Power Transformer Market Size, Industry Demand, Global Analysis, 2025-2034

REPORT DETAILS

Market Statistics

Market Overview

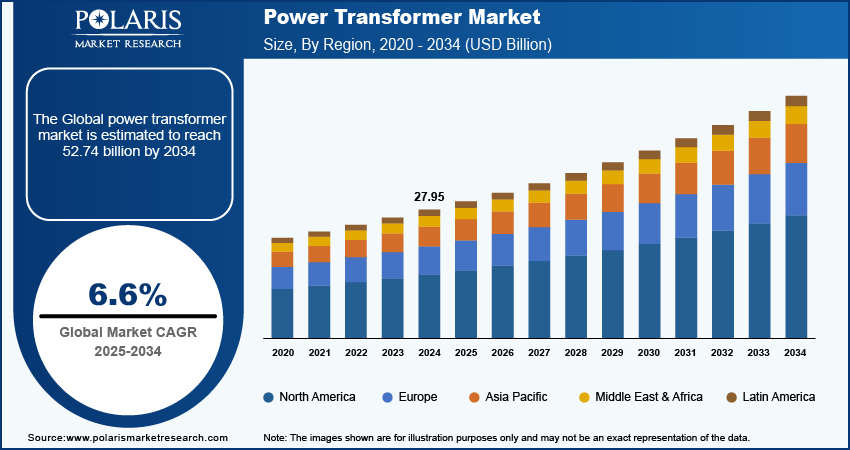

The power transformer market size was valued at USD 27.95 billion in 2024 and is expected to register a CAGR of 6.6% from 2025 to 2034. Increasing investments in transmission and distribution infrastructure, expanding power grid networks, and supportive government regulations drive the industry growth. Additionally, increasing private sector investments in power equipment to match supply with the rising demand boost the requirement for power transformers.

Key Insights

- The small power transformer (up to 60MVA) segment dominated the power transformer industry share in 2024. This is due to the expansion of distributed generation system and growing demand for un-interrupted electricity supply.

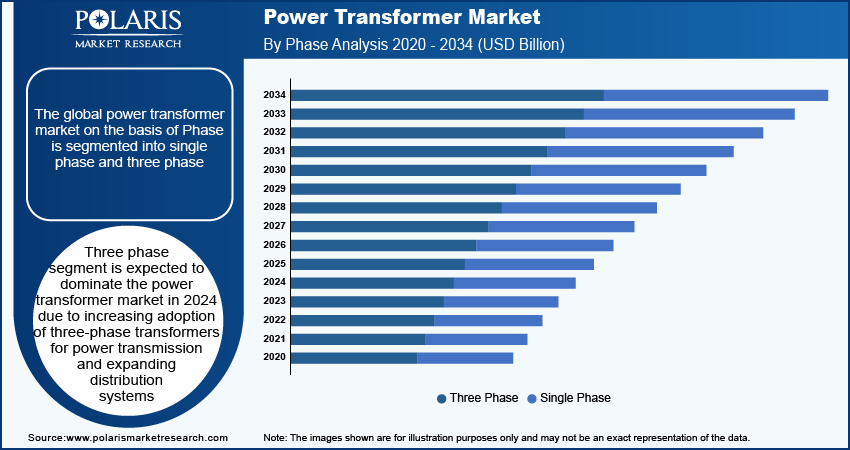

- The three phase segment accounted for the largest revenue share in 2024. The adoption of three-phase transformers is rising for power transmission and expanding distribution systems.

- In 2024, the utilities segment held the largest revenue share. Expanding industrial activities and the need for efficient power supplies in rural areas have created significant demand for power transformers.

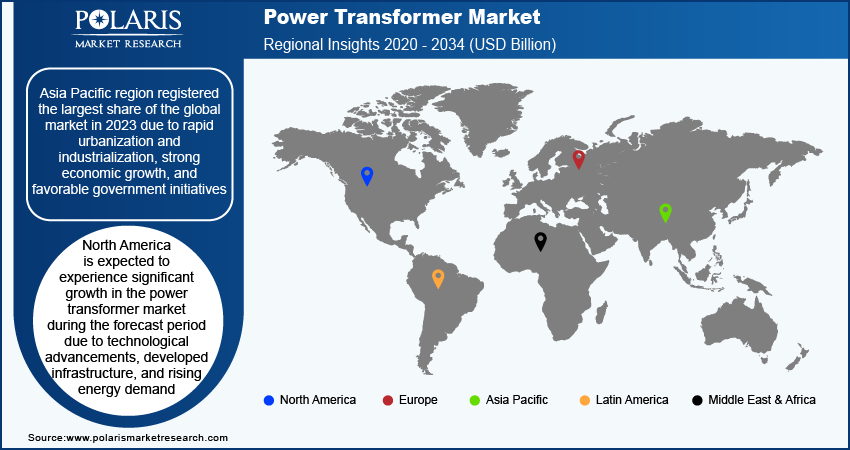

- Asia Pacific held the largest share of the power transformer industry in 2024. The dominant position is fueled by rapid urbanization, industrialization, and strong economic growth.

- The industry in North America is expected to experience significant growth during the forecast period. Technological advancements, developed infrastructure, and rising energy demand propel the growth.

Industry Dynamics

- Rising population, urbanization, and industrialization in developing economies are significantly increasing the demand for electricity. This factor is leading to the growth of the market.

- Governments worldwide invest in modernizing aging power grids into advanced, smart grids. It is propelling the demand for power transformers.

- High initial costs, especially for high-capacity transformers, restrain the adoption of power transformers.

- The rising global shift toward renewable energy sources, including wind and solar, necessitates advanced power transformers to manage and integrate these resources effectively. This is expected to offer opportunities in the coming years.

Market Statistics

2024 Market Size: USD 27.95 billion

Source: Polaris Market Research Analysis

2034 Projected Market Size: USD 52.74 billionSource: Polaris Market Research Analysis

CAGR (2025–2034): 6.6%Source: Polaris Market Research Analysis

Asia Pacific: Largest market in 2024AI Impact on Power Transformer Market

- Artificial intelligence (AI)-enabled sensors and analytics monitor transformer health in real time. It tracks gas buildup and vibration levels. This facilitates the early detection of faults, which reduces unplanned downtime and extends transformer lifespan.

- The technology enables smart transformers that detect overloads and optimize energy flow by analyzing demand patterns.

- AI models forecast energy demand and adjust transformer loads in real time. This minimizes thermal stress and insulation breakdown.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Rapid urbanization and industrialization in developing economies are significantly fueling the growth of the power transformer market during the forecast period. Increased energy demands have resulted in the expansion of infrastructure projects, leading to increased demand for the installation of new power transformers. Additionally, the global shift towards renewable energy sources, such as wind and solar, necessitates advanced power transformers to manage and integrate these resources effectively. Government initiatives promoting energy efficiency and extending reliable power supply to remote areas also contribute to rising demand. Together, these factors are accelerating power transformer market expansion during the forecast period.

Growth Drivers

Growing Demand for Electricity

Rising population, urbanization, and industrialization in developing economies are significantly increasing the demand for electricity, leading to the growth of the power transformer market during the forecast period. The need for efficient and reliable power transmission systems, including advanced power transformers, is growing. For example, according to the U.S. Energy Information Administration, total U.S. electricity consumption reached approximately 4.07 trillion kWh in 2022—14 times higher than in the 1950s. This surprising increase highlights the urgent need for enhanced power infrastructure to meet escalating energy demands. Thus, increase in demand for electricity is driving the power transformer market

Increase in Investment for Advance Power Grids

To enhance grid reliability, reduce transmission losses, and support the integration of renewable energy sources, governments worldwide are investing in modernizing aging power grids into advanced, smart grids. This technological shift is expected to drive significant growth in the power transformer market. For example, in October 2023, the U.S. Department of Energy announced a substantial investment of USD 3.46 billion to upgrade the country’s aging electric grid. Such investments in grid modernization are likely to accelerate the demand for advanced power transformers, which are crucial for improving grid performance and accommodating new energy technologies.

Restraining Factors

High Initial Investment

High initial costs, especially for high-capacity transformers, pose substantial financial barriers and create obstacles for countries with limited budgets, restraining power transformer market growth during the forecast period. These cost constraints can hinder the widespread adoption and deployment of advanced power transformers, impacting market growth in regions where budget limitations are a critical concern.

Source: Polaris Market Research Analysis![]()

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Report Segmentation

The market is primarily segmented based on power rating, phase, cooling type, end user and region.

By Power Rating Analysis

Small Power Transformer (up to 60MVA) dominated power transformer market in 2024

Small Power Transformer (up to 60MVA) segment dominated the power transformer market in 2024. This is primarily due to the expansion of distributed generation system, growing renewable energy sources, with increasing demand for un-interrupted electricity supply are bolstering the segment growth. Low cost and ease of installation are creating new growth avenues for small power transformers in the utility sector.

By Phase Analysis

Three Phase segment garnered with the fastest revenue share in 2024

Three phase segment accounted for the fastest revenue share in the power transformer market, due to increasing adoption of three-phase transformers for power transmission and expanding distribution systems. Their superior reliability in managing large power loads and efficient performance make them a preferred choice, further propelling the segment's growth.

By End Use Analysis

Utilities segment witnessed the significant revenue share in 2024

Utilities segment accounted for the largest revenue share in the power transformer market, owing to its crucial role in the generation, transmission, and distribution of power. Expanding industrial activities and the need for efficient power supplies in rural areas have created significant demand for the power transformers. This segment is particularly involved in the modernization of aging power grids for a reliable supply of electricity, which companies are participating in acquisition initiatives to fulfill this demand.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

Asia Pacific region registered the largest share of the global market in 2024

The Asia-Pacific region holds the largest share of the power transformer market, due to rapid urbanization and industrialization, strong economic growth, and favorable government initiatives. The region’s significant investments in infrastructure development and expansion of renewable energy sources further propel the power transformer market growth. These factors combine to enhance energy capacity and modernize power grids, placing Asia-Pacific as a leading player in the global power transformer market. The increasing demand for reliable and efficient power transmission solutions boosts the power transformer market growth in the forecast years.

North America is expected to experience significant growth in the power transformer market during the forecast period due to technological advancements, developed infrastructure, and rising energy demand. For example, according to the U.S. Energy Information Administration, U.S. energy production exceeded consumption in 2022, with production reaching 102.92 quads and consumption at 100.41 quads. This rising energy demand underscores the region’s commitment to enhancing its energy infrastructure and meeting growing demands, further supporting the expansion of the power transformer market in the region.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Competitive Analysis

The market is highly competitive, with major players like Siemens, General Electric, and Schneider Electric leading innovation and offering advanced products. These companies focus on improving transformer efficiency, durability, and capacity to meet evolving energy demands. The market also sees a rise in smart transformers and environmentally friendly solutions, such as oil-free and recyclable transformers, driven by sustainability goals. Competition is intense, with companies striving for technological advancements, geographic expansion, and strategic mergers and acquisitions to maintain market leadership and meet diverse customer needs.

List Of Key Companies

- Hitachi Energy

- General Electric

- Siemens

- Schneider Electric

- Mitsubishi Electric

- Eaton Corporation

- Hyundai Electric

- Fuji Electric

- Toshiba corporation

- MGM Transformer Company

- CG Power and Industrial Solutions

- Ningbo Ironcube Works International Co., Ltd.

- Chint Group

Recent Developments in the Industry

- February 2025: Schneider Electric Infrastructure Ltd., a unit of Schneider Electric, announced an expansion of its Vadodara, Gujarat transformer plant. With an investment of ₹13.6 crore (~USD 1.5 million), the project will raise medium power transformer capacity by 1,500 MVA annually, increasing total output from 5,500 MVA to 7,000 MVA.

- July 2024: Siemens Energy announced a major investment to expand its grid division, supporting global energy infrastructure and the clean energy transition. The plan includes new facilities, highlighted by a large power transformer plant in Charlotte, North Carolina, to address the US transformer shortage and upgrade aging grid systems.

- May 2024: Hitachi Energy has announced a USD100 Billion investment to upgrade and modernize its power transformer factory in Varennes and other Montreal facilities, funded by the Government of Quebec. This investment aims to meet increasing North American demand for sustainable energy and supports global plans for electrification. The expansion includes a new 130,000 sq ft transformer testing facility, set to be completed by 2027, creating around 70 jobs. The initiative aligns with Quebec’s strategy to achieve carbon neutrality by 2050.

- August 2023: CES Transformers' USD 4 million investment in expanding its Markham facility, supported by USD 610,000 from AMIC, and created 80 jobs and strengthen Ontario's manufacturing sector, reaching its highest employment since 2008.

Power Transformer Market Segmentation

By Power Rating Outlook (USD Billion, 2020 - 2034)

- Small Power Transformer (up to 60MVA)

- Medium Power Transformer (61-600MVA)

- Large Power Transformer (Above 600MVA)

By Phase Outlook (USD Billion, 2020 - 2034)

- Single

- Three

By Cooling Type Outlook (USD Billion, 2020 - 2034)

- Oil-cooled

- Air-Cooled

By End User Outlook (USD Billion, 2020 - 2034)

- Utilities

- Residential & Commercial

- Industrial

By Regional Outlook (USD Billion, 2019 – 2032)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Coverage

The power transformer market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, power rating, phase, cooling type, end user and their futuristic growth opportunities.

Power Transformer Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 27.95 billion |

| Revenue forecast in 2034 | USD 52.74 billion |

| CAGR | 6.6% from 2025 – 2034 |

| Base year | 2024 |

| Historical data | 2020 – 2023 |

| Forecast period | 2025 – 2034 |

| Quantitative units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Segments covered |

|

| Regional scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, region, and segmentation. |

Source: Polaris Market Research Analysis

Power Transformer Market FAQ's

The Power Transformer Market size was valued at USD 27.95 billion in 2024 and is projected to grow to USD 52.74 billion by 2034.

The global market is projected to grow at a CAGR of 6.6% during the forecast period, 2024-2032.

Asia Pacific had the largest share in the global market

The key players in the market are Hitachi Energy; General Electric; Siemens; Schneider Electric; Mitsubishi Electric; Eaton Corporation; Hyundai Electric; Fuji Electric; Toshiba Corporation; MGM Transformer Company; CG Power and Industrial Solutions; Ningbo Ironcube Works International Co., Ltd.; Chint Group.

The three-phase segment is anticipated to experience substantial growth with a significant CAGR in the global market. This growth is due to increasing adoption of three-phase transformers.

The Utilities segment accounted for the largest revenue share of the market in 2024 due to its major role in power transmission.

Download Sample Report of Power Transformer Market

Please fill out the form to request a customized copy of the research report.