Overview

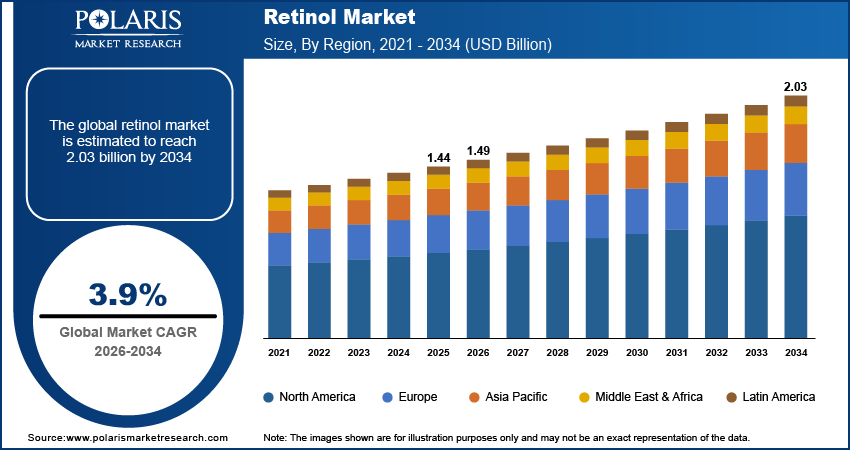

The global retinol market is estimated around USD 1.44 billion in 2025, with consistent growth anticipated during 2026–2034. Growth is supported by rising demand for anti-aging skincare, increasing acne and hyperpigmentation treatment adoption, and expanding dermatology-backed cosmetic formulations. The market is projected to grow at a CAGR of 3.9% during the forecast period.

Key Takeaways:

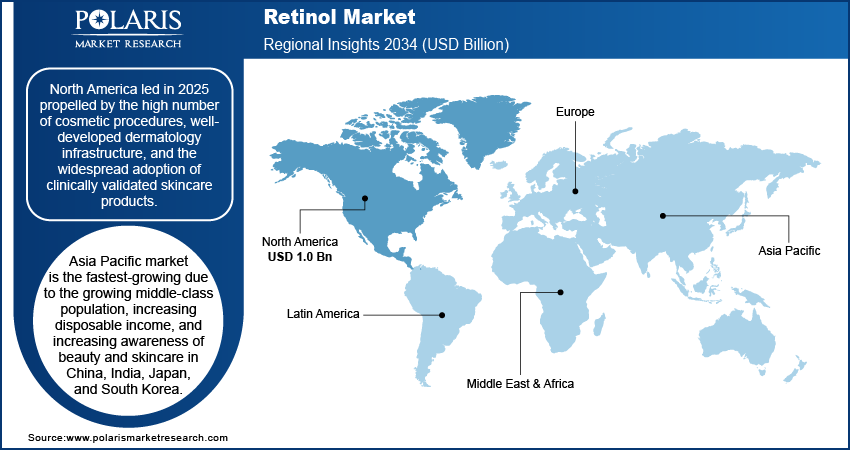

- North America accounted for the largest regional share of around 35.8% in 2025, driven by strong consumer awareness of dermatological skincare, rising aesthetic procedures, and presence of established cosmetic brands.

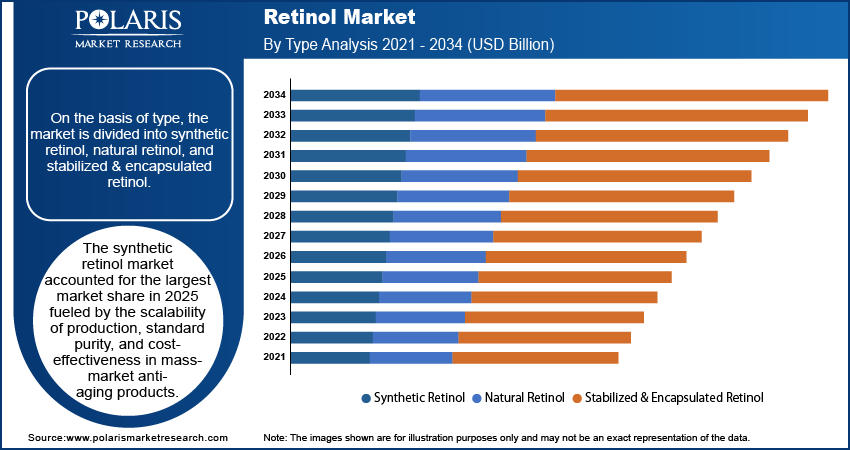

- By Type, Synthetic Retinol segment accounted for the largest share of approximately 68.4% in 2025, supported by high purity, consistent concentration, and cost-effective production for commercial cosmetic and pharmaceutical formulations.

- By Formulation, Cream segment accounted for the largest share of around 52.7% in 2025, driven by gentle absorption profile, lower irritation risk, and strong consumer preference in anti-aging skincare products.

- By Application, Cosmetics & Personal Care segment accounted for the largest share of nearly 61.9% in 2025, supported by widespread use of retinol in anti-aging formulations for wrinkle reduction and skin texture improvement.

Market Statistics

- 2025 Market Size: USD 1.44 billion

- 2034 Projected Market Size: USD 2.03 billion

- CAGR (2026-2034): 3.9%

- North America: Largest market in 2025

Industry Dynamics

- Rising consumer focus on wrinkle reduction, collagen stimulation, and pigmentation correction is strengthening demand for retinol-based skincare products.

- Increasing acne prevalence across adolescent and adult populations is expanding inclusion of retinol in therapeutic and maintenance regimens.

- Regulatory concentration limits and vitamin A safety concerns are creating formulation and compliance complexity.

- Advancements in microencapsulation and stabilized retinol technologies are unlocking long-term high-performance product development opportunities.

What Are Retinol?

The retinol Market refers to the structured production, formulation, and commercial distribution of retinol and related vitamin A derivatives used across dermatology devices, pharmaceuticals, and regulated cosmetic applications. Within the broader vitamin A derivatives market, retinol represents a distinct category differentiated from prescription retinoids, which alters scope in any retinoids market comparison. The market comprises synthetic retinol market supply chains made by controlled chemical synthesis, in addition to natural retinol market trends associated with bio-based materials and stability enhancement technologies.

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Increasing demand for anti-aging skincare products: Growing interest of consumers in the reduction of wrinkles, elasticity enhancement, and pigmentation is driving the demand for retinol skincare products. The property of retinol in stimulating collagen synthesis and improving cell turnover makes it an attractive ingredient in premium anti-aging skincare products. In July 2025, Kao Corporation launched a new anti-aging skincare product in the market under its Kanebo brand, which targets firmness and aging skin, showing continuous commercial interest in retinol-based products. This, in turn, is fueling the demand for OEM retinol-stabilized and encapsulated solutions, thus driving the retinol market.

Rising incidence of acne and hyperpigmentation: Rising prevalence of acne and post-inflammatory hyperpigmentation are fueling the demand for therapeutic skincare products. Retinol is widely used in dermatology treatment protocols for pore control, skin smoothing, and discoloration management. This clinical relevance fuels greater inclusion in topical prescription and OTC medications. The shift towards long-term maintenance therapies in acne treatment further drives the demand for cosmetic- and pharmaceutical-grade retinol formulations.

Restraints & Challenges

Regulatory restrictions and concentration limits: The EU retinol regulation in the cosmetic industry demands concentration limits to avoid irritation and toxicity exposure. This, in turn, increases the cost of reformulation and compliance. Regulatory restrictions on retinoids and toxicity regulations of vitamin A influence the permissible use level, particularly in leave-on products. On the other hand, consumer concerns about dryness and photosensitivity affect adoption in the general market. These factors further drive R&D investments in buffered and controlled-release formulations, thus putting a significant effect on the retinol side effects market.

Opportunity

Expansion through e-commerce and emerging applications: The growth in e-commerce sales of retinol products is expanding the reach of premium and dermatologically recommended brands. The market forecast indicates strong growth propelled by the growing awareness and affluence in the beauty market. The influence of clean beauty on retinol is encouraging stabilized, encapsulated, and plant-based retinol alternatives marketed as lower-irritation options. New retinol uses in body products, scalp treatments, and combination serums are unlocking new revenue streams in the retinol market.

Segmental Insights

This report offers detailed coverage of the Retinol market by type, formulation, and application to help readers identify the fastest expanding and most attractive demand segments.

By Type

-

Synthetic Retinol

Synthetic retinol accounted for the largest market share in the synthetic retinol market in 2025. This is propelled by the ease of chemical synthesis and purity. This ensures that the concentration is standardized for cosmetic and pharmaceutical purposes. Cost-effectiveness over natural retinol further cements its strong market position, especially in commercial anti-aging products.

-

Natural Retinol

The natural retinol market is relatively smaller but has a steady growth rate. Natural retinol is primarily derived from plant carotenoid sources. Natural retinol is preferred in clean-label and organic product lines. The growing acceptance of botanical and minimally processed ingredients further accelerates incremental demand.

-

Stabilized & Encapsulated Retinol

Stabilized retinol industry is projected to grow at a fast pace during the forecast period. Microencapsulated retinol technology advancements further improves standardized stability and controlled release. This overcomes the usual challenges of retinol oxidation and degradation. Encapsulation further minimizes irritation potential while maintaining bioactivity, further boosting dermatologist-formulated products.

By Formulation

-

Retinol Cream Market

The retinol cream market held the largest market share in 2025. Creams have a formulation that allows for slow absorption and minimize irritation, which makes them ideal for mass-market consumption. They are easily paired with moisturizing bases, which widens their appeal to first-time users.

-

Retinol Serum Market

Retinol serum market is the fastest-expanding formulation type. Serums have a higher concentration and faster dermal penetration, which makes them attractive to experienced users. Lightweight serums and advanced stabilization methods improve consumer acceptance.

-

Gel & Topical Formulations

The topical retinol market includes gels and light emulsions, which are in high demand for acne and oily skin. The market is steadily growing but is a niche industry compared to cream and serum formulations. The market experiences rising demand in dermatology clinics, where controlled and prescription-strength dosages are required.

By Application

-

Cosmetics & Personal Care

Cosmetics & Personal Care application accounted for the largest market share in the retinol in cosmetics market in 2025. Retinol is a non-negotiable active component in the anti-aging products market fueled by its established efficacy in collagen induction and skin texture enhancement.

-

Dietary Supplements

The retinol nutraceutical market is growing steadily with the supplementation of vitamin A for the immune system and vision. Government regulations and the standardization of dosage affect market positioning.

-

Food & Beverage Fortification

Retinol pharmaceutical market overlap occurs in fortified foods addressing micronutrient deficiencies. Nutrition programs with government support in developing nations sustain the baseline demand.

-

Animal Feed

The animal feed vitamin A market is a stable industrial use. Retinol is added to animal feed for promoting growth, immunity, and reproduction. Demand correlates with global meat and dairy production cycles.

Regional Analysis

North America Retinol Market Assessment

North America dominated the retinol market in 2025, driven by the adoption rate of dermatology and the established cosmetic and aesthetic procedure market. Consumer knowledge of anti-aging treatments and clinical skincare practices drove the demand for prescription-strength and over-the-counter retinoid products. According to the American Society of Plastic Surgeons, 2023 procedural statistics reflected a 5% rise in plastic surgeries and a 7% increase in minimally invasive procedures compared to the previous year. The rise in aesthetic procedures fueled the complementary topical skincare market, which in turn reinforced retinol consumption in dermatology clinics and high-end cosmetic brands. Well-developed supply chains and established regulatory systems also contributing to the stability of the market penetration.

Asia Pacific Retinol Market Insight

Asia Pacific retinol market experiencing rapid growth growth due to the increasing middle-class population, rising disposable income, and increased awareness about skincare. The India middle class is forecasted to increase from 432 million people in 2020-21 to 715 million by 2030-31, and further to 1.02 billion in 2047. This contributed to the increasing adoption of high-end skincare products, thereby driving the India retinol skincare market. On the other hand, the growth of the China anti-aging ingredients market contributed to the development of formulations and local production, thereby increasing consumption of local and foreign cosmetic brands.

Europe Retinol Market Overview

Europe retinol market is driven by the regulatory environment and the EU vitamin A regulation compliance. The market is influenced by the formulation of products, which are closely tracked to ensure compliance with concentration levels and packaging, thereby affecting innovation and product development in the cosmetic industry. The regulatory environment has heightened the need for clinical evidence and safety information, thereby moderating product development and maintaining a steady market for dermatologist-recommended skincare products. The established high-end beauty markets in France, Germany, and Italy have maintained a stable consumption pattern within a defined regulatory compliance framework.

Middle East Retinol Market Assessment

Middle East retinol market grew steadily, driven by increasing consumer expenditure on high-end skincare products and the rising number of aesthetic clinics in the UAE and Saudi Arabia. Market demand was driven by urban areas where there was a growing awareness of anti-aging treatments and dermatological procedures. The retailing of products and brand presence in the Middle East region has helped to create a stable market for retinol-based products in the premium and cosmeceutical market.

Heat Map Analysis

|

Region |

Market Position |

Growth Momentum |

Regulatory Strength |

Recycling Infrastructure |

Secondary Lead Production Base |

|

North America |

Leading |

High |

High |

Low |

Low |

|

Asia Pacific |

High |

Very High |

Medium |

Low |

Low |

|

Europe |

Medium–High |

Medium |

Very High |

Low |

Low |

|

Middle East |

Emerging |

Medium–High |

Medium |

Low |

Low |

Strategic Insights & Future Outlook

The future outlook for the retinol market is positive due to the demand for scientifically proven anti-aging products and the development of the skincare ingredients market. The retinol ingredient is a major player in the anti-aging ingredients market, but the future growth of retinol is now more reliant on the stabilization of science, high-end branding, and regulation rather than volume growth.

-

Technological Innovation in Stabilization

The instability of retinol is a major factor for innovation in encapsulation, controlled release, and oxygen-resistant packaging. These technologies enhance efficacy preservation, tolerability, and shelf life, making possible the development of more advanced products. The ability to stabilize is becoming a key differentiator among ingredient companies and branded players.

-

Premiumization of Skincare

Premium and dermo-cosmetic branding remains a driving force in market demand. Consumers are prepared to pay for dermatologist-backed efficacy and visible anti-aging results. Higher concentration products, combination actives, and clinical claims continue to support pricing power and margin growth in the anti-aging ingredients market.

-

Regulatory Evolution

The regulatory focus, especially in Europe and certain Asian countries, is increasing regarding acceptable concentration levels and the ease of understanding labeling. The challenge of compliance requires better safety documentation and harmonized claims. This scenario is more suited to established companies with proven formulations and effective manufacturing process controls.

-

Long-Term Investment Opportunities

Investment opportunities for Retinol exist in brands and suppliers with sophisticated formulation development and harmonized regulations worldwide. The growth, however, remains in North America and Asia Pacific, driven by the rising middle class and contributing to the long-term resilience of the category.

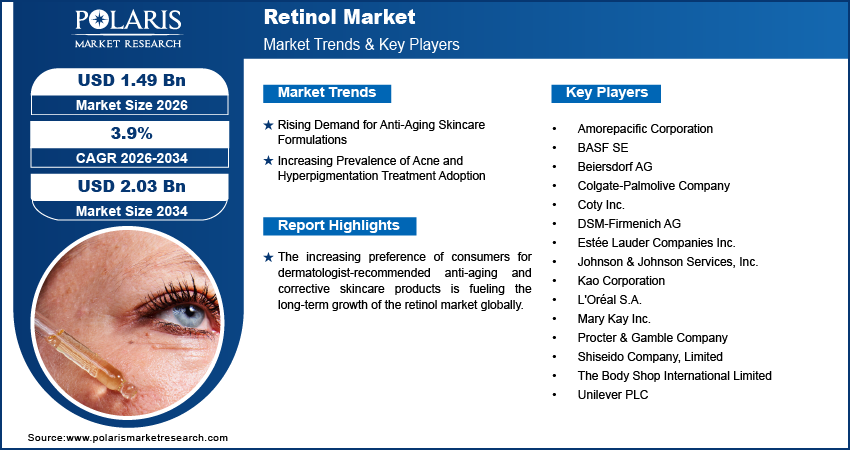

Key Players & Competitive Analysis Report

The retinol market is moderately consolidated, driven by the presence of global personal care conglomerates and specialty ingredient providers serving the premium skincare, dermo-cosmetic, and mass market. The competitive rivalry is driven by the formulation stability, clinical efficacy positioning, brand differentiation, and regulatory compliance. Global brands require vertically integrated R&D, dermatological testing facilities, and distribution networks to maintain market share and pricing leadership. Specialty ingredient suppliers compete on the basis of the degree of purity, encapsulation technology, and reliability of supply to support anti-aging, acne treatment, and skin regeneration.

Key companies shaping the global retinol market include Amorepacific Corporation, BASF SE, Beiersdorf AG, Colgate-Palmolive Company, Coty Inc., DSM-Firmenich AG, Estée Lauder Companies Inc., Johnson & Johnson Services, Inc., Kao Corporation, L'Oréal S.A., Mary Kay Inc., Procter & Gamble Company, Shiseido Company, Limited, The Body Shop International Limited, and Unilever PLC.

Key Players

- Amorepacific Corporation

- BASF SE

- Beiersdorf AG

- Colgate-Palmolive Company

- Coty Inc.

- DSM-Firmenich AG

- Estée Lauder Companies Inc.

- Johnson & Johnson Services, Inc.

- Kao Corporation

- L'Oréal S.A.

- Mary Kay Inc.

- Procter & Gamble Company

- Shiseido Company, Limited

- The Body Shop International Limited

- Unilever PLC.

Industry Developments

- April 2025: Obagi Medical introduced a new retinol 1.0 product designed to improve tolerability while addressing the appearance of aging. This product launch further expanded the company’s retinol offerings, providing consumers with a dermatologist-recommended choice within the retinol market.

- January 2025: BASF’s Personal Care division launched a new encapsulation technology intended to improve the delivery and stability of retinol in cosmetic formulations. This technology further enhanced the development of retinol-based products by ensuring that the active ingredients are more effective and less irritating, thus facilitating further launches in advanced anti-aging and skin renewal products.

Retinol Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021-2034)

- Synthetic Retinol

- Natural Retinol

- Stabilized & Encapsulated Retinol

By Formulation Outlook (Revenue, USD Billion, 2021-2034)

- Retinol cream

- Retinol serum

- Gel & topical formulations

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Cosmetics & Personal Care

- Dietary Supplements

- Food & Beverage Fortification

- Animal Feed

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Retinol Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 1.44 Billion |

|

Market Size in 2026 |

USD 1.49 Billion |

|

Revenue Forecast by 2034 |

USD 2.03 Billion |

|

CAGR |

3.9% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2022–2024 |

|

Forecast Period |

2026–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2026 to 2034 |

|

Report Coverage |

Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 1.44 billion in 2025 and is projected to grow to USD 2.03 billion by 2034.

North America dominated the retinol market due to the high adoption rate in dermatology, awareness of anti-aging treatments, and a well-established premium skincare market.

Cosmetic and personal care manufacturers represent the largest application, followed by pharmaceuticals, nutraceuticals, and fortified foods.

A few of the key players in the market are Amorepacific Corporation, BASF SE, Beiersdorf AG, Colgate-Palmolive Company, Coty Inc., DSM-Firmenich AG, Estée Lauder Companies Inc., Johnson & Johnson Services, Inc., Kao Corporation, L'Oréal S.A., Mary Kay Inc., Procter & Gamble Company, Shiseido Company, Limited, The Body Shop International Limited, and Unilever PLC.

Growth is fueled by the increasing demand for anti-aging products, adoption of acne and hyperpigmentation treatments, expansion of high-end skincare product lines, and growth of e-commerce retinol product sales.

Page last updated on:

Mar-2026

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

Market size estimates (USD Mn/Bn)

Segment-wise distribution (%)

Growth metrics (CAGR %)

Final Outputs

Structured tables and charts

Segment-level datasets

Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements