Polysilicon Market Size, Share, Growth | Industry Trends, 2026-2034

REPORT DETAILS

Market Statistics

Polysilicon Market Overview

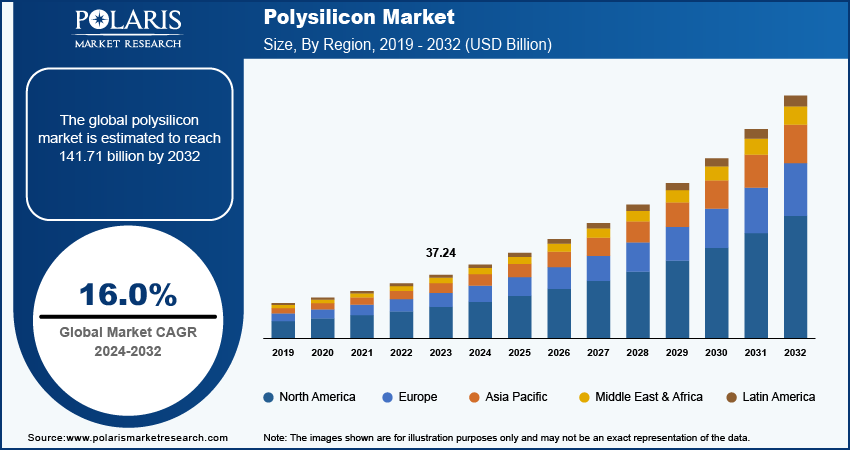

The global polysilicon market size was valued at USD 50.52 billion in 2025 and is forecasted to register a CAGR of 16.4% from 2026 to 2034. Growth is driven by increasing demand from the solar photovoltaic and semiconductor industries. Also, government policies and incentives, such as subsidies and tax credits, play a key role in propelling the demand for polysilicon in the solar sector.

Key Takeaways

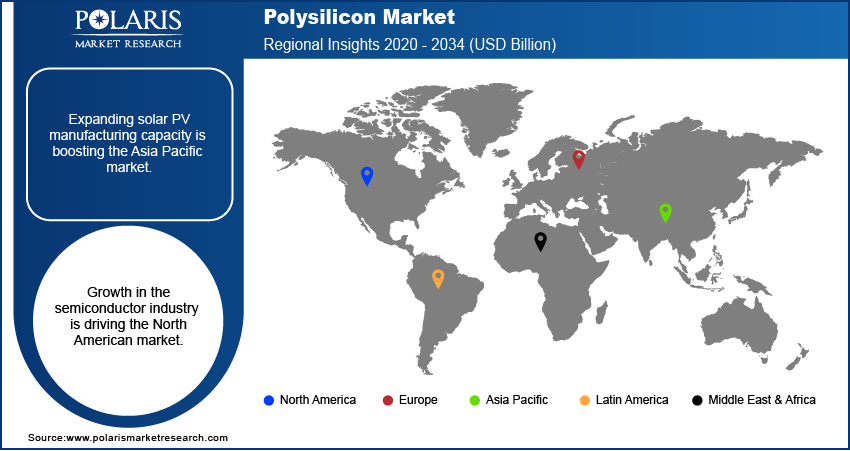

- Asia Pacific polysilicon market dominated the market with a 62.65% revenue share in 2025. The regional market is led by China’s strong manufacturing and exports, supported by low-cost labor and abundant coal resources.

- North America polysilicon CAGR is expected to be the highest at 17.5% from 2026 to 2034. Growing demand from the solar photovoltaic sector contribute to the regional market expansion.

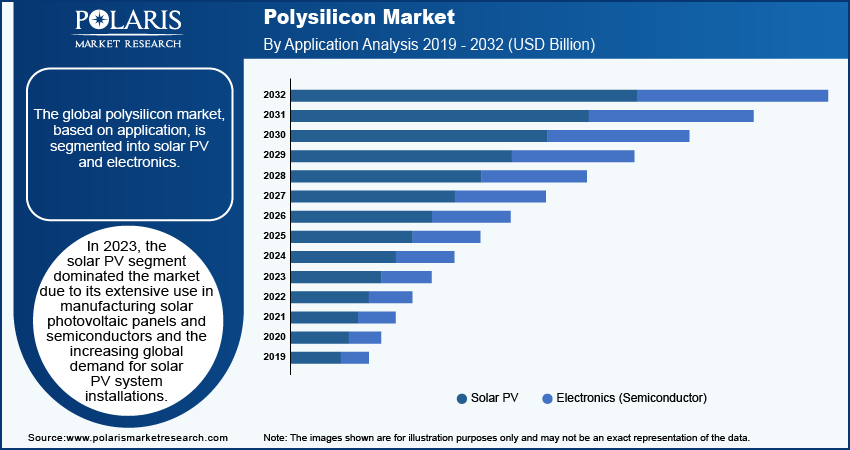

- In 2025, the solar PV segment accounted for the largest share of 89.4%. It is due to its extensive use in manufacturing solar photovoltaic panels and semiconductors.

- The monocrystalline solar panels sub-segment held a significant market revenue share of 74.5%. This is owing to the industry’s shift towards high-efficiency, mono-based technologies.

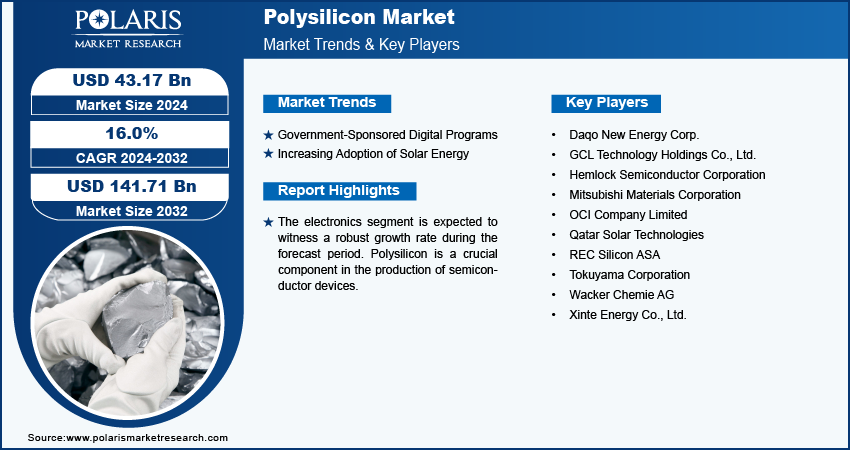

- The electronics segment is expected to grow at a 16.0% CAGR during the forecast period. The rising demand for electronic devices, such as smartphones and computers, drives the segment growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The industry is witnessing rapid growth driven by government policies and flagship programs aimed at boosting digitalization.

- The increasing use of 5G networks, IoT, cloud computing, and electric vehicles has driven demand for electronics grade polysilicon, which offers the highest purity for semiconductor wafer production.

- The growing adoption of solar energy is a significant driver of polysilicon demand.

- The rapid development of electronics and allied industries, driven by the rise of 5G and IoT, is expected to drive demand for polysilicon in the coming years.

- Fluctuating raw material prices are a major polysilicon market restraint.

- Volatility in metallurgical-grade silicon prices, energy costs, and logistics can affect polysilicon raw material prices, thereby impacting production costs and overall market pricing and margins.

Market Statistics

- 2025 Market Size: USD 50.52 billion

- 2034 Projected Market Size: USD 198.17 billion

- CAGR (2026–2034): 16.4%

- Asia Pacific: Largest market in 2025

The solar power sector has experienced tremendous growth, boosting polysilicon demand. The increasing demand for solar energy, a green energy source, has driven up solar cell production. Also, the development of the electronic and related industries, driven by the growing demand for 5G and the Internet of Things (IoT), has boosted polysilicon demand. Moreover, government policies and initiatives, such as subsidies and tax credits, are important for increasing demand for polysilicon in the solar industry.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

Low-carbon polysilicon is also emerging as a new market differentiator, as more customers become concerned about sustainability. Organizations increasingly use suppliers that opt for sustainable polysilicon across the solar, semiconductor, and other markets. This is further increasing the trend toward sustainable, green polysilicon manufacturing.

In April 2024, Highland Materials has plans for constructing a commercial polysilicon manufacturing unit in the USA, which is expected to have an annual production capacity of 16,000MT. It is proud of having reduced its carbon emissions during the manufacturing process by 90%.

Polysilicon, also known as polycrystalline silicon, is produced from metallurgical-grade silicon. It has high purity and consists of small silicon crystal lattices. It is applied in the production of solar cells and components. In the realm of electron materials, the purity obtained by polysilicon is very high. It only contains an impurity that is less than one in every billion. The quality of the solar field is lower, but it is very important for the formation of solar cells.

Creating a polysilicon factory requires a significant investment and advanced technology. Currently, China accounts for 80% of the world’s polysilicon supply. Following the COVID-19 outbreak, the disruption of the global supply chain has led to a severe shortage of silicon chips.

Powering Future: Polysilicon Production & Technology

The production of polysilicon requires that metallurgical-grade silicon undergo rigorous processes that consume considerable energy. Presently, the Siemens process is still used to manufacture highly purified polysilicon for solar cells and semiconductor materials. Although it is a proven process, it requires considerable amounts of energy.

This has made FBR polysilicon technology an emerging, more efficient trend. It boasts lower energy consumption, reduced carbon footprint, and cost benefits, especially for solar-grade polysilicon production. Polysilicon fluidized bed reactors are increasingly becoming an important complement to traditional methods, with demand on the rise.

Riding the Waves: Polysilicon Pricing & Supply–Demand Insights

The market demand and supply of polysilicon exhibit clear cycles. The boom in solar projects drives spiking demand for polysilicon, leading to a supply shortage and higher prices. The sudden increase in production capacity by many firms affects demand, leading to oversupply and lower prices.

Currently, polysilicon wafer prices fluctuate due to limited supply, rising energy costs, and delayed expansion start-ups. However, as more expansion facilities come into operation, this will help stabilize prices by increasing supply.

Market Trends

Government-Sponsored Digital Programs

The polysilicon industry is expected to grow in the coming years, driven by government policies and flagship programs. Digitalization would offer significant opportunities for emerging economies to enhance their economy. It helps connect people, optimize resource use, and fast-track development and economic growth. To unlock the potential benefits of digitalization, the government and other global organizations are taking serious steps to promote and invest in this field. In the same way, the Government of India started the “Digital India program.”

Digitalization enhances access to electronic services by improving online infrastructure, boosting internet connectivity, and empowering the country technologically. Furthermore, growing digitalization increased the demand for consumer electronics and raised electricity consumption. As a result, the ongoing digitalization would fuel growth in the polysilicon industry in the coming years by driving demand for electronics-grade products.

Increasing Adoption of Solar Energy

The growing use of solar energy is a key driver of the polysilicon market. Many countries are shifting toward renewable energy to reduce carbon emissions and achieve sustainability goals, fueling demand for solar PV systems. This change is greatly dependent on polysilicon, as it acts as a major feedstock for solar cells. In addition, governments worldwide are offering various incentives, subsidies, and support to enhance solar installations and thereby increase demand for solar-grade polysilicon. In April 2024, the Biden-Harris Administration committed USD 19 million to support the installation of solar panels atop canals. Alongside this, improvements in solar technologies and reductions in installation costs have made solar energy more feasible, further increasing polysilicon consumption. It is expected that surging demand from the solar sector will drive growth in the polysilicon industry.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Real-World Use Cases of Polysilicon

- Solar panels utilized in solar farms both residentially and commercially.

- Semiconductor chips incorporated in the manufacture of phones and computers.

- Electric cars running on semiconductor components produced by polysilicon.

- Data centers using silicon-made processors to facilitate cloud computing.

- Electronic products like laptops and smart devices.

Segment Insights

Market Breakdown – Application Insights

The global polysilicon industry, based on application, is segmented into solar PV and electronics. In 2025, the solar PV segment dominated the market due to extensive use in manufacturing solar photovoltaic panels and semiconductors, as well as the increasing global demand for solar PV system installations. Solar PV is one of the fastest-growing industries in the world. According to the International Energy Agency (IEA), it represents nearly two-thirds of net energy capacity worldwide.

The electronics segment is expected to grow robustly during the forecast period. Polysilicon plays a very important role as a material in the manufacturing of semiconductor devices. Polysilicon wafers serve as a basic material for producing semiconductor wafers used to build integrated circuits. The purity of polysilicon plays a very important role in the manufacturing of semiconductor devices, as high-quality electronic components depend on it.

The growing demand for electronic devices such as smartphones, tablets, computers, and IoT (Internet of Things) devices drives the need for semiconductors. This increased demand for semiconductors, in turn, increases the need for polysilicon, a fundamental material in semiconductor production.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominates the global polysilicon market in 2025. China has established dominance in the global market, driven by high manufacturing and export volumes, coupled with the availability of low-cost labor and coal. Most polycrystalline silicone manufacturers are based in China and are struggling to keep up with the growing demand from the photovoltaic industry. As a result, prices for polycrystalline silicon have surged by 40% due to supply shortages and are expected to stay elevated in the coming years. For instance, according to China’s National Energy Administration, the country's solar power generation capacity increased by 55.2% in 2023, with over 216 GW added throughout the year.

China polysilicon production remains a world leader, but rising geopolitical and supply risks are driving a shift. New investment in the US polysilicon manufacturing industry and the developing Indian polysilicon market aims to achieve diversification.

Other Asian nations started investing in domestic facilities to protect their growing photovoltaic and electronic sectors from potential shortages. For instance, Indian public companies NTPC & BHEL announced to foray into poly-crystalline silicon manufacturing with a capacity of ∼10 GW, aiming to reduce reliance on China.

The North America market will experience the sharpest CAGR from 2026 through 2034. The drivers of this market's growth include rising demand from the solar photovoltaic sector. In America, residential and commercial solar power capacity additions have surged, driven by cost reductions, tax incentives, and low carbon emissions. According to the Solar Energy Industries Association (SEIA), solar growth in the United States has increased at a compound annual rate of 24% over the last decade, driven by tax incentives, declining solar prices, and rising demand for low-carbon fuels. Today, the United States has a total solar installation capacity of 162 GW, sufficient to power 30 million homes.

Large-scale capacity expansion and localized polysilicon supply chains across Asia Pacific, North America, and Europe support strong polysilicon market growth. Continued investment in solar manufacturing has strengthened regional production ecosystems. As the most important upstream material, fluctuations in polysilicon supply and demand directly affect its price and market stability. This makes the market size cyclical and strategically important through the polysilicon market forecast 2034.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

The market for polysilicon is growing; polysilicon manufacturers from around the world are teaming up in joint ventures to expand their operations. The demand for powerful, energy-efficient electronic devices is currently a key driver of the growth of high-quality polysilicon manufacturers. Technological advancements in solar panel production have driven a strong demand for premium-grade polysilicon. With several technological advances, PV manufacturers are focusing on increasing efficiency. Government incentives and policies promoting the adoption of renewable energy resources drive market growth, thereby boosting the overall polysilicon market share.

Daqo New Energy Corp. (China); GCL Technology Holdings Co., Ltd. (China); Hemlock Semiconductor Corporation (US); Mitsubishi Materials Corporation (Japan); OCI Company Limited (South Korea); Qatar Solar Technologies (Qatar); REC Silicon ASA (Norway); Tokuyama Corporation (Japan); Wacker Chemie AG (Germany); and Xinte Energy Co., Ltd. (China) are among the major players in the market.

Mitsubishi Materials Corp (MMC) is a diversified materials manufacturer engaged in aluminum, metals, electronic materials and components, advanced materials and tools, energy, cement, and recycling. Mitsubishi Materials Corp. provides environmental, recycling, and energy-related services. Additionally, the company conducts R&D through its Naka Energy Research Laboratory and Central Research Institute in Japan. MMC’s operations span across Asia Pacific, Europe, and North America. The company is headquartered in Tokyo, Japan.

Wacker Chemie AG (Wacker) is a chemical company that markets a wide range of silicon and ethylene-based products. Its offerings include siloxanes, silicone fluids, silicone emulsions, pyrogenic silica, and silanes. Additionally, the company produces binders and polymeric additives, such as dispersible polymer powders and dispersions. Wacker is also a producer of hyper-pure polysilicon for the semiconductor and solar industries. They supply products to diverse industries, including consumer goods, food, textiles, base chemicals, technology, electronics, automotive, and construction. The organization has operations in Europe, the Americas, Asia, and other continents, with its headquarters in Munich, Germany.

List Of Key Companies

- Daqo New Energy Corp.

- GCL Technology Holdings Co., Ltd.

- Hemlock Semiconductor Corporation

- Mitsubishi Materials Corporation

- OCI Company Limited

- Qatar Solar Technologies

- REC Silicon ASA

- Tokuyama Corporation

- Wacker Chemie AG

- Xinte Energy Co., Ltd.

Polysilicon Industry Developments

- January 2026: United Solar announced securing over USD 900 million in funding to complete construction of its 100,000-ton polysilicon production plant in Oman's Sohar Free Zone. The company stated that production is expected to begin in 2026. (source: unitedsolarholding.com)

- July 2025: OCI Holdings and Japan’s Tokuyama Corp. have formed a joint venture, OTSM, which will be used to erect a semiconductor-grade polysilicon production facility in Sarawak, Malaysia, with an investment of USD 435 million. The facility broke ground on June 16th, with production expected to have an annual capacity of 8,000 MT by 2029, utilizing clean hydropower. (Source: renewablesnow.com)

- March 2025: 1KOMMA5°, based in Hamburg, has recently released the Full Black double-glass solar module, which uses German polysilicon to meet environmental and social criteria. The new version has enhanced parameters and guarantees, while continuing to prioritize transparency and sustainability. (Source: 1komma5.com)

- Feburary 2024: Oman-based United Solar Holding announced its plans to build a polysilicon project with a capacity of 100,000 tonnes per year at the Sohar Freezone. The project is estimated to cost USD 1.35 billion. (Source: www.saurenergy.com)

- January 2024: Hanwha Solutions' Qcells Division established an 8-year strategic partnership with Microsoft. Under this partnership, Hanwha Solutions' Qcells will supply 12 gigawatts of solar modules and EPC (Engineering, Procurement, and Construction) services. This capacity is sufficient to power over 1.8 million homes annually. (Source: www.hanwha.com)

Future of Polysilicon Market

Polysilicon demand is projected to grow significantly owing to increased use of solar power and rising demand for semiconductors. The trend towards green energy sources, combined with the set goals by the authorities for the production of electrical energy using renewable energy sources, will continue to drive the development of production capacity. New technological developments and cost reduction will make it easier to implement photovoltaic systems. Additionally, it is anticipated that demand will increase because of the developing electronics and automotive sectors.

Polysilicon Market Segmentation

By Application Outlook

- Solar PV

- Monocrystalline Solar Panel

- Multicrystalline Solar Panel

- Electronics (Semiconductor)

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Polysilicon Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 50.52 Billion |

| Market Size in 2026 | USD 58.62 Billion |

| Revenue Forecast by 2034 | USD 198.17 Billion |

| CAGR | 16.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

polysilicon market FAQ's

The global polysilicon industry is set to reach USD 198.17 billion by 2034 at an approximate CAGR of 16.4% from 2026 to 2034. This is primarily due to the increasing use of solar photovoltaic cells and semiconductors, as well as favorable government initiatives and policies promoting renewable energy.

Asia Pacific dominates the global polysilicon market, led by China’s strong manufacturing capacity, low costs, and high solar photovoltaic demand.

North America is expected to register the highest CAGR from 2026 to 2034, driven mainly by growing demand from the solar photovoltaic sector.

The increased use of renewable energy sources, governments' targets for zero emissions, the rising number of semiconductors, and the digitization of developing nations are contributing to the increased demand for polysilicon.

A low-carbon and sustainable polysilicon solution is fast becoming a key strength for firms. Top producers are investing in green polysilicon to address E, S, and C elements. Prices are driven by tight supply, rising energy costs, and delayed plant commissioning. Emerging technologies, including polysilicon produced in a fluidized-bed reactor, are also attracting increasing attention to enable low-cost, efficient processing.

China polysilicon production remains dominant, but geopolitical and supply chain risks are driving investment in US polysilicon manufacturing and the Indian polysilicon market. Other Asian countries are also developing domestic facilities to secure their solar and electronics industries.

Polysilicon is an essential material for solar PV and semiconductor production. Solar-grade polysilicon still accounts for most global consumption, while electronics-grade polysilicon is growing faster due to rising semiconductor demand.

Download Sample Report of polysilicon market

Please fill out the form to request a customized copy of the research report.