What is the Current Market Size?

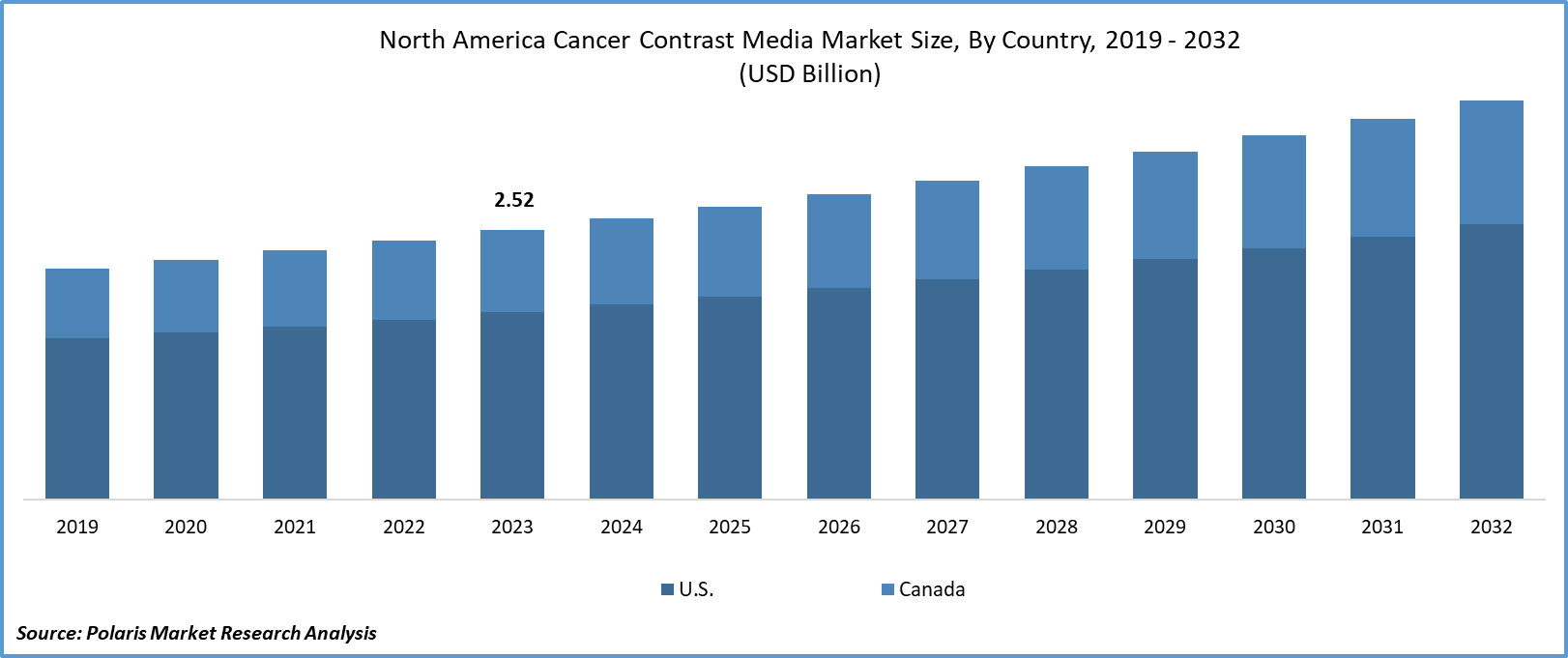

The north america cancer contrast media market size was valued at USD 2.74 billion in 2025. The market is anticipated to grow from USD 2.86 billion in 2026 to USD 4.10 billion by 2034, exhibiting the CAGR of 4.60% during the forecast period.

Market Statistics

- 2025 Market Size: USD 2.74 billion

- 2034 Projected Market Size: USD 4.10 billion

- CAGR (2026-2034): 4.60%

- U.S.: Largest market in 2025

Market Overview

The rising penetration of advanced imaging technology in developed or high-income countries and the emergence of imaging tests such as MRI (magnetic resonance imaging) and CT (computed tomography) scans as an integral part of cancer diagnosis are major factors fostering the market’s growth. In addition, several regulatory bodies, including the US Food and Drug Administration (FDA), focus on the approval of advanced medical imaging contrast agents and implement grants to ensure contrast media availability and address supply shortages.

- For instance, in August 2022, Bracco Diagnostics Inc. announced that the US FDA granted the import of Bracco’s Iodinated Contrast Medium Iomeron into the United States with the aim of addressing the shortage of iodinated contrast media.

To Understand More About this Research: Request a Free Sample Report

Furthermore, the rapid advances and emergence of photoacoustic imaging as a highly successful clinical imaging platform for the management of cancer, as well as many other health conditions, further contribute to the need for contrast agents as contrast agents are being widely used to improve photoacoustic imaging with fewer side effects, improved target specificity, and lower accumulation.

Growth Factors

Rising healthcare expenditure and focus on early diagnosis propelling the market’s growth

As healthcare expenditures in countries like the U.S. and Canada are growing significantly, leading to a drastic rise in domestic healthcare spending, both publicly funded and out-of-pocket, the demand for effective diagnosis solutions also rises. The rising focus on early diagnosis of diseases including cancer encouraging companies to bring innovations to diagnostic technologies like nuclear imaging and radiographic tests, also contributes to the demand for contrast media.

For instance, according to the American Medical Association, spending on healthcare in the U.S. rose by 2.7% in 2021 to around USD 4.3 trillion or approx. USD 12,194 per capita compared to previous year.

Rising number of MRI and CT scans in the region to drive market growth

The substantial increase in the volume of MRI and CT scans across the region has a significant impact on the cancer contrast media demand. In contrast, media are often used to improve and enhance the visibility during the scans that aid in more accurate diagnosis. Thus, the increase in the number of these scans positively influences the need for contrast media. For instance, according to a recent study on MRIs, more than 30 million MRI scans are performed by medical professionals every year in the United States.

Restraining Factors

Regulatory hurdles and side effects associated with contrast agent to hinder growth

The stringent regulatory requirements and standards and complex approval process for contrast media create significant challenges and hurdles for key market companies. Also, some contrast agents might have side effects or safety concerns with use that limit their adoption by healthcare professionals and patients as well.

Clinical Trial & Research Funding

|

Year |

Clinical Trial/Regulatory (Imaging/Contrast) |

Research/Funding (Grant Amount) |

North America Provider (Cancer Contrast Media) |

|

2021 |

FDA approves piflufolastat F-18 (PYLARIFY) for PET imaging |

NIH awards USD 2M+ for ProCA32 contrast development |

Lantheus (USA) FDA approval PET agent |

|

2022 |

FDA clears gadobutrol (Gadavist) for pediatric patients |

NCI R01 grants for imaging biomarker studies |

Bayer (USA) Gadovist pediatric clearance |

|

2023 |

FDA approves fluciclovine F-18 (Axumin) for prostate cancer |

NIH Phase 1 SBIR USD 4.5M potential (ProCA32 toxicology) |

GE Healthcare (USA) contrast expansion |

|

2024 |

Early clinical data (GE Healthcare Phase I) Manganese-based contrast |

NIH/NCI exploratory grants (PA-25-253) |

Lantheus (USA) clinical trials expansion |

|

2025 |

Phase I/II trials (Lantheus) Lu-TARGO (osteosarcoma) |

PAR-25-175: <USD 500K/year imaging research grants |

GE Healthcare USD 138M investment + Bayer Phase III QUANTI |

Report Segmentation

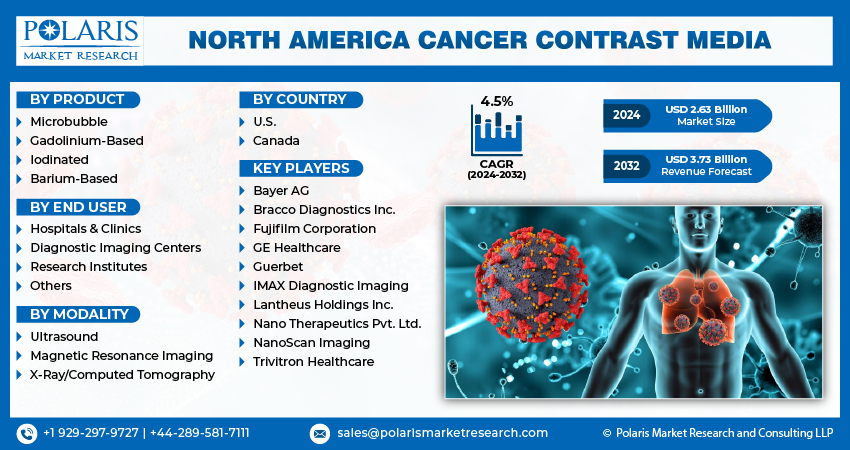

The market is primarily segmented based on product, modality, end user, and country.

|

By Product |

By Modality |

By End User |

By Country |

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

By Product Insights

Iodinated segment accounted for the largest share in 2025

The iodinated segment accounted for the largest share of the market and is likely to maintain its dominance over the North America cancer contrast media market forecast period. Segment’s dominance is due to its significant use in X-ray based imaging because of its ability to provide greater quality images of X-ray scans. Also, ionic-based contrast agents have a better propensity to dissociate into the ions on dissolution into a polar solvent, which results in the introduction of a large number of particles per molecule, thereby fostering the demand for iodinated contrast agents.

The microbubble segment is expected to witness the highest growth. Segment’s growth is accelerated by the numerous benefits associated with microbubble imaging, such as improved imaging quality of ultrasounds, real-time imaging, biocompatibility, and precise imaging. Also, this type of contrast media can effectively reflect the ultrasound waves to appear brighter and clear.

By Modality Insights

X-ray/computed tomography segment captured largest share in 2025

The X-ray/computed tomography segment captured the largest share of the market. This dominance is attributed to the rising volume of X-ray and CT scans across the region that often require different types of contrast media, such as barium-based and iodinated. Additionally, the growing awareness among the general public about the importance of early diagnosis of cancer leads to a surge in the number of imaging procedures for early disease detection, which, in turn, influences the need for contrast media, which significantly improves the accuracy of diagnostic techniques.

The ultrasound sound segment is projected to grow fastest. This growth is attributable to the rising popularity of ultrasound imaging as a non-invasive and safer imaging modality as compared to other imaging techniques available in the market. Moreover, rapid advancements in ultrasound imaging technologies, such as enhanced contrast agents and better resolution, also contributed to the segment’s growth.

By End User Insights

Hospitals & clinics segment led the market in 2025

The hospitals & clinics segment led the market. Segment’s dominance is fueled by a rapid boost in the number of patient admissions and a greater proliferation of MRI and CT scans in hospitals due to the availability of the most advanced and latest medical equipment and technologies. Various government agencies and private entities are investing heavily in healthcare infrastructure that includes the development of modern clinics and hospitals equipped with advanced state-of-the-art facilities, also supporting the growth of the market.

Regional Insights

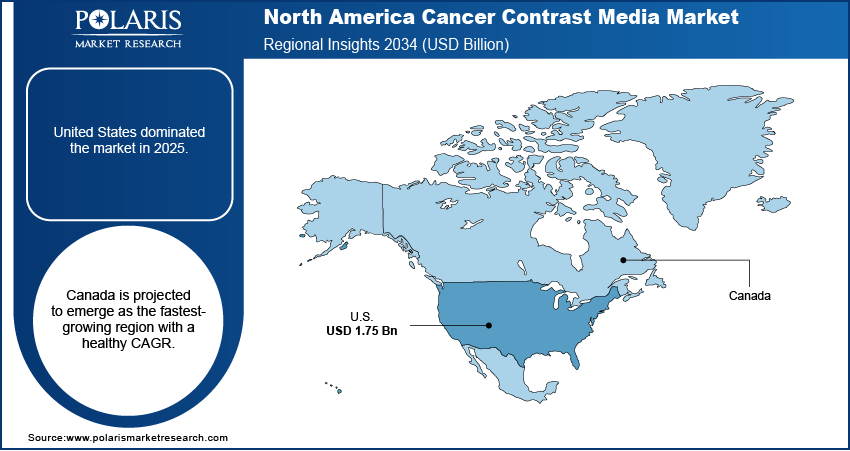

United States dominated the market in 2025

The United States dominated the region’s market. This dominance is due to a continuous increase in the incidences of cancer in the country and the robust presence of favorable government initiatives that are mainly aimed at improving early cancer diagnosis and treatment. In addition, the United States also accounts for the largest share in terms of sales of contrast media formulations with approx. USD 1.6 billion as of June 2023.

Canada is projected to emerge as the fastest-growing region with a healthy CAGR. The country’s growth is accelerated by the rising number of people diagnosed with cancer, and the focus of government authorities on promoting early cancer diagnosis influences the adoption of contrast media for accurate imaging of scans. For instance, according to a report by the Canadian Cancer Society, the number of new cancer cases was expected to be around 239,100 in 2023, and approximately 86,700 deaths were estimated in 2023. On average, 655 people in Canada were diagnosed with cancer, with 238 deaths in 2023.

Key Market Players & Competitive Insights

Increasing clinical trials and adherence to regulatory standards to drive competition

The North America cancer contrast media market is moderately competitive in nature with the robust presence of some of the world’s leading healthcare companies. Major companies in the market are competing on factors such as improving diagnostic accuracy, compliance or adherence with regulatory standards and obtaining necessary approvals, investing on clinical trials, and expanding their market presence.

Some of the major players operating in the global market include:

- Bayer AG

- Bracco Diagnostics Inc.

- Fujifilm Corporation

- GE Healthcare

- Guerbet

- IMAX Diagnostic Imaging

- Lantheus Holdings Inc.

- Nano Therapeutics Pvt. Ltd.

- NanoScan Imaging

- Trivitron Healthcare

Recent Developments in the Industry

- In June 2023, Bayer announced that the U.S. Food and Drug Administration approved Ultravist, a new iodine-based contrast agent developed for enhanced mammography. This FDA-approved solution aligns with the growing focus on supplemental imaging needs for women who are at higher risk of breast cancer.

- In July 2023, NorthStar Medical Radioisotopes announced the supply agreement with Nucleus RadioPharma for therapeutic radioisotope actiium-225. It is a high-energy alpha-emitting radioisotope that directly delivers therapeutic doses of the radiation to destroy cancer cells in the patients.

Report Coverage

The North America cancer contrast media market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, product, modality, end user, and their futuristic growth opportunities.

North America Cancer Contrast Media Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2025 |

USD 2.74 billion |

| Market size value in 2026 | USD 2.86 billion |

|

Revenue forecast in 2034 |

USD 4.10 billion |

|

CAGR |

4.60% from 2026 – 2034 |

|

Base year |

2025 |

|

Historical data |

2021 – 2024 |

|

Forecast period |

2026 – 2034 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2026 to 2034 |

|

Segments covered |

|

|

Regional scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The north america cancer contrast media market size is expected to reach USD 4.10 billion by 2034.

Key players in the market are Bayer AG, GE Healthcare, IMAX Diagnostic Imaging

The north america cancer contrast media market exhibiting the CAGR of 4.60% during the forecast period.

The North America Cancer Contrast Media Market report covering key segments are product, modality, end user, and country.

Page last updated on:

Feb-2024

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements