Reports

Metal Binder Jetting Market Growth Rate, Volume, and Forecast, 2025-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

What is Metal Binder Jetting Market Size?

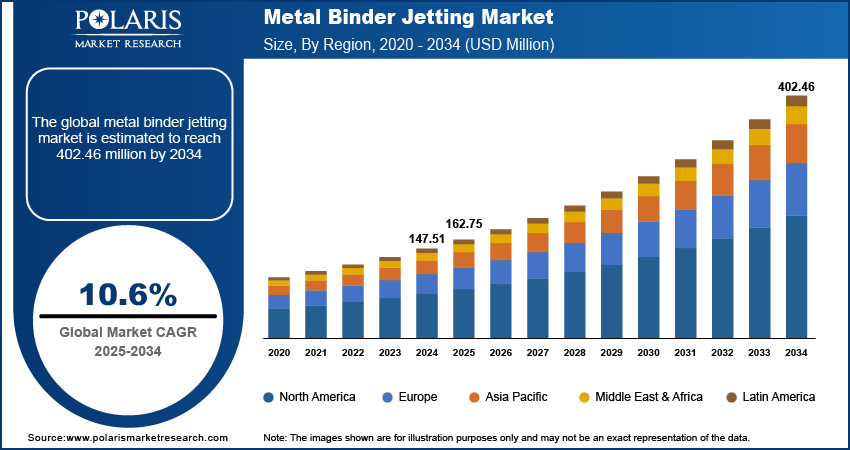

The global metal binder jetting market size was valued at USD 147.51 million in 2024, growing at a CAGR of 10.6% from 2025–2034. Key factors driving the growth is growth of automotive industry, growing usage in aerospace and defense, and technological advancement.

Key Insights

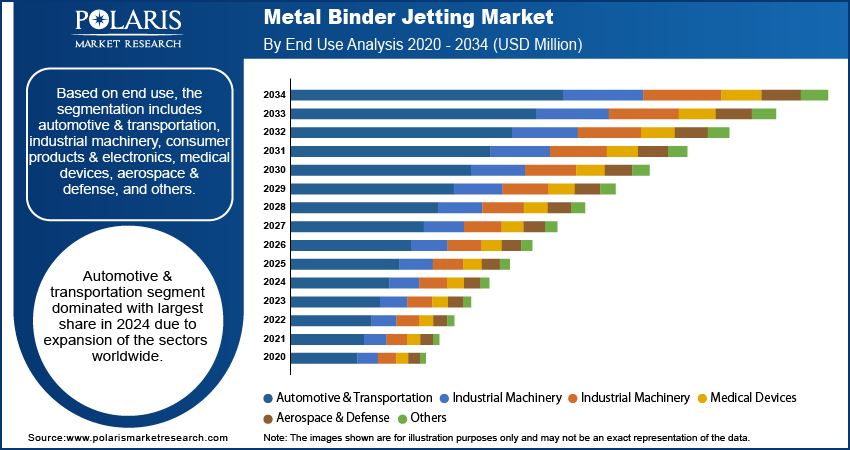

- Automotive & transportation segment dominated with largest share in 2024 due to expansion of the sectors worldwide

- Medical devices segment is expected to witness a significant share over the forecast period due to demand for medical devices with advance design with lightweight material

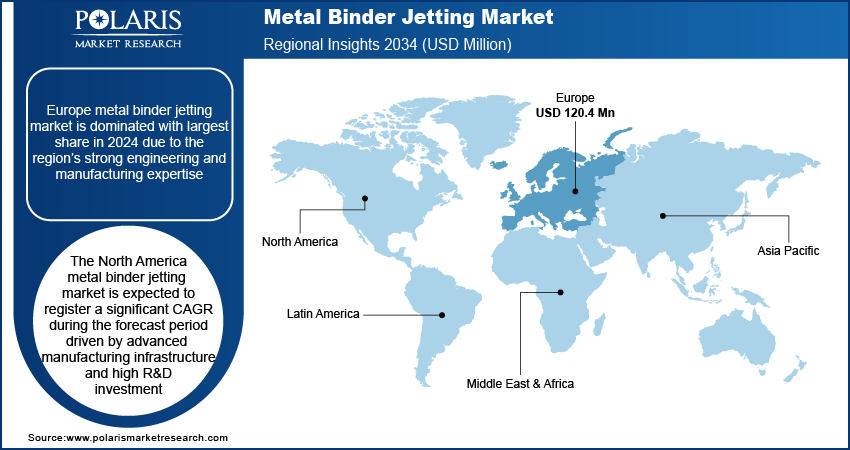

- Europe metal binder jetting Market is dominated with largest share in 2024 due to the region’s strong engineering and manufacturing expertise

- The North America metal binder jetting market is expected to register a significant CAGR during the forecast period driven by advanced manufacturing infrastructure and high R&D investment

Industry Dynamics

- The rise in adoption in automotive industry is driving the growth.

- Increase in demand from aerospace and defense is fueling the growth.

- Technological advancement is boosting the growth.

- High production costs limits the growth of the market.

Market Statistics

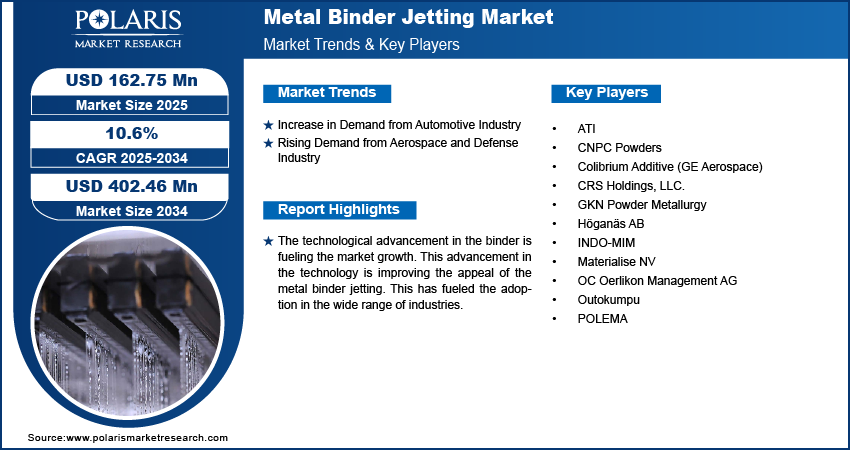

- 2024 Market Size: USD 147.51 Million

- 2034 Projected Market Size: USD 402.46 Million

- CAGR (2025-2034): 10.6%

- Europe: Largest Market Share

Metal binder jetting is an additive manufacturing process where a liquid binding agent is selectively deposited onto a bed of metal powder, layer by layer, to create a 3D object. After printing, the part undergoes sintering or curing to fuse the metal particles into a solid component. This technique enables high-volume, cost-effective production of complex metal parts with minimal material waste.

The rising adoption of the smart manufacturing, digital production and Industry 4.0 is fueling the industry growth. Manufacturers are increasingly shifting to additive manufacturing which is fueling the adoption. Metal binder jetting is scalable, design free and integrates with the digital production system and companies shifting to digital and smart manufacturing are rapidly adopting this technology. Moreover, the investment in the industry 4.0 and smart manufacturing ecosystem is rising worldwide. Major private capitalist and public sector is investing in this manufacturing segment, consequently further fueling the demand for metal binder jetting, thereby driving the industry growth.

The technological advancement in the binder is fueling the market growth. This advancement in the technology is improving the appeal of the metal binder jetting. This has fueled the adoption in the wide range of industries. Further, this advancement has made metal binder jetting more cost-effective which has boosted the adoption in the small and medium enterprises and resulted in the industry expansion. Moreover, rising research and development spending by the major players operating the market has further accelerated the development of new technologies, thereby fueling the growth.

Drivers & Opportunities

What are Factors Driving Industry Growth?

Increase in Demand from Automotive Industry: The adoption of the lightweight material in the automotive component is rising. This rise in the adoption is fueled by stringent environmental regulations, the growth of electric vehicles, and the demand for improved vehicle performance and safety. Consequently, the usage of metal binder jetting has increased by the automotive manufacturers. Metal binder jetting helps produce lightweight automotive components by enabling complex, material-efficient geometries and thin-walled metal structures that reduce mass without compromising strength. Moreover, the rise in the automotive production fueled by expanding middle class and disposable income is further driving the demand for metal binder jetting, thereby driving the industry growth.

Rising Demand from Aerospace and Defense Industry: The modern aircraft design is getting more complex. This has increased the demand for the technology which is capable of producing the aircraft parts efficiently without hampering the cost constraint. As a result, the adoption of the metal binder jetting in the rising in the aerospace and defense industry. It creates an intricate internal geometry, lightweight lattice structures, and consolidated multi-part assemblies without the design limits of machining or casting. This enables high-precision, high-strength components that meet aerospace performance requirements. Moreover, rising government spending in the defense research and development is further fueling the demand of this technology, thereby driving the industry growth.

Technological Innovations:

| Evolution Area | Specific Advancement | Details |

| Binder Improvements | Low-VOC furfuryl resins | Tweaking hydroxymethyl content cuts benzene outgassing by almost a third during mold burnout. |

| Binder Improvements | Low-temperature acrylics | Lower cure temperatures enable binder cross-linking without inducing thermal shock in oxide-prone powders such as Al 6061. |

| Sintering Technologies | PureSinter furnace for challenging alloys | Introduction enables repeatable sintering of Al 6061 and titanium alloys, unlocking aerospace-grade components. |

| Sintering Technologies | In-sinter correction with spatially varying shrink maps | Live Sinter beta incorporates shrink maps so gradient prints maintain accuracy during sintering. |

| Sintering Technologies | Infiltration for densification | Densification of porous structure with lower melting point material like bronze achieves complete density with minimal dimensional impact via capillary action. |

| Multi-Metal Printing | Droplet-spacing modulation for gradient density | Oak Ridge National Laboratory tunes porosity from 5% to 45% within single Ti-6Al-4V part for weight savings. |

| Multi-Metal Printing | Shell printing and new binders | Techniques provide insights for high-performance metal parts via advanced reinforcement in BJAM alloys. |

| Multi-Metal Printing | Advanced sintering methods | Evolving processes enable compatibility across iron, nickel superalloys, titanium, copper, magnesium, and aluminum alloys. |

Segmental Insights

Why Automotive & Transportation Dominated in 2024?

Automotive & transportation segment dominated with largest share in 2024 due to expansion of the sectors worldwide. The automotive sector is expanding worldwide. This expansion is fueled by the rising middle class and increase in the disposable income in developed and developing regions. This has increased the demand for the personal vehicles, consequently fueling the automotive productions and need for technology to produce high strength, lightweight automotive parts. Moreover, rising government spending in the public transportation is driving the demand for the buses worldwide which is further fueling the demand in this segment, thereby driving the segment growth.

Which Segment by End Use is Expected to Witness a Significant Share?

Medical devices segment is expected to witness a significant share over the forecast period due to demand for medical devices with advance design with lightweight material. These devices need to be lightweight to improve patient comfort, surgical precision, reduce fatigue for clinicians, and ensure easier implantation and mobility, especially for wearable or implantable. This has fueled the demand for the metal binder jetting as it enables highly customized, complex, and lightweight metal components. Moreover, advancement in the treatment of chronic injuries is further fueling the demand for advance medical devices, thereby driving the segment growth.

Regional Analysis

What are Regional Statistics of Industry?

Europe metal binder jetting Market is dominated with largest share in 2024 due to the region’s strong engineering and manufacturing expertise. Countries such as Germany, the UK, and France are leading adoption, particularly in automotive, aerospace, and medical device sectors. European companies value MBJ for producing lightweight, precise metal parts with less material waste, aligning with sustainability and circular economy goals. MBJ use is expanding beyond prototyping into full-scale production with supportive regulations and increasing investments in additive manufacturing, especially for high-quality, efficient, and complex components that meet industrial standards, thereby driving the growth in the region.

The North America metal binder jetting market is expected to register a significant CAGR during the forecast period driven by advanced manufacturing infrastructure and high R&D investment. Aerospace, automotive, and medical industries are the key drivers of growth. Companies in the region are leveraging MBJ to produce complex, lightweight, and high-performance metal parts efficiently, moving beyond prototyping into serial production. The focus on automation, supply chain optimization, and cost-effective manufacturing further accelerates adoption. It is becoming an essential part of North America’s modern manufacturing ecosystem as industries seek precision, reduced production time, and material efficiency, thereby driving the growth.

Key Players & Competitive Analysis

The market is fairly fragmented, with a mix of established powder‑metallurgy suppliers and newer additive‑specialist firms competing. Leading powder producers such as ATI, Höganäs AB, OC Oerlikon Management AG, GKN Powder Metallurgy, INDO-MIM and CNPC Powders provide high‑quality metal powders optimized for binder‑jetting, while additive‑centric companies such as Colibrium Additive (GE Aerospace), Materialise NV, CRS Holdings, LLC., Outokumpu and POLEMA position themselves around specialty alloys, part‑production services or niche regional supply. Competitive differentiation lies in powder quality (morphology, purity), alloy range, and vertical integration with binder‑jetting systems.

Key Players

- ATI

- CNPC Powders

- Colibrium Additive (GE Aerospace)

- CRS Holdings, LLC.

- GKN Powder Metallurgy

- Höganäs AB

- INDO-MIM

- Materialise NV

- OC Oerlikon Management AG

- Outokumpu

- POLEMA

Industry Developments

November 2025, Matsuura Machinery Ltd. was appointed as HP’s exclusive UK reseller for its Metal Jet additive manufacturing machines. The company supported UK manufacturers with demonstrations, training, and applications development, leveraging its AM/CNC hybrid LUMEX expertise for automotive, medical, and industrial sectors.

Metal Binder Jetting Market Segmentation

By End Use Outlook (Revenue, USD Million, 2020–2034)

- Automotive & Transportation

- Industrial Machinery

- Consumer Products & Electronics

- Medical Devices

- Aerospace & Defense

- Others

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Metal Binder Jetting Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 147.51 Million |

| Market Size in 2025 | USD 162.75 Million |

| Revenue Forecast by 2034 | USD 402.46 Million |

| CAGR | 10.6% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 147.51 million in 2024 and is projected to grow to USD 402.46 million by 2034.

The global market is projected to register a CAGR of 10.6% during the forecast period.

North America dominated the market in 2024

A few of the key players in the market are ATI, CNPC Powders, Colibrium Additive (GE Aerospace), CRS Holdings, LLC., GKN Powder Metallurgy, Höganäs AB, INDO-MIM, Materialise NV, OC Oerlikon Management AG, Outokumpu, and POLEMA.

The automotive and transportation segment dominated the market revenue share in 2024.

The medical, device segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Metal Binder Jetting Market

Please fill out the form to request a customized copy of the research report.