Hydrogen Generation Market Growth & Opportunity, 2026-2034

REPORT DETAILS

Market Statistics

Hydrogen Generation Market Overview

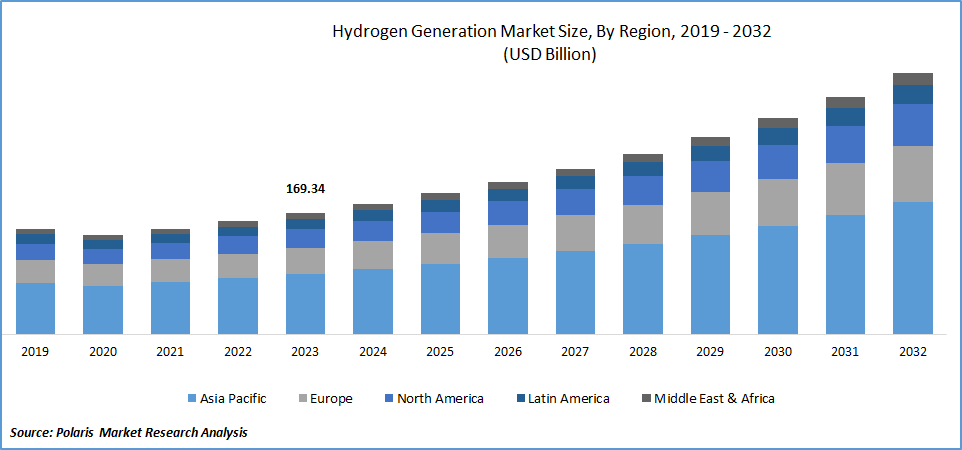

The global hydrogen generation market was valued at USD 199.2 billion in 2025 and is anticipated to grow at a CAGR of 9.20% from 2026 to 2034. The hydrogen generation market analysis by Polaris reveals that the increasing focus on clean energy alternatives and decarbonization initiatives is propelling market expansion.

Key Takeaways

- The Asia Pacific market accounted for 40.0% market share in 2025. The market in the region is led by rapid industrialization and the strong demand for the production of ammonia and hydrogen.

- North America is expected to experience rapid growth at a CAGR of 8.2%. This is due to many leading solution-provider corporations, such as Air Liquide, being present in this region.

- Steam methane reforming remains the leading process capturing 60% share. This is because it is a commercially mature solution capable of mass-producing hydrogen on a large scale. However, the long-term dynamics of the market have begun shifting towards lower-carbon solutions due to stringent environmental regulations.

- The ammonia production segment held the largest market share valued at 30.0% in 2025. This is driven by growing fertilizer demand and industrial applications.

- The merchant generation segment generated 29.97% revenue in 2025. The segment’s growth is supported by increasing third-party hydrogen supply contracts and expanding initiatives in the hydrogen economy.

Industry Dynamics

- Hydrogen generation is in high demand, driven by industries seeking alternative fuels to fossil fuels, especially the steel, refining, and heavy transportation industries.

- Several countries around the world have been supporting the transformation through policies, investment options, and development projects aimed at large-scale production of green hydrogen.

- The use of electrolysis technology and the integration of renewable energy sources offer opportunities for expanding sustainable hydrogen generation.

- The cost of production is quite high due to the lack of widespread infrastructure.

Hydrogen Generation Market Statistics

- 2025 Market Size: USD 199.2 billion

- 2034 Projected Market Size: USD 439.8 billion

- CAGR (2026-2034): 9.20%

- Asia Pacific: Largest market in 2025

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

What is Hydrogen Generation Market?

The hydrogen generation market is increasingly a central part of the world's transition to new energy sources. It is enabling industries to cut emissions without necessarily compromising energy security. Hydrogen is increasingly recognized as an extremely versatile carrier of energy that can support power generation, industrial processes, and transportation, with long-term energy storage. As commitments to net-zero grow, investment in deploying technologies for clean hydrogen generation is accelerating across developed and emerging economies.

The deployment of generation systems is being driven by the increasing need to reduce carbon emissions from refining activities. Over the long term, implementing different incentive schemes to limit the sulfur content of motor oil, diesel fuel, and gasoline would promote growth in the generation industry. Highly efficient energy carriers, such as hydrogen, are expected to continue expanding into previously untapped markets. Over the projected period, it is expected that worldwide energy demand will increase by almost two-thirds of its current level.

The market for hydrogen gas covers on-site hydrogen generation systems, the rising adoption of advanced innovations, increased use of hydrogen across multiple industries, and the development of green production technologies. New-age projects related to distributed energy and its usage are expected to boost the market growth. For instance, in January 2024, TotalEnergies and Air Liquide announced the launch of TEAL mobility, a combined venture to form the leader in the distribution of hydrogen in Europe for heavy-duty vehicles.

The U.S. is one of the world's pioneers in the use of sustainable energy solutions across industries such as manufacturing, transportation, and power generation. In December 2006, the Department of Transportation (DOT) and the Department of Energy (DOE) in the U.S. unveiled an initiative to enhance research and development (R&D) and validate technologies for establishing hydrogen infrastructure. Deliverables established by the federal government were included in this plan to support the nation's hydrogen infrastructure development. It was created in accordance with the National Hydrogen Energy Roadmap and Vision. One of the main goals government agencies have set for themselves is the development and installation of energy-efficient, reasonably priced hydrogen stations across the nation. It is anticipated that all of these factors will increase U.S. demand for the hydrogen generation market.

Difference Between Green Hydrogen and Blue Hydrogen

Green hydrogen is considered the clean hydrogen solution. It has a zero-emission production pathway. However, blue hydrogen acts as a bridge technology. It helps reduce emissions using existing fossil fuel infrastructure.

| Parameter | Green Hydrogen | Blue Hydrogen |

| Production Method | Produced through electrolysis of water | Produced from natural gas using SMR or ATR |

| Energy Source | Renewable energy (solar, wind, hydro) | Fossil fuel (mainly natural gas) |

| Carbon Emissions | Near-zero carbon emissions | Reduced emissions with carbon capture |

| Use of Carbon Capture | Not required | Required (CCS technology used) |

| Environmental Impact | Highly sustainable and clean | Lower emissions than gray hydrogen but still fossil-based |

| Production Cost | Higher due to renewable electricity and electrolyzer costs | Lower than green hydrogen in many regions |

| Infrastructure Requirement | Requires renewable power and electrolyzers | Uses existing gas infrastructure with CCS |

| Market Role | Long-term clean energy solution | Transitional low-carbon solution |

| Adoption Growth | Rapidly growing with net-zero policies | Growing where gas and CCS infrastructure exist |

| Example Use Cases | Renewable fuel, mobility, green steel | Industrial fuel, refineries, ammonia production |

Source: Polaris Market Research Analysis

What’s Driving Hydrogen Generation Market Demand?

Rising Industrialization and Infrastructure Development

The increasing urban and industrial expansion is encouraging countries to adopt various power generation methods to fulfill rising energy demand. Additionally, rapid infrastructure development activities and an increasing population across regions such as the Middle East, Africa, and the Asia Pacific. Rising concern regarding clean and sustainable energy use for reducing the dependency on traditional fossil fuels, such as natural gas & crude oil, is supporting the adoption of hydrogen-based energy solutions worldwide. These combined factors are driving demand in the hydrogen generation market.

Shift Toward Sustainable and Clean Energy

A growing focus on the clean energy transition and supportive government policies are influencing the hydrogen generation market. The global energy challenge has increased interest in low-carbon energy sources. Higher investments are being made in the research and development of alternative energy solutions. Sustainability in energy generation involves early-stage use of cleaner technologies due to their long-term environmental and industrial impact. These shifts are positively influencing the demand for hydrogen generation.

Environmental Regulations and Clean Fuel Research

Over the past two decades, increased research into clean fuels and emission-reduction technologies, including the desulfurization of petroleum products, has supported environmental catalysis activities worldwide. Rising air pollution levels and stricter fuel quality regulations, such as those enforced by the U.S. EPA, are influencing the production and distribution of gasoline and diesel fuels. Such regulatory pressure is encouraging the adoption of hydrogen in cleaner energy and industrial applications.

What’s Restraining Hydrogen Generation Market Demand?

Expensive Storage, Transport, and Handling Costs

Nowadays, tanks are the most popular place to store hydrogen for stationary and small-scale mobile applications, either as a gas or a liquid. However, hydrogen storage is only part of the cost challenge. The broader cost challenge also includes transportation, compression, and handling infrastructure. Transporting and storing hydrogen requires the use of high-pressure compression systems and cooling equipment. Specialized logistics are also needed. All of this increases overall operational costs.

The storage tanks used to store hydrogen must have low temperatures, a non-reactive medium, and fast, reversible hydrogen adsorption/desorption that doesn't require heat energy. Meeting these technical requirements makes storage systems capital-intensive. It also limits scalability in large-scale and distributed applications. It requires specialized storage tanks, which tend to have a huge price, creating a major hindrance to the market.

There are energy losses due to the compression or liquefaction of hydrogen when it is transported over long distances. Additional costs are incurred due to the transport vessels or reinforced pipes. When hydrogen molecules are needed, the ammonia stored as hydrogen must be broken down using thermal energy. This adds to conversion and energy expenses. As a result, modified storage and transport systems for hydrogen involve high costs.

In addition, the storage of hydrogen, as well as the expensive hydrogen infrastructure constraints for compression and distribution, have been identified as another major hindrance to the widespread adoption of fuel cells. These factors are expected to continue to hamper the market's growth due to associated costs and scaling issues.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Report Segmentation

The segmentation of the hydrogen generation market provides a detailed overview of technology adoption and end-use demand, supply models, and regional performance. The hydrogen generation market segmentation enables stakeholders to identify high-growth areas and emerging investment opportunities along the value chain.

By Technology Insights

Based on technology analysis, the market is segmented on the basis of coal gasification, steam methane reforming, and others. The steam methane reforming segment dominated with 60.0% revenue share in the hydrogen generation market. Since steam methane reformers are the most cost-effective means of producing hydrogen, the growing global demand for hydrogen generation is a major driving force behind technological breakthroughs. Operational advantages, such as the steam methane reforming process's high conversion efficiency, are additional growth-promoting factors. Over the projected period, the steam methane reforming segment is expected to remain the leading segment.

Coal gasification technology is anticipated to expand rapidly with 7.4% CAGR over the forecast period. For two centuries, hydrogen has been produced from coal using a process known as coal gasification. It is also recognized as a tried-and-true method of producing hydrogen, similar to steam methane reforming. The U.S. has a vast domestic coal resource. It is anticipated that using coal to produce hydrogen for the transportation sector will help America become less reliant on foreign petroleum supplies.

Comparison Matrix: SMR vs Electrolysis vs Gasification in Hydrogen Generation Market

| Parameter | Steam Methane Reforming (SMR) | Electrolysis | Gasification |

| Feedstock | Natural gas (mainly methane) | Water + Electricity | Coal, biomass, or waste |

| Process Type | Thermal catalytic process | Electrochemical process | Thermochemical conversion |

| Hydrogen Output | High-volume, large-scale production | Moderate to high depending on power source | High, especially for industrial use |

| Carbon Emissions | High CO₂ emissions (unless paired with CCS) | Very low if powered by renewables | Moderate to high depending on feedstock |

| Cost Efficiency | Lowest production cost; mature technology | Higher cost due to electricity demand | Moderate to high capital and operating cost |

| Infrastructure Maturity | Highly established and widely deployed | Rapidly growing but still developing | Mature for coal; developing for biomass |

| Energy Source Dependency | Fossil fuel dependent | Renewable electricity dependent | Fossil fuels or biomass dependent |

| Scalability | Highly scalable for industrial hydrogen | Scalable with renewable energy expansion | Suitable for large centralized plants |

| Sustainability Level | Low to medium (higher with CCS) | High (green hydrogen pathway) | Medium (higher with biomass feedstock) |

| Key Applications | Refineries, ammonia, methanol production | Green hydrogen, mobility, energy storage | Power generation, chemicals, industrial fuels |

Source: Polaris Market Research Analysis

By Application Insights

Based on application type analysis, the market has been segmented on the basis of power generation, transportation, petroleum refining, ammonia production, methanol production, and others. Ammonia production is a dominant application generating 30.0% share in the hydrogen generation market. Ammonia offers potential as a carbon-free fuel, energy storage, and a hydrogen carrier, presenting an opportunity for renewable hydrogen innovations that can be practiced on a large scale. At ammonia facilities, hydrogen is usually produced on-site using fossil fuels as feedstock. Demand for hydrogen-based power generation is rising, as it is a reliable and relatively inexpensive source of energy. In developed areas where clean, efficient energy is a top priority, such as North America and Europe, hydrogen-based power generation technology has established a strong foothold.

By System Insights

Based on system analysis, the market has been segmented into captive and merchant. Of these two types of generation systems, the merchant generation system accounts for a significant market share. This is due to its feature of producing at a central facility and later delivering and selling to consumers via pipeline.

Source: Polaris Market Research Analysis Need Granular Data Across All Market Segments? Request Customization

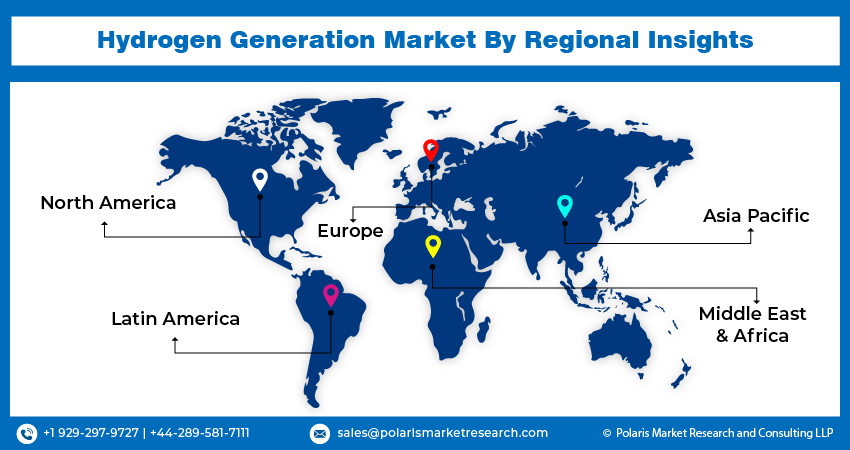

Regional Insights

Asia Pacific

The Asia Pacific region dominated the global market with the 40.0% market share in 2025 and is expected to maintain its dominance over the anticipated period. The growth of the segment market can be largely attributed to significant investments in research and development to develop eco-friendly solutions. This is boosting market growth in the Asia Pacific region. Also, the countries in their respective regions have multiple refineries, which play an essential role in hydrogen generation. Additionally, a few governments in some countries in this region are focusing on clean, green technologies for the hydrogen generation market.

North America

North America is anticipated to grow rapidly with a CAGR of 8.2% over the forecast period. The region is experiencing significant growth due to the presence of major solution-provider companies such as Air Products, Chemicals, and Air Liquide. Blue hydrogen is produced on a large scale in the region. Also, chemical companies and the oil refining industry are driving demand for hydrogen, which is driving the overall market.

The industry is highly fragmented and is expected to face intense competition from multiple competitors across different stages of the value chain. Major hydrogen generation companies continue to enhance their technological capabilities with the primary aim of increasing efficiency and reducing costs. These companies are continually enhancing their technological capabilities to increase efficiency.

Hydrogen production market players are focusing on strengthening their market position through strategic partnerships, technology-powered product upgrades, and joint ventures. Strategic alliances have become common among energy, industrial consumer, and infrastructure companies.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Some of the major players operating in the global market include:

- Air Liquide S.A.

- Cummins Inc.

- Total Energies

- ITM Power

- Air Products and Chemicals, Inc.

- FuelCell Energy, Inc.

- Iwatani Corporation

- The Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- Linde Plc

- Uniper SE

- Green Hydrogen Systems

- Hydrogenics Corporation

- Tokyo Gas Chemical Co., Ltd

- INOX Air Products Ltd.

Recent Developments

Recent developments in the hydrogen generation sector include a focus on green hydrogen projects, massive electrolysers, and supportive government frameworks. All these emerging hydrogen generation market trends point to growing commercial acceptability and viability of hydrogen fuel.

- April 2026: H2SITE signed a strategic agreement with Petronor to deploy its high-efficiency hydrogen separation technology at Petronor’s refinery. The partnership aims to to pioneer high-purity hydrogen production in refining using advanced membrane technology. (Source: h2site.eu)

- May 2025: Hitachi Energy revealed the successful demonstration of its new energy supply system, HyFlex. The company stated that the new system is based on zero-emission hydrogen-powered fuel cell technology. Its portable design allows for quick transportation and immediate use. (Source: hitachienergy.com)

- May 2025: ITM Power signed an agreement with a confidential customer to supply over 300 MW of electrolyzers for a green hydrogen power plant in the Asia Pacific (APAC) region. ITM Power stated that the project is aimed at reducing carbon emissions. It has secured local government funding and is currently awaiting a Final Investment Decision (FID). (Source: itm-power.com)

- March 2025: Air Liquide inaugurated a new hydrogen energy facility in Shanghai. The company stated that the new facility can supply 12 hydrogen refueling stations and has the capacity to fuel more than 1,000 medium- and heavy-duty trucks daily. (Source: airliquide.com)

- January 2025: U.S. Treasury finalized regulations for the Section 45V clean hydrogen production tax credit. These rules, under the Inflation Reduction Act, define the requirements producers must meet to qualify for tax credits for clean hydrogen generation.(Source: treasury.gov)

- May 2024: The state-owned natural gas company GAIL Ltd. (India) contracted their first-ever green hydrogen project 2024 in central India. By electrolyzing water with renewable energy, this green hydrogen plant is expected to generate a whopping 4.3 TPD of hydrogen using 10MW PEM electrolyzer units imported from Canada. (Source: gailonline.com)

- April 2024: SJVN Limited inaugurated India's first Multi-purpose Green Hydrogen Pilot Project at SJVN’s 1,500 MW Nathpa Jhakri Hydro Power Station (NJHPS) in Jhakri, Himachal Pradesh. The green hydrogen produced from the project will be utilized for the High Velocity Oxygen Fuel (HVOF) Coating Facility of NJHPS to meet its combustion fuel requirements. (Source: pib.gov.in)

- March 2024: Chevron New Energies received a 5-MW electrolyzer technology system from the company Accelera by Cummins in order to produce low-carbon-intensity electrolytic hydrogen at its capacity plants located at Lost Hills, California, USA. (Source: accelerazero.com)

Hydrogen Generation Market Segmentation

By Technology Outlook (Revenue – USD Billion, 2021–2034)

- Coal Gasification

- Steam Methane Reforming

- Others

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Power Generation

- Transportation

- Petroleum Refining

- Ammonia Production

- Methanol Production

- Others

By System Outlook (Revenue – USD Billion, 2021–2034)

- Captive

- Merchant

By Source Outlook (Revenue – USD Billion, 2021–2034)

- Water

- Biomass

- Coal

- Natural Gas

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Hydrogen Generation Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 199.2 billion |

| Market Size in 2026 | USD 217.3 billion |

| Revenue Forecast by 2034 | USD 439.8 billion |

| CAGR | 9.20% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Hydrogen Generation Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Hydrogen Generation Market FAQ's

The hydrogen generation market is expected to reach USD 439.8 billion by 2034, growing at a CAGR of 9.20% from 2026 to 2034.

Steam methane reforming leads this market because of its economies of scale and conventional infrastructure. Water electrolysis is emerging rapidly for the production of green hydrogen and is GHG emissions-free.

Ammonia production leads the application segment, followed closely by petroleum refining, chemical processing, fuel cells, and the transportation sector.

The Asia Pacific region has the leading hydrogen generation market share due to increased government spending on R&D, the development of clean energy projects, and the expanding hydrogen infrastructure base in China, Japan, and India.

Green hydrogen has a zero-carbon-emission cycle when produced by electrolysis using renewable energy sources. It thus plays a crucial role in decarbonizing industries and achieving net-zero carbon emissions by 2050.

Download Sample Report of Hydrogen Generation Market

Please fill out the form to request a customized copy of the research report.