Plant-based Meat Market Size, Share, Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

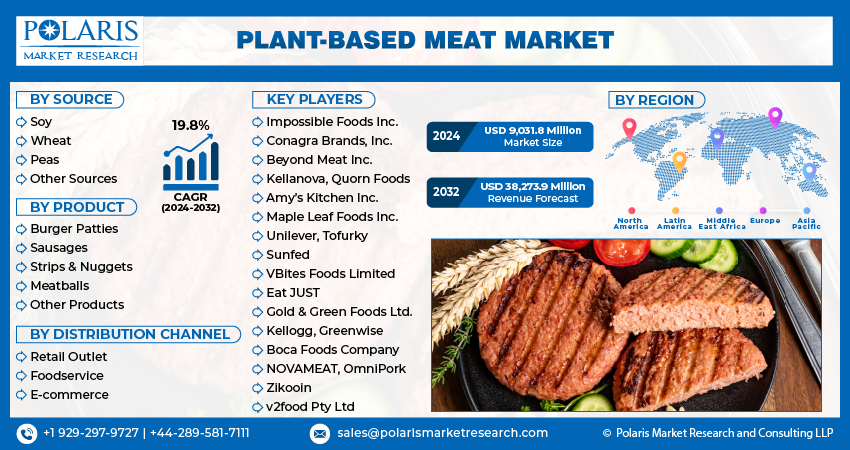

The global plant-based meat market size was valued at USD 10.77 billion in 2025, growing at a CAGR of 19.8% from 2026 to 2034. Key factors driving demand include growth in the number of flexitarian, ethical, and health-conscious consumers worldwide, strategic revisions by industry participants, and the advent of the direct-to-consumer (D2C) model.

This plant-based meat market analysis examines the impact of innovative products, storage types (frozen, refrigerated, shelf-stable), and the types of meat being substituted (beef, chicken, pork, seafood) on sales across the foodservice, retail, and online market segments. Other factors that influence brand or investment choices include regulatory standards for labeling and progress toward price parity with meat.

Key Insights

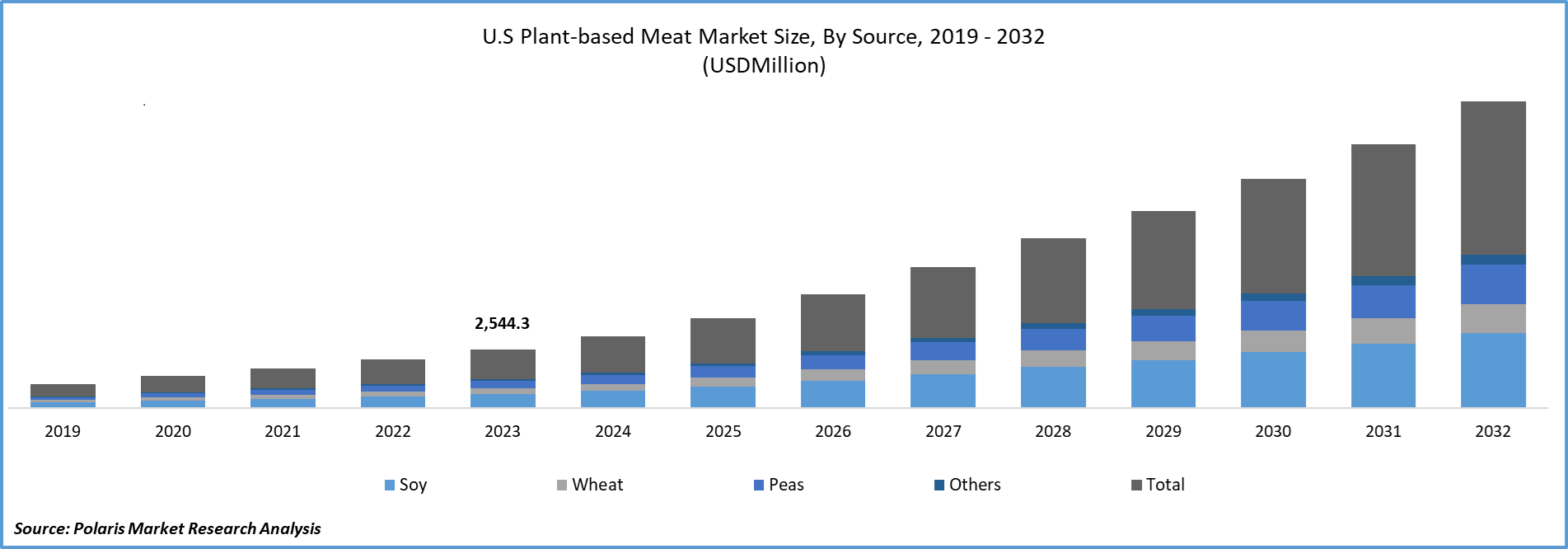

- The soy segment is expected to register a CAGR of 20.3% during the forecast period. This is due to the growing awareness of the environmental impacts of traditional meat production.

- The e-commerce segment accounted for a market share of 11.86% in 2025. This is because companies are focusing on e-commerce platforms, which are particularly preferred by millennials.

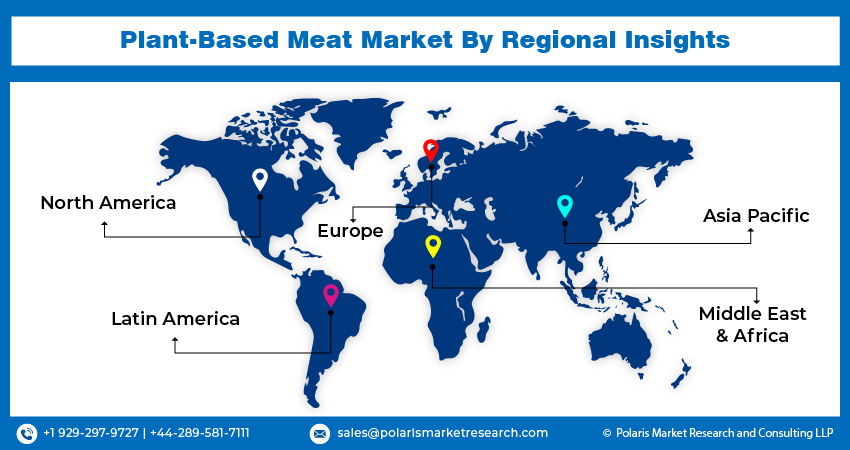

- North America accounted for 40.65% of the global plant-based meat market revenue in 2025 due to increasing health awareness and changing consumer preferences.

- The U.S. accounted for 84.55% of the revenue share in North America in 2025. High consumer awareness and demand for healthy food alternatives are driving market growth in the country.

- The Asia Pacific is expected to register a CAGR of 20.3% during the forecast period. Rising population, urbanization, and increased awareness of health and sustainability are driving the regional market growth.

Industry Dynamics

- Growth in the number of flexitarian, ethical, and health-conscious consumers worldwide is driving demand for plant-based meat.

- Strategy revisions by industry participants and the advent of the direct-to-consumer (D2C) model are fueling market expansion.

- Industry participants are trying to expand their footprint by entering into partnerships with retail chains and restaurants.

- High product prices compared to conventional meat limit the growth. The higher pricing is driven by raw materials (such as protein isolates, binders, and fats) and processing complexities. The need to store frozen and refrigerated plant-based meat products in cold conditions also adds to the pricing.

- Larger production scale, advanced recipe technology, and optimized logistics chains have been bridging this plant-based meat pricing gap. This is especially the case with high-demand meat alternatives such as burger patties and nuggets.

Market Statistics

- 2025 Market Size: USD 10.77 billion

- 2034 Projected Market Size: USD 54.49 billion

- CAGR (2026-2034): 19.8%

- North America: Largest Market Share

AI Impact on Plant-Based Meat Market

- Artificial intelligence (AI) speeds up the development of new meat alternatives. It uses large amounts of data on taste, texture, and nutritional content to create products that are almost indistinguishable from their animal-derived counterparts.

- The integration of AI helps with predictive modeling, which optimizes ingredient mixtures, formulation, and processing to enhance flavor, texture, and shelf life.

- AI-based tools for consumer insights assist in interpreting market trends and preferences. They can also analyze buying patterns to innovate and market products.

- The use of AI in plant-based meat market enables supply chain optimization and automated manufacturing. This results in less wastage of food as well as lower costs.

- During the forecast period, the use of AI-based formulation and production optimization is expected to increase companies' profitability by reducing variability across product batches.

Plant-based meat can be defined as products manufactured by using plant ingredients that mimic animal-derived meat both in terms of taste and appearance. These products are made by using a variety of sources such as peas, wheat, and soy. As they directly substitute animal meat, they are often referred to as meat products.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

This market focuses on plant-based meat analogs that mimic the look, feel, and taste of real meat products. These include burgers, sausages, chicken nuggets, and minced meat. It doesn’t cover whole plant-based proteins unless they can be classified as meat substitutes. The plant-based meat market scope also considers ingredients, processing, shaping, taste, texture, nutrient profiles, and storage life. All of these play a critical role as purchasing criteria for flexitarian consumers.

The concept of plant-based meat was originally developed to replace animal meat consumption and to curb its adverse effects on human health and the environment. The concept has garnered a lot of attention from the public and the government alike.

Inclination toward healthy lifestyles, competitive strategies adopted by key plant-based meat market participants, and favorable initiatives worldwide are driving growth. Moreover, there have been considerable investments and ventures by leading personalities worldwide, such as Bill Gates. The founder of Microsoft Corporation has invested in Beyond Meat, a major player in the industry. There have been many such instances of investments, funding, and deals in the recent past, and this trend is expected to continue over the forecast period, thus favoring the growth of the plant-based meat industry.

Many companies, both startups and established companies, are entering the market. Industry participants are trying to expand their footprint by entering into partnerships with retail chains and restaurants. Such moves aim to improve overall product availability by leveraging the pre-established distribution channels of retail chains and restaurants. Another driving factor behind rapid growth, mainly in the U.S. and Europe, is the adoption of a flexitarian lifestyle and the incorporation of plant-based foods into the diets of a sizeable number of citizens.

Drivers and Opportunities

Growth in Number of Flexitarian, Ethical, and Health Conscious Consumer Globally

The demand for plant-based meats has grown significantly due to increasing ethical consumer awareness, especially among millennials, and the rise of flexitarian consumer behavior worldwide. Flexitarians prefer limiting consumption of meat and dairy food products because of health, environmental, and ethical concerns, thereby increasing demand for plant-based alternatives. Initially, the target market was either vegetarians or vegans, but demand has grown significantly since then. The UK, along with other European countries, has observed a considerable increase in the number of vegans. The European Vegetarian Union stated that in 2021, sales of plant-based products in Germany reached USD 952.3 million. Social, as well as conventional, media have significantly contributed to increasing consumer awareness of the environmental and ethical concerns associated with animal meat production. Moreover, animal protection groups have efficiently pointed out inhumane practices taking place in the production of animal meat, hence shaping consumer behavior and fueling demand.

Strategy Revision by Industry Participants and Advent of Direct to Consumer Model (D2C)

Traditional meat manufacturers and plant-based brands are updating their approaches to capitalize on the growing plant-based meat market. Large manufacturers are entering the market through acquisitions, such as Unilever's acquisition of The Vegetarian Butcher. They are also pursuing future acquisition strategies. The plant-based meat industry also comprises agile, innovative brands, even the smaller ones, that compete with established brands, forcing them to defend market share gains while growing. Most manufacturers are turning to the Direct-to-Consumer (D2C) approach to better understand consumer behavior, facilitating personalized marketing and product development. E-commerce and social media platforms improve the strategic impact of this approach. The new approach drives market profitability and helps meet consumers’ personalized experience needs by avoiding the need to go to the marketplace.

Nutrition, Ingredient Transparency, and Consumer Trust

Even though sustainability and ethical concerns make plant-based meat a promising option, some consumers are concerned about its processing, sodium content, and new ingredients. Nutritional profiling may also vary considerably depending on the protein being substituted, the fats used, or the vitamins or minerals added. Clear labeling and ingredient transparency are therefore important for building trust, encouraging repeat purchases, and supporting long-term market growth.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Analysis

Source Analysis

Based on source, the plant-based meat market segmentation includes soy, wheat, peas, and other sources. The soy segment is projected to register a CAGR of 20.3% over the forecast period. This is due to the growing awareness of the environmental impact of traditional meat production. Consumers are increasingly looking for sustainable alternatives to animal-based products, as awareness of climate change and resource depletion rises. Soy-based plant-based meats are an emerging alternative to current meat production systems. The cultivation of soy takes fewer resources as compared to traditional livestock farming. This helps lower greenhouse gas emissions and environmental impact. Health-related factors have also contributed to the success of soy-based plant-based meat. There has been an increasing need for the preparation and processing of health- and nourishing plant-based alternatives to meet the health-conscious needs and the growing awareness of the health risks posed by excessive meat consumption. Soy-based plant-based meats are cholesterol-free and high in protein, making them an ideal choice and a key factor in growth and expansion.

The wheat segment is expected to witness a significant share during the forecast period. The segment’s growth is due to the shift toward plant-based diets as consumer awareness regarding health, sustainability, and animal welfare continues to rise. Wheat proteins, especially gluten, are key ingredients in many plant-based meats. They provide texture, structure, and protein just like conventional meats. The use of this readily available protein enables the production of a wide variety of meats with characteristics and flavors similar to those of conventional meats. The Vegetarian Butcher (Netherlands) Morningstar Farms (U.S.), Maple Leaf Foods (U.S.), VBites (UK), Quorn Foods (UK), and Garden Protein International (U.S.) are only a few of the major players in the market that use wheat as an ingredient in the production of meat-based products.

Product Analysis

In terms of product, the plant-based meat market segmentation includes burger patties, sausages, strips & nuggets, meatballs, and other products. The burger patties segment held 39.28% of the revenue share in 2025. A considerable number of companies are trying to gain share in the segment. Novel product development and partnerships with retail and smart retail chains are among the strategies adopted by leading plant-based burger patties manufacturers. Competitors have developed superior products that are in line with the traditional meat-based burgers in terms of similarities. Further, the growing demand for plant-based food also relates to the demographic changes and emerging trends associated with the food preferences of the population. Millennials and Generation Z consumers drive the demand for sustainable and responsible food. The health advantages and value for money associated with these food types also support the demand from this group. The versatility associated with plant-based food has led to the popularity of food like burger patties. Companies can develop products that resemble beef burgers in terms of taste, texture, and sponginess using food and nutritional sciences and technology.

Distribution Channel Analysis

In terms of distribution channel, the segmentation includes retail outlets, foodservice, and e-commerce. The e-commerce segment held a significant revenue share of 11.86% in 2025. Organizations are focusing on e-commerce platforms, which are particularly popular with millennials. Moreover, the convenience factor introduced by e-commerce websites, coupled with the widespread adoption of mobile phones, has also led to increased use of this distribution channel. Offering a seamless shopping experience that caters to the changing demands of the new-age consumer, online retail websites provide various plant-based meat alternatives from various brands. This helps consumers to explore and choose products that suit them. Moreover, the convenience of online shopping enables consumers to overcome the geographical constraints of conventional retail, thereby boosting the segment.

Storage Analysis

By storage, the market is segmented into refrigerated plant-based meat, frozen plant-based meat, and shelf-stable plant-based meat. Storage format is highly significant for product cost, distribution, shelf life, and consumer purchase of those products. Frozen plant-based meat alternatives have longer storage life and easier distribution in larger regions. Refrigerated products are typically located relatively close to fresh meat on supermarket shelves. However, they need strong cold-chain capabilities. Shelf-stable products still have limited applications, but they can be particularly useful in reaching those markets that lack storage or cooling facilities.

Type Analysis

Based on type, the market is segmented into chicken, pork, beef, fish, and others. Beef substitutes remain the leading category, as the products are already well known in burger and mince forms. Plant-based chicken products are rapidly gaining popularity, especially in nuggets, strips, and foodservice applications. Plant-based seafood alternatives are also gaining interest, especially given their positioning as premium products and their sustainability focus. However, challenges remain in matching taste and texture and controlling ingredient prices.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

The North America plant-based meat market accounted for a 40.65% of global revenue share in 2025. This is due to rising consumer awareness of healthy eating. With growing concerns among consumers about animal cruelty, climate change, and rising lifestyle conditions such as chronic illnesses, there is a surge in demand for plant-based meat. The region also boasts flexitarians and vegans, especially among younger generations. Food chains and retailers across North America are increasing their consumption of plant-based meat. Further, the growing use of social media and influencer campaigns has increased consumer awareness, thereby propelling industry growth.

U.S. Plant-Based Meat Market Insights

The U.S. accounted for 84.55% of the revenue share in North America in 2025. The U.S. plant-based meat market growth is driven by high consumer awareness and demand for healthier food substitutes. The growing concern about the environmental impacts of animal agriculture and the rise in flexitarian trends are propelling this industry forward. The U.S. has emerged as a leader in innovation. The country has the presence of several leading American firms in this industry, including Beyond Meat and Impossible Foods. Moreover, plant-based foods are no longer a new concept at American supermarkets and restaurants and are a mainstream choice among consumers. Online transactions are increasing further, and customer convenience and availability are being promoted. All of these factors are contributing to market growth in the country.

Asia Pacific Plant-Based Meat Market Trends

The Asia Pacific market is expected to register a CAGR of 20.3% during the forecast period, driven by rising population, urbanization, and growing awareness of health and sustainability. Cultural openness to plant-based diets in countries such as India and Buddhist-influenced regions is supporting expansion. Growing consumer interest in protein-rich diets, food security, and environmental concerns has encouraged people to adopt meat substitutes. In addition, government entities and food brands are developing infrastructure to encourage plant-based food consumption.

China Plant-Based Meat Market Overview

The demand for plant-based meat in China is increasing owing to changing eating habits and concerns about food safety. Greater awareness of health and sustainability is also contributing to market growth in the country. The awareness among the young population and the growing middle class generates a considerable demand for meat alternatives. The age-old practice among the Chinese population of consuming plant-based foods such as tofu and mock meat fosters strong cultural acceptance of these new entrants. Chinese companies, as well as foreign companies, are increasing their footholds through strategic collaborative ventures. Government support for sustainable food innovation also fuels demand for such foods.

Europe Plant-Based Meat Market Overview

The strong environmental and animal welfare awareness is driving the Europe plant-based meat market, which is likely to register a CAGR of 19.3% during the forecast period of 2026 to 2034. Countries like the UK, Germany, and the Netherlands have seen an increase in veganism and flexitarianism. European customers are highly aware of food sustainability. Therefore, their preference for plant-based options is a prominent way to reduce their carbon footprint. More importantly, the European Union has supported plant-based innovation through funding and regulatory support. Fast-moving retail chains and restaurants have expanded their plant-based options rapidly, making them available everywhere. This growing consumer interest, combined with supportive policies, fuels growth in Europe.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Regulatory and Labeling Landscape

Regulatory clarity around naming conventions (such as the use of "meat" terminology), allergens, and health or nutrition claims helps products reach the marketplace. Labeling laws for plant-based meat differ by geography, so manufacturers need to be careful when packaging items for different countries around the world. Many manufacturers are turning to clean label plant-based meat while still incorporating ingredients necessary to achieve the desired texture and shelf life.

Key Players and Competitive Analysis

The competitive landscape is characterized by intense competition from established food processors and new-age startups. To differentiate themselves in the market, leading plant-based meat market players are competing in four distinct areas: the degree to which their product resembles meat in terms of taste and texture, the degree to which they communicate effectively on their nutritional marketing messages such as protein and sodium, how well they balance foodservice, retail, and direct-to-consumer channels, as well as the ability to reduce costs to align their price points.

Companies such as Beyond Meat and Impossible Foods are market leaders in the sector through innovation and brand building. Traditional food manufacturers such as Kellogg (MorningStar Farms), Conagra Brands (Gardenburger), Unilever (Vegetarian Butcher), Maple Leaf Foods, and Amy’s Kitchen are also expanding in the plant-based foods sector because of their existing capabilities in food processing and distribution networks. Other prominent firms in the market, such as Quorn Foods, Tofurky, Gold & Green Foods, and Sunfed Foods, also market various products. New plant-based meat market players, including NOVAMEAT, v2food, OmniPork, VBites, and Eat JUST, have been capitalizing on technological innovations and local market needs to introduce new products.

List of Key Players

- Amy’s Kitchen Inc.

- Beyond Meat Inc.

- Boca Foods Company (Kraft Foods, Inc.)

- Conagra Brands, Inc.

- Eat JUST

- Gold & Green Foods Ltd.

- Greenwise

- Impossible Foods Inc.

- Kellanova

- Kellogg

- Maple Leaf Foods Inc.

- NOVAMEAT

- OmniPork

- Quorn Foods

- Sunfed

- Tofurky

- Unilever

- v2food Pty Ltd

- VBites Foods Limited

- Zikooin

Competitive Strategy Matrix: Plant-Based Meat & Alternative Proteins

| Company | Product Focus | Channel Focus | Core Region(s) | Innovation Theme |

| Beyond Meat | Burgers, sausages, ground meat | Retail, foodservice, QSR | North America, Europe | Protein formulation, taste parity, clean-label reformulation |

| Impossible Foods | Burgers, nuggets, pork & chicken alternatives | Foodservice-led, retail expansion | North America, Asia | Heme-based flavor science, sensory optimization |

| Kellogg (MorningStar Farms) | Frozen plant-based meals, meat alternatives | Mass retail | North America | Scale-driven innovation, mainstream affordability |

| Conagra Brands (Gardein) | Frozen meat alternatives, ready meals | Retail, foodservice | North America | Portfolio expansion, SKU diversification |

| Unilever (The Vegetarian Butcher) | Meat analogs (beef, chicken, deli) | Retail, foodservice | Europe, expanding globally | Culinary-led product design, flexitarian appeal |

| Maple Leaf Foods | Plant-based meat substitutes | Retail, foodservice | North America | Sustainability positioning, protein diversification |

| Amy’s Kitchen | Organic plant-based meals | Retail | North America | Clean-label, organic, comfort-food positioning |

| Quorn Foods | Mycoprotein-based meat alternatives | Retail, foodservice | Europe, North America | Mycoprotein fermentation, nutritional differentiation |

| Tofurky | Deli slices, sausages, holiday products | Retail, natural food stores | North America | Plant-forward simplicity, brand authenticity |

| Gold & Green Foods | Oat- and legume-based proteins | Retail, foodservice | Europe | Local sourcing, allergen-free formulations |

| Sunfed | Whole-food plant proteins | Retail | Australia, New Zealand | Minimal processing, clean ingredients |

| Eat JUST | Cultivated meat, plant-based eggs | Foodservice, strategic partnerships | North America, Asia | Cellular agriculture, alternative protein platforms |

| NOVAMEAT | 3D-printed whole-cut meat alternatives | B2B, foodservice | Europe | Structuring technology, fiber mimicry |

| OmniPork | Pork alternatives tailored to Asian cuisine | Foodservice, retail | Asia Pacific | Regional flavor localization |

| v2food | Beef and sausage alternatives | Retail, foodservice | Australia, Asia Pacific | Nutrition-first reformulation |

| VBites | Meat, cheese, ready meals | Retail, foodservice | Europe | Vertical integration, brand-led innovation |

| Boca Foods (Kraft Heinz) | Frozen meat alternatives | Retail | North America | Legacy brand leverage, cost efficiency |

| GreenWise | Private-label plant-based foods | Retail (private label) | North America | Value positioning, retailer alignment |

| Zikooin | Cultured meat R&D | B2B, pilot-scale | Asia | Lab-grown protein innovation |

| Kellanova | Adjacent plant-based snacking & foods | Retail | Global | Portfolio adjacency, functional innovation |

Source: Polaris Market Research Analysis

Plant-Based Meat Industry Developments

In August 2025, Eat Just launched its new plant-based chicken line under the JUST Meat brand. It features original, buffalo, and sesame ginger flavors. Spotted at Sprouts and listed on H-E-B, the products offer 18g of protein and quick frozen preparation.

In August 2025, Juicy Marbles partnered with Revo Foods to launch Kinda Salmon, a raw, plant-based salmon filet featuring 13g of protein and omega-3s. Released in the U.S. on August 4, the product followed the sellout success of Kinda Cod.

Market Segmentation

By Source Outlook (Revenue, USD Billion, 2021–2034)

- Soy

- Wheat

- Peas

- Other Sources

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Burger Patties

- Sausages

- Strips & Nuggets

- Meatballs

- Other Products

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Chicken

- Pork

- Beef

- Fish

- Others

By Storage Outlook (Revenue, USD Billion, 2021–2034)

- Refrigerated Plant-based Meat

- Frozen Plant-based Meat

- Shelf-stable Plant-based Meat

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Retail Outlet

- Foodservice

- E-commerce

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Plant-Based Meat Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 10.77 billion |

| Market Size in 2026 | USD 12.86 billion |

| Revenue Forecast by 2034 | USD 54.49 billion |

| CAGR | 19.8% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Plant-Based Meat Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Plant-based Meat Market FAQ's

The plant-based meat market is projected to reach USD 54.49 billion by 2034. It is expected to account for a CAGR of 19.8% between 2026 and 2034.

The refrigerated plant-based meat storage format is expected to witness the fastest growth due to increased availability in supermarkets and grocery stores.

The pricing of these foods has mainly been influenced by their production costs, including specialized ingredients and processing technology.

Industry participants are focusing on partnerships with retail chains and restaurants to expand their operations in these regions.

E-commerce is highly attractive to new entrants. It is primarily used by millennials and is preferred for the convenience it offers and the direct-to-consumer platforms that provide insights into consumer data.

Download Sample Report of Plant-based Meat Market

Please fill out the form to request a customized copy of the research report.