standards. For instance, in the US, the tax credit is available for developments purchased and installed from January 2023 to December 2032. Tax credit sets specific limits on individual installations, with an annual maximum credit of USD 3,200. This includes a cap of USD 1,200 for home envelope improvements (windows, doors, insulation, and more) and HVAC systems such as furnaces and central air conditioners. Hence, supportive government incentives boost the insulation market demand across residential, commercial, and industrial sectors.

Automotive Industry Development

Rising sales of hybrid and electric vehicles have increased demand for high-performance thermal and acoustic insulation solutions that enhance energy efficiency, performance, and comfort. As stated by the International Trade Administration, the US logged sales of around 11.5 million light vehicles in 2022. Foreign automakers also contributed to the US market, with overall production of around 4.9 million units by 2023. Adequate thermal insulation plays an important role in regulating the operating temperature of EV and hybrid batteries, directly affecting performance, safety, and EV lifespan. As the automotive market innovates with new developments and expansion, demand for thermal acoustic insulation is also expected to grow over the coming years. Thus, growing vehicle sales and technological advancements may drive the market for thermal acoustic insulation over the coming period.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Market Segmentation

Market Assessment by Product

Based on product, the global insulation market has been segmented into glass wool, mineral wool, EPS, XPS, CMS fibers, calcium silicate, and others. The EPS segment dominated the market in 2025. EPS offers outstanding thermal insulation performance and is more cost-effective. EPS insulation is also used in residential and industrial buildings for wall insulation, roof insulation, and foundation insulation. Its energy-saving and water-resistant properties make it largely used in buildings. It is also recyclable and meets the criteria for sustainable buildings due to its eco-friendly nature. In addition to this, its increasing adoption in energy-saving construction techniques and an official regulation to make insulation compulsory in buildings are fueling EPS demand at a significant pace. Furthermore, the rising use of EPS insulation as a packaging material and a cold storage insulation material is rapidly boosting its market dominance.

Market Evaluation by End Use Outlook

The global insulation market segmentation, based on end use, includes industrial, construction, HVAC & OEM, packaging, transportation, and others. In 2025, the construction segment held the largest share of the insulation market, driven by rising demand for energy-efficient buildings, rapid urbanization, and the consequent growth in global infrastructure development. In recent years, the growing adoption of sustainable construction methods, driven by stringent regulations on energy and environmental concerns, has led to a substantial increase in insulation use across residential, institutional, and industrial construction projects. In addition, rising incentives and subsidies for energy-efficient development have accelerated the adoption of insulation in the construction industry. Due to significant spending on large-scale infrastructure development projects, particularly in emerging countries, the construction industry is expected to lead the global insulation market.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

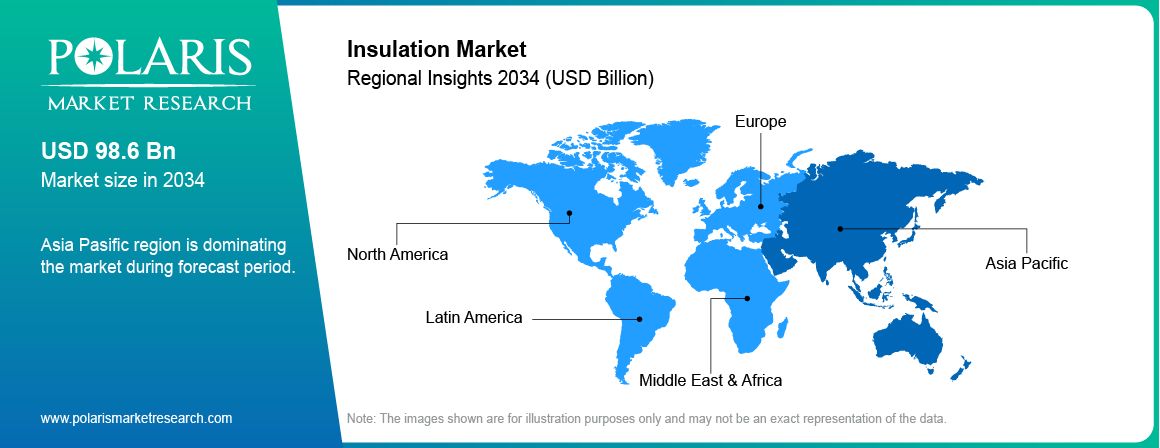

By region, the study provides insulation market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, the Asia Pacific region generated the highest revenue in the global insulation market because of rapid urbanization, extensive construction, and a focus on energy efficiency. Asia Pacific is undergoing rapid infrastructure developments due to population growth and rising demands for residential, commercial, and industrial facilities. According to Worldometer, the population of Asia was ∼4.82 billion in December 2024, up from 4.78 billion in 2023. This marks a population growth of ∼0.84% over the past year. There is a rising demand for energy-efficient solutions to reduce energy consumption and enhance sustainability in the built environment as cities expand. The governments of countries like China, India, and Japan are also increasingly adopting strict construction policies that make the use of insulation materials compulsory in any construction and renovation work. All these are contributing to the positive growth of the market.

The North America insulation market is likely to witness significant growth over the coming years due to the imposition of energy standards for buildings, the growing number of renovation projects, and greater awareness of sustainable insulation materials. The government’s promotion of energy-efficient renovation of residential and non-residential structures is increasing the demand for insulation. Ongoing research and development in spray foam and fire-resistant insulation are further driving the market’s growth.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Analysis Report

The insulation market is highly competitive. It has several global and local insulation manufacturers. These players compete with one another on the basis of product performance, sustainability, pricing, and regulatory compliance. Major players in the industry include Owens Corning, Saint-Gobain, Rockwool International, Kingspan Group, and BASF. The products manufactured by them include fiberglass insulation products, rock wool products, foam board products, and cellulose products. They are making efforts to increase the reach of the company through mergers and acquisitions. New and local competitors are focusing on innovative and more economical approaches to insulation. Increasing consumer demand for eco-friendly, energy-efficient materials is driving investment in R&D to develop materials that meet strict environmental criteria and perform exceptionally well in thermal and sound insulation. Enterprises are also working on strengthening distribution channels and consumer service in order to compete in the market. The increasing demand for eco-friendly, energy-efficient products, driven by government regulations and consumer preferences, is shaping the competitive landscape.

A few key major players are DuPont, BASF, Rockwool International A/S, Owens Corning, Atlas Roofing Corp., Rockwool International A/S, Saint-Gobain S.A., Kingspan Group, Knauf Insulation, Recticel NV/SA, Covestro AG, Bridgestone Corp., and 3M.

3M Company is a global technology services provider. Its operations span the US and international markets. Organized into four main segments, such as transportation and electronics, safety and industrial, healthcare, and consumer segment, which includes a variety of products designed for home improvement, office organization, and personal care.The transportation and electronics segment focuses on ceramic solutions, tapes, films, and products for temperature management in vehicles as well as graphic films for advertising. 3M also provides interconnection and packaging solutions, and reflective signage for safety applications.

BASF SE is a global chemical corporation that operates through seven segments: Chemicals, Materials, Industrial Solutions, Surface Technologies, Nutrition & Care, Agricultural Solutions, and Others. The Chemicals segment provides petrochemicals and intermediates, while the Materials segment offers industrial precursors such as isocyanates and polyamides. Additionally, the company supplies advanced materials, inorganic basic products, and specialty solutions for the plastics and plastic processing industries.

List of Key Companies

- 3M

- Atlas Roofing Corp.

- BASF

- Bridgestone Corp.

- Covestro AG

- DuPont

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Recticel NV/SA

- Rockwool International A/S

- Rockwool International A/S

- Saint-Gobain S.A.

Insulation Industry Developments

October 2025: Australia’s building ministers implemented a temporary pause on select residential energy efficiency upgrades under the National Construction Code. The decision intends to ease housing supply constraints and improve affordability (Source: thegoodbuilder.com)

July 2025: Saint-Gobain Weber introduced its new weberfloor acoustic systems. According to Saint-Gobain Weber, the systems have been developed in collaboration with REGUPOL and use advanced technology to improve insulation. (Source: Weber)

March 2025: Sherwin-Williams introduced the Heat-Flex Advanced Energy Barrier (AEB). According to Sherwin-Williams, the coating prevents corrosion under insulation. It also serves as a replacement for the bulky mineral-based insulation that’s traditionally used on process vessels, storage tanks, and piping for the retention of process heat. (Source: Industrialsherwin-williams.com)

September 2024: Armacell, a company offering flexible foam for equipment insulation, launched an advanced aerogel technology. (Source: Armacell.com)

May 2024: PPG introduced the PPG PITT-THERM 909 thermal spray injection coating to provide high-temperature protection in the oil & gas industry, as well as in the chemical/petrochemical industry, using silicone-based coatings. This innovative thermal protection coating outshines other thermal insulators in safety, asset protection, and productivity. (Source: investorppg.com)

Insulation Market Segmentation

By Product Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Glass Wool

- Mineral Wool

- EPS

- XPS

- CMS Fibers

- Calcium Silicate

- Other

By End Use Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- Industrial

- Construction

- Residential

- Non-Residential

- HVAC & OEM

- Packaging

- Transportation

- Other

By Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Insulation Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 107.42 billion |

| Market Size in 2026 | USD 114.62 billion |

| Revenue Forecast by 2034 | USD 194.52 billion |

| CAGR | 6.8% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Insulation Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Insulation Market FAQ's

The insulation market is expected to reach USD 194.52 billion by 2034 with a CAGR of 6.8% from 2026 to 2034.

The EPS segment leads the market due to its outstanding thermal performance, cost-effectiveness, flexibility, and recyclability. The material is applied in many ways in residential and commercial buildings.

The market drivers that contribute to its growth are government incentives, rising energy prices, growing demand from the automotive sector, urbanization, strict building standards, and a sustainability focus.

The Asia Pacific region accounts for the largest market share. This is due to urbanization, an increase in construction activities, and government initiatives towards energy-efficient building solutions.

A few key major players are DuPont, BASF, Rockwool International A/S, Owens Corning, Atlas Roofing Corp., Rockwool International A/S, Saint-Gobain S.A., Kingspan Group, Knauf Insulation, Recticel NV/SA, Covestro AG, Bridgestone Corp., and 3M.

In 2024, the construction segment accounted for the largest market share due to the increasing demand for energy-efficient buildings.

Download Sample Report of Insulation Market

Please fill out the form to request a customized copy of the research report.