Polymer Foam Market Size, Share, Global Analysis Report, 2026-2034

REPORT DETAILS

Market Statistics

Overview

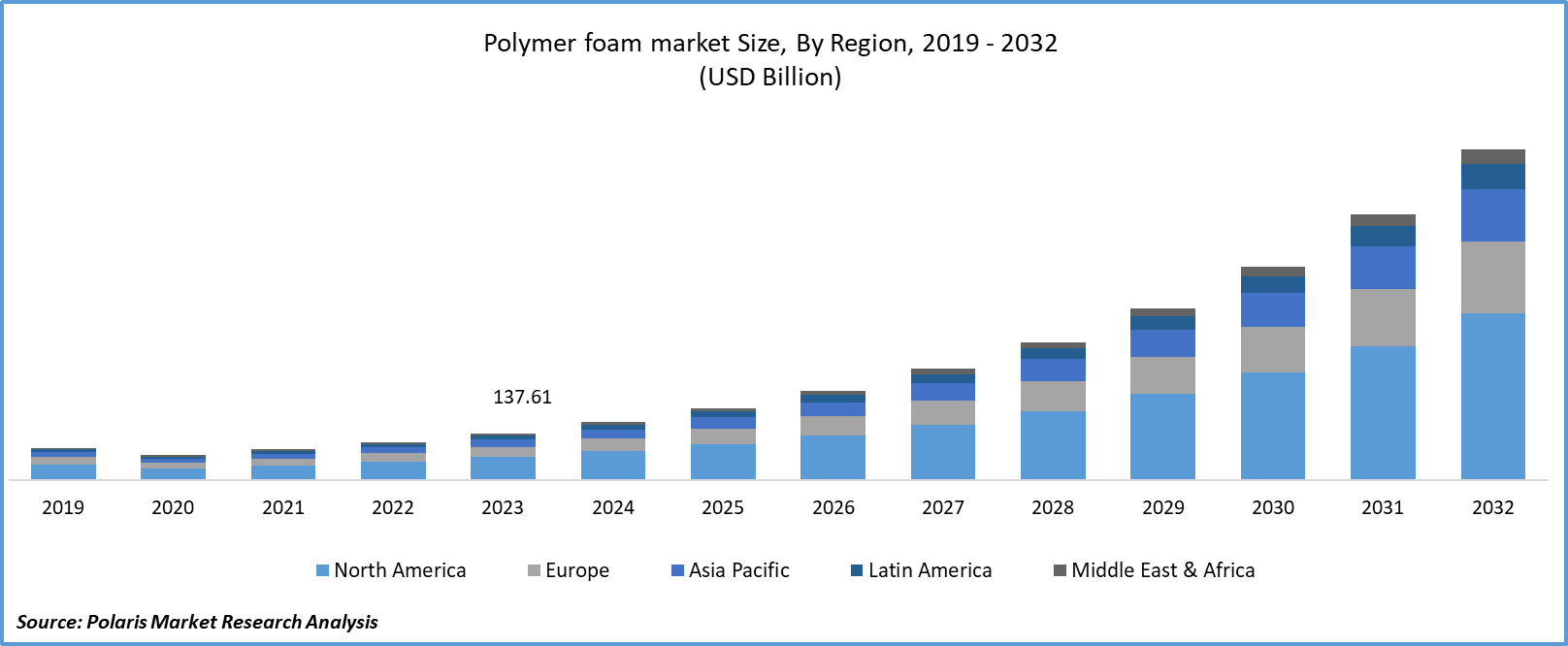

The global polymer foam market is estimated around USD 207.12 million in 2025, with consistent growth anticipated during 2026–2034. The market is projected to grow at 24.4% CAGR during the forecast period propelled by expansion of protective and specialty packaging applications and automotive light weighting and efficiency-driven material substitution.

Future Demand Scenarios

- Base scenario: Demand continues to increase in the construction and insulation, automotive light weighting, and industrial packaging sectors, while concurrent growth in energy-efficient and performance-grade foam applications provides incremental gains.

- Upside scenario: Advanced polymer foams are adopted more quickly in EV platforms, green buildings, cold-chain logistics, and sustainable insulation systems-a combination that accelerates the market expansion.

- Conservative scenario: Slower construction activity and softer automotive production reduce demand for foam; delayed capacity additions and substitution pressure from alternative materials limit volume growth.

Key Insights

- The polyurethane foam segment held the largest share of the market in 2025 due to the flexibility of polyurethane foam in flexible and rigid formats.

- Polystyrene foam is expected to grow rapidly due to its lightweight structure and strong insulating properties

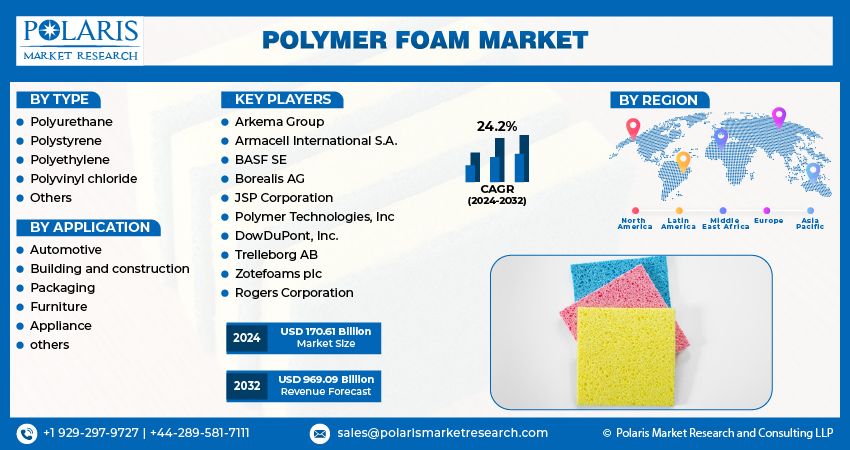

- The Asia Pacific dominated the market in 2025 driven by the continuous construction activity in China, India, and Southeast Asia, coupled with growing manufacturing and packaging.

- North America is anticipated to witness the highest growth. This is due to the renovation cycles, insulation retrofitting programs, and consistent automotive production volumes.

Industry Dynamics

- Rising Demand for Energy-Efficient Buildings

- Expansion of Protective and Specialty Packaging Applications

- Automotive Lightweighting and Efficiency-Driven Material Substitution

- Raw Material Price Volatility and Feedstock Exposure

Market Statistics

- 2025 Market Size: USD 207.12 million

- 2034 Projected Market Size: USD 1,474.56 million

- CAGR (2026-2034): 24.4%

- Asia Pacific: Largest market in 2025

What is Polymer foam and Why It Matters

Polymer foams support lightweight insulation, cushioning, and energy-absorption needs across construction, automotive, packaging, and consumer goods. The growth of the polymeric foam market is supported by the availability of materials with a controlled density, thermal, and mechanical performance, resulting in a continuous growth of the polymeric foam market. The increasing demand from construction insulation, interior applications of autos, and protective packaging applications is expected to foster growth in the polymeric foam market, leading to a rise in the polymeric foam market volume.

Polyurethane Foam vs Polystyrene Foam – Key Differences

-

Polyurethane Foam

Polyurethane foam occupies the higher-end side of the polymer foam industry, manufactured using definite chemical reactions between polyols and isocyanates. The prime benefit of polyurethane foam primarily focuses on its versatility in foam composition. It can be designed in terms of rigidity, elasticity, insulation properties, and overall cushioning properties according to certain applications in the fields of construction, automobile cushioned seating, bedding, refrigerated storage, and industrial cushioning. This widens its applications in the polymer foam industry as a high-end product in the overall polymer foam market.

-

Polystyrene Foam

Polystyrene foam represents a more standardized segment, driven by the expansion or extrusion process of polystyrene resins, which creates foams that have closed cells. They are price-efficient, strong, and good insulators. With their applications in the construction industry, protective packaging, or cold-chain logistics, where their high-volume efficiency matters rather than their formulation. Polystyrenes remain less complex than polyurethane foams in their industry structure, due to which they remain viable options for an array of markets sensitive to their pricing. In the upcoming market structure projection, the growth rate for polystyrene foams is tied to the cyclical development in the construction industry or the corresponding packaging markets.

Polymer Foam Market - Type-wise Comparison

| Foam Type | Key Characteristics | Major Applications | Cost Position | Market Role |

| Polyurethane Foam | High formulation flexibility, broad density range, good insulation and cushioning properties | Building insulation, automotive seating, bedding, refrigeration, furniture | Medium–High | Performance-driven, largest value contributor |

| Polystyrene Foam | Low weight, rigid construction, effective thermal insulation | Construction insulation, protective packaging, cold-chain logistics | Low–Medium | Volume-driven, cost-efficient segment |

| PVC Foam | High strength/weight ratio, Resistant to moisture, Stability | Marine panels, wind blades, construction boards, transportation | Medium | Structural and load-bearing applications |

| Phenolic Foam | High resistance to fire, low smoke evolution, high thermal efficiency | Fire-rated insulation, industrial buildings, HVAC systems | Medium–High | Safety- and regulation-driven niche |

| Polyolefin Foam | Chemical Resistant: When a material is resistant to chemicals. | Automotive parts, sports equipment, packaging, insulation | Medium | Light weighting and durability-focused uses |

| Melamine Foam | Open-cell structure, sound absorption, heat resistance | Acoustic panels, cleaning products, industrial soundproofing | High | Specialty acoustic and thermal applications |

| Others | Application-specific properties, blended or specialty formulations | Medical, aerospace, electronics, niche industrial uses | Variable | Innovation-led, small-volume segments |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

Drivers & Opportunities

Growing Demand for Energy Efficient Buildings

Stringent energy conservation codes and rising prices for heating and cooling are fueling interest in efficient insulation materials. According to European Union policy, any amendments to the Energy Performance of Buildings Directive adopted in 2023 must ensure that buildings are emission-free after 2026 if they are public buildings and after 2028 for all other buildings, with gradually increasing demands for old buildings to achieve climate neutrality by 2050. This impacts foam insulation specifically as a need that is fueled by commercial and residential building activities. Polymer foams help conserve energy through better thermal performance of walls, roofs, and foundations.

Expansion of Protective and Specialty Packaging Applications

Growth in e-commerce and global goods movement increases the risk of product damage during transportation. According to a report by the International Trade Administration, the global B2C ecommerce sales projected to reach USD 5.5 trillion by the end of 2027, growing at a CAGR of 14.4%. This translates into a greater need for polymer foam packaging materials that have the abilities to be impact-resistant and dimensionally stable. Shock-absorbing packaging foam helps resist shock or vibrations that occur during multiple shipments. The use of foam cushioning helps cut breakage and return rates for producers. The rising need for performance-based packaging has made polymer foam a preferred choice for packing delicate items.

Automotive Light weighting and Efficiency-Driven Material Substitution

Car manufacturers are challenged to enhance fuel economies for mileage and the range for electric cars, in addition to meeting the permissible emissions. Car foam materials replace heavier components without affecting comfort and safety. NVH foams reduce noise and vibrations, and reduce weight, hence fulfilling the objectives of weight reduction. EV thermal management foam helps regulate battery temperatures and protect critical components. These requirements increase polymer foam use across interior, structural, and electric vehicle applications.

Restraints & Challenges

Price Volatility of Raw Materials and Feedstock Exposure

Volatility in material price across petrochemical feedstocks that shape cost structures impede market growth. Polyols, isocyanate, and styrene continue to be susceptible to crude-linked pricing cycles, as well as supply disruption and regional imbalances. These changes directly feed into the manufacturing economy and inhibit margin predictability. Procurement planning becomes more onerous, especially for smaller producers with less hedging flexibility.

Environmental Regulations, Recycling Constraints, and Waste Management Pressures

Environmental regulations on polymer foam increasingly restrain the market through tighter controls on the level of disposability and recyclability. There are challenges in managing foam waste arising from low material density and a generally fragmented recovery system. The paths to recycling polymer foam are available, yet there is limited quantitative scale and consistency in different regions. Increasing sustainability expectations accelerate compliance costs and hinder market growth while slowing adoption in regulation-sensitive applications.

Regulatory Mapping

| Regulation / Policy | Region | Foam Types Directly Impacted | Core Compliance Focus | Explicit Market Impact |

| EU Waste Framework Directive (2008/98/EC) | Europe | EPS, XPS, PU | Recycling targets, waste hierarchy, EPR obligations | Increases end-of-life compliance costs for polymer foam packaging and construction insulation; constrains low-recyclability foam formats |

| EU Single-Use Plastics Directive (EU) 2019/904 | Europe | EPS (primarily) | Restrictions and bans on disposable plastic products | Direct demand suppression for EPS food containers and disposable packaging foams |

| REACH Regulation (EC No 1907/2006) | Europe | PU, specialty foams | Registration and restriction of isocyanates, flame retardants, additives | Raises formulation compliance costs and limits use of certain petrochemical feedstocks |

| EU Construction Products Regulation (CPR) | Europe | EPS, XPS, PU | Fire performance, emissions, sustainability declarations | Tightens certification burden for insulation foams used in buildings |

| EU Circular Economy Action Plan | Europe | All foam types | Recyclability, material recovery, lifecycle reporting | Forces redesign of polymer foams toward mono-material or recyclable systems |

| US EPA Solid Waste Disposal Act (RCRA) | United States | EPS, PU | Landfill disposal standards, waste handling | Raises disposal and logistics costs for foam waste management |

| Toxic Substances Control Act (TSCA) | United States | PU | Risk evaluation of isocyanates and blowing agents | Drives reformulation and substitution in polyurethane foam systems |

| Extended Producer Responsibility (EPR) Laws | US, EU, Asia Pacific | EPS, packaging foams | Producer-funded waste collection and recycling | Shifts post-consumer waste costs directly to foam manufacturers |

| China Plastic Pollution Control Action Plan | China | EPS | Restrictions on non-degradable plastic foams | Limits EPS packaging growth and accelerates material substitution |

| India Plastic Waste Management Rules (Amended) | India | EPS, PU packaging foams | Collection, recycling mandates, EPR compliance | Raises compliance and recovery costs for foam packaging suppliers |

| Global ESG Disclosure Standards (GRI / ISSB-aligned) | Global | All foam types | Emissions, waste, material traceability | Penalizes high-waste foam portfolios and favors recyclable or bio-based alternatives |

Source: Polaris Market Research Analysis

Emerging Opportunities

Bio-Based and Sustainable Foam Innovations

The rising innovatory developments in bio-based and sustainable foam technology are expected to create new market trends. In November 2025, Storopack launched a newly developed bio-based foam packaging material made from renewable materials. Bio-based polymer foam formulations containing renewable bio-polyols make way for the growth of sustainable polyurethane foam offerings without compromising thermal insulation and strength properties. The application of the technology is increasing in the subject market of Europe and North America, which is driven by regulation and buying decisions that support the usage of material that has less impact.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segmental Insights

This report provides granular coverage of the polymer foam market by type and application, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Type

-

Polyurethane Foam

The major market share of polymer foams is dominated by polyurethane foams due to their adaptability in flexible and rigid foams. This combination of cushioning properties, insulation properties, and an affordable cost has led to the increased usage of polyurethane foams. In the case of rigid insulation panels, any slight deviation in the density could impact the thermal resistance and, accordingly, the energy efficiency.

-

Polystyrene Foam

Polystyrene foam holds a significant position, supported by its light structure and strong insulating properties. Expanded and extruded polystyrene grades are heavily used in packaging and construction, where dimensional stability and moisture resistance are critical. In building insulation, compressive strength consistency determines long-term load-bearing performance under flooring and roofing systems.

-

PVC Foam

PVC foam fills a specific type of niche, which requires strength, chemical resistance, and fire retardancy. Other applications include public transport fitments, industrial panels, and signs. In public transport and railways, a regular foam cell structure is important for vibration dampening and sound insulation, making consistency a crucial criterion for foam selection.

-

Phenolic Foam

Phenolic foam is classified as a high-end type of insulation owing to its low smoke evolution and excellent fire resistance properties. Its usage is mostly observed in the case of commercial buildings, industrial setups, and transport systems that follow harsher regulations in terms of firefighting safety measures. Even slight changes in the composition of the resin affect its brittleness and thermal conductivity.

-

Polyolefin Foam

Polyolefin foam remains increasingly popular as it has the properties mentioned above. Polyolefin foam has applications in automotive parts, sport equipment, and protectively packing various products. The impact absorption properties have high dependence on the uniform cellular structure as it contributes directly to the safety applications of the foam.

-

Melamine Foam

Melamine foam serves a highly specific functional role, especially in acoustic absorption. The open cell structure of melamine foam makes it useful for sound damping without using chemicals. The demand is also tied to interior noise control.

-

Others

Other foam materials, such as rubber foams and specialty foam hybrids, fill specific industry demands that mandate specific mechanical and thermal performance. These foams are chosen based on performance matching, and not economic volume principles.

The report evaluates each grade by market size, share, growth rate, and indicative pricing differentials.

By Application

-

Automotive

The automotive segment represents a major consumption channel for polymer foams, driven by the need for light weighting, comfort, or sound absorption. Polymer foams have wide applications in seating, headliners, dashboard roofs, and insulation parts. Even marginal increases in foam weight can affect fuel efficiency and electric vehicle range calculations.

-

Building and Construction

Building and construction account for a substantial share due to insulation, sealing, and structural applications. In addition, polymer foams provide thermal efficiency, moisture regulation, and sound reduction properties. On the contrary, in building insulation applications, the degradation process independently influences energy costs over the building life cycle.

-

Packaging

Packaging applications rely on polymer foams for shock absorption, thermal buffering, and product protection. Electronics, appliances, and temperature-sensitive goods depend on foam integrity to prevent transit damage. Variability in foam density can increase breakage risk and logistics-related losses.

-

Furniture

Furniture applications are centered on comfort, durability, and shape retention. Flexible foams are largely used for making seats and beds based on the compression set values. Irrelevance of foam resilience affects time adjustment and user satisfaction.

-

Appliance

Appliances use polymer foams for insulation purposes, sound damping, and structural support. Refrigeration units, in particular, depend on foam insulation efficiency to meet energy performance standards. Minor formulation changes can shift thermal conductivity and regulatory compliance margins.

-

Others

Other applications include medical equipment, sporting goods, marine, and industrial machinery. The demand for these applications is influenced by performance rather than widespread volume consumption.

Application Segment Analysis

| Segment | Market Share Ranking | Fastest-Growing Indicator | Key Driver |

| Automotive | High | No | Lightweighting demand, NVH control, and comfort requirements in ICE and EV platforms |

| Building and Construction | High | Yes | Thermal insulation mandates, energy efficiency regulations, and urban infrastructure expansion |

| Packaging | Medium | No | Shock protection needs for electronics, appliances, and temperature-sensitive goods |

| Furniture | Medium | No | Demand for comfort, durability, and long product lifecycle in seating and bedding |

| Appliance | Medium | Yes | Energy efficiency standards and insulation performance in refrigeration and household appliances |

| Others | Low | No | Specialized performance needs in healthcare, marine, sports, and industrial equipment |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

Asia Pacific Polymer Foam Market Assessment

Asia Pacific represented the largest market share in the polymer foam industry in 2025 due to steady construction progress in China, India, and other countries within the Asia Pacific region. According to data from the International Trade Administration, China remains the largest construction market globally at present, with a market value of around USD 4.82 trillion in 2025. In regards to the Asia Pacific market for polymer foams, high-volume usage within the industry can be linked to its applications in the fields of insulation, cushioning, as well as protective packaging. China drives the overall market for polymer foams within Asia Pacific due to ongoing large-scale residential as well as infrastructure projects, thus solidifying market research for the market in China. Secondly, the market within the Indian subcontinent is driven by urban development, thus indicating steady growth within the Indian market for polymer foams.

North America Polymer Foam Market Insights

North America represents a mature yet stable market, fueled by renovation cycles, programs of retrofitting with insulations, and vehicle manufacturing. Figures from the National Association of Home Builders show that the number of remodeling businesses in the US has almost been seen to double in the last 25 years, rising from less than 69,000 in the year 2000 to more than 128,000 in the first quarter of 2025. In North America, there are steady sales of polymer foams in the transportation, residential, and commercial markets; here, the level of consistent performance and dictates influence foam choice. In the US, the replacement market and energy-saving modifications have driven the U.S. polymer foam market.

Europe Polymer Foam Market Overview

Europe’s polymer foam market operates within a framework defined by environmental compliance and sustainability-driven material shifts. In November 2025, the European Commission launched the EU Bioeconomy Strategy 2025, which emphasizes that the bioeconomy is a central component of Europe’s industry, sustainability, and competitiveness toolkit, covering all biological resource-using industries, from manufacturing, energy, and materials, through to construction. The Europe polymer foam market holds preference for compositions that target emissions goals, recyclability, and energy-efficient-building norms. The usage of biological and lower-emission types is also steadily growing, making sustainable polymer foam Europe a focus point for development and consumption-compliant purchases related to construction and automotive interior segments.

Rest of the World Polymer Foam Market Snapshot

Latin America, the Middle East, and Africa exhibit gradual growth patterns, driven by investments in infrastructure, urbanization, and increasing industry growth. The industry in Latin America is growing due to investments in the construction industry and appliance manufacturing. For the market in Middle East Africa, growth is driven by commercial construction projects and investments in the logistics industry.

Heat Map Analysis

| Region | Demand Intensity | Construction & Infrastructure Pull | Industrial & Packaging Usage | Regulatory Influence | Growth Momentum |

| Asia Pacific | Very High | Very High | High | Medium | High |

| North America | Medium–High | Medium | Medium–High | Medium–High | Medium |

| Europe | Medium | Medium | Medium | Very High | Medium–Low |

| Rest of the World | Medium | Medium–High | Medium | Low–Medium | Medium |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The polymer foam market is moderately consolidated, with polymer foam market players competing across a broad range of foam chemistries and end-use applications. The competitive dynamics of polymer foam are driven by the presence of giants like Pfizer, Johnson & Johnson, and Dow Inc., which concentrate on capacity enhancement, innovation, and sustainable materials derived through focusing on biologically based raw materials and circular economy projects to cater to end-use industry demands. Competitive differentiation factors evolve around light weighting, thermal and acoustic insulation performance, recyclability, and low VOC materials, along with a focus on biologically based raw materials and circular economy projects.

Key companies operating in the global polymer foam market include Armacell International S.A., Arkema Group, BASF SE, Borealis AG, Dow Inc. / DowDuPont Inc., Fritz Nauer AG, JSP Corporation, Koepp Schaum GmbH, Polymer Technologies, Inc., Recticel NV/SA, Rogers Corporation, Sealed Air Corporation, SEKISUI ALVEO AG, Synthos S.A., and Trelleborg AB.

Key Players

- Armacell International S.A.

- Arkema Group

- BASF SE

- Borealis AG

- Dow Inc. / DowDuPont Inc.

- Fritz Nauer AG

- JSP Corporation

- Koepp Schaum GmbH

- Polymer Technologies, Inc.

- Recticel NV/SA

- Rogers Corporation

- Sealed Air Corporation

- SEKISUI ALVEO AG

- Synthos S.A.

- Trelleborg AB

Sustainability, Regulations & Innovation Trends

Sustainability

Sustainability is moving from a positioning theme to an operating requirement across the sustainable polymer foam market. Producers are shifting feedstock strategies toward renewable inputs, lowering caron intensity across formulation stages, and tightening material efficiency at scale. The demand for green foam materials is on the upswing, given the growing trend to associate purchases with the attainment of energy performance goals in the construction, automotive, and packaging industries. Sustainability has made its impact felt on material choices and capacity developments.

Regulations

Regulatory pressure is intensifying around emissions, waste handling, and end-of-life recovery. Regionally, there are preferences for recyclable polymer foams, forcing foam producers to reformulate to meet demands for greater environmental transparency. Fire retardancy regulations, construction requirements, and chemical use laws also impact formulation decisions, particularly for applications involving thermal insulation and transport. Time to compliance and certification costs are emerging as major filters for supplier choices.

Innovation Trends in the Polymer Foam Market

| Innovation Area | Description | Market Implication |

| Recyclable Polymer Foams | Foam material developments compatible with mechanical and chemical recycling processes | Expands adoption in regulated markets and supports circular economy procurement. |

| Green Foam Materials | Bio-based polyols, renewable additives, and raw materials with a low impact | Strengthens positioning within the sustainable polymer foam market |

| Low-Emission Foaming Agents | Evolution towards Foaming Technologies with Lower VOC Emissions & GHG Footprints | Enhance regulatory compliance and reduce life cycle environmental footprint. |

| Lightweight High-Performance Designs | Optimization of cell structure regarding strength, insulation, and weight savings | Drives demand in construction, automotive, and energy-efficient applications. |

| Energy-Efficient Manufacturing | Process improvements to eliminate heating, pressuring, and material waste | Lower operating costs, sustainability targets supported |

| Sustainability-Linked Product Qualification | Integration of ESG and Lifecycle Metrics within the processes of customer validation | Increasing supplier differentiation and long-term contracting possibilities |

Source: Polaris Market Research Analysis

Industry Developments

December 2025: BASF developed a new low VOC catalyst named Lupragen N-208, specifically formulated for use in polyurethane foam production to help manufacturers meet stricter indoor-air quality and sustainability standards. This product launch contributed to the polymer foams market by offering a catalyst solution that reduced volatile organic compound emissions from foam fabrication

June 2025: Arkema, a major specialty chemicals company, announced a strategic partnership with LG Chem to develop and commercialize polymeric insulation materials for the building and construction industry. The collaboration leverages Arkema’s expertise in high-performance polymers alongside LG Chem’s advanced battery technology to create innovative insulation solutions.

May 2025: Borealis invested over USD 110 million to expand its production capacity for recyclable, lightweight polymer foam solutions using Daploy High Melt Strength polypropylene (HMS PP) at its Burghausen, Germany facility. The investment aimed to triple the company’s supply capability for fully recyclable foam material to meet growing global demand for sustainable foam applications.

January 2025: the European Union (EU) introduced new regulations for insulation materials, including expanded polystyrene (EPS) and extruded polystyrene (XPS) foams. The updated rules set stricter emission limits for these foams, aiming to lower greenhouse gas emissions and enhance energy efficiency in buildings.

August 2024: Covestro, a global polymer producer, completed the acquisition of US-based foam manufacturer Icynene-Lapolla. This move expanded Covestro’s footprint in the spray foam insulation market, strengthening its position as a key supplier of insulation materials for the construction sector.

Polymer foam Market Segmentation

By Type Outlook (Revenue, USD Million, 2021-2034)

- Polyurethane Foam

- Polystyrene Foam

- PVC Foam

- Phenolic Foam

- Polyolefin Foam

- Melamine Foam

- Others

By Application Outlook (Revenue, USD Million, 2021-2034)

- Automotive

- Building and constructions

- Packaging

- Furniture

- Appliance

- Others

By Regional Outlook (Revenue, USD Million, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Polymer foam Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 207.12 Million |

| Market Size in 2026 | USD 257.42 Million |

| Revenue Forecast by 2034 | USD 1,474.56 Million |

| CAGR | 24.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Polymer Foam Market FAQ's

The global market size was valued at USD 207.12 million in 2025 and is projected to grow to USD 1,474.56 million by 2034.

The?Asia Pacific region holds the largest share in the polymer foam market, supported by sustained construction momentum across China, India, and Southeast Asia, alongside expanding manufacturing and packaging activity.

Automotive is the primary application due to rising requirements for lightweighting, comfort, and noise control.

A few of the key players in the market are Armacell International S.A., Arkema Group, BASF SE, Borealis AG, Dow Inc. / DowDuPont Inc., Fritz Nauer AG, JSP Corporation, Koepp Schaum GmbH, Polymer Technologies, Inc., Recticel NV/SA, Rogers Corporation, Sealed Air Corporation, SEKISUI ALVEO AG, Synthos S.A., and Trelleborg AB

Key factors include rising demand for energy-efficient buildings coupled with expansion of protective and specialty packaging applications.

The global market is projected to register a CAGR of 24.4% during the forecast period.

Download Sample Report of Polymer Foam Market

Please fill out the form to request a customized copy of the research report.