Metal Stamping Industry Overview

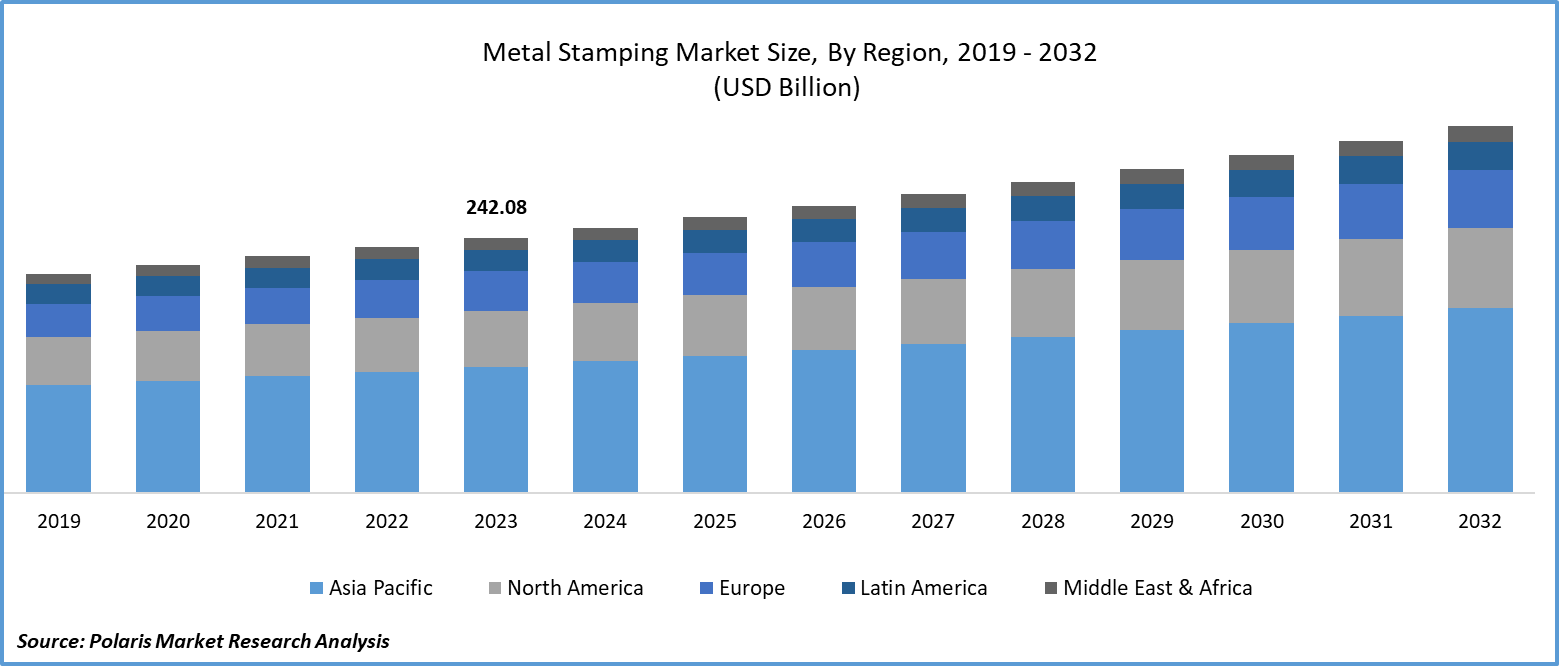

The global metal stamping market size was valued at USD 256.29 billion in 2025. The market is expected to account for a CAGR of 4.57% between 2026 and 2034. Steady demand from automotive, electronics, and industrial equipment manufacturing continues to drive market growth.

Key Insights

- Asia Pacific led the market with over 46.38% revenue share in 2025. This is due to the growing demand for phones and other consumer electronics in the region.

- Europe is projected to witness rapid growth, with a 2.99% CAGR. This is primarily attributed to its well-established automotive industry and the growing consumer electronics sector.

- The blanking segment accounted for the largest market revenue share of 32.77% in 2025. This is because blanking is essential for automobile manufacturing due to its precise and superior stamping capabilities.

- The servo press segment is projected to grow at a 6.98% CAGR. Servo press technology is increasingly used in the metalworking industry for precision metal-forming processes such as stamping.

Market Statistics

- 2025 Market Size: USD 256.29 billion

- 2034 Projected Market Size: USD 380.95 billion

- CAGR (2026–2034): 4.57%

- Asia Pacific: Largest Market in 2025

Industry Dynamics

- Increased demand for sheet metal to produce various automotive components has driven the expansion of the metal stamping market.

- The continuous growth of the consumer electronics industry is also contributing to the market development.

- Rising adoption of Industry 4.0 automation is projected to create several market opportunities.

- Fluctuating raw material prices may hinder market growth.

To Understand More About this Research:Request a Free Sample Report

Metal stamping is a vital part of the metal forming and precision manufacturing ecosystem. Metal stamping is a technique of shaping flat metal sheets using dies and presses. The products are used for various purposes. They find usage in the automobile, electronics, and aerospace industries. This technique is used to manufacture products on a mass scale at a lower cost. Therefore, it is a crucial industry for OEMs and Tier-1 suppliers across the globe.

The value chain of the metal stamping industry includes raw material suppliers such as steel, aluminum, and copper, along with tooling and die suppliers, stamping service providers, and end-use industries such as the automobile and electronics industries. The efficiency of the stamping value chain is directly related to the cost and competitiveness of the products.

Metal stamping continues to witness consistent demand due to its scalability and cost advantage in large-scale production. The metal stamping market is driven by a strong market for automotive production, miniaturization in electronics, and increased industrial automation. The trend towards electric cars and smart devices is also creating opportunities for components such as battery enclosures, connectors, and shielding parts.

The continuous growth of consumer electronics is also a major driving factor for this industry. This is due to the fact that metal frames are used in various consumer electronics. These include mobile phones, headphones, speakers, game pads, and controllers. In mobile phones, metal stamping is used to manufacture various mobile phone components. This is due to the various advantages of metal stamping. These include high tolerance, conductivity, and smooth finish. According to the GSMA Mobile Economy 2026 report, there were 5.8 billion unique mobile subscribers globally as of Q1 2026. Unique mobile subscribers are growing at an annual rate of 1.79%. This continuous increase in mobile phone subscribers is seen to be a major driving factor for mobile phones and hence metal stamping in the years to come.

The increased production of lightweight vehicles, driven by stringent government regulations across various countries, is expected to boost demand for alternative products. In the U.S., the development of Corporate Average Fuel Economy (CAFE) regulations to enhance fuel efficiency is boosting demand for alternative automotive products. This may therefore negatively affect the metal stamping market.

Market Dynamics

Growth Drivers

Automotive Industry Expansion

Rising automotive manufacturing is driving robust growth in the metal stamping market. According to the International Energy Agency, the global electric vehicle sales were 17 million in 2024. China maintained its dominant market position, with electric car sales exceeding 11 million. Government initiatives, such as subsidies for electric cars given to local manufacturers to encourage the development of EVs, have been instrumental in promoting an increase in their production. This increase in electric vehicle manufacturing is set to result in an increased demand for sheet metal in the manufacture of various auto components. These include chassis, interior and exterior structural elements, EV stamping components, and transmission components. This is expected to spur the automotive metal stamping market growth during the forecast period.

Consumer Electronics Demand

The continuous growth of consumer electronics is also a major driving factor for this industry. This is because metal frames are used in various consumer electronics. These include mobile phones, headphones, speakers, game pads, and controllers. In mobile phones, metal stamping is used to manufacture various mobile phone components. This is due to the various advantages of metal stamping. These include high tolerance, conductivity, and smooth finish. According to the GSMA Mobile Economy 2026 report, there were 5.8 billion unique mobile subscribers globally as of Q1 2026. Unique mobile subscribers are growing at an annual rate of 1.79%. This continuous increase in mobile phone subscribers is seen to be a major driving factor for mobile phones and hence consumer electronics metal stamping in the years to come.

Industrial Manufacturing Growth

Industrial machines and equipment manufacturing growth stamping is another key factor contributing to the metal stamping market development. The need for robust and high-strength components for heavy machines, automated equipment, and tools is increasing the use of metal stamping components.

Market Challenges & Restraints

Despite steady growth, there exist several metal stamping market challenges. These include changes in raw material costs, supply chain stamping issues, and increased competition from other manufacturing processes, such as casting and additive manufacturing. The increasing use of lightweight materials substitution, such as plastics and carbon fiber, in the manufacture of automobiles is also expected to reduce demand for traditional metal stamping.

Technology Trends & Innovation

The use of advanced technologies is transforming the metal stamping industry. The technologies involved are servo press systems, AI-based quality control systems, and simulation systems. Servo press systems are more precise and energy-efficient. They are also more flexible compared to traditional mechanical press systems. Technologies such as predictive maintenance, which is part of Industry 4.0, are also being employed in making the processes more efficient.

Report Segmentation

By Process Analysis

By process, the market is segmented into blanking, embossing, bending, coining, flanging, and others. The blanking segment led the market with a revenue share of 33.5% in 2025. Blanking is an important process in the manufacture of automobiles because of its accuracy and efficiency. The blanking process involves a die for cutting a part of a metal into a specific shape. The use of blanking in the automobile industry, especially in mass production, is a major contributor to the blanking process metal stamping dominance.

The bending segment is anticipated to grow at the fastest rate. The bending process requires pressure to be applied to the metal to take the desired shape on a flat surface. This process is found to be cost-effective, especially for lower or moderate quantities of metals. Bent components have many uses in automobiles, such as wheels, door hinges, and engine parts. The versatility and cost-effectiveness of bending are contributing to the bending metal stamping growth.

By Press Type Analysis

Based on press type, the market is segmented into mechanical press, hydraulic press, servo press, and others. The mechanical press segment led the metal stamping market in 2025. Mechanical press machines are widely used in sheet metal working, as they are known to apply pressure at high speeds without any interruption over a short distance. Unlike hydraulic press machines, mechanical press stamping machines have been demonstrated to operate at higher speeds, making them suitable for stamping operations.

The servo press segment is expected to grow rapidly, with a 5.9% CAGR. The servo press technology is gaining increased recognition in the market, especially within the metalworking industry, for precise metal forming techniques like stamping. The use of servo motors and controllers helps control the ram of the press more precisely. This increases the accuracy and flexibility in stamping.

By Application Analysis

Based on application, the market is segmented into automotive, industrial machinery, consumer electronics, aerospace, electrical & electronics, building & construction, telecommunications, and others. The automotive segment accounted for the largest market share in 2025. Various segments of the automotive industry, including passenger cars, light commercial vehicles (LCVs), trucks, buses, and coaches, require metal stamping parts for body panel manufacturing to ensure safety and control costs. As per the International Organization of Motor Vehicle Manufacturers, there was an increase of 6% in global vehicle manufacturing in 2022 compared to 2021. The projected increase in vehicle manufacturing on a large scale is anticipated to contribute to the growth of the metal stamping market in the automotive industry in the near future.

The aerospace segment is expected to experience significant growth. In the aerospace industry, metal stamping is critical for producing parts such as aircraft channels and frames. This is intended for attaining ultra-lightweight aircraft, contributing to improved fuel efficiency. The use of metal stamping in the manufacture of aircraft parts is a cost-effective, durable solution, which is expected to increase demand. Additionally, the rise in the production of commercial and fighter aircraft is expected to propel growth in aerospace metal stamping.

Regional Insights

Asia Pacific led the market with a revenue share of over 43.0% in 2025. The dominance is driven by developing countries, where there is an increase in the need for phones and consumer electronics. The favorable impact on the demand for machinery and equipment in the region is expected to be driven by the increase in industrialization, infrastructure, and expansion in the defense sector.

Countries such as China and India are increasing their investment in the defense sector. For example, China announced a 2026 defence budget of approximately USD 275 billion (1.9 trillion yuan) in March 2026. This marked a significant increase of roughly 10% over the previous year. The demand for defense equipment is anticipated to be a driving force for the stamped products market in the near future. India is also a promising market for the metal stamping market, as the growth of component production is anticipated to have a positive impact on the market.

Europe is projected to grow rapidly, with a 4.8% CAGR. This is because of the well-established automotive industry and the growing consumer electronics sector. The Europe region, which has stringent regulations to improve fuel economy, is witnessing growing demand for electric vehicles (EVs). The International Energy Agency (IEA) projects that sales of EVs are likely to rise to 44 million vehicles per annum by 2030. The growing demand for electric vehicles is also likely to boost the market in the upcoming years.

Key Players and Competitive Insights

The metal stamping competitive landscape is highly fragmented, with global as well as regional players. Metal stamping companies compete based on technology, capacity, and the ability to provide customized solutions.

The local players in the metal stamping market compete with global companies by offering services and customized products to the clients. The local players have the flexibility to provide customized services to the clients. At the same time, the local players have the capability to provide standardized products to major industrial machinery manufacturers, automotive OEMs, and consumer electronics manufacturers.

Ford Motor Company is an international automobile manufacturing company based in the U.S., established in 1903. The company uses metal stamping to manufacture major automobile parts such as body parts and other components. It has large manufacturing plants worldwide and emphasizes efficient manufacturing to meet its wide variety of products.

Tempco Manufacturing Company, Inc. is a U.S.-based company that provides custom metal stamping and fabrication services. The company was established in 1945 and serves industries such as automotive, aerospace, and medical. It specializes in high-quality metal components and offers flexible solutions for small and large production needs.

List of Key Companies

- AAPICO Hitech Public Company Limited

- Acro Metal Stamping

- CAPARO

- Clow Stamping Company

- D&H Industries, Inc.

- Ford Motor Company

- Gestamp

- Goshen Stamping Company

- Interplex Holdings Pte. Ltd.

- Kenmode, Inc.

- Klesk Metal Stamping Co

- Manor Tool & Manufacturing Company

- Nissan Motor Co., Ltd

- Tempco Manufacturing Company, Inc

Value Chain and Cost Analysis

The cost structure of the metal stamping market is affected by raw materials such as the cost of steel and aluminum, tooling costs, labor costs, and energy consumption. The metal stamping cost analysis reveals that tooling cost involves a high investment, particularly for large-scale production. The value chain of the metal stamping market involves raw material suppliers, tool manufacturers, stamping companies, and industries. Proper supply chain management is necessary for the smooth functioning of businesses.

Sustainability Trends

Sustainability is also becoming an important trend in the metal stamping market. Companies are adopting green strategies such as recycling, reducing waste, and reducing energy consumption through efficient processes. There is also an increasing trend towards the use of lightweight and recyclable materials, especially in the automotive sector. Furthermore, the metal stamping industry is adhering to environmental policies, encouraging the development of a cleaner, more sustainable industry.

Industry Dynamics

- April 2025: DEF Industries acquired GHI Manufacturing. The company said that the strategic acquisition will boost its manufacturing capacity and its position in the aerospace industry.

- May 2025: The European Union implemented new safety and environmental regulations for the metal stamping industry. The implementation of the regulations has had a significant impact in Europe.

- May 2024: The IMTS Conference was centered on increasing U.S. manufacturing productivity and workforce development. The main highlight was AI feedback for sheet metal stamping, created by ORNL, AutoForm, and USCAR (Ford, GM, Stellantis).

- February 2024: Sewon Precision Industry Co., Hyundai’s supplier based in South Korea, announced plans to invest $300 million in establishing a stamping plant in Rincon, GA. Once operational, the company will employ 1,600 people across its two facilities.

- February 2024: American Cadrex opened a 150,000-square-foot facility in Juarez, Mexico, expanding its total manufacturing space there to 405,000 square feet. The expansion marked the company’s largest operation.

Metal Stamping Market Segmentation

By Process Outlook (Revenue, USD Billion, 2021–2034)

- Blanking

- Embossing

- Bending

- Coining

- Flanging

- Others

By Press Type Outlook (Revenue, USD Billion, 2021–2034)

- Mechanical Press

- Hydraulic Press

- Servo Press

- Others

By Thickness Outlook (Revenue, USD Billion, 2021–2034)

- Less than & up to 2.5 mm

- More than 2.5 mm

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Automotive

- Industrial Machinery

- Consumer electronics

- Aerospace

- Electrical & Electronics

- Building & Construction

- Telecommunications

- Others

By Part Size (Maximum Finished Component Dimension) (Revenue, USD Billion, 2021–2034)

- Micro & Precision Components (≤ 50 mm)

- Small - Medium Components (> 50 mm to ≤ 300 mm)

- Large Structural Components (> 300 mm)

By Metal Type Outlook (Revenue, USD Billion, 2021–2034)

- Low Carbon Steel

- Stainless Steel

- Aluminum Alloys

- Copper and Copper Alloys

- Iconel & Nickel Alloys

- Titanium and Titanium Alloys

- Other Specialty Metal Stamping (Magnesium, Zinc, Precious Metal Alloys)

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Metal Stamping Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 256.29 billion |

|

Market Size in 2026 |

USD 266.39 billion |

|

Revenue Forecast by 2034 |

USD 380.95 billion |

|

CAGR |

4.57% |

|

Base Year |

2025 |

|

Historical Data |

2021–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD billion, and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Metal Stamping Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

Gain profound insights into the 2025 Metal Stamping Market with meticulously compiled statistics on market share, size, and revenue growth rate by Polaris Market Research Industry Reports. This thorough analysis not only provides a glimpse into historical trends but also unfolds a roadmap with a market forecast extending to 2034. Immerse yourself in the comprehensive nature of this industry analysis through a complimentary PDF download of the sample report.

FAQ's

The market for metal stamping stood at USD 256.29 billion in 2025. It is projected to grow to USD 380.95 billion by 2034.

The market is projected to account for a CAGR of 4.57% during the forecast period, 2026 to 2034.

The metal stamping market refers to the global industry involved in shaping metal sheets into components using stamping techniques for various applications.

Growth is driven by rising automotive production and industrial manufacturing expansion.

Asia Pacific led the market for metal stamping in 2025. This is due to the region’s strong manufacturing and industrial growth.

Metal stamping is important in automotive manufacturing for the high-speed production of durable and precise components.

Metal stamping utilizes a wide range of ferrous and nonferrous materials. Steel, aluminum, and copper alloys are the most common.

Stamping is a cold working process in which sheet metal is shaped by dies and presses. Casting is a process in which molten metal is poured into molds to obtain complex shapes.

Page last updated on:

Jan-2024

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements