Market Overview

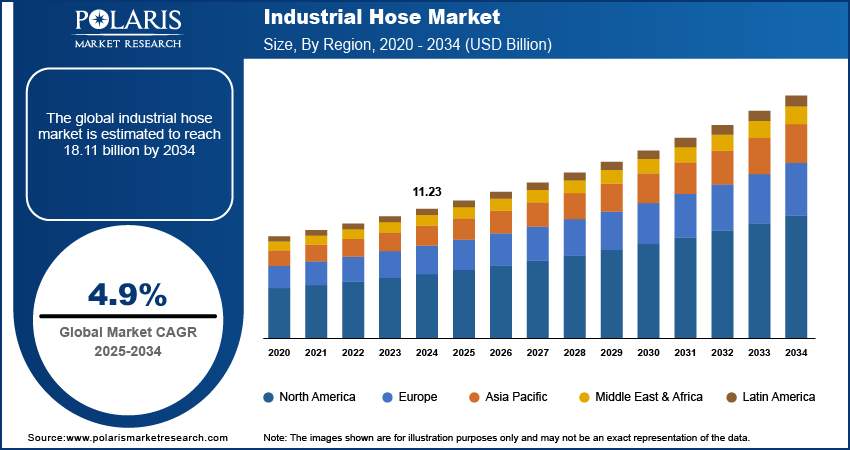

The global industrial hose market size was valued at USD 15.84 billion in 2025. The industrial hose market CAGR is projected to be 7.8% from 2026 to 2034. The growing number of offshore exploration ventures, shale gas production, and refinery upgrades creates a demand for high-performance hoses that can resist extreme temperatures, corrosive fluids, and high pressure.

The market comprises flexible and reinforced tubing systems that are employed for the transportation of liquids, gases, and other materials in various industries. The hoses are of prime importance in the oil & gas, agricultural, chemical, food processing, construction, and water treatment sectors, as they are designed to withstand pressure, harsh environments, and special requirements. The requirement for hygienic and FDA-compliant hoses is on the rise in the food and beverage sector, where the transfer of fluids needs to be safe and contamination-free. The application of these hoses in dairy, brewery, and processing plants is fueling the growth of specialized hose solutions.

Key Insights

- The rubber segment led the industrial hose market in 2025. Industrial hoses made from rubber can resist abrasion and high-pressure conditions.

- The pharmaceuticals segment is projected to witness the highest CAGR. This is due to increasing investments in cleanroom manufacturing and biopharmaceutical production.

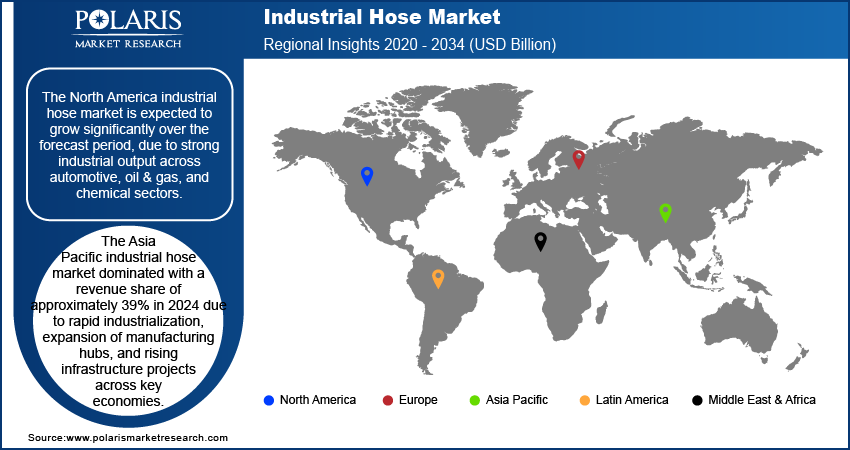

- Asia Pacific accounted for the largest market share in 2025. This is attributed to the fast-growing industrialization and development of manufacturing bases in the region.

- The North America market is expected to register substantial growth.The market is fueled by the strong manufacturing base in the automotive and chemical industries.

Industry Dynamics

- There is an increase in infrastructure development and construction activities across the globe. This has resulted in a rise in the demand for quality and long-lasting hose systems at construction sites.

- An increase in oil and gas operations creates a demand for industrial hoses.

- Advancements in material science are opening up possibilities for green products.

- High raw material costs could pose a challenge for the industrial hose market.

Market Statistics

2025 Market Size: USD 15.84 billion

2034 Projected Market Size: USD 31.22 billion

CAGR (2026–2034): 7.8%

Asia Pacific: Largest Market in 2025

To Understand More About this Research:Request a Free Sample Report

In modern agriculture, irrigation, pesticide spraying, and slurry transfer are highly dependent on industrial hoses that can withstand exposure to sunlight, rough handling, and varying weather conditions. Industrial hoses with high flexibility and resistance to wear are particularly valuable in agricultural applications. In addition, innovations in materials have introduced thermoplastics, polytetrafluoroethylene (PTFE), and reinforced rubber. These materials allow for longer-lasting and more flexible hose solutions. Such advances are increasing the use of industrial hoses in various sectors.

Industrial hoses can be broadly categorized depending on the type of fluid that they are meant to handle, including water, air, chemicals, oil or fuel, steam, and food-grade fluids. They can also be categorized depending on the type of material that they are made of, including rubber, PVC, silicone, PTFE, and thermoplastics. They can also be categorized depending on their design, including braided or spiral reinforcement. For clarity, this analysis focuses on industrial hoses used for fluid transfer across commercial and industrial sectors. It excludes basic consumer garden hoses.

Market Dynamics

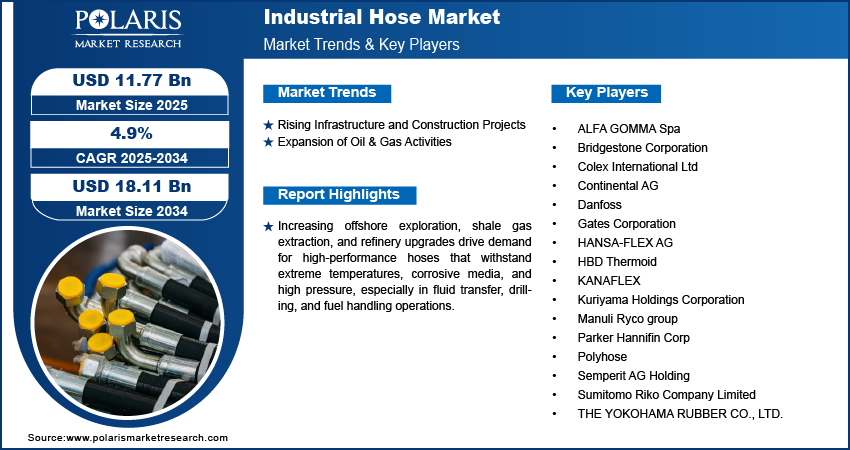

Rising Infrastructure and Construction Projects

The increasing number of infrastructure and construction projects is a key driver for the market. As per the U.S. Census Bureau, the construction spending done in the first four months of 2025 was USD 660.2 billion, marking a 1.4% increase from the same period in 2024, which stood at USD 651.3 billion. This positive movement indicates the steady growth of infrastructure and construction projects. The growing urbanization, transportation, and development of public utilities are also accelerating the demand for robust and efficient hose systems in the construction sector. Hoses are a critical requirement for applications such as concrete pumping and draining water from flooded areas. They are also needed for transporting cement mixtures and operating pneumatic tools. Construction sites are known to be harsh and unpredictable. As such, the demand for hoses that are flexible, abrasion-resistant, and capable of withstanding intense mechanical loads is increasing. Large-scale construction projects like highways, office buildings, and metro rail networks require high-capacity construction industrial hose systems to ensure smooth functionality. This steady demand in new and existing construction projects is fueling the market for industrial hoses.

The growing construction activities are thereby creating a substantial demand for rubber and reinforced thermoplastic hoses, particularly for dewatering and handling rough materials. The demand is also being fueled by the use of air hoses for operating tools and water suction and discharge hoses for drainage and site management. With the increasing infrastructure and construction projects, the need for reliable hose solutions is also increasing.

Expansion of Oil & Gas Activities

A rise in oil and gas operations drives demand for industrial hoses. According to the Bureau of Ocean Energy Management, there has been a 22.6% rise in remaining recoverable reserves, which stood at 7.04 billion barrels of oil equivalent as of 2025. This includes 5.77 billion barrels of oil and 7.15 trillion cubic feet of natural gas, which reflects the rise in exploration and production activities since 2021. This trend indicates the development and investment in oil and gas resources, which will continue to fuel the growth of the industry. Exploration of deep-sea and hard-to-reach regions has led to an increase in the demand for hoses that can withstand extreme temperatures, corrosive conditions, and high pressure. These hoses are widely used in offshore platforms, onshore drilling, refinery plants, and petrochemical transportation. Fuel transfer, mud circulation, hydraulic fracturing, and chemical injection operations require specialized hoses that can withstand aggressive fluids and maintain their integrity. The increasing emphasis on energy security and investment in shale gas and LNG infrastructure is driving the demand for high-performance industrial hoses that can meet tough safety and performance criteria.

In the oil and gas industry, buyers are emphasizing more on safety and reliability while choosing the hoses. The main concerns of the buyers are chemical resistant hose varieties that can withstand aggressive fluids, high temperature industrial hose solutions that can withstand extreme temperatures, and good burst pressure rating performance to avoid hose failure. In addition, there is a growing need for static dissipative hose designs and secure hose couplings integrity.

Industrial Hose Buyer’s Guide

A good industrial hose selection guide will begin by examining media compatibility, including chemical composition, fluid viscosity, and the presence of solid materials. The buyer will then examine operating pressure or vacuum, temperature range, and the requirement for an abrasion-resistant industrial hose. When selecting an industrial hose solution, the bend radius and flexibility are also considered, particularly in confined spaces. In industrial hose solutions involving fuels or solvents, chemical compatibility and electrostatic hazards are also considered. Appropriate couplings and fittings for the hoses are chosen depending on the installation requirements and the anticipated maintenance frequency.

Segment Insights

Material Type Analysis

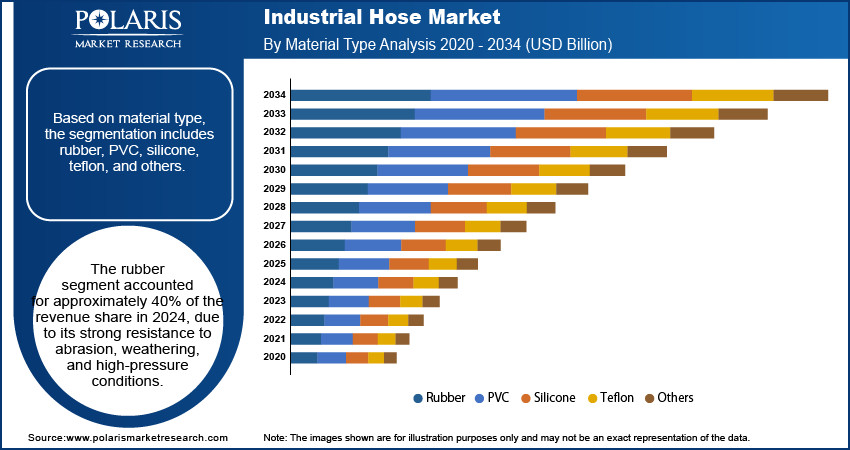

Based on material type, the segmentation includes rubber, PVC, silicone, teflon, and others. The rubber segment accounted for about 40% of revenue in 2025. This is due to its high resistance to abrasion, weathering, and high pressure. Rubber hoses are commonly used in demanding applications like mining, construction, and oil & gas due to their high performance and durability. Their ability to operate in harsh fluids and rugged terrain makes them the best choice for heavy-duty industrial applications. Moreover, the development of synthetic rubber materials such as EPDM and nitrile has improved their reliability, making them the preferred choice for heavy-duty applications that require flexibility and high resistance to mechanical stress.

The PVC segment is gaining popularity due to its light weight, cost-effectiveness, and suitability for medium- and low-pressure applications. In 2025, demand for PVC increased in sectors where hose replacement and ease of handling are considered. These include agriculture, water supply, and ventilation systems. PVC hoses are chemically inert to many chemicals. This makes them ideal for light chemical transfer and food-grade applications. The smooth inner surface of PVC hoses minimizes friction losses, making them ideal for fluid transfer. Furthermore, color-coded, transparent PVC hoses are ideal for industrial use in observing fluid flow. The use of PVC hoses offers an additional level of control and safety.

In general, the choice of hose material depends on several factors. These are chemical resistance, flexibility, temperature resistance, and life-cycle cost of the hose. Different materials for chemical-resistant hoses are selected based on the specific application's needs. For example, PTFE and silicone hose solutions are widely used in applications where high hygiene and purity, as well as the handling of aggressive fluids, are critical. Composite industrial hose solutions are also being widely used in applications that demand a strong yet lightweight solution.

Application Analysis

Based on application, the industrial hose market segmentation includes automotive, construction & infrastructure, oil & gas, pharmaceuticals, food & beverages, water & wastewater treatment, mining, and others. The construction & infrastructure industry had the largest revenue share in 2025. This is mainly due to the increasing expenditure on infrastructure around the world. The construction & infrastructure industry demands high-quality hoses for concrete transfer, dewatering, cement spraying, and dust suppression systems.. The increasing urbanization and smart city development have fueled demand for heavy-duty hose systems that operate efficiently in harsh site conditions and high temperatures. Construction and infrastructure industrial hoses require both flexibility and high mechanical resistance. This has further fueled demand for reinforced and multi-layered hose solutions.

The pharmaceutical industry is expected to post the highest CAGR over the forecast period, driven by rising investments in cleanroom manufacturing and biopharmaceutical production. There is a sharp rise in demand for high-purity hoses that meet stringent sanitary and regulatory requirements. These hoses need to be resistant to contamination, flexible during autoclaving, and provide consistent fluid transfer in aseptic conditions. Silicone- and PTFE-based hoses are commonly used for the transfer of active pharmaceutical ingredients and solvents. The scale of pharmaceutical manufacturing is expanding as the number of drugs, vaccines, and personalized medicine applications grows, thereby creating a continuous demand for specialized hose solutions that meet stringent industry protocols.

Media Type Analysis

Industrial hoses are also categorized depending on the type of media they transport, including water suction and discharge, air/pneumatic, chemical transfer, steam, oil and fuel transfer, and food-grade fluids. The media type is one of the most important factors that determine the inner lining material, layers of reinforcement, and coupling requirements, thus providing a convenient means for procurement and engineering groups to compare alternatives.

Reinforcement Analysis

By construction, industrial hoses are generally categorized into textile-braided, wire-braided, wire-spiral, and composite hoses. The selection of the reinforcement material is normally based on pressure requirements, resistance to repeated use, and handling characteristics. The composite hose is generally preferred when strength-to-weight ratio and flexibility are required.

Compliance Considerations Shaping Purchase Decisions

Compliance is emerging as an important consideration in selecting industrial hoses. This is particularly true for highly regulated industries such as food and beverage, pharmaceutical, chemical, and oil and gas. There is an increasing emphasis on satisfying the requirements of specific applications related to hygiene, safety, and performance. These include contamination control, material compatibility, and traceability.

Common Failure Modes and Prevention

Several factors influence the reliability of industrial hoses. These include abrasion, kinking, swelling caused by chemical incompatibility, loose couplings, heat stress, and material degradation. To prevent unexpected failures, a preventive inspection program may include visual inspections and pressure testing. It can also encompass a thorough assessment of the coupling condition. This helps reduce downtime and improve overall operational safety.

Regional Analysis

The North America industrial hose market is anticipated to register substantial growth over the forecast period, owing to the high industrial production in the automotive, oil & gas, and chemical industries. Growing investments in automation, infrastructure development, and shale gas production are also contributing to the growing demand for high-performance hose systems. For instance, in 2023, the U.S. government passed the Bipartisan Infrastructure Law (BIL), which allocated USD 1.2 trillion in federal funds for transportation, energy, and climate infrastructure projects. A major portion of these funds has been allocated to state and local governments to enable large-scale development. Furthermore, regulations on workplace safety and emissions reduction are also driving demand for certified leak-proof hoses. Technological developments in hose technology and materials that improve their lifespans and maintenance requirements are also driving market growth. Companies in the North America industrial hose industry are also focusing on domestic manufacturing to ensure timely delivery and customization for end-use customers.

U.S. Industrial Hose Market Trends

The U.S. market is projected to witness substantial growth during the forecast period, owing to the country’s large-scale manufacturing and energy production base. The growing number of upgrades in public infrastructure and transportation systems is also fueling steady demand for heavy-duty hoses. The automotive sector, with its transition to the production of electric and hybrid vehicles, is also fueling the demand for thermal management and fluid transfer hoses. In addition, the U.S. food and pharmaceutical sectors demand FDA- and USP-compliant hose systems, thereby fueling the growth of specialized hoses.

Asia Pacific Industrial Hose Market Overview

The Asia Pacific market led with a revenue share of around 39% in 2025. This is because of the fast growth of industries, the development of manufacturing bases, and the growth of infrastructure projects in major economies. According to data from the National Bureau of Statistics of China, in 2025, the value added for the processing of food from agricultural and sideline products grew by 2.2% compared to the previous year. The textile industry grew faster by 5.1%. The production of raw chemical materials and chemical products grew substantially by 8.9%. The increasing trend reflects the continued growth and vitality of the Chinese manufacturing industry, making it a major manufacturing center in Asia. In addition, emerging nations like India, Vietnam, and Indonesia are heavily investing in the construction equipment, energy, and transportation sectors, thus increasing the demand for high-performance hoses. The region also has a strong local manufacturing base that provides competitively priced hose solutions to meet the local requirements. The rising use of modern agricultural practices and the growth of the food processing industry are increasing the demand for flexible and durable hose systems.

China Industrial Hose Market Outlook

China represented the highest revenue share in the Asia Pacific region in 2025, driven by high production in the automobile, construction, and chemical sectors. Large-scale investments in infrastructure development, such as urbanization and high-speed rail networks, remain key drivers of the heavy-duty hose system market. China’s status as a manufacturing powerhouse translates to large-scale production of hoses made of various materials, providing cost competitiveness and easy access to the product. China’s focus on automation and smart factory also provides opportunities for high-efficiency hose systems compatible with high-efficiency machines, ensuring its dominant market in the region.

Europe Industrial Hose Market Insights

The Europe industrial hose market is expected to grow at a significant rate during the forecast period. This is due to the rising investments in sustainable manufacturing and the imposition of stringent regulatory standards. Industries in Germany, France, and the UK are upgrading to environmentally compliant hose systems that have low leakage rates. The demand for specialty hoses in the pharmaceutical and food processing sectors is increasing due to the imposition of stringent EU hygiene and safety standards. The transition to renewable energy projects and the upgradation of water and wastewater treatment facilities are also contributing to the increasing adoption of chemically resistant hose solutions.

Key Players and Competitive Analysis

Technological developments, effective market expansion strategies, and joint ventures across major regions are driving the competitive landscape in the industrial hose industry. Industry analysis indicates a competitive environment focused on product differentiation through material development, performance enhancement, and adherence to industrial safety norms. Mergers and acquisitions, and subsequent integration, form the core of market consolidation and development of distribution channels across the globe. The joint ventures between the industrial hose market key players and the industrial equipment manufacturers are also accelerating the entry into the high-growth sectors such as oil & gas, food processing, and pharmaceuticals. The investments in the automation-compatible hose products and intelligent fluid transfer systems are also opening up new avenues for differentiation. The manufacturers are also concentrating on sustainable manufacturing processes. There is also a focus on lightweight and high-performance hose products to cater to the changing demands. The competitive environment is also becoming tougher due to the fast pace of industrialization. There is also the need for customized fluid-transfer solutions.

The competition is shifting to the scope of certifications, the extent of chemical compatibility, the speed of customization, the strength of distribution and assembly networks, and the availability of online monitoring capabilities. Companies that integrate innovative materials with fast specification assistance and reliable distribution networks are more likely to win repeat business in environments where downtime is costly.

List of Key Companies

- ALFA GOMMA Spa

- Bridgestone Corporation

- Colex International Ltd

- Continental AG

- Danfoss

- Gates Corporation

- HANSA-FLEX AG

- HBD Thermoid

- KANAFLEX

- Kuriyama Holdings Corporation

- Manuli Ryco group

- Parker Hannifin Corp

- Polyhose

- Semperit AG Holding

- Sumitomo Riko Company Limited

- THE YOKOHAMA RUBBER CO., LTD.

- Trelleborg Group

Industrial Hose Industry Developments

April 2025: Danfoss Power Solutions launched the Synflex by Danfoss 3TMH thermoplastic hydraulic hose. This is intended to improve performance in material handling machinery like telehandlers, boom lifts, and scissor lifts. According to the company, the hose provides improved durability with abrasion resistance up to 10 times higher than other hoses. This improves the lifespan of the hose and lowers maintenance costs.

September 2024: Gates Corporation launched an IoT-based smart hose monitoring system. The system includes pressure sensors, temperature monitoring, and cloud connectivity. The system allows predictive maintenance notifications. It lowers downtime by 35% and helps in scheduling preventive maintenance services for improved efficiency.

August 2024: Parker Hannifin Corp. expanded its production capacity for thermoplastic hoses in Ohio and Indiana. The company aims to meet the 6.8% CAGR growth in lightweight composite hoses. The product is intended for the automotive and precision machinery markets with improved performance and reliability.

February 2024: Gates introduced the Clean Master Plus hose platform, a new addition to its industrial hose range. It is created to perform in high-pressure applications and challenging industrial environments.

Industrial Hose Market Segmentation

By Material Type Outlook (Revenue USD Billion, 2021–2034)

- Rubber

- PVC

- Silicone

- Teflon

- Others

By Size Outlook (Revenue USD Billion, 2021–2034)

- Small Diameter

- Medium Diameter

- Large Diameter

By Media Type Outlook (Revenue USD Billion, 2021–2034)

- Water Suction and Discharge

- Air/Pneumatic

- Chemical Transfer

- Steam

- Oil and Fuel Transfer

- Food-Grade Fluids

By Reinforcement Outlook (Revenue USD Billion, 2021–2034)

- Textile-Braided

- Wire-Braided

- Wire-Spiral

- Composite Hoses

By Application Outlook (Revenue USD Billion, 2021–2034)

- Automotive

- Construction & Infrastructure

- Oil & Gas

- Pharmaceuticals

- Food & Beverages

- Water & Wastewater Treatment

- Mining

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Industrial Hose Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 15.84 billion |

|

Market Size in 2026 |

USD 17.06 billion |

|

Revenue Forecast by 2034 |

USD 31.22 billion |

|

CAGR |

7.8% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Current Sensor Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market for industrial hoses stood at USD 15.84 billion in 2025. It is projected to reach USD 31.22 billion by 2034.

The market is projected to account for a CAGR of 7.8% between 2026 and 2034.

Asia Pacific accounted for the largest market share in 2025. This is due to rapid industrialization and the expansion of manufacturing hubs in the region.

A few of the key players in the market include ALFA GOMMA Spa; Bridgestone Corporation; Colex International Ltd; Continental AG; Danfoss; Gates Corporation; HANSA-FLEX AG; HBD Thermoid; KANAFLEX; Kuriyama Holdings Corporation; Manuli Ryco group; Parker Hannifin Corp; Polyhose; Semperit AG Holding; Sumitomo Riko Company Limited; THE YOKOHAMA RUBBER CO., LTD.; and Trelleborg Group.

The rubber segment led the market in 2025. This is due to its strong resistance to abrasion, weathering, and high-pressure conditions.

The construction & infrastructure segment accounted for the largest revenue share in 2025. The segment is driven by rising global infrastructure investments in roads, buildings, and public utilities.

Selection is based on several factors. These include the type of media being transferred, operating pressure, and temperature range. End users also consider safety and the total cost of ownership.

An industrial hose is the flexible conduit used to transfer fluids or gases. Hose assembly includes the hose combined with end fittings and connectors.

Page last updated on:

Jul-2025

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements