Market Overview

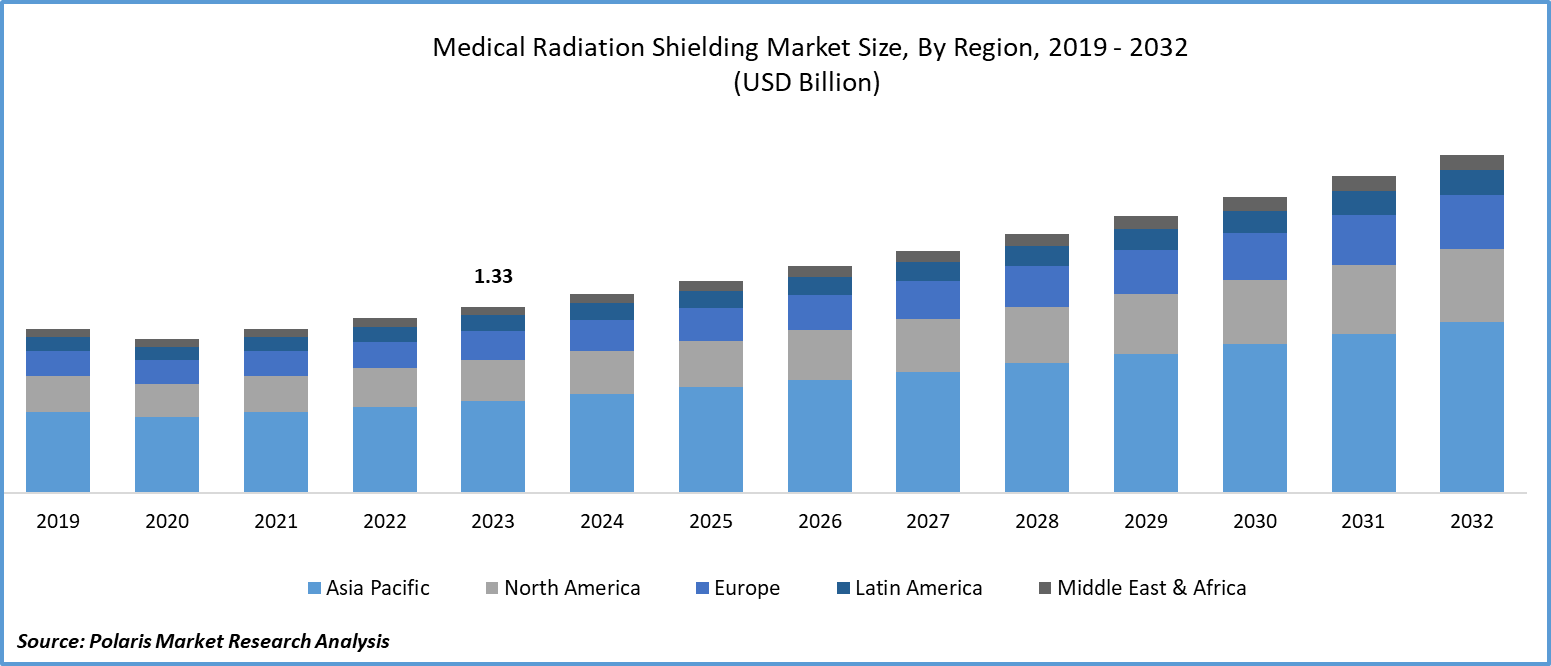

The global medical radiation shielding market size was valued at USD 1,507.73 million in 2025. The medical radiation shielding market CAGR is expected to be 6.7% during 2026–2034. The market expansion is primarily driven by increasing government regulations to improve workplace safety and ongoing R&D activities, both of which are creating new growth opportunities.

Medical radiation shielding comprises structural barriers (such as lead-lined walls, doors, and glass) and wearable protective devices used to shield against harmful radiation exposure during imaging and cancer treatment procedures. The demand for medical radiation shielding solutions is increasing as hospitals and diagnostic centers expand their services in CT scans, X-rays, fluoroscopy, and radiotherapy, while also adhering to tougher radiation shielding regulations.

Key Insights

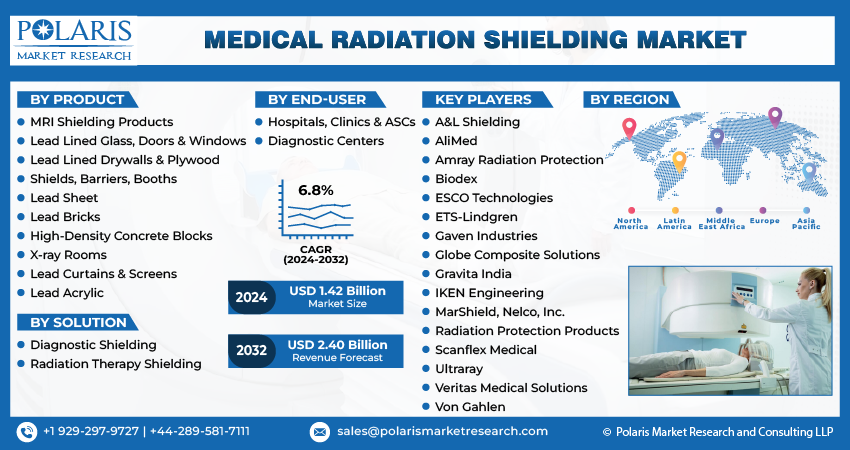

- The hospitals, clinics, & ASCs segment is anticipated to register significant growth, owing to the growing number of radiation therapies and diagnostic imaging procedures being done in these facilities.

- Lead-free, lightweight shielding materials are also being developed as new alternatives for healthcare providers who are looking for options that are easier to handle. These materials also promote sustainability goals.

- The diagnostic shielding segment led the market in 2025. The segment’s dominance is attributed to the rising use of imaging technologies such as CT scans and X-rays in diagnostic centers and hospitals.

- The North America medical radiation shielding market accounted for the largest market share in 2025, primarily driven by its advanced healthcare infrastructure and a high number of routine diagnostic procedures.

- The Asia Pacific medical radiation shielding market is anticipated to register the highest CAGR. Increasing healthcare investments and growing awareness about radiation safety are driving regional market growth.

Industry Dynamics

- Increasing government investments in the healthcare sector in developed and developing countries are leading to more healthcare facilities, thereby increasing demand for medical radiation.

- The growing number of cases of chronic diseases, such as cancer, is increasing the demand for diagnostic and radiation therapy, thus fueling the growth of the market.

- A greater focus on tailoring solutions to specific environments is likely to create many opportunities for the medical radiation shielding market.

- The initial manufacturing cost is likely to slow market growth. High upfront costs are often driven by material pricing, installation labor, and downtime during construction.

Market Statistics

2025 Market Size: USD 1,507.73 million

2034 Projected Market Size: USD 2,703.29 million

CAGR (2026-2034): 6.7%

North America: Largest Market in 2025

To Understand More About this Research:Request a Free Sample Report

Radiation shielding is a barrier positioned between the radiation source and individuals or regions that require protection to limit exposure to safe levels. In the absence of appropriate radiation shielding in hospitals and imaging facilities, personnel and the general public, including dentists, veterinarians, and interventional radiologists, may be exposed to radiation levels exceeding permitted radiation exposure limits. This can increase long-term health risks and compliance liabilities.

Medical Radiation Shielding Explained

Radiation shielding is employed in healthcare facilities to reduce exposure not only for patients but also for healthcare providers and the surrounding areas. It is done using lead-lined drywall or plywood, shielding doors and windows with lead glass, fixed or mobile shielding, and protective clothing such as aprons and thyroid shields. The extent and nature of shielding vary depending on the imaging equipment and room design, such as in X-ray rooms compared to CT or interventional rooms, due to differences in radiation distribution and procedure duration.

It is necessary to distinguish between medical radiation shielding and MRI shielding. In MRI systems, there is no ionizing radiation. Instead, RF shielding is installed in facilities to prevent interference and ensure clear images. This distinction is essential for hospitals to make informed purchasing decisions when expanding their facilities.

Shielding is an important consideration in every medical facility, as it significantly reduces unwanted exposure, though it is hard to avoid radiation completely. The current research activities are creating new growth opportunities with innovative product launches in the market. Furthermore, the government's strict regulations to enhance workplace safety for medical professionals and patients are also fueling the adoption of medical radiation shielding systems.

Radiation shielding is undergoing developments that go beyond the conventional heavy lead-based shielding. New lead-free radiation shielding materials, modular shielding panels, and mobile radiation barriers are being developed and introduced into the market to facilitate easier installation, faster setup, and greater environmental compatibility. For instance, a study published on PubMed Central in 2022 demonstrated the development and laboratory evaluation of a robotic shielding device for interventional cardiology procedures, which showed a definite reduction in personnel exposure compared to procedures performed without shielding. These developments are supporting upgrades in cath labs and interventional suites. They are ensuring a steady demand for new radiation shielding solutions.

Market Dynamics

Rising Government Investments in Healthcare Sector

Government expenditure on healthcare is rising in both developed and developing areas. According to the Centers for Medicare & Medicaid Services, the United States spent approximately USD 4.9 trillion on healthcare in 2023. Increased expenditure is resulting in the development of hospitals, diagnostic centers, and specialty clinics. This is fueling the demand for medical radiation shielding to safeguard patients and healthcare professionals during procedures such as digital X-rays, CT scans, and interventional procedures. Increasing healthcare expenditure supports demand for shielding not only in new hospital construction but also in renovation and upgrade cycles. When facilities upgrade their imaging rooms, install new CT scanners, expand radiotherapy departments, or upgrade older spaces to meet current safety standards, they may require new or upgraded shielding. This creates repeat business for installation services and structural components such as shielding doors, lead glass, and lead-lined walls.

Rising Cases of Chronic Diseases

The number of cancer patients is rising globally, which has led to an increase in the demand for cancer diagnosis and radiation oncology. Both procedures require exposure to ionized radiation, which is toxic to normal tissues if not handled carefully. According to the International Patients, the Heidelberg University Hospital in Germany alone treats 4,500 patients annually using radiation therapy. Hospitals and clinics need to provide a safe environment for patients and staff as patient numbers continue to rise. With the increasing number of radiotherapy procedures, there is a growing need for specialized shielding in treatment rooms such as LINAC suites. The shielding in these rooms differs from that in imaging rooms because LINAC rooms involve higher-energy radiation and more detailed room planning.

Segment Analysis

Market Assessment by End User

The medical radiation shielding market segmentation, based on end user, includes hospitals, clinics, & ASCs and diagnostic centers. The hospitals, clinics, & ASCs market is anticipated to register substantial growth during the forecast period, driven by the rising number of diagnostic imaging procedures and radiation therapies performed in these institutions. Patients are increasingly seeking treatment in these centers because of the rising incidence of cancer and chronic diseases, thus creating a demand for radiation protection. Moreover, developments in the infrastructure of the healthcare sector, particularly in developing nations, are fueling the growth of this market.

Diagnostic centers are primarily driven by repeat demand for protective shielding used in CT, X-ray, and fluoroscopy suites, where standard building materials such as shielding doors, lead glass, and lined walls are required. Hospitals, on the other hand, are also driven by demand for specialized shielding for therapy rooms as they expand their cancer programs. This explains the difference in demand trends between standard shielding products and therapy shielding solutions.

Market Evaluation by Solution

The market segmentation, based on solution, includes diagnostic shielding and radiation therapy shielding. The diagnostic shielding segment accounted for the largest share in the medical radiation shielding market in 2025. This is due to the increasing adoption of imaging technologies such as X-ray, CT scans, and fluoroscopy in hospitals and diagnostic centers. Shielding has become the need of the day with the rising number of patients undergoing these procedures for early detection and follow-ups. Diagnostic shielding products, such as lead-lined walls, doors, and glass, help in mitigating the effects of harmful radiation. The rising concern for patient and staff safety is also fueling the growth of this segment.

The demand for diagnostic shielding is more closely linked to the increase in imaging procedures. In contrast, the demand for radiation therapy shielding is more closely linked to the installation of radiotherapy equipment such as LINACs and proton therapy systems, as well as the establishment of new cancer centers.

Regional Insights

The study provides the medical radiation shielding market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, the North America medical radiation shielding market led the global market due to its well-developed healthcare infrastructure and a large number of adoption rates for diagnostic imaging and radiation therapy. The region has a well-developed regulatory system that strictly follows safety guidelines, thereby encouraging hospitals and clinics to invest in efficient shielding solutions. The large number of cancer cases and frequent diagnostic procedures also boost the demand for shielding materials. According to the American Cancer Society, 1,958,310 people in the US were diagnosed with cancer in 2023, which highlights the large number of cancer cases in the region, thus fueling the growth of the market. In North America, demand is driven by periodic compliance audits, improvements in imaging infrastructure, and the expansion of outpatient diagnostic services. These shifts create a steady stream of replacement and retrofit requirements for shielded doors and glass, lead-lined wall systems, and protective barriers in hospitals and imaging centers.

The Asia Pacific medical radiation shielding market is expected to register the highest CAGR during the forecast period due to increased investments in the healthcare sector, advancements in medical infrastructure, and increased awareness about radiation safety. Countries such as China, Japan, and South Korea are increasing their diagnostic and cancer treatment facilities to cater to their large populations. The need for radiation shielding is also increasing as more hospitals are installing advanced imaging systems and radiotherapy facilities. Furthermore, government efforts to enhance healthcare accessibility and quality are also contributing to the demand for radiation protection equipment, thus fueling the growth of the Asia Pacific market. In the Asia Pacific region, the main drivers of growth are new diagnostic installations and the development of oncology facilities. With more X-ray rooms and the construction of new radiotherapy facilities, demand for X-ray room shielding, CT room shielding, and therapy room shielding is increasing.

The medical radiation shielding market in India is expanding rapidly. This is because of the increasing number of cancer cases and the establishment of more imaging and treatment facilities. The government's emphasis on improving access to healthcare and infrastructure in both urban and rural areas has led to increased use of diagnostic equipment and radiotherapy facilities. Hospitals are adopting more effective shielding practices as medical professionals become increasingly aware of radiation safety. In addition, the entry of private players into the healthcare industry is contributing to rising demand for better facilities, which in turn is fueling demand for high-quality radiation shielding materials.

Key Players and Competitive Analysis

The medical radiation shielding market opportunity is constantly evolving, with many firms seeking to innovate and differentiate themselves. The top global radiation shielding suppliers dominate the market through extensive research and development and sophisticated methods. These firms focus on strategic initiatives such as mergers and acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

Typically, buyers evaluate their vendors on their capacity to provide customized solutions, assist with installation, possess the necessary quality certifications, have acceptable lead times, and provide excellent after-sales support. Vendors with a full range of turnkey shielding solutions are often more competitive, particularly for hospital renovations and retrofits.

New companies are impacting the medical radiation shielding market by introducing innovative products to meet the demand of specific sectors. The competitive trend is amplified by continuous progress in product offerings. A few major players in the market are A&L Shielding; AliMed; Amray Radiation Protection; Mirion Technologies, Inc.; ESCO Technologies; ETS-Lindgren; Gaven Industries; Globe Composite Solutions; Gravita India; IKEN Engineering; MarShield; Nelco, Inc.; Radiation Protection Products, Inc.; Scanflex Medical; Ultraray; Veritas Medical Solutions; and Von Gahlen.

Mirion Technologies, Inc. is a business entity that deals with radiation detection, measurement, and medical technology. The company is headquartered in Atlanta, Georgia, and has operations in several other countries, including the US, Canada, the UK, France, Germany, Finland, China, Belgium, the Netherlands, Estonia, and Japan. The company caters to various sectors like nuclear energy, healthcare, defense, and scientific research. Mirion Technologies was established in 2005 following the merger of several companies that specialized in radiation technology. The company’s business is categorized into two segments: Medical and Nuclear & Safety. The Medical business offers products associated with radiation therapy and imaging. These products include dosimetry solutions, patient safety solutions, and quality assurance solutions for imaging and therapy. It also encompasses shielding and handling solutions for nuclear medicine. This business mainly caters to hospitals, cancer therapy centers, and imaging facilities. The Nuclear & Safety business offers radiation detection and measurement solutions. These solutions are employed in nuclear power plants, defense, industry, and research laboratories. Its portfolio comprises personal radiation detectors, area monitors, reactor solutions, waste management solutions, and laboratory analysis solutions like process spectroscopy solutions. Mirion’s solutions help measure the levels of radiation and ensure that safety standards are met. They are also employed for scientific analysis in an environment where ionizing radiation is present. The company’s global presence enables it to offer localized sales and service support to its customers.

Radiation Protection Products, Inc. (RPP) is an organization that produces radiation shielding materials and nuclear shielding products. Founded in 1952, it has its headquarters in Wayzata, Minnesota, with a major production facility in Chapel Hill, Tennessee, and a sales office in Mesa, Arizona. RPP offers its products to the medical, nuclear, and industrial markets, with a major focus on materials for radiation control. The various products offered by RPP include lead-lined drywall and plywood, radiation-shielded doors, leaded X-ray safety glass, lead-lined door and window frames, lead bricks, and interlocking lead bricks. These products are applied in different environments, including medical imaging rooms, radiation therapy centers, nuclear power stations, and industrial facilities where radiation protection is of prime importance. RPP's products are used in medical imaging procedures such as X-ray, CT, PET, and fluoroscopy, as well as in linear accelerators and proton therapy. The products also serve nuclear storage and research facilities and offer industrial lead products for special applications. RPP provides consultation, design, and installation services to aid in complex shielding projects. Although the company is primarily based in the US, it serves customers nationwide and supports international projects.

List of Key Companies

- A&L Shielding

- AliMed

- Amray Radiation Protection

- ESCO Technologies

- ETS-Lindgren

- Gaven Industries

- Globe Composite Solutions

- Gravita India

- IKEN Engineering

- MarShield

- Mirion Technologies, Inc.

- Nelco, Inc.

- Radiation Protection Products, Inc

- Scanflex Medical

- Ultraray

- Veritas Medical Solutions

- Von Gahlen

How Buyers Implement Radiation Shielding

A general radiation shielding project involves a distinct step-by-step procedure: facility planning and equipment selection → shielding design and safety evaluation → procurement of materials such as doors, glass, lead-lined panels, and barriers → installation and completion → final inspection and acceptance → monitoring and maintenance.

For imaging rooms, shielding requirements depend on frequency of use, room design, and the presence of nearby occupied spaces. As a result, hospitals typically collaborate with radiation safety experts to determine the shielding requirements for X-ray rooms before approval. The inclusion of this structured information enhances the document's value to procurement specialists and supports more specific procurement decisions on installation planning and cost analysis.

Medical Radiation Shielding Industry Developments

September 2024: Burlington Medical introduced BAT, an innovative radiation protection garment for the breast, axilla, and thyroid. With the new garment, the company aims to address critical protection gaps and reduce cancer risks for healthcare workers.

March 2022: Radiaction Medical Ltd. received FDA clearance for its innovative radiation protection system. The clearance made it possible for Radiaction to introduce the technology in the U.S. This represented a major leap in radiation protection in healthcare facilities.

Medical Radiation Shielding Market Segmentation

By Product Outlook (Revenue, USD Million, 2021–2034)

- MRI Shielding Products

- Lead Lined Glass, Doors & Windows

- Lead Lined Drywalls & Plywood

- Shields, Barriers, Booths

- Lead Sheet

- Lead Bricks

- High-Density Concrete Blocks

- X-ray Rooms

- Lead Curtains & Screens

- Lead Acrylic

By Solution Outlook (Revenue, USD Million, 2021–2034)

- Diagnostic Shielding

- Radiation Therapy Shielding

By Material Outlook (Revenue, USD Million, 2021–2034)

- Lead-based Shielding

- Non-lead Shielding

- Hybrid Shielding

By End Users Outlook (Revenue USD Million, 2021–2034)

- Hospitals, Clinics, & ASCs

- Diagnostic Centers

By Regional Outlook (Revenue, USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical Radiation Shielding Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 1,507.73 million |

|

Market Size in 2026 |

USD 1,607.30 million |

|

Revenue Forecast by 2034 |

USD 2,703.29 million |

|

CAGR |

6.7% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD million, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Medical Radiation Shielding Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market size was valued at USD 1,507.73 million in 2025 and is projected to grow to USD 2,703.29 million by 2034.

The market is projected to account for a CAGR of 6.7% between 2026 and 2034.

North America accounted for the largest market share in 2025. This is due to its well-developed healthcare infrastructure and high adoption rates for diagnostic imaging and radiation therapy.

A few key players in the market are A&L Shielding; AliMed; Amray Radiation Protection; Mirion Technologies, Inc.; ESCO Technologies; ETS-Lindgren; Gaven Industries; Globe Composite Solutions; Gravita India; IKEN Engineering; MarShield; Nelco, Inc.; Radiation Protection Products, Inc.; Scanflex Medical; Ultraray; Veritas Medical Solutions; and Von Gahlen.

The diagnostic shielding segment dominated the medical radiation shielding market in 2025. It is driven by the increasing use of imaging technologies such as X-rays, CT scans, and fluoroscopy in both hospitals and diagnostic centers.

The hospitals, clinics, & ASCs segment is expected to witness significant growth during the forecast period due to the increasing number of diagnostic imaging procedures.

Medical radiation shielding refers to special materials used in hospital walls, doors, and windows to block harmful radiation. It helps protect patients, doctors, and visitors from unnecessary exposure.

Diagnostic shielding is used in imaging rooms like CT scans to control lower radiation levels. Radiation therapy shielding is intended for treatment rooms with much higher radiation doses.

Common products used for X-ray room shielding include lead-lined drywall or panels, radiation shielding doors, and radiation shielding glass for viewing windows.

The cost of radiation shielding installation is based on various factors. These include room size, radiation levels, and local safety rules, amongst others.

Page last updated on:

Jan-2024

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements