Industrial Lubricants Market Share & Trends Analysis, 2026-2034

REPORT DETAILS

Market Statistics

Industrial Lubricants Market Overview

The industrial lubricants market was worth USD 57.05 billion in 2025. It is expected to grow at a CAGR of from 3.8% from 2026 to 2034. The market for industrial chemicals is growing due to the expansion of the manufacturing sector. It is also benefiting from the continuous need for efficient machinery maintenance.

Key Takeaways

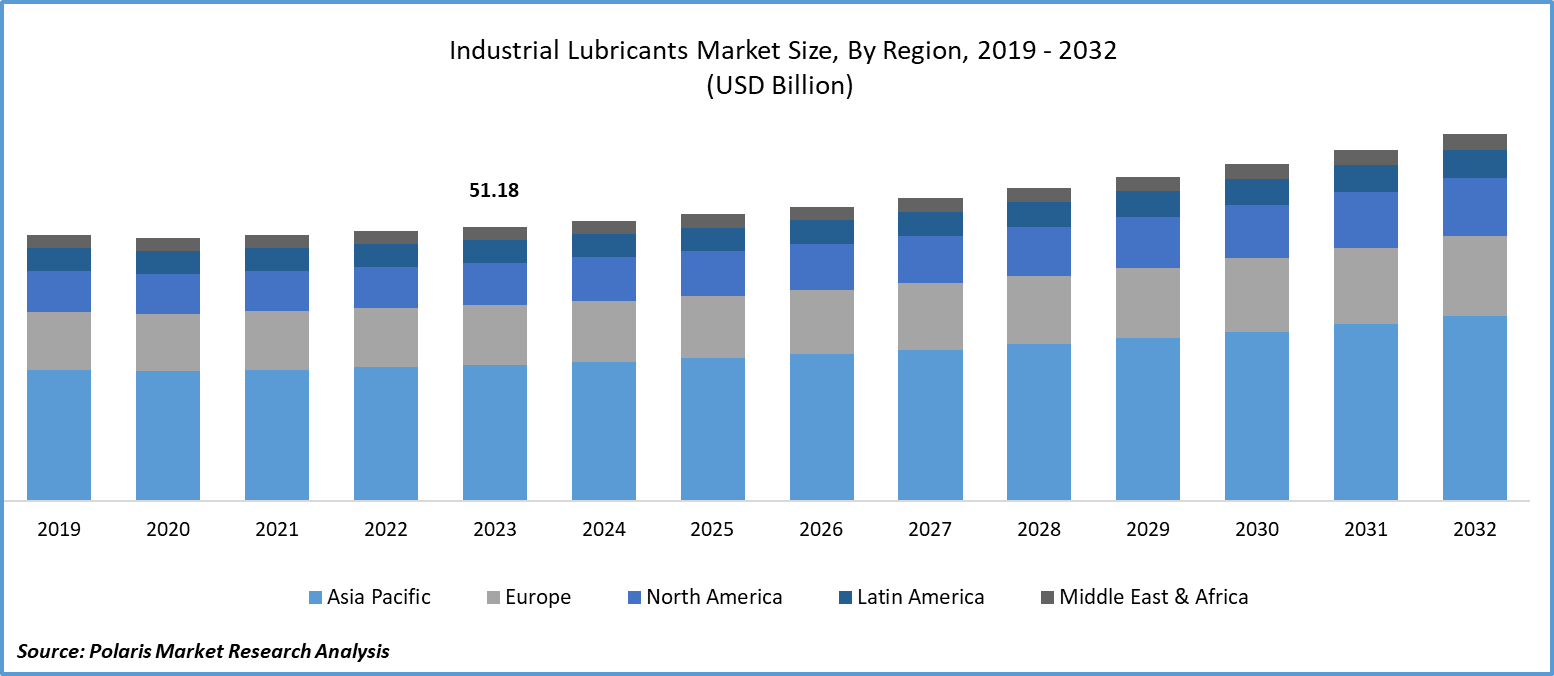

- Asia Pacific led the global industrial lubricants market in 2025. A strong demand for lubricants, particularly in the automotive sector in the region, is largely driven by the superior qualities of industrial lubricants.

- North America is expected to witness growth with a CAGR of 3.1%, during the forecast period. This is due to the steady expansion of manufacturing and heavy industry particularly the automotive and machinery industries

- In terms of product, the metalworking fluids segment is projected to record a significant CAGR during the forecast period. There has been a rising demand for precision machining, especially in medical devices and aerospace components. This has accelerated the adoption of advanced metalworking fluids. These industrial machining lubricants are increasingly engineered with multifunctional additives that improve cooling efficiency and corrosion resistance.

- The synthetic oil segment is expected to register the fastest CAGR among all based oils over the forecast period. Compared to mineral oils, synthetic industrial lubricants offer superior thermal stability and oxidation resistance. So, they are suitable for high-temperature and continuous-operation environments.

- The chemical manufacturing segment dominated the industrial lubricants market in 2025. Use of lubricants in these plants helps extend equipment lifespan and keep oil temperatures lower. They also help reduce friction, heat generation, wear, and energy consumption.

Market Statistics

- Market Size in 2025: USD 57.05 billion

- Projected Market Size in 2034: USD 78.41 billion

- CAGR, 2026–2034: 3.8%

- Largest Regional Market, 2025: Asia Pacific

Industry Dynamics

- Stringent sustainability regulations and energy efficiency are pushing industries such as construction and automotive towards high-performance lubricants that reduce friction and wear.

- The growing trend of rapid automation in the industry and the use of robotics in various manufacturing units are raising the demand for high-performance lubricants that can withstand high pressure, temperatures, and speed.

- The volatility in crude oil prices immediately reflects in the prices of raw materials used for industrial lubricants. This factor provides a severe price push for lubricant manufacturers and industrial buyers. Volatility may affect long-term supply contracts and procurement planning.

- The increasing adoption of predictive maintenance and condition monitoring systems creates great opportunities for smart lubricant systems integrated with sensors and AI-based analytics.

AI Impact on Industrial Lubricants Market

- Combining artificial intelligence (AI) with smart sensors in machines can automate the monitoring of lubricant conditions (viscosity, pollution, and oxidation) to check if they are structurally and functionally intact throughout their use.

- AI can be used to predict lubrication needs and prevent equipment degradation, thereby reducing the risks of downtime.

- In manufacturing units, AI tools can improve cost efficiencies by optimizing raw material sourcing, inventory management, and lubricant distribution operations, among others.

- AI can help create eco-friendly and longer-lasting lubricants. This enables compliance with regulations that ensure sustainability in industrial operations.

What are Industrial lubricants?

Industrial lubricants are used throughout the industrial lubricants value chain, from sourcing base oils and additives to formulation, blending, and final use in heavy machinery, processing equipment, and automated production systems. The industrial lubricants market moves in line with industrial investment cycles, the need to minimize downtime, and ongoing efforts to manage maintenance costs across sectors such as automotive manufacturing, chemical processing, power generation, and construction.

The market for industrial lubricants is driven by several factors. These include the growing manufacturing industry, particularly in automotive and general-purpose machinery. According to the India Brand Equity Foundation, India's manufacturing industry is set to reach USD 1 trillion in 2025-26. This is due to substantial growth in states like Gujarat, Maharashtra, and Tamil Nadu. The growth is mainly due to significant investment in sectors such as automotive and textiles. Government programs initiated in India, including Make in India and the Production-Linked Incentive (PLI) scheme, are key catalysts for this expansion, increasing foreign direct investment (FDI) and boosting the country's manufacturing industry. At the same time, sustainable and energy-conserving norms are pushing manufacturers to adopt high-performance lubricants to conserve energy and reduce friction.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

There has been an increased emphasis on predictive maintenance in industrial settings. This has increased the adoption of next-generation lubricants that improve machine efficiency and extend their lifespan. The shift towards automation and smart manufacturing across industries is also driving demand for lubricants that have strong high-temperature performance and can resist harsh conditions.

Industrial Lubricants Market Trends

Rising Usage in Construction and Automobile Industry

Market CAGR for industrial lubricants is being driven by the increasing demand for lubricants in the construction and automobile industries. The construction sector is the largest consumer of industrial lubricants. The increasing infrastructure development in emerging economies is expected to gradually boost demand for industrial lubricants. Hydraulic fluid is the preferred product type for lubricating heavy machinery in the construction sector. This is because it’s more cost-effective than other lubricants. Further, the automotive industry's growth has increased demand for industrial lubricants. These lubricants have several advantages for vehicles. They have high electrical resistance and can provide effective protection against corrosion. They also extend the lifespan of automotive components under demanding operational conditions. Additionally, the rise of electric vehicles has increased the demand for specialty chemicals and industrial lubricants for EV manufacturing.

Rapid Industrialization, Along with the Influence of Western Culture

The industrial lubricants market growth is expected to rise in the coming years, driven by rapid industrialization and increased trade, especially in developing countries. The growth of various industrial processes and increased investments in research and development (R&D) are supporting this expansion. Industries such as mining, chemicals, and unconventional energy are expected to see significant growth during this period. The demand for industrial lubricants in applications such as bearings, hydraulics, compressors, centrifuges, and industrial engines is also expected to increase as a result of these trends.

Moreover, the lifestyles of emerging nations have been significantly influenced by Western culture. There has been an increased demand for processed and frozen meals in recent years. This shift is expected to drive the growth of industrial lubricants, as many packaging industries are adopting automation and artificial intelligence to enhance production. Consequently, in the near future, the industrial lubricant market is projected to expand and become more integral to automation and robotics processing.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Insights

Industrial Lubricants Product Insights

The global industrial lubricants market segmentation, based on product, includes metalworking fluids, industrial engine oils, process oils, general industrial oils, and others. The metalworking fluids segment is projected to grow at a CAGR of 4.3%, during the industrial lubricants market forecast period. Their rising popularity stems from their ability to enhance surface finish quality. These fluids are used in specialized fields such as medical machining. To extend tool lifespan and reduce downtime, manufacturers often augment metal removal fluids with antioxidants and emulsifiers.

The process oils segment captured 17.5% recenue share of the industry in 2025. Process oils are versatile. They are used in tire production, rubber processing, and the processing of polymers. Process oils are manufactured to enhance the processing of materials. Their ease of flow and additive dispersability allow for the production of high-quality goods.

Industrial Lubricants Base Oil Insights

The global industrial lubricants market segmentation, based on base oil, includes bio-based oil, mineral oil, and synthetic oil. The synthetic oil segment is expected to grow at the fastest CAGR of 5.0% over the industrial lubricants market forecast period. Synthetic oils outperform traditional mineral oils in terms of performance. They have high viscosity index, oxidation resistance, and thermal stability. This results in increased equipment life and efficiency. Many industrial sectors, such as the automobile, manufacturing, and energy sectors, can employ synthetic lubricants. Their adaptability makes them a well-liked option in many sectors.

Industrial Lubricants Application Insights

The global industrial lubricants market segmentation, based on application, includes metalworking, textiles, energy, chemical manufacturing, food processing, and hydraulic. The chemical manufacturing segment held 11.4% revenue share in 2025. Chemical manufacturing and processing plants encounter various challenges, such as extreme temperatures, continuous operation, and the risk of contamination from particles, water, and chemicals. Using lubricants in these plants helps to extend lubricant and equipment lifespan, maintain lower oil temperatures, increase production output, reduce friction, heat, wear, and energy consumption, and extend oil drain intervals.

Chemical manufacturing requires high performance from lubricants due to interactions with aggressive chemicals, high operating pressure, and high operating temperatures. The increased complexity of chemical processing operations is contributing to the demand for chemically stable, high-temperature industrial lubricants.

The metalworking segment is expected to grow at the fastest CAGR of 3.9% during the industrial lubricants market forecast period. This segment’s growth will be driven by the increase in industrial activity and the demand for metal in construction and equipment applications. Additionally, the expansion will be fueled by the requirement for metalworking processes, including cutting, welding, and shaping, in various applications such as foundries, ships, airplanes, milling, and industrial machinery.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Use Cases of Industrial Lubricants Across Various Applications

| Industry Segment | Real-World Example | Equipment/Application | Industrial Lubricant Used | Purpose |

| Manufacturing | Steel plant rolling mill | Bearings, gearboxes, conveyor systems | Gear oils, bearing greases, circulating oils | Reduces friction, prevents wear, improves uptime |

| Injection molding factory | Hydraulic presses, molding machines | Hydraulic oils, compressor oils | Maintains hydraulic pressure and machine efficiency | |

| Cement plant | Kilns, crushers, grinding mills | High-temperature greases, industrial gear oils | Protects equipment under extreme heat and load | |

| Automotive | Vehicle assembly plant | Robotic arms, stamping presses, conveyors | Hydraulic fluids, chain oils, greases | Ensures smooth automation and reduces downtime |

| Engine manufacturing unit | CNC machines, machining centers | Metalworking fluids, spindle oils | Cooling, cutting efficiency, corrosion prevention | |

| Commercial vehicle fleet maintenance | Trucks, buses, diesel engines | Heavy-duty engine oils, transmission fluids | Engine protection and extended drain intervals | |

| Heavy Equipment | Construction site | Excavators, bulldozers, cranes | Hydraulic oils, chassis greases | Supports heavy load handling and reduces wear |

| Mining operations | Haul trucks, crushers, drilling machines | Extreme-pressure greases, gear oils | Withstands dust, shock loads, and harsh conditions | |

| Agricultural machinery | Tractors, harvesters, pumps | Engine oils, hydraulic fluids, multipurpose grease | Improves field performance and machine lifespan | |

| Power Generation | Wind turbines | Bearings, gearboxes | Synthetic gear oils, turbine oils | Minimizes maintenance and supports continuous operation |

| Marine & Ports | Port cranes and forklifts | Lifting systems, bearings | Hydraulic oils, open gear lubricants | Handles heavy-duty movement and corrosion resistance |

Source: Polaris Market Research Analysis

Industrial Lubricants Regional Insights

By region, the study provides market insights into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The Asia Pacific industrial lubricants market accounted for the largest market share of 43.8% in 2025 and is expected to maintain its dominance over the anticipated period. The region's industrial lubricants market is experiencing strong demand from key industries. This demand is largely driven by the superior qualities of industrial lubricants, such as enhanced performance, improved adhesion, protection against damage, and longer machinery lifespan, particularly in the automotive sector. In a notable contrast to the decline over the past three years, the China Association of Automobile Manufacturers (CAAM) has reported year-over-year increases in automotive production and sales, reaching 26.08 million and 26.27 million units, respectively. This growth is fueled by the rise in automobile production in key Asia-Pacific (APAC) regions, further driving the China industrial lubricants market.

Moreover, the Japan Automobile Manufacturers Association (JAMA) reported an increase in motor vehicle production in Japan, rising from 344,875 units in December 2019 to 360,103 units in January 2020. Furthermore, the expanding residential building and infrastructure development in the Asia Pacific region offer opportunities for market expansion. For instance, the Made in India campaign aims to attract USD 965.5 million in infrastructure investments for India by 2040. As a result, the booming demand for lubricants in automobile production, construction, and other industries across the Asia Pacific region is driving the expansion of the Indian industrial lubricants market. Because of THESE factors, the Asia Pacific represents the most significant geographical area for lubricant manufacturers during the forecast period.

Further, the major countries studied in the market report are the US, Canada, Germany, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, Brazil, and Others.

North America is expected to witness growth with a CAGR of 3.1%, during the forecast period. This is due to the steady expansion of manufacturing and heavy industry particularly the automotive and machinery industries, which is propelling demand for the North America industrial lubricants market. The rising need for high performance and energy efficient lubricants to enhance life of machineries also drives the market growth. Strict environmental norms are driving the use of bio-based and low-emission lubricants. Moreover, the industrial automation and maintenance requirements of dilapidated equipment also account for the steady growing market.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Industrial Lubricants Key Market Players & Competitive Insights

Leading market players are investing heavily in research and development in order to expand their product lines, which will help the industrial lubricants market, grow further. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, the industrial Lubricants industry must offer cost-effective solutions.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the global Industrial Lubricants industry to benefit clients and increase the market sector. In recent years, the industrial lubricants industry has witnessed some technological advancements. Major players in the industrial lubricants market include ExxonMobil Corp, Fuchs Group, The Lubrizol Corporation, Royal Dutch Shell, Phillips 66, Lucas Oil Products, Inc., Amsoil, Inc., Bel-Ray Co., Inc., BASF SE, Total Energies, Kluber Lubrication, Valvoline International, Inc., Chevron Corp., Clariant, and Quaker Houghton.

BASF SE is a chemical corporation that operates all over the world. It operates through seven segments, including chemicals, industrial solutions, materials, surface technologies, nutrition & care, agricultural solutions, and others. Petrochemicals and intermediates are provided in the chemicals section. Advanced materials and their precursors for applications such as isocyanates and polyamides are available through the Materials section, as well as inorganic basic products and specialties for the plastic and plastic processing industries. In January 2024, BASF and Lubrizol entered into a license agreement for the production and distribution of selected industrial lubricants.

Clariant is a manufacturer of specialty chemicals with three core business areas, including care chemicals, natural resources, and catalysis. The Care chemicals segment has a distinct focus on highly appealing, high-margin, and low-cyclicality categories, with around two-thirds of the business being consumer-facing in consumer care and industrial applications. This segment focuses on personal care, home care, crop solutions, paints & coatings, aviation, construction chemicals, and industrial lubricants. In September 2022, Clariant launched additives for fully synthetic metalworking fluids, enhancing efficiency, sustainability, and performance in aluminum cutting operations with biodegradable options.

List of Key Companies:

- Amsoil, Inc.

- BASF SE

- Bel-Ray Co., Inc.

- Chevron Corp.

- Clariant

- Exxonmobil Corp

- Fuchs Group

- Kluber Lubrication.

- Lucas Oil Products, Inc.

- Phillips 66

- Quaker Houghton

- Royal Dutch Shell

- The Lubrizol Corporation

- Total Energies

- Valvoline International, Inc.

Industrial Lubricants Industry Developments

May 2025: Petronas Lubricants International launched premium insulating oils with Glide Technology and co-branded Tutela Iveco technical fluids with Iveco. According to Petronas Lubricants, the move strengthened Malaysia’s energy infrastructure and expanded its long-standing OEM-lubricant partnership in the commercial vehicle segment. (Source: iveco.com)

June 2024: Castrol India Limited unveiled a range of products within the Castrol EDGE line. This advanced engine oil is designed for on-demand performance. It includes three new variants that are tailored for the passenger car segment. (Source: castrol.com)

Industrial Lubricants Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Metalworking Fluids

- Industrial Engine Oils

- Process Oils

- General Industrial Oils

- Others

By Base Oil Outlook (Revenue – USD Billion, 2021–2034)

- Bio-Based Oil

- Mineral Oil

- Synthetic Oil

- Group III (Hydro cracking)

- Polyalphaolefins (PAO)

- Polyalkylene Glycol (PAG)

- Esters

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Metalworking

- Industrial Heat Exchangers

- Metal Forming

- Metal Cutting

- Metal Joining

- Metalworking Electronics

- Others

- Textiles

- Textile Weaving

- Non-woven Textiles

- Textile Finishing

- Textile Composites

- Others

- Energy

- Transformers

- Pipelines

- Liquefied Natural Gas (LNG)

- Ocean Energy

- Others

- Chemical Manufacturing

- Industrial gases

- Fertilizers

- Polymers

- Others

- Food Processing

- Beverages

- Frozen Food

- Canned Food

- Processed Potatoes

- Bakery

- Cocoa & Chocolate

- Others

- Hydraulic

- Compressors

- Bearings

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Industrial Lubricants Market

The industrial lubricants market is expected to grow steadily. Rising industrial automation and expanding manufacturing activities would boost the growth. Also, increasing demand for equipment efficiency across sectors such as automotive, construction, mining, and power generation will propel lubricant demand. The shift toward synthetic and bio-based lubricants is expected to offer lucrative opportunities. Also, the rising demand for predictive maintenance technologies and sustainability-focused operations will drive long-term market expansion.

Industrial Lubricants Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 57.05 billion |

| Market Size in 2026 | USD 58.40 billion |

| Revenue Forecast by 2034 | USD 78.41 billion |

| CAGR | 3.8% |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Industrial Lubricants Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Industrial Lubricants Market FAQ's

Growing manufacturing sector, automation, stringent sustainability standards, and increasing demand from automotive and construction segments are propelling the market.

The Asia Pacific market leads with the largest market share, particularly due to a well-developed automobile production industry in emerging countries.

Examples of industrial lubricants include metalworking fluids, industrial engine oils, process oils, and general industrial oils.

Synthetics possess greater viscosity, more resistance to oxidation, thermal stability, and longer equipment life than mineral oils.

The industrial lubricant market is expected to reach USD 78.41 billion by 2034, growing at a CAGR of 3.8% from 2026 to 2034.

The synthetic oil is expected to grow at fastest CAGR in the industrial lubricants market.

Download Sample Report of Industrial Lubricants Market

Please fill out the form to request a customized copy of the research report.