Market Overview

The global medical gas market size was valued at USD 16.25 billion in 2025. The market is projected to account for a CAGR of 8.4% between 2026 and 2034. The medical gas market growth is attributed to rising hospital infrastructure development and increased home healthcare usage. The market also benefits from growing demand for respiratory therapy gases, driven by the prevalence of respiratory diseases. Medical gases are an essential part of modern healthcare delivery. They support respiratory therapy, anesthesia administration, critical care, diagnostic procedures, and pharmaceutical manufacturing. The market benefits from recurring demand, as these gases are continuously consumed across hospitals, ambulatory surgical centers, emergency departments, and home-based care settings.

The need for medical gases in healthcare applications is becoming increasingly important, given the rising prevalence of chronic diseases. Medical gases are playing a very important role in therapeutic and diagnostic applications, making them essential in the modern healthcare setting. Governments are taking initiatives to enhance the accessibility and quality of medical gas services, thereby boosting the market growth. Also, an aging population is associated with the prevalence of age-related diseases, making healthcare services a primary need. The growing medical gas market trends of home healthcare oxygen therapy solutions and point-of-care products further contribute to the expanding scope of the market. In addition to this, the market is being fueled by investments in healthcare modernization and the installation of medical gas pipeline systems. Healthcare providers are increasing their focus on ensuring the uninterrupted supply of gas, safety, and regulatory compliance. Thus, medical gases are not only a product but also part of the infrastructure in healthcare settings.

Key Insights

- The therapeutic segment led the market with 35.64% revenue share in 2025. This is due to the widespread use of medical gases in treating and managing various diseases.

- The gas mixtures segment is projected to witness rapid growth. Gas mixtures are essential in the calibration of analytical instruments that detect the quantity of carbon monoxide.

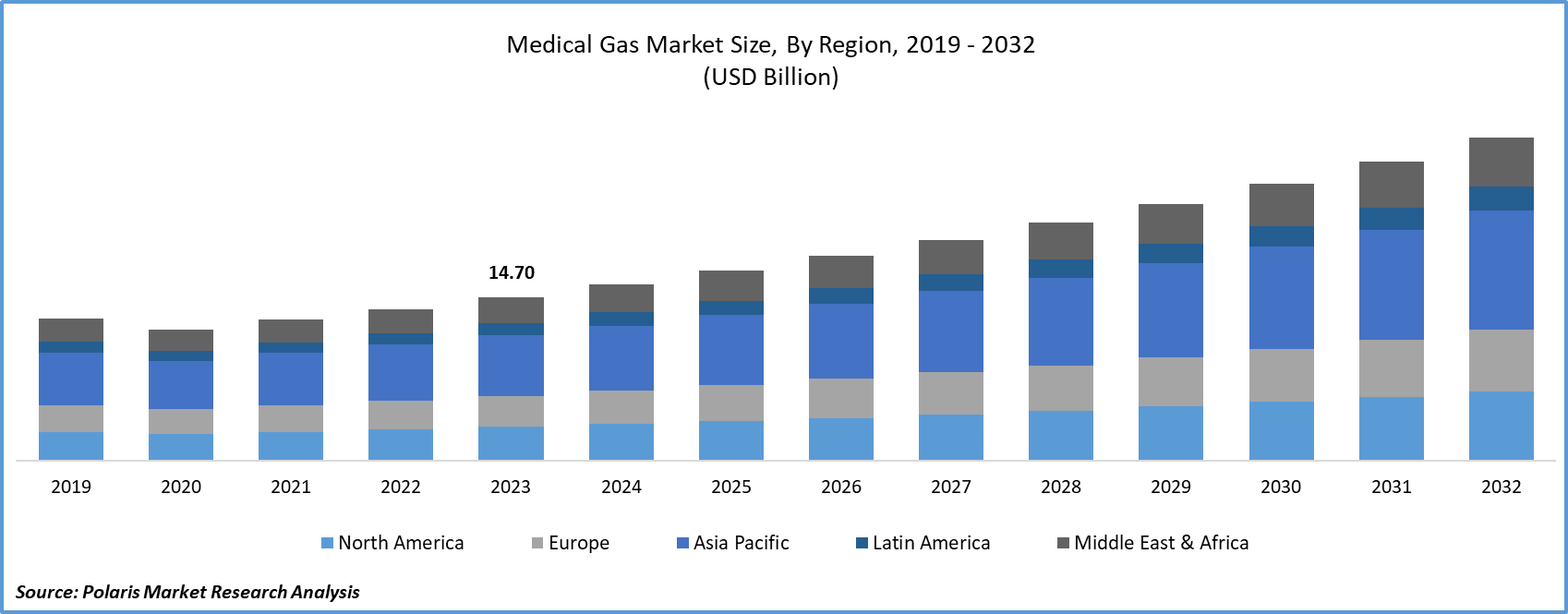

- North America dominated the medical gas market with a 49.80% revenue share in 2025. The rising use of medical gases in treating respiratory diseases contributes to the regional market dominance.

- Asia Pacific is projected to witness the fastest growth during the projected period. The presence of densely populated emerging economies drives market growth in the region.

Industry Dynamics

- The growing prevalence of respiratory diseases is one of the major factors driving the market for medical gases.

- The rising preference for home healthcare solutions and point-of-care products contributes to the regional market demand.

- Rapid development of hospitals and healthcare facilities in emerging markets is expected to create several market opportunities.

- High costs associated with medical gases may hinder market growth.

Market Statistics

2025 Market Size: USD 16.25 billion

Medical Gas Market Forecast 2034: USD 33.58 billion

Medical Gas Market CAGR (2026–2034): 8.4%

North America: Largest Market in 2025

To Understand More About this Research:Request a Free Sample Report

Every year, over 2 million individuals receive medical oxygen. As per the National Health Service (NHS), around 17.5% of patients in the UK are receiving medical oxygen at any given time. This totals approximately 18,000 patients daily. Furthermore, a research article published in MDPI (2018) calculated annual hospital bed gas consumption per bed, reporting 350 m3 for oxygen, 325 m3 for medicinal air, 9 m3 for nitrogen oxide, and 3 m3 for CO2. The usage patterns demonstrate the constant need for medical gases in medical facilities. They are commonly used in intensive care units, operating rooms, recovery rooms, and respiratory therapy departments. These facilities require uninterrupted medical gases to deliver proper medical care to their patients.

The medical gas market is witnessing an increasing demand, and this is attributed to the rise in the incidence of chronic respiratory diseases (CRDs) like asthma, chronic obstructive pulmonary disease, occupational lung diseases, and pulmonary hypertension. In 2019, chronic obstructive pulmonary disease (COPD) resulted in 3.23 million deaths worldwide, as reported by the World Health Organization (WHO). In addition, asthma affected 262 million people in 2019 and resulted in 455,000 deaths worldwide. Medical gases like oxygen, lung gas mixtures, and heliox are of significant importance in the diagnosis and treatment of these respiratory disorders. The growing incidence of such diseases continues to increase the need for oxygen therapy, pulmonary tests, blood gas analysis, and home respiratory care. All these treatments are heavily reliant on medical gases. Hence, demand for pure and mixed gases remains high.

The medical gas market report provides insights into the major market dynamics and enables industry players to align their medical gas market strategy with the prevailing and emerging trends. It discusses technological advancements and innovations in the industry and their impact on its presence. Moreover, the report includes a detailed regional analysis of the industry at the local, national, and global levels.

According to the WHO, in 2020, the global population aged 60 and above exceeded that of children aged 5 and below. Moreover, it is estimated that by 2050, the global population aged 60 and above will almost double to 2.1 billion, with the number of persons aged 80 and above expected to reach 426 million. The increase in the geriatric population has also led to an increase in respiratory diseases. For instance, 15.0% of older persons are suffering from respiratory diseases such as asthma, COPD, and other respiratory diseases, as estimated by data from the Princeton Health Care Center. These trends indicate a growing demand for oxygen supply. The aging population is also fueling demand for post-acute care, home oxygen therapy, ambulatory respiratory support, and long-term disease management. This segment of the population needs respiratory support and monitoring. Thus, the geriatric population is likely to be a key contributor to the demand for medical gases in the future.

How the Medical Gas Ecosystem Works?

A broader ecosystem of healthcare facilities influences the medical gas market. This medical gas ecosystem includes medical gas producers, cylinder suppliers, bulk storage facilities, pipeline system installers, monitoring device suppliers, and healthcare facilities. In many hospitals, medical gases such as oxygen, medical air, nitrous oxide, nitrogen, and carbon dioxide are supplied via a centralized pipeline system. These hospital gas pipeline systems are connected to operating rooms, ICUs, neonatal facilities, and recovery rooms. In smaller facilities and home healthcare settings, medical gas is supplied through medical gas cylinders and concentrators. This expanded ecosystem demonstrates that the medical gas market is driven not only by the number of patients. It is also fueled by the need for upgrades, safety, and a reliable medical gas supply.

Growth Drivers

Increasing Prevalence of Respiratory Diseases

Oxygen is essential for preventing pulmonary artery hypertension. Its prolonged use may alleviate strain on the heart. Due to the rising number of people suffering from respiratory diseases, the medical gas industry is growing. However, the medical gas industry faced significant challenges during the COVID-19 pandemic. The demand for oxygen during the COVID-19 pandemic led to shortages and supply chain disruptions. For example, in India, demand for liquid medical oxygen (LMO) increased from 700 TPD before the pandemic to 2,800 TPD during the first wave. In the second wave of the pandemic, demand rose more than sevenfold from pre-pandemic levels and reached 5,000 TPD. This increase in demand also caused healthcare systems to invest in localized oxygen generation systems, hospital backup oxygen systems, cryogenic storage, and medical gas supply chains. Many hospitals also began to focus on reliability and emergency preparedness. These developments continue to influence medical gas supply and management today.

Expansion of Healthcare Infrastructure and Home Healthcare

The medical gas market is also gaining support from healthcare infrastructure development, expansion of critical care facilities, and the modernization of healthcare facilities, especially in emerging economies. In addition, the increasing use of home healthcare and long-term oxygen therapy is driving market growth outside the conventional hospital setting, thereby supporting the need for oxygen, medical air, and portable oxygen delivery systems, along with associated infrastructure, in home-based and home care settings.

Segmental Insights

By Product Analysis

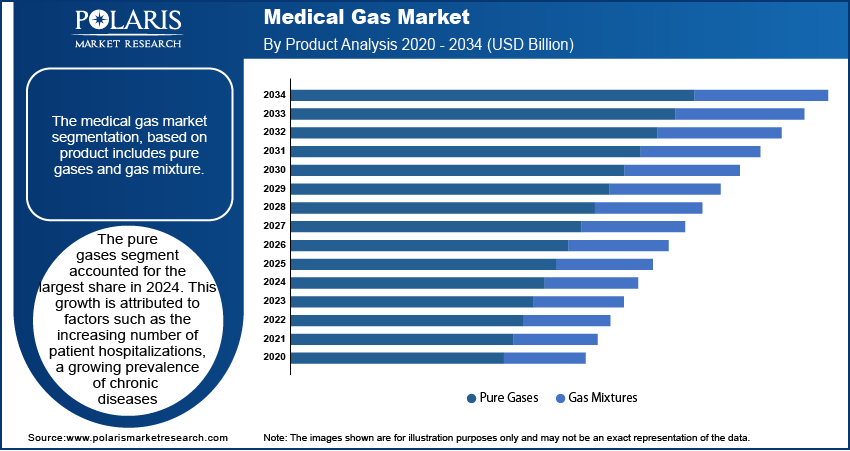

Pure Gases Segment Accounted for the Largest Market share in 2025

The pure gases segment has the largest market share in 2025. This is due to the increasing number of patients admitted to hospitals, the rise in the incidence of chronic diseases, and the increase in road accidents worldwide. According to the United Nations statistics in 2021, 1.3 million people die each year as a result of road accidents, with the WHO stating that over 20 to 50 million people are injured annually, many of whom suffer from permanent disability as a result of these accidents. This is causing a significant increase in the need for hospital oxygen therapy across different settings of life care.

In the category of pure gases, the oxygen sub-segment is likely to grow at the fastest rate. According to a report published by Pharma Review, the use of oxygen is required in varying concentrations for the treatment of different medical conditions, ranging from 20 to 40% for the treatment of COPD, 40 to 60% for the treatment of bronchial asthma, and 100% for the treatment of severe hypoxia and noxious gas poisoning, thereby increasing the growth rate in this segment. In addition, ICU patients and those undergoing surgeries in ambulatory care services also require oxygen for life support. The oxygen market is further supported by the increasing shift towards home healthcare and post-discharge care for patients with respiratory problems. This is because more and more patients are using home oxygen concentrators and backup systems for their care outside the hospital. It has led to increased oxygen use in decentralized care settings.

The gas mixtures segment is set to experience rapid growth. Gas mixtures find critical application in the calibration of instruments that measure the quantity of carbon monoxide in the lungs and are used in pulmonary function testing. These tests have applications in various fields, including intensive care, neonatal care, rehabilitation, disability assessment, and the diagnosis of diseases related to the respiratory, gastrointestinal, and cardiovascular systems. Gas mixtures are useful in accurate diagnosis, special tests, and advanced pulmonary function tests. Therefore, it is expected that their demand will increase at a higher rate, even though pure gases are expected to retain the largest share in market revenue.

By Application Analysis

Therapeutic Segment Accounted for the Largest Market Share in 2025

The therapeutic segment led the medical gas market with 35.64% revenue share in 2025. This is because medical gases are commonly used in the management and control of various diseases. Medical gases are classified as medicines and are required to comply with strict purity and quality specifications. The main medical gases are oxygen, medical air, carbon dioxide, nitric oxide, and the mixture of oxygen and helium. Medical oxygen is commonly used in various healthcare settings, ranging from anesthesia to inhalation therapy. Medical gases are repeatedly utilized in critical care services, respiratory therapy, anesthesia support, and emergency treatment. These services require a consistent flow of medical gases; hence, the need for therapeutic medical gases is consistent. Thus, therapeutics is the most significant application segment in the market.

On the other hand, the diagnostics segment is expected to grow significantly, particularly as medical gases are used in medical imaging and laboratory activities. Laboratories require a controlled gas environment to perform activities such as cell culture and tissue development. Oxidizing gas mixtures are needed to develop aerobic environments, whereas hydrogen or CO2 gas mixtures are required to create anaerobic environments. Furthermore, diagnostic medical gases play a role in supporting pulmonary testing, blood gas calibration, and laboratory operations. Accurate gas mixtures are necessary to support the accurate results of respiratory tests and other complex medical analyses.

By End Use Analysis

Based on end use, the market is segmented into hospitals, ambulatory surgical centers, home healthcare, pharmaceutical and biotechnology companies, diagnostic and research laboratories, and academic and research institutions. Hospitals are the largest end-use category because they have a high patient count and perform many surgeries. They also have emergency admissions and require a consistent flow of medical gases like oxygen, medical air, and nitrous oxide in ICUs, operating rooms, and recovery rooms.

Ambulatory surgical centers are also emerging as key users as the trend continues to shift from inpatient to outpatient surgeries and the need for anesthesia and respiratory support increases. Home healthcare is expected to be a growing market in the future as the incidence of chronic respiratory diseases increases, the population ages, and the trend toward long-term oxygen therapy outside the hospital setting continues. Diagnostic laboratories and pharmaceutical and biotechnology companies also contribute to the demand through gas calibration, testing, manufacturing, and research.

Regional Insights

North America Dominated the Global Market in 2025

The North America medical gas market dominated the global market with a 49.80% revenue share in 2025. This steady growth can be attributed to the increasing use of medical gases in the treatment of respiratory diseases such as COPD and asthma. The high incidence of diseases like COPD and asthma, as well as other medical conditions like cardiovascular and lifestyle diseases, is expected to drive the regional market in the coming years. Also, the presence of technologically advanced hospital infrastructure, especially in ICU cases, a well-developed market, and a growing geriatric population has helped the U.S. account for a major share in the regional market. The market in North America is further supported by the high adoption of respiratory care technologies, the widespread home healthcare penetration, and strict regulations requiring continuous, reliable gas availability.

The Asia Pacific medical gas market is expected to witness the fastest growth during the forecast period. The rapid growth can be attributed to the presence of densely populated emerging economies in this region, which is expected to contribute significantly to the growth of this market. In addition, significant investment growth can be seen in this region. For instance, in May 2023, INOX Air announced plans to invest around USD 364 million by 2025 in response to growing demand in this market. The market is also growing due to rapid expansion in healthcare infrastructure, increasing ICU and surgical capacity, and rising awareness about respiratory disease management.

Key Market Players and Competitive Insights

The level of market consolidation is moderate. It is mainly because of the presence of a limited number of key players. The prominent medical gas market key players are highly involved in activities such as collaborations, product launches, mergers, and acquisitions as strategic measures to enhance their product portfolios.

The competitive landscape of this market is not based solely on product availability. Companies that have a wider supply chain and long-term contracts with hospitals and healthcare organizations have a larger competitive edge. Additionally, the ability to provide bulk gas supply, gas generation, and delivery systems is important to cater to the continuous demand of hospitals and healthcare organizations.

Furthermore, the provision of medical gas equipment and monitoring systems can be advantageous to hospitals and laboratories. Quick service, including the replacement of cylinders and provision of technical support, is also important to build customer relationships. In recent times, the provision of sustainable medical gases has become a key factor for medical gas suppliers. This includes the provision of low-carbon medical gases and environmentally friendly production processes.

Air Liquide is a medical gas supplier that provides medical gases to hospitals, medical facilities, and home healthcare settings worldwide. The company offers medical gases, such as oxygen and nitrous oxide, which are essential for patient care and treatment.

Linde plc is one of the world’s leading medical gas companies and a provider of medical solutions. The company offers medical gases for medical applications such as respiratory care and anesthesia. It has a global medical supply network and reliable delivery systems to provide medical facilities with a consistent and safe medical gas supply.

List of Key Medical Gas Companies

- Air Liquide

- Air Products and Chemicals Inc.

- Atlas Copco

- HORIBA Group

- INOX-Air Products Inc.

- Linde plc.

- Matheson Tri-Gas Inc.

- Messer SE & Co. KGaA

- SOL India Private Limited

- TAIYO NIPPON SANSO CORPORATION

Recent Developments

January 2025: Atlas Copco Group revealed the acquisition of Medi-teknique Ltd, a UK-based provider of medical gas maintenance and services. According to Atlas Copco Group, the strategic move aims at expanding its UK footprint.

January 2025: Air Liquide collaborated with 20 clinics and hospitals in Europe and Brazil, providing certified low-carbon medical gases, which helped the healthcare facilities reduce their carbon footprint by more than 70%.

March 2023: Atlas Copco acquired the operating assets of FS Medical, which include medical gas equipment, laboratory gas systems, and other related medical gas systems.

January 2022: NOVAIR confirmed the acquisition of Oxygen Generating Systems Intl., which is expected to increase the company's manufacturing capacity and global footprint.

Market Segmentation

By Product Outlook (Revenue – USD Billion, 2021–2034)

- Pure Gases

- Medical Air

- Oxygen

- Nitrous Oxide

- Nitrogen

- Carbon Dioxide

- Helium

- Gas Mixtures

- Aerobic Gas Mixtures

- Anaerobic Gas Mixtures

- Blood Gas Mixtures

- Lung Diffusion Mixtures

- Medical Laser Mixtures

- Medical Drug Gas Mixtures

- Others

By Application Outlook (Revenue – USD Billion, 2021–2034)

- Therapeutic

- Diagnostics

- Pharmaceutical Manufacturing

- Others

By End Use Outlook (Revenue – USD Billion, 2021–2034)

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare

- Pharmaceutical and Biotechnology Companies

- Diagnostic and Research Laboratories

- Academic and Research Institutions

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical Gas Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 16.25 billion |

|

Market Size in 2026 |

USD 17.59 billion |

|

Revenue Forecast by 2034 |

USD 33.58 billion |

|

CAGR |

8.4% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Medical Gas Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The medical gas market stood at USD 16.25 billion in 2025. The market is projected to grow to USD 33.58 billion by 2034.

The market is anticipated to account for a CAGR of 8.4% between 2026 and 2034.

North America accounted for the largest medical gas market share in 2025. The increasing use of medical gases in the treatment of respiratory diseases such as COPD and asthma contributes to the regional market dominance.

The market for medical gases is driven by the growing prevalence of respiratory diseases and the rising preference for home healthcare solutions.

The diagnostics segment is expected to grow significantly, particularly as medical gases are used in medical imaging and laboratory activities.

Page last updated on:

Jan-2024

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements