Market Overview

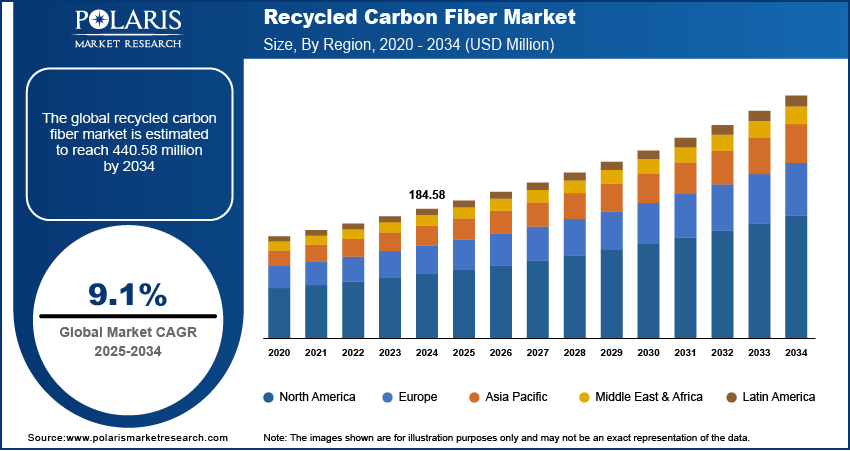

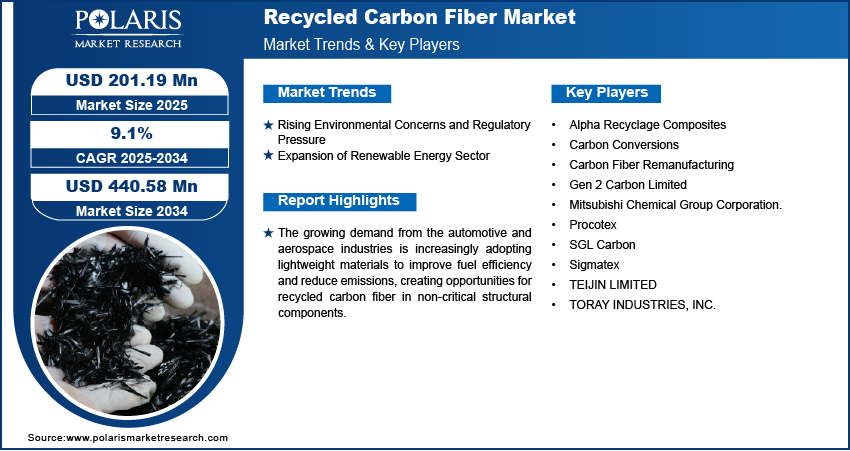

The global recycled carbon fiber market size was valued at USD 201.19 million in 2025 and is projected to register a CAGR of 9.1% from 2026 to 2034. The growing automotive and aerospace industries are increasingly adopting lightweight materials to improve fuel efficiency and reduce emissions. This factor is expected to create opportunities for recycled carbon fiber in noncritical structural components. Additionally, companies across industries are integrating sustainable materials into their supply chains to meet environmental, social, and governance (ESG) targets. It is boosting the carbon fiber recycling market growth.

Key Insights

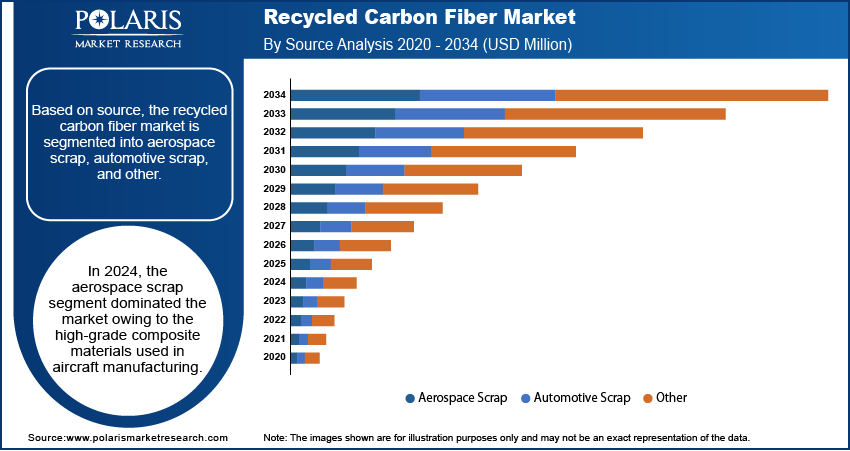

- In 2025, the aerospace scrap segment led the revenue share. The high-grade composite materials used in aircraft manufacturing contributed to the dominance.

- The chopped fiber segment held a larger share in 2025. The leading position is driven by its wide applicability in thermoplastic compounding and compression molding processes.

- In 2025, the automotive & transportation segment emerged as the largest end-use category. The largest share is attributed to escalating demand for lightweight, high-performance materials in electric vehicles and structural components.

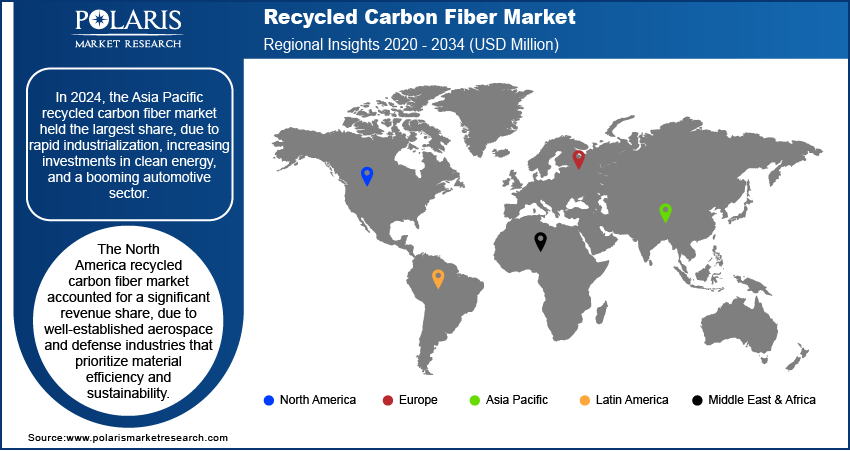

- In 2025, Asia Pacific held the largest share. Rapid industrialization, increasing investments in clean energy, and a booming automotive sector boost the Asia Pacific recycled carbon fiber market share.

- The Europe recycled carbon fiber industry is expected to grow significantly during the forecast period. Regional market growth is driven by stringent EU directives on waste reduction and lifecycle sustainability of products.

Industry Dynamics

- Increasing environmental concerns and regulatory pressure boost the preference for recycled carbon fiber.

- Growth of the renewable energy sector boosts the expansion of the market.

- Rising emphasis on innovative recycling techniques would create lucrative opportunities in the coming year.

- Concerns related to performance & quality hinder the recycled carbon fiber market growth.

Market Statistics

- 2025 Market Size: USD 201.19 million

- 2034 Projected Market Size: USD 440.58 million

- CAGR (2026-2034): 9.1%

- Asia Pacific: Largest Market in 2025

AI Impact on Recycled Carbon Fiber Market

- AI-driven material sorting systems will use computer vision and spectroscopy. It accurately identifies, separates, and grades carbon fiber waste from mixed industrial scrap and end-of-life composites.

- Machine learning algorithms are used to optimize recycling process parameters, including temperature, pressure, and chemical exposure. Technology adoption improves fiber recovery rates and mechanical performance.

- AI-enabled predictive maintenance systems are used to detect early signs of reactor, shredder, and filtration system failures. These tools help recycling plants reduce equipment downtime.

- Digital twins powered by AI simulate recycling workflows. It reduces energy consumption, minimize processing time, and improve throughput.

- AI tools help predict scrap availability from aerospace, automotive, and wind energy sectors. It enhances supply chain forecasting.

- Automated quality control systems using AI will ensure consistent fiber length, tensile strength, and surface integrity. It increases adoption across high-performance applications.

What is Recycled Carbon Fiber?

Recycled carbon fiber is a budget-friendly and environmentally friendly choice compared to new carbon fiber. The recycled carbon fiber market includes collecting, processing, and reusing carbon fiber waste from manufacturing or discarded products. Carbon fiber is a tough and lightweight material. It is widely used in industries like aerospace, automotive, wind energy, and sporting goods. Its production requires high energy consumption and can be expensive. As a result, there is a rising focus on the recycling of carbon fiber to reduce environmental impact and cut material costs.

Recycling carbon fiber involves recovering fibers from pre-consumer scrap (production waste) or post-consumer waste (discarded products). Methods like pyrolysis, solvolysis, and mechanical recycling are used in the process. Most of the original strength is retained in the recycled product. It is used in various applications, especially where cost efficiency and sustainability are important.

The high costs and energy demands of producing virgin carbon fiber prompt manufacturers to switch to recycled options. These alternatives provide similar performance at a lower cost. New recycling techniques, including microwave-assisted pyrolysis and chemical solvolysis, have enhanced fiber quality and recovery rates. These aspects make recycling more economically practical.

Recycled carbon fiber is majorly used in applications where ultra-high structural performance is not mandatory. In addition to weight-reduction benefits, manufacturers are increasingly evaluating recycled carbon fiber as part of long-term material-cost optimization and ESG-compliance strategies. Thus, recycled carbon fiber is used widely in automotive, industrial, and consumer composite applications. From the perspective of the recycled carbon fiber value chain, the market includes pre-consumer carbon fiber scrap and post-consumer scrap. Pre-consumer carbon fiber scrap comes from aerospace and automotive manufacturing. Post-consumer scrap is made from aircraft, vehicles, wind turbine blades, and industrial equipment. These scrap types are processed using advanced carbon fiber recycling methods to recover usable fibers.

According to our recycled carbon fiber market analysis, pyrolysis and chemical solvolysis are becoming more popular. They achieve higher fiber recovery rates and retain mechanical properties better. This is improving the commercial viability of recycled carbon fiber in semi-structural applications.

Market Dynamics

Recycled Carbon Fiber Market Drivers

Rising Environmental Concerns and Regulatory Pressure

Governments set strict rules on industrial waste and carbon emissions amid rising environmental concerns. In March 2024, the EPA finalized the Multi-Pollutant Emissions Standards for light-duty and medium-duty vehicles. This rule will begin in the 2027 model year and later. It establishes tougher emissions limits to reduce harmful air pollutants and improve air quality. Many countries focus on circular economy models that prioritize recycling and reuse. These policies make it more expensive and difficult for industries to throw away carbon fiber waste in landfills. As a result, companies are choosing recycled carbon fiber as a more sustainable option. Regulatory support, including subsidies, tax incentives, and green certifications, encourages this shift. This shift helps businesses comply with environmental laws and also enhances their sustainability image. It assists them in aligning with global climate goals and consumer expectations. For manufacturers, carbon fiber recycling regulations are increasing landfill disposal costs and compliance risks. It enables a strategic shift toward circular economy composites such as recycled carbon fiber. Recycled carbon fiber improves material traceability and lifecycle performance. Thus, regulatory compliance, sustainability certifications, and pressure from downstream OEMs boost the adoption of recycled carbon fiber.

Expansion of Renewable Energy Sector

The renewable energy sector witnesses rapid expansion, particularly the wind power segment. The sector grows due to the rising focus of countries on achieving clean energy goals. The Biden-Harris administration has approved the Maryland Offshore Wind Project. This approval raises the total authorized offshore wind capacity to over 15 gigawatts, nearing the administration's target of 30 gigawatts by 2030. Wind turbine blades are often made from composite materials containing carbon fiber. These blades last a long time, but they will eventually need to be disposed. Their disposal creates major environmental concerns. As a result, recycling efforts are gaining traction to recover valuable carbon fiber. The rising number of decommissioned blades creates a significant opportunity for the recycled carbon fiber industry. Companies invest a significant amount in technologies that extract and reuse fibers. It helps improve resource use and sustainability in the energy transition.

Segment Insights

By Source

Based on source, the segmentation includes aerospace scrap, automotive scrap, and others. In 2025, the aerospace scrap segment led the market because of the high-quality composite materials used in aircraft manufacturing. Retired aircraft and leftover production materials generate significant amounts of carbon fiber scrap. This scrap consists of excellent mechanical properties even after being recovered. The strength and consistency of aerospace-grade carbon fiber are driving its demand for reuse in tough structural applications. These advantages appeal to recyclers and manufacturers looking for strong, cost-effective options compared to new carbon fiber. The market stays strong due to the high-quality carbon fiber composites produced during aircraft manufacturing and retirement programs. These materials ensure reliable fiber quality, which makes aerospace carbon fiber scrap particularly attractive for recycling into high-performance applications.

The automotive scrap segment will report the highest growth rate from 2026 to 2034. This increase is driven by the automotive industry's focus on improving sustainability and cutting production costs. The growing use of carbon fiber-reinforced composites in EVs and lightweight vehicle platforms boosts scrap generation. Recovering and reusing this material helps manufacturers reach their emissions and recycling goals. This creates a strong incentive to integrate recycled carbon fiber into new automotive parts. The increasing use of carbon fiber in electric vehicles, body panels, and lightweight structural parts is driving growth in this segment. Original equipment manufacturers (OEMs) are looking for affordable ways to reduce weight to meet emissions standards. As a result, automotive carbon fiber recycling is becoming more popular.

By Type

Based on type, the recycled carbon fiber industry segmentation includes chopped fiber and milled fiber. In 2025, the chopped fiber segment held a larger share. Its wide applicability in thermoplastic compounding and compression molding processes drives the dominance. Its compatibility with automated manufacturing systems and superior reinforcement capabilities make it the preferred format in high-volume industries such as automotive and electronics. Chopped recycled carbon fiber offers a strong balance of mechanical performance and processing efficiency. It is especially ideal for parts that require strength, stiffness, and dimensional stability.

The milled fiber segment is expected to grow faster during the forecast period. Its increasing use in coatings, adhesives, and 3D printing filaments is driving this growth. Milled recycled carbon fiber has a large surface area and good dispersibility. It boosts electrical conductivity, wear resistance, and thermal stability in products. It enhances functional properties without significantly altering viscosity or density. This makes it ideal for new applications in smart materials and conductive polymers. Milled recycled carbon fiber is becoming more popular in coatings, adhesives, conductive polymers, and additive manufacturing because of its fine particle size, better dispersibility, and ability to reinforce function.

By End Use

Based on end use, the segmentation includes automotive & transportation, consumer goods, sporting goods, industrial, aerospace & defense, marine, and others. In 2025, the automotive and transportation segment became the largest end-use category because of growing demand for lightweight, high-performance materials in electric vehicles and structural components. Recycled carbon fiber provides the industry with cost-effective, sustainable options compared to virgin composites. Major OEMs use recycled carbon fiber in under-the-hood applications, interior parts, and body panels. This supports circular economy goals and reduces vehicle weight, which helps improve efficiency.

The marine segment is expected to grow at highest rate in the next few years. This growth comes from the rising use of recycled carbon fiber in hulls, decks, and interiors of leisure boats, yachts, and unmanned vessels. The material's natural resistance to corrosion, high strength-to-weight ratio, and durability are crucial in harsh saltwater conditions. Thus, its demand is rising in marine applications. Manufacturers in the marine industry are seeking sustainable alternatives to traditional composites. Recycled carbon fiber offers a cost-effective option that maintains structural integrity. Its flexible design and better fuel efficiency from weight reduction also promote its use in today's marine applications, particularly in custom and performance-focused boats.

Regional Analysis

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, Asia Pacific held the largest share. It is driven by rapid industrialization, rising investments in clean energy, and a growing automotive production base. According to Zero Carbon Analytics, since 2020, ASEAN has seen a strong annual growth rate of about 15% in international investment projects focused on renewable energy, which is higher than the global average of 11%. By 2022, total investments in this sector within the region surged to USD 43 billion. It reflects a significant trend toward sustainable energy development. China, Japan, South Korea, and India played a key role in the Asia Pacific recycled carbon fiber market. These countries adopt advanced recycling technologies and encourage circular economy practices. The region's growing aerospace manufacturing base also increased demand. Additionally, rising awareness about sustainable materials among manufacturers resulted in higher use of recycled carbon fiber in various applications, including electronics and infrastructure.

The China recycled carbon fiber market held the dominant share in the region in 2025. Strong government support for green manufacturing and electric vehicle adoption drives this dominance. According to the International Energy Agency (IEA), China led the electric vehicle (EV) market in 2025. In China, electric cars accounted for nearly 50% of total automotive sales. The country sold over 11 million units. This marked a significant increase in EV adoption and market presence compared to previous years. Policies that require waste reduction and resource reuse encouraged investments in recycling infrastructure. Chinese automakers increasingly used lightweight composites to reach fuel efficiency goals, which increased local demand. Companies improved their processing of carbon fiber waste from wind turbines and aircraft parts. China’s strong push for renewable energy also resulted in many decommissioned turbine blades. This situation raises the demand for effective recycling solutions. In January 2025, the China Passenger Car Association (CPCA) reported that China produced about 2.11 million passenger vehicles, a 3.6% increase from the previous year. Exports reached 380,000 units, marking a 3% increase from the prior year. Thus, increasing automotive production propels the market growth in China.

The North America recycled carbon fiber market held a significant revenue share in 2025. Market growth is fueled by the presence of well-established aerospace and defense industries that prioritize material efficiency and sustainability. The U.S. Department of Energy and other agencies funded research into recycling composites, which supported new recovery methods. Automotive manufacturers used recycled carbon fiber to reduce weight in high-performance and electric vehicles. A strong set of regulations on waste management and emissions encouraged companies to use recycled materials. Additionally, partnerships between material suppliers and industries that use these materials helped expand commercial applications in various sectors. The North America recycled carbon fiber industry also gains from the early commercialization of recycled carbon fiber solutions in automotive and defense applications.

The U.S. recycled carbon fiber market held the dominant share in North America in 2025. The U.S. market growth is driven by its mature composites industry and early adoption of recycling technologies. Major players in the aerospace and automotive sectors actively integrated recycled carbon fiber into production lines. The adoption helps them cut costs and meet environmental goals. Federal incentives for green manufacturing and landfill diversion pushed companies toward sustainable alternatives. Research institutions and private firms collaborated on improving fiber recovery techniques. Also, the country generated high volumes of carbon fiber waste from military equipment, aircraft, and wind farms. It creates a consistent feedstock supply for recyclers.

The Europe recycled carbon fiber market is expected to grow significantly during the forecast period. Strict EU directives on waste reduction and product lifecycle sustainability boost the growth. Germany, France, and the UK led efforts to boost the use of recycled materials in the automotive, aviation, and construction sectors. European automakers use lightweight composites to comply with CO₂ emission standards. The rise of wind energy propelled need to recycle old turbine parts. Government-funded research and development programs support the creation of chemical and thermal recycling methods. Consumer demand for eco-friendly products also pushed brand owners to source recycled carbon fiber. This factor is boosting market growth across the region. The European market growth is driven by strong research programs that support composite recycling in the automotive and wind energy sectors.

Key Players and Competitive Analysis

The recycled carbon fiber industry has a dynamic competitive landscape.It is driven by ongoing technology improvements, changing market plans, and a growing focus on sustainable materials. Recycled carbon fiber manufacturers emphasize partnerships, joint ventures, and mergers and acquisitions. These strategies help them strengthen their presence and improve recycling capabilities. Many carbon fiber recycling companies launch products to showcase better fiber recovery rates and higher material performance. This helps them stand out in a crowded market. Post-merger integration is essential for combining skills and improving production capacities in critical areas. Companies collaborate with end-use industries like automotive, aerospace, and renewable energy to customize recycled fiber applications.

There is an increasing trend toward vertical integration, where manufacturers team up with waste suppliers to secure a consistent supply of raw materials. As environmental regulations become stricter, companies gain a competitive edge through innovation in pyrolysis, solvolysis, and mechanical recycling methods. The market keeps evolving through collaborative efforts aimed at achieving circularity and cost efficiency. Players in the recycled carbon fiber market are focusing more on vertical integration, securing long-term scrap supply agreements, and developing their own recycling technologies. It helps them improve fiber quality, scalability, and cost efficiency. Competitive differentiation is increasingly based on recycling process efficiency, fiber consistency, and application-specific customization.

List of Key Companies

- Alpha Recyclage Composites

- Carbon Conversions

- Carbon Fiber Remanufacturing

- Gen 2 Carbon Limited

- Mitsubishi Chemical Group Corporation.

- Procotex

- SGL Carbon

- Sigmatex

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

Recycled Carbon Fiber Industry Developments

In June 2025, Vartega Inc. announced a partnership with Syensqo. The partnership aims to accelerate the production of sustainable, high-performance plastics by using a new method to recycle carbon fiber. This collaboration enables large-scale recycling in a closed loop and at a reduced cost.

In March 2025, Syensqo and Vartega partnered to repurpose industrial carbon fiber waste into high-performance materials. Under the collaboration, Vartega used its own technology to turn Syensqo’s dry carbon fiber and prepreg waste into EasyFeed Bundles. These recycled fibers were then added to Syensqo’s ECHO line of carbon fiber-reinforced polymers. These materials are often used in automotive applications.

In August 2024, Hera SpA teamed up with the Visa Cash App RB Formula One Team to use recycled carbon fiber in the production of the VCARB Formula One car. This partnership supports the team's effort to reduce carbon emissions and its larger aims to improve circular economy practices in motorsports.

In December 2023, Toray Industries, Inc. created recycled carbon fiber from waste produced during Boeing 787 component manufacturing. They used their TORAYCA carbon fiber for this process. This initiative offered a high-quality source of recycled material.

Recycled Carbon Fiber Market Segmentation

By Source Outlook (Volume, Kilotons; Revenue, USD Million; 2021–2034)

- Aerospace Scrap

- Automotive Scrap

- Other

By Type Outlook (Volume, Kilotons; Revenue, USD Million; 2021–2034)

- Chopped Fiber

- Milled Fiber

By End Use Outlook (Volume, Kilotons; Revenue, USD Million; 2021–2034)

- Automotive & Transportation

- Consumer Goods

- Sporting Goods

- Industrial

- Aerospace & Defense

- Marine

- Others

By Regional Outlook (Volume, Kilotons; Revenue, USD Million; 2021–2034)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Recycled Carbon Fiber Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 201.19 million |

|

Market Size in 2026 |

USD 219.34 million |

|

Revenue Forecast in 2034 |

USD 440.58 million |

|

CAGR |

9.1% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2022–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market is expected to grow from USD 201.19 million in 2025 to USD 440.58 million by 2034. It is expected to register a CAGR of 9.1% during 2026-2034.

Automotive and transportation dominate market share. Aerospace, wind energy, sporting goods, consumer electronics, and marine industries use the recycled fiber for lightweight material solutions.

Pyrolysis leads with 35.4% market share, followed by mechanical recycling, solvolysis, and chemical recycling methods. Pyrolysis preserves fiber strength while efficiently removing resins.

The Asia Pacific market witnesses fastest growth. The expansion is driven by China's circular economy initiatives and expanding EV production. Also, increasing composite waste from wind turbines and electronics manufacturing boosts the regional market growth.

Automotive lightweighting for EVs and circular economy regulations are helping the market grow. Cost benefits compared to virgin fiber and the need for sustainability are also driving this expansion.

Page last updated on:

Jun-2025

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements