Overview

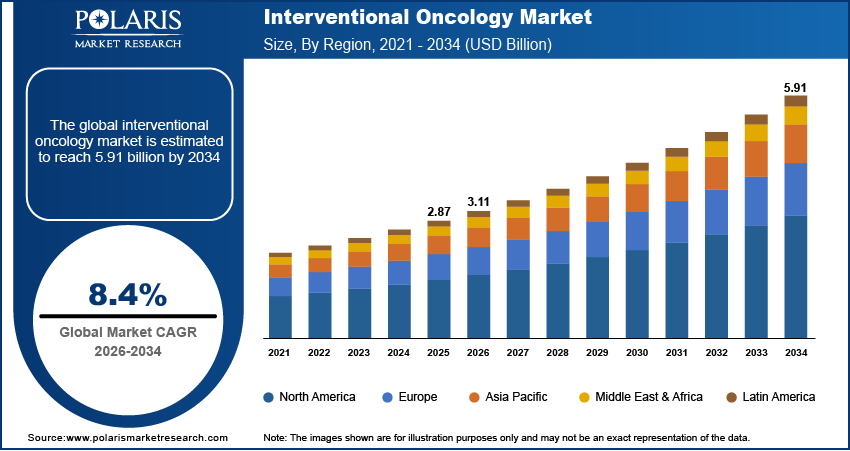

The global interventional oncology market is estimated around USD 2.87 billion in 2025, with consistent growth anticipated during 2026–2034. The market is projected to grow at a 8.4% CAGR during the forecast period due to the rising global cancer burden and procedural demand expansion coupled with shift toward minimally invasive cancer treatment pathways.

Future Demand Scenarios

- Base scenario: Demand grows steadily as minimally invasive oncology procedures expand and hospital adoption increases.

- Upside scenario: Faster uptake of advanced ablation, embolization, and AI-guided platforms accelerates market growth.

- Conservative scenario: Capital constraints, reimbursement pressure, and specialist shortages slow adoption beyond major centers.

Key Insights

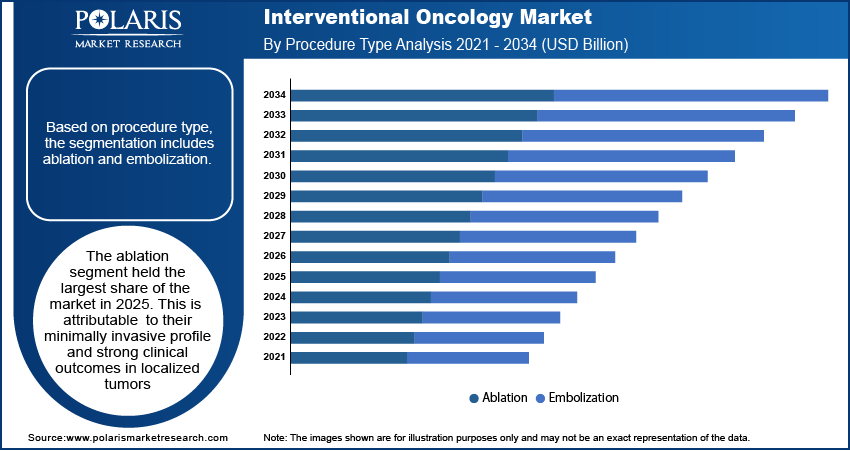

- The ablation segment held the largest share of the market in 2025 supported by their minimally invasive profile and strong clinical outcomes in localized tumors.

- Embolization consumables are key product segment, with improved particle design, drug-eluting beads, and catheter precision expanding use across liver-dominant and metastatic cancers.

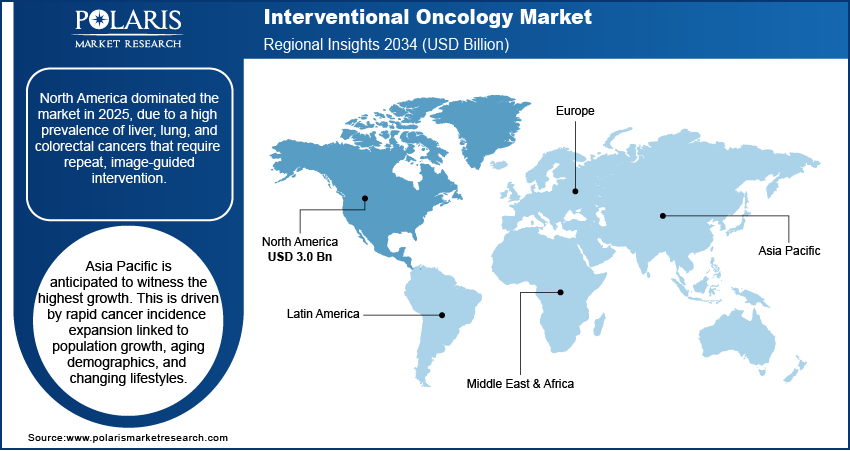

- North America dominated the market in 2025 due to a high prevalence of liver, lung, and colorectal cancers that require repeat, image-guided intervention

- Asia Pacific is anticipated to witness the highest growth. This is driven by rapid cancer incidence expansion linked to population growth, aging demographics, and changing lifestyles.

Industry Dynamics

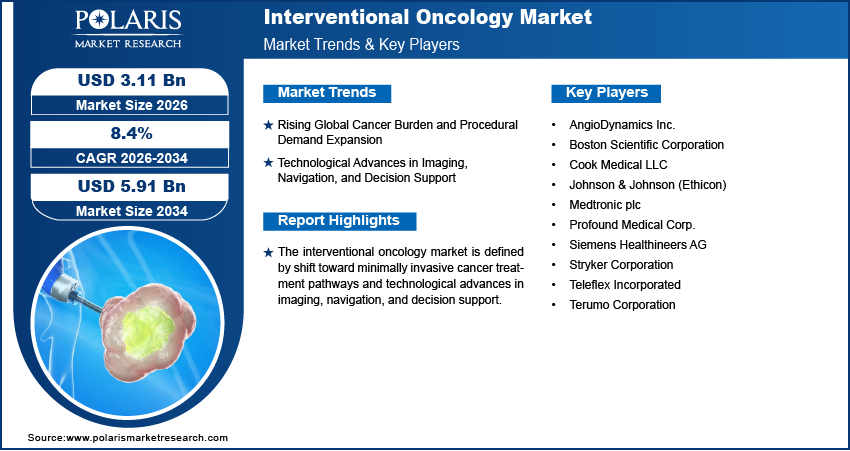

- Rising Global Cancer Burden and Procedural Demand Expansion

- Shift Toward Minimally Invasive Cancer Treatment Pathways

- Limited Availability of Trained Specialists are Restraining Market

- AI-Guided Planning and Precision Oncology Creating Opportunities

Market Statistics

- 2025 Market Size: USD 2.87 billion

- 2034 Projected Market Size: USD 5.91 billion

- CAGR (2026-2034): 8.4%

- North America: Largest market in 2025

What Is Interventional Oncology and Why It Matters

Interventional oncology is a specialized branch of cancer care focused on minimally invasive oncology treatments delivered through real-time imaging. It represents the confluence of oncology, radiology, and procedural medicine, where visual precision is translated directly into therapeutic intervention. By using image guidance, it is possible to precisely target cancer while sparing as much tissue as possible around it, and this makes it possible to achieve shorter recovery times and inclusive treatment criteria, and it also meshes very well with systemic cancer treatments.

Procedures and Technologies Included in This Market

- The market covers core interventional oncology procedures using catheter-based systems, percutaneous tools, and imaging guidance.

- Tumor ablation therapy is central, applying thermal, cryogenic, or electrical energy for precise tumor destruction.

- Embolization procedures form a major pillar, focused on cutting off tumor blood supply through targeted vascular access.

- Key techniques include transarterial chemoembolization (TACE), transarterial radioembolization (TARE), and tumor embolization.

- Image-guided biopsies appear in a supporting role within image-guided cancer therapy, aiding diagnosis and planning.

- Together, these approaches define minimally invasive oncology as a precision-driven, localized cancer treatment model.

Drivers & Opportunities

Rising Global Cancer Burden and Procedural Demand Expansion

Cancer incidence growth triggers demand for care associated with localized control of tumors in liver, lung, kidney, and bone applications. As estimated in a World Health Organization report, there is estimated over 35 million new cases of cancer expected by 2050, reflecting a 77% increase over 20 million in 2022. This disease demand on the healthcare community structures their practice around those treatments that are repeated, focused, and performed on an outpatient basis. It leads to the development of interventional cancer care service lines in facilities that address their case volumes effectively. Thus, interventional cancer care market drivers are directly shaping demands for interventional equipment and therapeutic processes despite challenges in current reimbursement structures.

Shift Toward Minimally Invasive Cancer Treatment Pathways

Physician preference and patient outcomes propel the demand for more minimally invasive approaches for the treatment of cancers based on the reduction of trauma, recovery time, and the need for hospitalization. This trend led to increasing usage of catheter therapy, percutaneous ablation, and localized drug delivery. The medical benefits lie in the repeatability of procedures with known risk profiles. Hospitals imbed such procedures for optimal utilization of the available beds. Demands lie in small interventional systems ideally designed for the hybrid operating rooms, which improves the prospect for interventional oncology.

Technological Advances in Imaging, Navigation, and Decision Support

Enhanced real-time imaging and navigation tools enhance the precision of procedures and enable the treatment of new patients. This is due to fusion biopsy and cone beam CT involve higher accuracy in targeting lesions, particularly in complex procedures. GE HealthCare introduced its lineup of advanced imaging solutions developed using the NVIDIA technology platform during the RSNA 2025 Annual Meeting. AI-driven interventional procedures improve the accuracy and rapidity of analysis and decision-making in delivering treatments. Variability is removed by AI, enabling greater confidence in treatment decisions. Hospitals continue to make investments in improved platforms to deliver standardized outcomes and enhance the portfolio for cancer care.

Restraints & Challenges

Limited Availability of Trained Specialists

The supply of trained interventional oncologists remains constrained, while procedural demand continues to rise alongside cancer incidence growth. This creates a bottleneck for the adoption of procedures within hospitals. The availability of qualified operator talent limits the scope of procedures, leading to their concentration in large tertiary hospitals. The implication for the industry is the varied adoption of minimally invasive cancer procedures, which reduces the adoption rate for the technology.

High Capital Equipment Costs

Interventional oncology relies on advanced imaging systems, catheter platforms, ablation generators, and radiation-shielded infrastructure, creating high upfront capital requirements. The medical facilities are under pressure to spend their budget and therefore are forced to space their expenditures or opt for devices suited for use in other facilities rather than focused on oncology. The interventional oncology market drivers are therefore influenced by the longer period involved for customers to purchase devices..

Emerging Opportunities

AI-Guided Planning and Precision Oncology

AI developments in the field of interventional oncology are transforming the aspects of procedure planning, target accuracy, and decision-making during procedures. AI-assisted image analysis can result in improved tumor segmentation, optimal catheter placement strategies, and reliable ablation margins. This will normalize the procedural variabilities and increase the adoption of AI technology by new sites. This will trigger growing demands for AI-supported imaging systems, navigation systems, and intelligent devices.

Technology & Procedure Landscape

-

Tumor Ablation Technologies

Tumor ablation remains a core pillar of interventional oncology, enabling localized tumor destruction through percutaneous, image-guided access. Ablation tools in tumor ablation are designed to handle multiple forms of energy based on the size, location, and vascular nature of the target neoplasm. The radiofrequency ablation market under the categories of predictable heating and economics is responsible for the widespread adoption of the technology in liver and renal metastases. The microwave ablation market in cancer, driven by faster heating and larger ablation margins, leads to the increased adoption in the ablation of larger or well-perfused lesions and subsequently drives the sales of microwave antennas and generators. Cryoablation in cancer requires the process of freezing and thawing.

-

Embolization-Based Interventions

Embolization procedures target tumor vasculature rather than tissue directly, reshaping blood flow to suppress tumor growth. The TACE market revolves around localized delivery of medications with an embolization component. TARE radioembolization involves selective radiation delivery via microspheres. These microspheres make it feasible for the chronic use of radioembolization in the context of liver-dominant disease. The purpose of bland embolization (TAE) revolves around the mere physical blockage of vessels without an overt need for sophistication and reproducibility. The demand for all types of procedures persists with the volume of embolization product demand.

-

Imaging, Navigation & AI Integration

The imaging solutions turn procedural intent into precise execution. The image-guided cancer treatment solutions combine CT imaging, fluoroscopy, cone beam CT imaging, and ultrasound to enable targeting, guiding, and verifying cancer treatment. The use of cancer treatment software enables efficiency in procedures, while AI solutions are changing planning precision.

Imaging, Navigation & AI - Technology Impact

|

Technology Component |

Functional Role |

Market Impact |

|

Advanced imaging platforms |

Real-time visualization and targeting |

Higher capital equipment demand |

|

Navigation software |

Improved accuracy and workflow efficiency |

Increased software adoption and upgrades |

|

AI-based planning tools |

Enhanced lesion mapping and margin control |

Rising demand for AI-enabled systems |

|

Integrated procedure suites |

Standardized interventional workflows |

Greater system utilization and repeat purchases |

Segmental Insights

This report provides granular coverage of the Interventional Oncology market by product type, procedure type, cancer type, end user, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Product Type

-

Devices

Devices accounted for the largest share of the interventional oncology devices market in 2025. Image-guided ablation systems, embolization delivery platforms, and navigation-enabled catheters form the procedural core of interventional oncology workflows. Capital-intensive procurement, long replacement cycles, and procedure dependency reinforce device dominance. Even marginal upgrades in imaging precision or energy control translate into measurable gains in tumor targeting accuracy, sustaining device-led revenue concentration.

-

Consumables

Consumables represent the fastest-growing product segment due to per-procedure usage intensity. Ablation probes, embolic agents, guidewires, and microcatheters are consumed with every intervention, creating recurring demand. Growth accelerates as procedure volumes rise and as oncology embolization procedures expand into broader indications. Short shelf lives and protocol-driven replacement further strengthen this trajectory.

-

Accessories

Accessories play a supporting role, including imaging disposables, introducers, and procedural kits. While it contributes lower value, accessories scale directly with procedure throughput and institutional adoption of standardized intervention kits.

By Procedure Type

-

Ablation

Ablation procedures held the leading share, fueled by their minimally invasive nature and success rates for localized cancers. The ablation procedure for liver cancer emerges as the highest adopter due to easy access, visibility, and high success rates for managing frequent recurrences.

-

Embolization

Embolization is the fastest-growing procedure segment. Improvements in the use of particles and the precision of the catheter have led to an increased use of embolizations in cancer. The fact that embolization are done alongside systemic treatment only adds to its attractiveness.

Ablation vs Embolization

|

Procedure |

Market Position |

Treatment Approach |

Cancer Suitability |

Primary Growth Driver |

|

Ablation |

Largest segment |

Localized, lesion-specific tumor destruction |

Liver, lung, kidney (small, well-defined tumors) |

Preference for minimally invasive, repeatable local control |

|

Embolization |

Fastest-growing segment |

Vascular-targeted tumor ischemia |

Liver-dominant and hypervascular tumors |

Expanding indications and combination therapy use |

By Cancer Type

-

Liver

Liver cancer comprises the largest market share. The anatomical acceptability, dual blood supply, and preponderance of inoperable cases make the liver the chief organ on which ablation and embolization will target. The compatibility of tumor behavior with image-guided interventions maintains their dominance.

-

Lung

The uses for lung cancer therapy continue to grow with the increased precision and reduced peri-procedural risk. There are improvements in imaging, tracking, and management of the normal respiratory motion, making the target more accurate with less chance for complications. The main condition for percutaneous ablation is patients who are unresectable for surgery and radiation oncology therapy.

-

Kidney

Renal cancers are responsive to local ablation techniques, especially with small, localized tumors. The preference for nephron-sparing techniques, keeping in mind preserving renal functions, helps to increase adoption. Lower morbidity associated with these techniques and shorter recovery periods make them preferable in comorbid patients with limited surgical risk tolerance.

-

Bone

Bone applications, mainly, target metastatic diseases, with aims of alleviating pain, shrinking tumor tissue, and stabilizing affected structures. Bone applications are usually implemented within frameworks of palliative treatments, excluding curative approaches. Use is still associated with increased survival incidence of cancer, an important factor for bone metastases presentation.

-

Others

Other cancer types include adrenal, pancreatic, soft tissue, and selected gastrointestinal tumors. Interventional oncology use in these indications depends heavily on anatomical feasibility and procedural risk. Adoption remains selective but is gradually expanding as device precision improves and operator experience increases.

Interventional Oncology Market - Cancer Type Segment Analysis

|

Cancer Type |

Market Position |

Clinical Suitability |

Typical Procedures |

Clinical Outcome Logic |

|

Liver |

Largest |

High accessibility; dual blood supply; high unresectable rates |

Ablation, embolization |

Repeatable local control with limited liver function impact |

|

Lung |

Medium |

Peripheral lesions; improving motion control |

Ablation |

Local tumor control with minimal pulmonary compromise |

|

Kidney |

Medium |

Small, localized tumors; nephron-sparing priority |

Ablation |

Tumor control while preserving renal function |

|

Bone |

Low–Medium |

Metastatic focus; palliative intent |

Ablation, cementoplasty |

Pain reduction and structural stabilization |

|

Others (adrenal, pancreatic, soft tissue) |

Low |

Case-specific anatomical feasibility |

Ablation, selective embolization |

Selective control in high-risk surgical cases |

By End User

-

Hospitals

Hospitals account for the largest share of hospitals interventional oncology procedures. They are dominating the market due to their access to advanced imaging infrastructure, multi-disciplinary oncology teams, intensive care backup, and alignment in reimbursement. Complex embolization and combination procedures require safety and the integration of workflow in a hospital-based setting.

-

Specialty Clinics

Specialty clinics offer focused oncology interventions, the majority are outpatient ablations in selected patient populations; adoption typically depends on the availability of imaging and integration into larger care networks.

-

Ambulatory Surgical Centers (ASCs)

Ambulatory Surgical Centers oncology procedures represent the fastest-growing end-user segment. Shorter recovery times, procedural standardization, and cost containment drive the migration of selected ablation cases into ASCs. Growth remains constrained to low-risk, well-defined interventions but continues to accelerate as technology simplifies procedural execution.

End-User Segment Analysis

|

End User |

Market Share Ranking |

Fastest-Growing Indicator |

Key Driver |

|

Hospitals |

High (Largest) |

No |

Advanced imaging access and multidisciplinary oncology care |

|

Specialty Clinics |

Medium |

No |

Outpatient-focused interventional workflows |

|

Ambulatory Surgical Centers (ASCs) |

Low–Medium |

Yes |

Cost-efficient settings for low-risk ablation procedures |

Regional Analysis

North America Interventional Oncology Market Assessment

North America dominated the market in 2025, due to a high prevalence of liver, lung, and colorectal cancers that require repeat, image-guided intervention. The American Cancer Society estimates that approximately 154,000 new colorectal cancer cases to be diagnosed in the US in 2025. This disease burden increases procedural volumes and sustains demand for ablation, embolization, and catheter-based systems. The adoption environment is supported by advanced hospital infrastructure and favorable reimbursement frameworks that recognize minimally invasive oncology procedures. Strong clinician familiarity and established referral pathways accelerate uptake across academic hospitals and specialty oncology centers.

Asia Pacific Interventional Oncology Market Insights

Asia Pacific is anticipated to witness the highest growth. This trend is fueled by the fast growth in cancer cases, exacerbated by increasing population, aging, and lifestyle factors. According to the World Health Organization, the number of persons aged 60 years and over globally is likely to double to 2.1 billion in 2050, and those aged 80 years and over will see their numbers triple to 426 million in 2050, from the level in 2020. This puts strain on surgical capacity, thereby propelling the shift to minimally invasive procedures. There has been direct investment in oncology facilities in China, India, Japan, and South Korea to provide access to high-quality imaging suites and hybrid operating suites.

Europe Interventional Oncology Market Overview

Europe growth in the interventional oncology market is due to the focus on cost-effective treatment options within public healthcare infrastructure. Cost control measures lead to an increase in the demand for procedures that decrease hospital stays and surgical interventions. Interventional oncology also satisfies this criterion, which offers targeted treatment options with guaranteed recovery periods. The development of comprehensive cancer screening programs ensures earlier diagnosis, hence qualifying more people for image-guided interventions.

Latin America and Middle East & Africa Interventional Oncology Market Insights

Latin America and the Middle East & Africa fall within emerging oncology markets where access and awareness define adoption pace. This is driven by awareness and access. Slowly, there is improvement in infrastructure related to oncology care that enables procedures. More physicians are exposed to minimal invasiveness procedures related to cancer treatment, which boosts adoption.

Heat Map Analysis

|

Region |

Market Status |

Cancer Burden |

Infrastructure & Reimbursement |

Adoption of Minimally Invasive Procedures |

Technology Penetration (Imaging, Navigation, AI) |

Growth Momentum |

|

North America |

Dominant |

High |

Very High |

Very High |

Very High |

Medium–High |

|

Asia Pacific |

Fastest Growing |

Very High |

Medium–High |

High |

Medium–High |

Very High |

|

Europe |

Mature |

High |

High |

High |

High |

Medium |

|

Latin America |

Emerging |

Medium–High |

Medium |

Medium |

Low–Medium |

Medium |

|

Middle East & Africa |

Emerging |

Medium |

Low–Medium |

Low–Medium |

Low |

Medium–Low |

Key Players & Competitive Analysis Report

The interventional oncology market is moderately competitive, with the competitive landscape interventional oncology shaped by continuous innovation across ablation systems, embolization technologies, and imaging-integrated platforms. Leading interventional oncology market players are focusing on frequent product launches, strategic partnerships with hospitals and cancer centers, and geographic expansion to strengthen clinical adoption. The key competitors among the interventional oncology firms and the established companies involved in the oncology devices sector are in the improvement of procedural accuracy, workflow, and outcomes, coupled with the expansion of their product offerings for the support of minimally invasive cancer treatment for various types of tumors.

Key players operating in the global interventional oncology market include AngioDynamics Inc., Boston Scientific Corporation, Cook Medical LLC, Johnson & Johnson (Ethicon), Medtronic plc, Profound Medical Corp., Siemens Healthineers AG, Stryker Corporation, Teleflex Incorporated, and Terumo Corporation.

Key Players

- AngioDynamics Inc.

- Boston Scientific Corporation

- Cook Medical LLC

- Johnson & Johnson (Ethicon)

- Medtronic plc

- Profound Medical Corp.

- Siemens Healthineers AG

- Stryker Corporation

- Teleflex Incorporated

- Terumo Corporation

Future Outlook & Premium Insights – Interventional Oncology Market

Key Trends Shaping the Next Decade

The interventional oncology market trends signal a decisive shift toward precision-led procedures, tighter care pathways, and capital-efficient delivery models. Technology, reimbursement logic, and site-of-care economics are converging. The future of interventional oncology favors repeatable outcomes, faster throughput, and scalable access, anchored by precision oncology technologies that translate imaging data into procedural certainty. The oncology market outlook therefore tilts toward platforms and programs that compress time, reduce variability, and extend reach beyond tertiary centers.

|

Trend / Development |

What to Monitor |

Potential Market Impact |

|

AI-driven precision targeting |

Adoption of AI-assisted planning, targeting accuracy, margin assessment |

Higher utilization of advanced imaging, navigation software, and smart disposables |

|

Combination therapies (IO + systemic) |

Protocols pairing IO with immuno-oncology or targeted drugs |

Increased procedure frequency per patient and sustained device demand |

|

Outpatient shift economics |

Migration from inpatient suites to ambulatory settings |

Broader site adoption, faster capital payback, higher procedure volumes |

|

Emerging market infrastructure buildout |

New interventional suites, training pipelines, reimbursement expansion |

Accelerated platform sales and consumables pull-through |

Analyst Insights & Strategic Implications

- AI-enabled workflows elevate consistency and shorten learning curves, which supports faster program scale-up across hospitals.

- Combination regimens anchor interventional oncology deeper into care pathways, lifting repeat procedures and consumables usage.

- Outpatient economics favor compact systems and standardized kits, shifting procurement criteria toward throughput and uptime.

- Infrastructure expansion in emerging markets widens the addressable base for imaging platforms, ablation systems, and embolization tools.

- Vendors aligned to precision, efficiency, and access stand to capture durable growth as interventional oncology consolidates its role in modern cancer care.

Industry Developments

- September 2025: Canon Medical Systems launched the Alphenix 4D CT integrated with Aquilion ONE / INSIGHT Edition, a next-generation Angio-CT interventional imaging solution showcased at CIRSE 2025. The technology allowed for the integration of high-precision angiography and volumetric CT in the same suite.

- September 2024: RenovoRx expanded production of its FDA-cleared RenovoCath delivery system in response to strong demand from oncology and interventional radiology physicians. The increased number of the RenovoCath Delivery System units facilitated the commercial launches in the interventional oncology space, as the device is employed in the treatment of cancer in the hepatic region.

Interventional Oncology Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Devices

- Consumables

- Accessories

By Procedure Type Outlook (Revenue, USD Billion, 2021-2034)

- Ablation

- Embolization

By Cancer Type Outlook (Revenue, USD Billion, 2021-2034)

- Liver

- Lung

- Kidney

- Bone

- Others

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Hospitals

- Specialty clinics

- Ambulatory Surgical Centers (ASC)

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Interventional Oncology Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 2.87 Billion |

|

Market Size in 2026 |

USD 3.11 Billion |

|

Revenue Forecast by 2034 |

USD 5.91 Billion |

|

CAGR |

8.4% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 2.87 billion in 2025 and is projected to grow to USD 5.91 billion by 2034.

The?North America region holds the largest share in the interventional oncology market, due to a high prevalence of liver, lung, and colorectal cancers that require repeat, image-guided intervention.

Devices represent the primary product segment in interventional oncology, as image-guided ablation systems, embolization platforms, and navigation-enabled catheters form the core of procedural workflows.

A few of the key players in the market are AngioDynamics Inc., Boston Scientific Corporation, Cook Medical LLC, Johnson & Johnson (Ethicon), Medtronic plc, Profound Medical Corp., Siemens Healthineers AG, Stryker Corporation, Teleflex Incorporated, and Terumo Corporation.

Key factors include rising global cancer burden and procedural demand expansion coupled with technological advances in imaging, navigation, and decision support.

Page last updated on:

Dec-2025

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements