What is the Current Market Size?

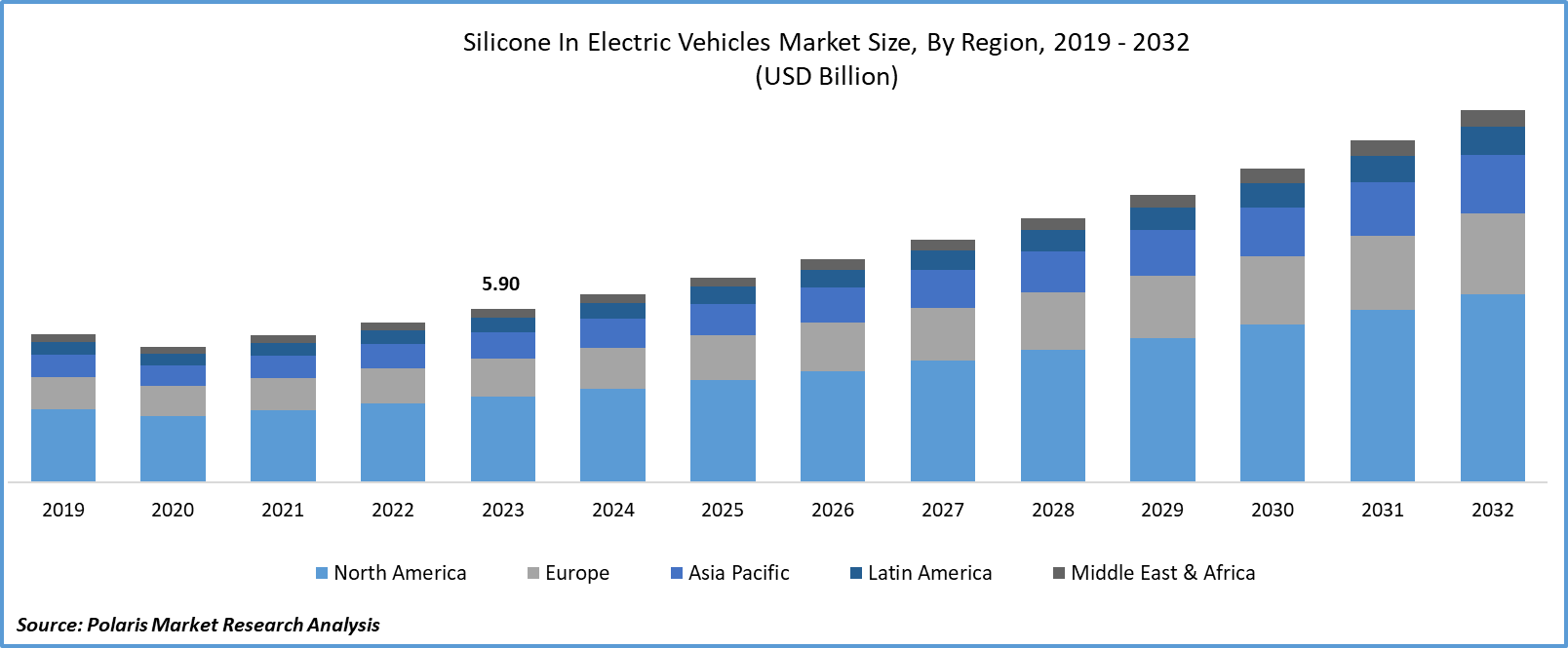

The global silicone in electric vehicles market size was valued at USD 6.95 billion in 2025. The market is anticipated to grow from USD 7.53 billion in 2026 to USD 14.72 billion by 2034, exhibiting a CAGR of 8.74% during the forecast period.

Market Statistics

- 2025 Market Size: USD 6.95 billion

- 2034 Projected Market Size: USD 14.72 billion

- CAGR (2026-2034): 8.74%

- Asia Pacific: Largest market in 2025

Industry Trends

Silicone finds extensive application in electric vehicles (EVs) owing to its exceptional electrical insulation properties, remarkable thermal stability, and resistance to extreme temperatures. It serves a multitude of purposes, including battery systems, electric motors, connectors, cables, sealants, and adhesives within EVs. The market for silicone in electric vehicles is poised for substantial growth, primarily fueled by the escalating global adoption of electric vehicles. Governments worldwide are actively advocating for reduced greenhouse gas emissions, thereby incentivizing the shift towards electric transportation. Furthermore, the increasing demand for lightweight and energy-efficient vehicles is bolstering the necessity for silicone in EVs.

However, there is a rising inclination towards silicone-based materials endowed with superior thermal conductivity. These materials aid in the efficient dissipation of heat from electric vehicle components, thus optimizing overall performance and efficacy. Additionally, there is notable progress in the development of advanced silicone formulations characterized by enhanced mechanical strength and durability, addressing the evolving needs of the market, resulting in the growth of silicone in electric vehicles market share.

The silicone in electric vehicles report details key market dynamics to help industry players align their business strategies with current and future trends. It examines technological advances and breakthroughs in the industry and their impact on the market presence. Furthermore, a detailed regional analysis of the industry at the local, national, and global levels has been provided.

To Understand More About this Research: Download Sample Report

With growing awareness of climate change and its impacts, there's increased pressure to reduce greenhouse gas emissions. EVs produce zero tailpipe emissions during operation, making them a cleaner alternative to traditional internal combustion engine vehicles. Many governments around the world are offering incentives and subsidies to encourage the adoption of EVs. These incentives may include tax credits, rebates, and grants, making EVs more affordable for consumers.

The silicone in electric vehicles (EVs) market is witnessing robust innovation across multiple fronts. As the demand for EVs continues to surge, propelled by environmental concerns and regulatory mandates, manufacturers are intensifying efforts to enhance the performance, durability, and safety of EV components through silicone-based solutions. Thus the silicone in the electric vehicles market is expected to grow during the forecast period.

Additionally, R&D efforts are directed toward developing advanced silicone-based thermal interface materials (TIMs) to address heat dissipation challenges in EVs. These materials play a crucial role in optimizing the performance and reliability of electric vehicle systems, particularly in high-temperature environments. The silicon in the electric vehicles market is characterized by a concerted effort to address key challenges and capitalize on emerging market opportunities. Collaboration between industry stakeholders, research institutions, and government agencies is driving forward-thinking initiatives aimed at shaping the future of sustainable and efficient electric transportation.

- For instance, In March 2023, Shin-Etsu Chemical innovated a silicone rubber formulation tailored for molding, precisely engineered to function as an optimal insulation coating material for high-voltage cables used in automobiles.

Moreover, there is a growing focus on sustainability, driving the development of eco-friendly silicone alternatives derived from renewable sources or recycled materials. This reflects the industry's commitment to reducing environmental impact while meeting the evolving needs of the EV market. In parallel, advancements in manufacturing techniques, such as additive manufacturing and advanced molding processes, are enabling the production of highly customized silicone components tailored to specific EV design requirements. These innovations aim to enhance production efficiency, reduce costs, and accelerate the adoption of silicone-based solutions in the rapidly expanding EV ecosystem, which further propel the silicone in electric vehicles market share.

Key Takeaways

- Asia Pacific dominated the largest market and contributed to more than 35% of the share in 2025.

- North America is expected to witness the fastest CAGR during the forecast period.

- By product type category, the elastomers segment accounted for the largest market share in 2025.

- By vehicle type category, light motor vehicles segment is expected to grow at the fastest CAGR during the forecast period.

What are the market drivers driving the demand for Silicone In Electric Vehicles Market?

Increasing Use of Silicone in EV Due to Its Thermal Stability Projected to Spur Product Demand.

The increasing use of silicone in electric vehicles (EVs) is primarily driven by its exceptional thermal stability, which is crucial for various components within EVs. Silicone is used in lithium-ion batteries, which power many electric vehicles. Silicone-based materials can improve the performance, safety, and longevity of these batteries. They are used in the production of battery electrodes, electrolytes, and battery pack sealants. Electric vehicles generate heat during operation, particularly in the battery pack and power electronics. Silicone-based thermal interface materials (TIMs) are used to manage heat transfer efficiently. These TIMs help dissipate heat from critical components, ensuring optimal performance and longevity. Silicone rubber is highly resistant to extreme temperatures, moisture, and chemicals. It is used for sealing battery compartments, electrical connections, and other sensitive areas in EVs to prevent water ingress, corrosion, and electrical shorts. This factor of silicone has increased its use in electric vehicles and shows a tremendous rise in silicone in the electric vehicles industry analysis.

Silicone rubber is an excellent electrical insulator and is used to insulate wires and cables in electric vehicles. It protects against high voltages, extreme temperatures, and environmental hazards. Silicone materials are used in the design and manufacturing of charging connectors for electric vehicles. Silicone seals and gaskets ensure waterproofing and prevent dust and debris from entering the connector interface. Silicone-based materials can be used as coatings or potting compounds for electric motor components. These materials offer protection against moisture, chemicals, and high temperatures, enhancing the durability and reliability of electric motors and resulting in an increasing market share of silicon in electric vehicles.

Which factor is restraining the demand for Silicone in Electric Vehicles?

High cost and long-term reliability are likely to impede the market growth.

Silicones can be relatively expensive compared to alternative materials, which can pose a challenge for widespread adoption in the EV market. Cost-effectiveness is a significant consideration While silicone is known for its durability, long-term performance in certain EV applications may still be a concern. Factors such as degradation over time due to exposure to heat, moisture, and other environmental factors could affect reliability, particularly in critical components like battery seals or thermal management systems. Or manufacturers striving to keep EV prices competitive with traditional vehicles. While silicone has good insulating properties, it has limited conductivity compared to metals like copper or aluminum. Manufacturers may opt for cheaper alternatives to silicone for certain components to reduce overall production costs, which may hamper the market growth.

Corporate R&D & Product Development Focus (DuPoint)

|

Dimension |

Corporate R&D & Product Focus for Silicone in EVs |

Key EV Application Areas Mentioned |

Example Technologies / Programs (from DuPont) |

R&D Themes Highlighted |

|

Overall e‑mobility strategy |

DuPont describes itself as a technology‑based materials innovator supporting alternative drive and electric vehicles, integrating silicone materials/adhesives into full battery and powertrain systems. |

Alternative drive vehicles, battery‑electric and hybrid platforms, advanced drivetrains. |

“Next‑Generation Technology for Alternative Drive Vehicles” platform, integrating advanced polymers, adhesives and thermal materials. |

System-level materials engineering for EV platforms (integration of structural, thermal and electrical functions). |

|

Battery assembly & safety |

BETAFORCE elastic structural adhesive is developed for EV battery assembly, especially pouch cell bonding, enabling durable, crashworthy packs by bonding aluminum‑laminate substrates without primers. |

Battery modules and packs, pouch cell bonding, structural battery bonding in EV platforms. |

BETAFORCE elastic structural adhesive winning a 2024 R&D 100 Award for EV battery assembly. |

R&D on crashworthiness, elastic structural bonding under dynamic and thermal loads, compatibility with lightweight materials. |

|

Thermal & electrical management |

DuPont EV materials literature highlights insulation and thermal management materials (including silicone‑containing systems) for motors and power electronics to improve efficiency and reliability. |

Electric motors, inverters, power electronics and high‑voltage components in EVs. |

Silicone materials & adhesives listed as a key portfolio element supporting insulation in electric vehicles and industrial motors. |

Focus on high‑temperature stability, insulation reliability and integration of insulation with bonding/assembly processes. |

|

Sustainability / next‑gen vehicles |

Corporate sustainability and innovation communications link new material platforms to “next‑generation electric vehicles,” emphasizing lower environmental impact and higher energy efficiency. |

Next‑generation EV architectures and alternative drive platforms. |

Sustainability and innovation initiatives aimed at enabling more efficient, lightweight and durable EV components. |

R&D driven by lifecycle emissions reduction, material efficiency and safety for EVs. |

Momentive Performance Materials

|

Dimension |

Corporate R&D & Product Focus for Silicone in EVs |

Key EV Application Areas Mentioned |

Example Technologies / Programs (from Momentive) |

R&D Themes Highlighted |

|

E‑mobility positioning |

Momentive states that its advanced silicones “play an essential role” in vehicles of today and tomorrow, supporting autonomous, connected and electrified mobility. |

E‑mobility and electrification, including BEVs, HEVs and “New Energy Vehicles” (NEVs). |

“Material Solutions for E‑mobility & Electrification” portfolio and NEVSil specialty elastomers for New Energy Vehicles. |

Platform‑level development of silicone solutions tailored to EV system needs rather than generic industrial use. |

|

Power electronics |

R&D focuses on thermal management, encapsulation/potting and sealing for inverter systems, IGBT modules, DC/DC converters and onboard chargers using silicone materials. |

Inverter systems, DC/DC converters, onboard chargers and related power electronics. |

SilCool thermal management silicones for keeping critical electronics cool in harsh environments. |

High thermal conductivity, electrical insulation, vibration damping and long‑term reliability for high‑power EV electronics. |

|

High‑voltage battery systems |

Portfolio includes silicone thermal gap fillers, thermally conductive adhesives, potting gels and sealing materials aimed at battery modules and housings. |

Battery modules and packs, battery housing components for EVs. |

Silicone gap fillers and adhesive TIMs; SFR100 silicone fluid as a non‑halogenated flame retardant for battery housings. |

Thermal runaway mitigation, fire safety, mechanical toughness and non‑corrosive flame retardancy for battery designs. |

|

Fire safety & polymer additives |

Dedicated silicone fluids improve fire safety in EV polycarbonate components and transparent parts, balancing mechanical and optical properties. |

Front‑end modules, headlamp and rear lamp covers, other EV polycarbonate parts. |

SFR320 silicone fluid for non‑transparent EV polycarbonate parts and clear exterior lighting covers. |

Flame‑retardant performance without compromising clarity or introducing highly corrosive or EHS‑problematic additives. |

|

Sensors, cables & lighting |

Momentive silicones provide coatings, sealing and optical management for sensors, cables/connectors and interior/exterior lighting in EVs. |

Sensor coatings, cable and connector materials, LED lighting modules in EVs. |

TSR spherical polymethylsilsesquioxane particles for light diffusion to reduce LED “hot spots” in EV lighting. |

Durability of electronics, light management, and comfort/visibility improvements via silicone‑based optical and protective materials. |

Report Segmentation

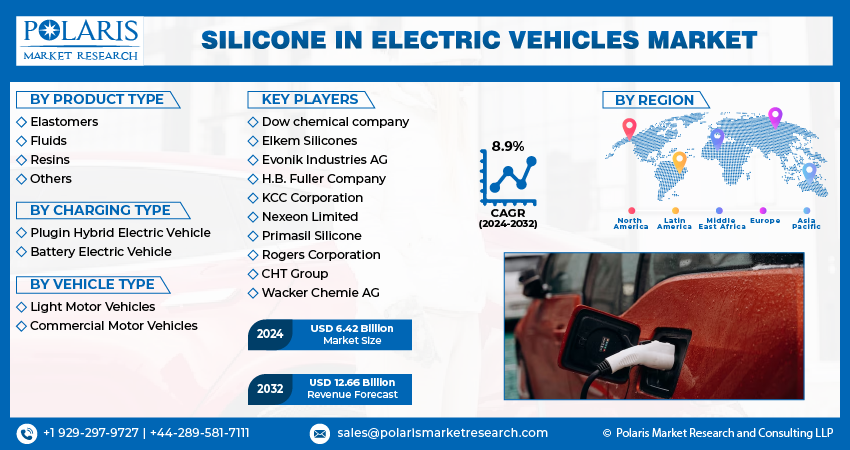

The market is primarily segmented based on product type, charging type, vehicle type, and region.

|

By Product Type |

By Charging Type |

By Vehicle Type |

By Region |

|

|

|

|

To Understand the Scope of this Report: Request Customization

Category Wise Insights

By Product Type Insights

Based on product type analysis, the market is segmented on the basis of Elastomers, Fluids, Resins, and Others. The elastomers segment accounted for the largest market share in 2025. Elastomers play a crucial role in safeguarding electric vehicle (EV) components by dissipating battery heat and shielding against electromagnetic interference. They also effectively manage battery temperature, a critical aspect of EV operation.

In the electric vehicle market, the fluids segment is anticipated to experience rapid growth during the forecast period. These fluids serve various purposes, such as enhancing thermal stability and transmitting torque through fan clutches in EVs. Additionally, they are utilized as coatings for high-voltage cables and as modifiers for tires. The growth of this segment is further propelled by a range of incentives offered by countries like Norway, Sweden, the UK, and Germany. Furthermore, resins, valued for their weather resistance, water and fire resistance, and dielectric properties, are essential components in EV technology. Silicone resins, in particular, find application in roll impregnation thanks to their advantageous characteristics.

By Vehicle Type Insights

Based on vehicle type analysis, the market has been segmented based on light motor vehicles and commercial motor vehicles. Light motor vehicles are expected to grow at the fastest CAGR during the forecast period. As the adoption of electric vehicles continues to rise, there will naturally be a corresponding increase in the demand for components and materials suitable for EV manufacturing. Silicones play a crucial role in various aspects of EV production, including sealing, bonding, thermal management, and electrical insulation. The development of new technologies and innovations in both the automotive and materials sectors can lead to greater integration of silicones in EVs. Growing awareness of climate change and air pollution is driving individuals and governments to seek cleaner transportation alternatives. Electric vehicles produce zero tailpipe emissions, making them attractive for reducing greenhouse gas emissions and improving air quality. Continuous advancements in battery technology, electric drivetrains, and charging infrastructure have made electric vehicles more practical, convenient, and affordable. Range anxiety, a common concern for early adopters, is decreasing as battery technology improves, allowing for longer driving ranges on a single charge.

Regional Insights

Asia Pacific

The Asia Pacific region dominated the global market with the largest market share in 2025. Increasing urbanization in the region has led to an upsurge in the number of vehicles and raised traffic congestion, which leads to problems of air and noise pollution. These challenges create an urgent need to promote the use of low-emission vehicles such as electric vehicles. Therefore, the rise in electric vehicles may, in turn, increase the demand for silicone products over the forecast period. The boom of the electric vehicle industry in China, Japan, and other countries, thanks to growing domestic consumption and favorable government policies, is expected to complement the growth of the market in the coming years. Hence, silicone in the electric vehicle market is expected to dominate the Asia Pacific region in the upcoming years.

North America

The North American region is expected to witness the fastest-growing CAGR during the projected period; governments in North America are increasingly implementing policies and regulations to promote the adoption of electric vehicles as part of their efforts to reduce greenhouse gas emissions and combat climate change. Substantial investments in EV infrastructure and incentives for consumers are driving the uptake of electric vehicles in the region. However, the growing awareness among consumers in North America about the environmental benefits of electric vehicles, as well as their potential cost savings in the long run. As a result, there is increasing demand for electric vehicles across various segments of the market, from passenger cars to commercial vehicles, increasing the silicone in the electric vehicle market share.

Competitive Landscape

The Silicone in Electric Vehicles Market is fragmented with competition due to several players' presence. The silicone for electric vehicles market is diverse and dynamic, with multiple players competing on various fronts to capture market share and drive innovation in this rapidly evolving industry. Collaboration, innovation, and responsiveness to market trends will be key factors determining success in the increasingly competitive EV market. Market participants participate in these events to strengthen their positions.

Some of the major players operating in the global market include:

- Dow chemical company

- Elkem Silicones

- Evonik Industries AG

- H.B. Fuller Company

- KCC Corporation

- Nexeon Limited

- Primasil Silicone

- Rogers Corporation

- CHT Group

- Wacker Chemie AG

Recent Developments

- In September 2025, DOW launched DOWSIL EG-4175 silicone gel targets next-generation power electronics. The material is engineered for IGBT modules operating at higher voltages and temperatures up to 180°C. It provides protection through vibration absorption and self-healing properties, while room-temperature curing supports manufacturing efficiency.

- In December 2023, Panasonic agreed with the US startup Sila to acquire silicon for incorporation into electric vehicle (EV) batteries, aiming to enhance its position in the EV industry through this partnership. By integrating Sila's silicon anodes into batteries at its global factories, Panasonic seeks to improve the performance and efficiency of EV batteries, thereby advancing the development of electric vehicles.

- In October 2022, Dow introduced the world's inaugural recyclable silicone self-sealing tire solution. This innovative solution has been effectively implemented in Bridgestone's recently unveiled B-SEALS, representing a breakthrough in recyclable tire sealant technology.

Report Coverage

The Silicone in Electric Vehicles Market report emphasizes key regions across the globe to provide a better understanding of the product to the users. Also, the report provides market insights into recent developments, and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis of various paradigm shifts associated with the transformation of this technology

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, product type, charging type, vehicle type, and futuristic growth opportunities.

Silicone In Electric Vehicles Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2025 |

USD 6.95 billion |

| Market size value in 2026 | USD 7.53 billion |

|

Revenue Forecast in 2034 |

USD 14.72 billion |

|

CAGR |

8.74% from 2026 – 2034 |

|

Base year |

2025 |

|

Historical data |

2021 – 2024 |

|

Forecast period |

2026 – 2034 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2026 to 2034 |

|

Segments Covered |

By Product Type, By Charging Type, By Vehicle Type, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

Gain profound insights into the 2025 silicone in electric vehicles market with meticulously compiled statistics on market share, size, and revenue growth rate by Polaris Market Research Industry Reports. This thorough analysis not only provides a glimpse into historical trends but also unfolds a roadmap with a market forecast extending to 2032. Immerse yourself in the comprehensive nature of this industry analysis through a Download Sample Report.

Browse Our Top Selling Reports

Lab Automation Market Size, Share 2024 Research Report

Airport Sleeping Pods Market Size, Share 2024 Research Report

Catalyst Handling Services Market Size, Share 2024 Research Report

Less Lethal Ammunition Market Size, Share 2024 Research Report

FAQ's

The global Silicone in Electric Vehicles Market size is expected to reach USD 14.72 billion by 2034.

Key players in the market are Dow Chemical Company, Elkem Silicones, Evonik Industries AG, H.B. Fuller Company, KCC Corporation

North American contribute notably towards the global Silicone In Electric Vehicles Market

Silicone In Electric Vehicles Market exhibiting the CAGR of 8.74% during the forecast period.

The Silicone In Electric Vehicles Market report covering key segments are product type, charging type, vehicle type, and region.

Page last updated on:

Feb-2024

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

1. Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

2. Data Collection

We gather information from both public and verified sources:

3. Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

Estimates are cross-verified across three sources:

Company-level data

• Primary inputs from industry participants

• Secondary benchmarks and published data

Variance maintained within +5-10%

Adjustments applied to align estimates

Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

Segment totals validated to 100%

Regional estimates aligned with global market size

Historical trends compared against forecast outputs

Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

Market size estimates (USD Mn/Bn)

Segment-wise distribution (%)

Growth metrics (CAGR %)

Final Outputs

Structured tables and charts

Segment-level datasets

Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements