Global Lactose Free Butter Market Size, Share Analysis Report, 2025-2034

REPORT DETAILS

Market Statistics

What is the lactose free butter market size?

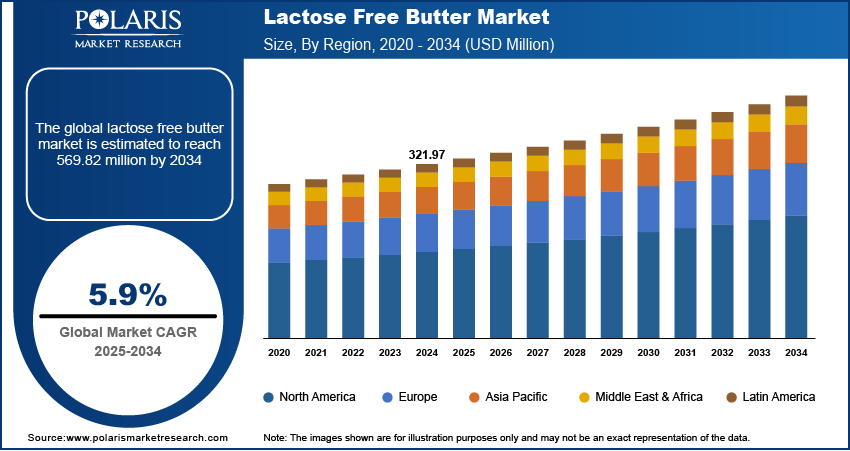

The global lactose free butter market was valued at USD 321.97 million in 2024 and is expected to grow at a CAGR of 5.9% during the forecast period. The rapidly emerging veganism trend and surge in the people’s expenditure for such plant-based products and significant inclinations towards the clean-label food including that includes organic, non-GMO, and gluten-free coupled with the growing product availability on various e-commerce platforms, as companies are exploring the ways to expand their customer base and market reach they are making their products online available, which are among the key factors boosting the market growth.

- For instance, in April 2022, Fonterra, introduced carbon zero butter under its brand “Anchor Dairy”, is audited through the Toitu Envirocare. The newly developed butter is a certified through USDA organic, non-GMO, and is also free from various synthetic fertilizers, antibiotics, pesticides, and hormones.

Key Insights

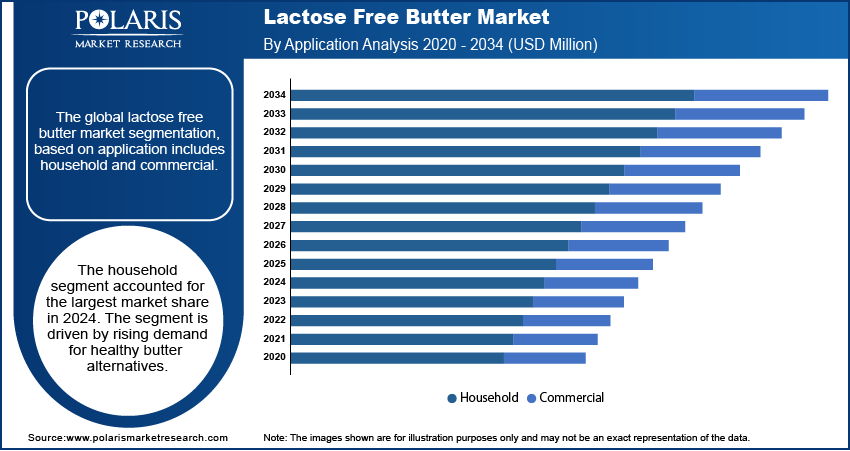

- The household segment accounted for the largest market share in 2024. The segment is driven by rising demand for healthy butter alternatives.

- The retail or household sector held a significant market share in 2024. This is supported by rising health-conscious consumers and availability of lactose-free options in convenience store.

- Online retail stores segment is expected to witness the highest growth during the forecast period. This is driven by expanding e-commerce platforms and consumer preference for convenient, doorstep dairy product delivery.

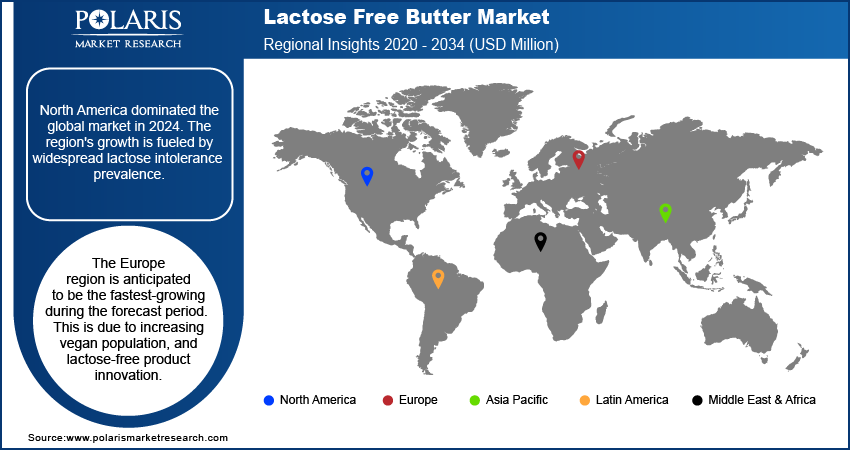

- North America dominated the global market in 2024. The region's growth is fueled by widespread lactose intolerance prevalence.

- The Europe region is anticipated to be the fastest-growing during the forecast period. This is due to increasing vegan population, and lactose-free product innovation.

Industry Dynamics

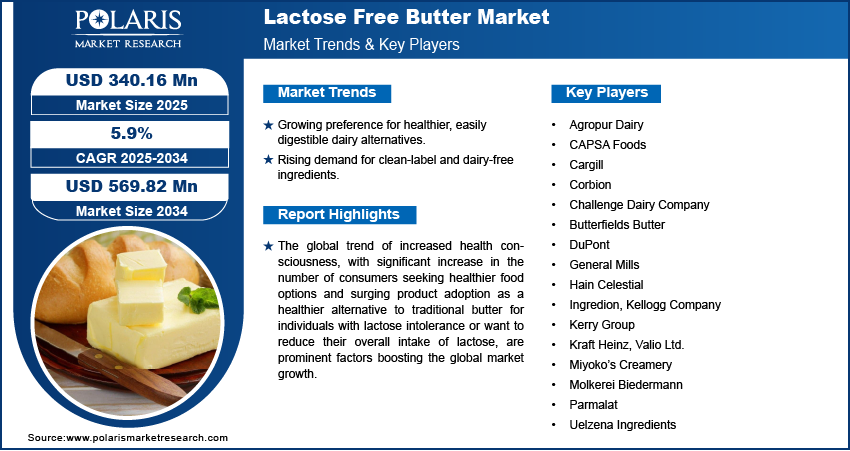

- The market is driving due to growing preference for healthier, easily digestible dairy alternatives.

- The market is boosting due to increasing demand for clean-label, natural, and dairy-free ingredients.

- Continuous innovations in food processing technologies and formulation improvements are creating new opportunities in the market.

- High production costs of lactose-free products and limited consumer awareness are the major restrains for the market.

Market Statistics

- 2024 Market Size: USD 321.97 Million

- 2034 Projected Market Size: USD 569.82 Million

- CAGR (2025–2034): 5.9%

- North America: Largest Market Share

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Moreover, surging proliferation for personalization and customization among the major companies and rising number of brands offering personalized lactose-free butter options, allowing consumers to choose specific flavors, ingredients, or even create their own custom blends that caters to individual preferences and provides a unique and tailored experience for consumers is likely to boost the global market.

However, the limited availability of the product and higher price point as compared to traditional butter coupled with the limited awareness regarding the incidence of lactose intolerance mainly in medium and low-income countries, are major factors restraining the market growth.

Industry Dynamics

Which factors are driving the lactose free butter market growth?

Growth Drivers

Rising awareness regarding health & wellness among the people

There is a rising awareness and emphasis among consumers globally on health and wellness and increasing number of individuals are becoming more conscious of their dietary choices and are actively seeking healthier options along with the rising demand for allergen-free products including lactose free butter and prevalence as a healthier alternative to the traditional butter mainly for people with lactose intolerance, are among the major factors driving the demand and growth of the market.

Furthermore, several large manufacturers across the globe have been investing heavily in research and development of lactose free butter to improve the taste, texture, and quality and are bringing innovations in manufacturing processes and ingredient formulations, resulting in significant improvements in product and are likely to influence the growth of the market in a positive way.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Report Segmentation

The market is primarily segmented based on application, end-use, distribution channel, and region.

| By Application | By End-Use | By Distribution Channel | By Region |

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

By Application Analysis

Household segment accounted for the largest market share in 2024

The household segment accounted of global market share in 2024, and is likely to retain its market position throughout the forecast period, on account of growing incidences of lactose intolerance among general population and residences across the globe leading to higher demand for lactose-free butter along with the rapid surge in product demand across several industrialized or developing economies because of the rising per capita consumer spending of food products.

The commercial segment is likely to be the fastest growing region with a healthy CAGR during the anticipated period, which is mainly attributed to growing developments and improvements in commercial food applications of lactose free butter including restaurants, hotels, colleges, schools, and catering services among others. The growing establishments of food service industry which often cater to customers with dietary restrictions and preferences including lactose intolerance and introducing lactose-free options on their menus, is among a key major trend influencing the market.

By End-Use Analysis

Retail or household sector held the significant market share in 2024

The retail or household sector held the maximum market share in terms of revenue in 2024, which is largely accelerated by growing awareness about lactose intolerance among consumers globally and surge in the adoption of these butter as an attractive alternative to conventional butter, as it offers a suitable option for individuals looking to reduce their lactose intake while still enjoying butter. In addition, the widespread availability of lactose free butter in retail stores and increasing prevalence of favorable policies supporting the use of vegan products, is positively contributing the market growth over the years.

The food industry segment is expected to gain substantial growth rate over the course of study period, mainly due to continuous expansion of global population and number of consumers seeking for vegan or plant-based products to reduce the dependence on dairy products for their body requirements. Hence, many individuals are actively seeking out lactose-free alternatives to cater to their dietary restrictions, which is likely to create a huge demand for lactose-free butter in the near future.

By Distribution Channel Analysis

Online retail stores segment is expected to witness highest growth during forecast period

The online retail stores segment is projected to witness highest growth rate during the anticipated period, which is mainly attributable to increasing number of online shoppers across the globe and rising penetration for smartphone or fast internet facilities, encouraging consumers to opt for online shopping channels due to their numerous beneficial features including convenience, easy accessibility, variety of choices, products from different brands, convenient payment methods, and free home delivery among others.

For instance, according to our findings, the number of online shoppers were around 268 million in 2022 in the United States, which is projected to reach almost 285 million by 2025 and the country’s annual growth rate would be around 14.5 between the period of 2021 to 2028.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

North America region dominated the global market in 2024

The North America region dominated the global market with substantial revenue share in 2024, and is projected to maintain its market dominance throughout the forecast period. The regional market growth can be highly attributed to rising number of health-conscious consumers and a drastic shift towards the lactose free butter from diary products and region’s high spending capacity compared to other regions in the world. Additionally, the presence of well-established distribution and retail networks that facilitates the availability of lactose free butter across various channels including supermarkets, specialty stores, and online platforms is further supporting the region’s growth.

The Europe region is anticipated to be the fastest growing region with significant growth rate over the coming years, owing to growing popularity of vegan and plant-based diets across the region and constantly increasing demand for dairy alternatives including lactose free butter made from plant-based sources such as almonds, soy, or coconut particularly in developed economies like UK, Germany, France, and Spain among others.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Market Players & Competitive Insights

The lactose free butter market is fragmented and is anticipated to witness competition due to several players' presence. Major players in the market are constantly launching novel varieties to stay ahead of the competition. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

Who are the major players in the lactose free butter market?

Some of the major players operating in the global market include

- Agropur Dairy

- CAPSA Foods

- Cargill

- Corbion

- Challenge Dairy Company

- Butterfields Butter

- DuPont

- General Mills

- Hain Celestial

- Ingredion

- Kellogg Company

- Kerry Group

- Kraft Heinz

- Valio Ltd.

- Miyoko’s Creamery

- Molkerei Biedermann

- Parmalat

- Uelzena Ingredients

Recent Developments

- November 2025: Lurpak (DK) introduced a new range of lactose-free butter spreads infused with natural flavors to appeal to younger, variety-seeking consumers. The launch strengthens its portfolio and taps into rising demand for flavorful, health-focused options.

- In July 2024, Challenge Butter launched a nationwide lactose-free clarified butter with canola oil, targeting lactose-intolerant consumers seeking rich butter flavor.

- In June 2023, Lurpak, announced the launch of its latest vegan version of iconic butter and dairy-free version across the United Kingdom. The company mainly focusing on the expansion of its product portfolio and meet the rising need for diary-free products across the globe, as these products have gained immerse traction over dairy products due to its several concerns regarding the environmental and health costs.

- In August 2021, WhiteCub, introduced its “WhiteCub Vegan Butter”, that is mainly crated without any type of dairy product and is completed developed with plant-based vitamins B12 & D.

Lactose Free Butter Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 321.97 million |

| Market size value in 2025 | USD 340.16 million |

| Revenue forecast in 2034 | USD 569.82 million |

| CAGR | 5.9% from 2025 – 2034 |

| Base year | 2024 |

| Historical data | 2020 – 2023 |

| Forecast period | 2025 – 2034 |

| Quantitative units | Revenue in USD million and CAGR from 2025 to 2034 |

| Segments covered | By Application, By End-Use, By Distribution Channel, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key companies | Parmalat S.p.A., Uelzena Ingredients, CAPSA Foods Company, Valio Ltd., Butterfields Butter LLC, Miyoko’s Creamery, Molkerei Biedermann AG, The Hain Celestial Group Inc., Cargill Inc., Corbion Inc., Kerry Group PLC, Ingredion Incorporated, DuPont Company, Kellogg Company, General Mills Inc., Agropur Dairy Cooperative, Challenge Dairy Company, and The Kraft Heinz Company. |

Source: Polaris Market Research Analysis

lactose free butter market FAQ's

The lactose free butter market report covering key segments are application, end-use, distribution channel, and region.

Lactose Free Butter Market Size Worth $569.82 Million by 2034.

The global lactose free butter market is expected to grow at a CAGR of 5.9% during the forecast period.

North America is leading the global market.

key driving factors in lactose free butter market are rising awareness regarding health & wellness among the people.

Download Sample Report of lactose free butter market

Please fill out the form to request a customized copy of the research report.