Solar Panel Recycling Market Size, Share, Industry Report, 2026-2034

REPORT DETAILS

Market Statistics

Market Overview

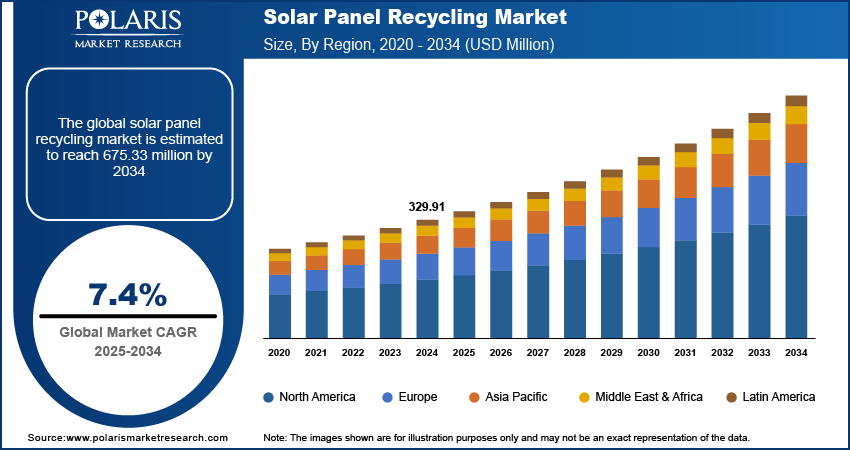

The global solar panel recycling market size was valued at USD 353.88 million in 2025, growing at a CAGR of 7.5% from 2026 to 2034. Market growth is primarily driven by government initiatives and regulations that encourage the responsible disposal of solar panels.

A large wave of end-of-life solar panels is expected from 2027 onward as early solar projects enter decommissioning and repowering phases. This emerging PV waste wave is making compliant solar panel disposal and solar module recycling unavoidable, driven by stricter regulations and circular economy goals.

Key Insights

- The silicon segment is anticipated to register the fastest growth during the projection period. This is primarily because crystalline silicon is present in most solar panels.

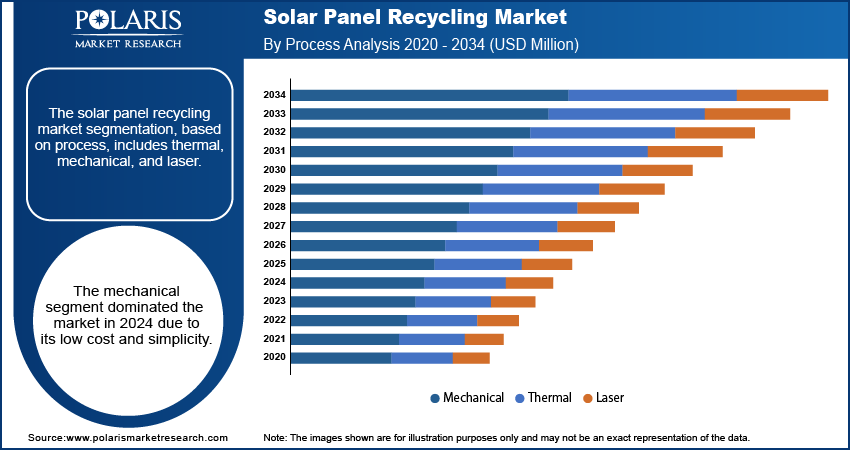

- The mechanical segment accounted for the largest market share in 2025. The simplicity, low cost, and high recovery rate of valuable materials contribute to the segment’s leading market position.

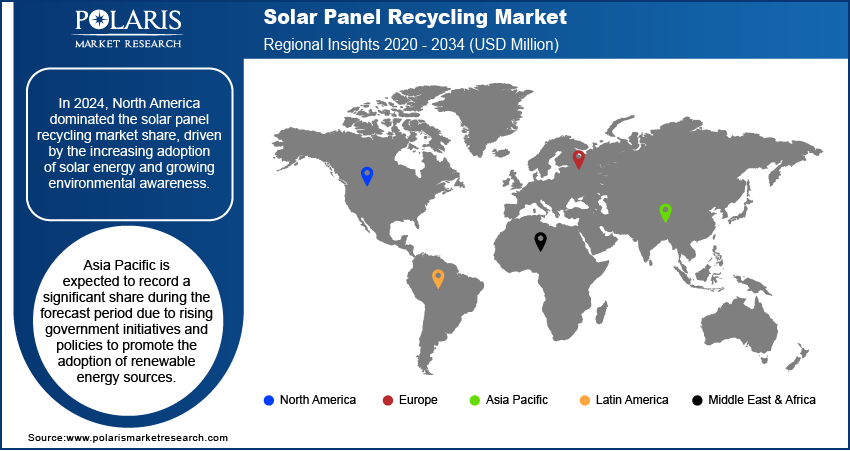

- North America led the global market in 2025. The regional market dominance is primarily attributed to growing environmental awareness and rising adoption of solar energy.

- Asia Pacific is anticipated to register a significant market share during the projection period. This is due to the launch of initiatives and policies by governments across Asia Pacific to promote the adoption of renewable energy sources.

- Extended producer responsibility (EPR) and WEEE regulations are emerging as key promoters of solar panel recycling. The solar panel producers have increasingly been held accountable for managing end-of-life solar panels and their disposal.

- The cost of recycling is a major issue, but improved material recovery has opened new avenues. The increased recovery of silicon, glass, and metallic resources is offsetting the recycling costs.

Industry Dynamics

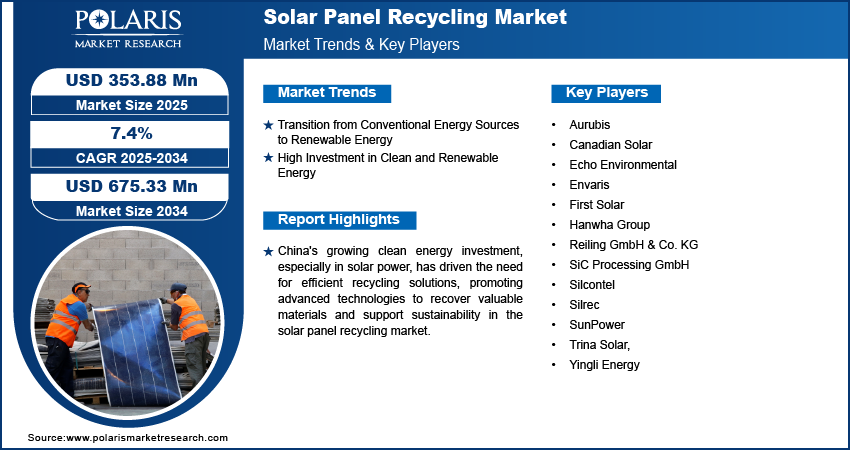

- There has been a transition from conventional to alternative energy sources, such as solar, resulting in a growing need to dispose of used solar panels.

- Rising private, corporate, and government investments in solar energy as a sustainability and carbon-emission-reduction strategy are boosting the market.

- New markets are expected to open as a result of advances in recycling technology.

- The high costs of recycling solar panels might hamper the growth of the solar panel market.

Market Statistics

- 2025 Market Size: USD 353.88 million

- 2034 Projected Market Size: USD 675.33 million

- CAGR (2026-2034): 7.5%

- North America: Largest Market in 2025

Solar panel recycling involves harvesting materials such as silicon, metals, and glass from decommissioned or damaged solar panel products, with the end result of repurposing them in the manufacture of other products. This is crucial in managing waste and reducing the pollution associated with solar energy.

The PV module recycling process follows a simple workflow. Panels are first collected and transported for dismantling, during which the aluminum frames are recycled, and cables are removed. Next, delamination loosens bonded layers, followed by material separation to enable glass recovery and metal extraction. The recovered materials are then refined and sent to end markets for reuse.

Government policies promote the responsible disposal of solar panels and support the growth of renewable energy. In May 2022, the Ministry of Environment, Forests, and Climate Change formally included solar PV cells and modules under the E-waste rules for solar PV, clarifying panel classification, requiring the use of authorized recyclers, and introducing takeback and EPR compliance duties for producers. Globally, solar panel recycling regulations are also tightening, with the EU WEEE directive setting a clear benchmark and the US following state-level PV waste regulations, making compliant recycling a standard requirement.

The solar panel recycling market demand is expected to rise during the forecast period due to the continued high value of the renewable energy industry and rising investments in solar power generation. The development of solar technology is expected to attract investment and create new opportunities for industry participants to grow. Due to the quick pace of PV installation, the number of retired PV panels has also surged. This is expected to accelerate the expansion of the solar panel recycling industry. According to the International Energy Agency, the value of clean energy resources could exceed USD 15 million by 2050. This amount can produce 630 GW of electricity using 2 million solar panels. As more solar panels approach the end of their lifespans every 10 to 20 years, demand for solar panel recycling will increase.

Source: Polaris Market Research Analysis

Want a Deeper Look at Key Market Players? Download Sample Report

Market Dynamics

Transition to Renewable Energy and Repowering Cycles

The rapid transition from traditional energy sources to solar energy is driving the installation of more solar panels. As early solar facilities mature, repowering projects that can involve replacing these solar panels even before they reach the end of their lives are becoming more common. This condition leads to solar panels nearing the end of their useful lives, which need to be traced and disposed of or recycled properly. Utility-scale power plant operators are also planning decommissioning in advance. These factors are directly driving growth in the solar panel recycling industry.

Investment Led Scale Up of Solar Assets

High investments in clean and renewable energy continue to expand the global solar base. As more panels are installed, future recycling volumes grow in parallel. Governments and developers are now focusing not only on installation but also on end-of-life planning, including collection networks and approved recycling routes. This shift is strengthening the need for organized reverse logistics and reliable recycling infrastructure.

Restraint: Logistics and Collection Gaps

Major challenges persist, despite the increasing demand: limited collection networks and weak recycling infrastructure. Transporting large numbers of panels is expensive, and reverse logistics remains significantly fragmented in many regions. The lack of accessible solar panel takeback programs slows the adoption of recycling and increases overall costs.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Analysis

Assessment by Type Outlook

The solar panel recycling market segmentation, by type, includes crystalline silicon (c-Si), monocrystalline, polycrystalline, and thin-film. Crystalline silicon panels are further divided into monocrystalline and polycrystalline modules. The silicon-based sector is projected to record the fastest growth over the forecast period, as over 95% of the solar panel market uses c-Si technology. Such solar panels are composed of materials that can be recycled, such as silicon, silver, copper, and aluminum.

Recycling of c-Si panels commonly uses mechanical recycling, often combined with thermal treatment or laser delamination in hybrid approaches. These processes improve material separation and support high-purity silicon recovery, which is critical for reuse in new solar modules. Thin-film PV recycling follows different pathways due to its material mix, but it still accounts for a smaller share of total volumes.

Evaluation by Process Outlook

The solar panel recycling market segmentation, based on process, includes thermal, mechanical, and laser. Mechanical recycling accounted for the highest share in the solar panel recycling market in 2025. Mechanical recycling is apparently done by the physical decomposition of solar cells into smaller units such as glass, aluminum, and silicon, which can then be reused. This method is commonly used as it is relatively inexpensive and easy to execute, and a high percentage of the material in solar cells is recyclable. The laser and thermal sectors will also register significant growth over the forecast period. The demand for high-purity silicon wafers will continue to rise. There is also a need to recycle used solar panels sustainably and responsibly. This will fuel market growth.

How Solar Panels are Recycled?

Collection & Sorting: The old or dysfunctional panels are collected from households, commercial establishments, and solar farms. The materials are sorted by type: crystalline silicon or thin-film modules, as they must be recycled differently.

Dismantling: The removal of frames, cables, and junction boxes follows. This step enables recyclers to extract valuable materials, such as aluminum and copper, from these components.

Delamination & Material Separation: The panels undergo delamination processes to separate the glass and solar cell material from the plastic. The glass, metals, and silicon are further separated.

Refining & End Markets: Recycled materials are refined. Glass, metal, and silicon are then processed into new products, such as solar panels, to keep the material loop and prevent it from going to a landfill.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Analysis

By region, the study provides insights into the solar panel recycling market in North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, the North America solar panel recycling market dominated due to strong solar adoption and rising focus on end-of-life planning. Large-scale solar deployment across the US and Canada is now moving into long-term asset management, where panel retirement and repowering are planned in advance. State-level policies are also taking their due role. Various states in the USA have enacted recycling regulations. Even take-back schemes have been introduced by some states. In addition, some states also make it compulsory for the producers of solar panels to recycle their waste. However, more solar panel systems are also nearing the end of their lives. This has increased the need for solar PV waste management in the USA.

Asia Pacific PV recycling is expected to capture a significant share of the market during the forecast period. The region is home to a large concentration of solar panel manufacturing, creating high volumes of panels that will eventually reach the end of their life. Governments are supporting renewable energy adoption through policies and incentives, while recycling capacity is being built out to handle growing volumes. These efforts enable material recovery and strengthen the region's circular economy.

China PV recycling capacity is increasing as investment in the clean energy segment grows. China Briefing estimates that the region’s investment in the clean energy sector touched USD 863 million during 2023. The growing installation of solar panels in the region creates demand for efficient recycling solutions to dispose of old panels and related photovoltaic materials at the end of their lifecycles. The India solar waste policy and other regulations are also impacting the Asia Pacific region’s recycling industry.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players & Competitive Analysis Report

The solar panel recycling market is ever-changing, with many players competing to innovate and outdo one another. The major global players dominate the solar panel recycling market through their extensive research and development and innovations. These players also engage in M&As and collaborations to expand their product and market lines.

New entrants in this industry are changing the landscape of solar panel recycling by launching innovative products to meet the demands of various industries. This competitive scenario is also intensified by product innovations. A few major players in the solar panel recycling market include First Solar, Echo Environmental, Silcontel, Canadian Solar, Silrec, SunPower, Reiling GmbH & Co. KG, Trina Solar, Aurubis, Envaris, SiC Processing GmbH, Yingli Energy, and Hanwha Group.

Canadian Solar Inc., often referred to as CSI, is a global solar energy company headquartered in Guelph, Ontario, Canada. It manufactures photovoltaic modules and battery energy storage systems and delivers integrated solutions that power the future of solar energy, including inverters and EPC services. Canadian Solar operates across several continents, including manufacturing operations in China, Southeast Asia, and North America. With a recycling partnership, the company offers solar panel recycling services with SOLARCYCLE. This collaboration focuses on material recovery, maintaining traceability, and ensuring a secure chain of custody for end-of-life panels. Currently, Canadian Solar is considered one of the major PV recycling service providers in the market.

SunPower Corporation is a US solar energy firm headquartered in San Jose, California. The firm has a product portfolio comprising high-efficiency solar panels and energy storage products. However, SunPower primarily operates its solar energy solutions in North America, Europe, and Asia. SunPower has partnered with solar panel recycling firms to ensure all the disposed solar panels are recycled. The firm has emphasized the need to trace all solar panels to maintain a complete chain of custody for recycled solar panels. This follows best practices for managing PV waste.

List of Key Companies

- Aurubis

- Canadian Solar

- Echo Environmental

- Envaris

- First Solar

- Hanwha Group.

- Reiling GmbH & Co. KG

- SiC Processing GmbH

- Silcontel

- Silrec

- SunPower

- Trina Solar

- Yingli Energy

Economics of Solar Panel Recycling

The economics of solar panel recycling are driven by the balance between costs and recovered value. A cost stack may include collection, transportation, dismantling, delamination, and refining as processes that make up a major component of solar panel recycling costs. On the other side of the equation, the value stack derives its value from the material components of silicon, aluminum, copper, silver, and glass. Efficient recovery, especially of high-purity silicon, increases the value of materials recovery. Recycling becomes profitable when the value of these materials exceeds the costs. Strong demand for recycled materials, organized collection networks, and advanced recovery methods all improve PV recycling economics and overall profitability.

Solar Panel Recycling Industry Developments

- August 2025: First Solar Inc. announced the expansion of its global recycling capacity, underscoring ongoing investment in photovoltaic recycling infrastructure as part of its long-term sustainability and circular economy strategy.

- May 2025: Envaris GmbH introduced a hybrid solar panel recycling method integrating thermal and mechanical processes to enhance material recovery from end-of-life photovoltaic modules, boosting yields of silicon wafers and other valuable materials while lowering processing expenses.

- May 2025: SOLARCYCLE signed a Recycling Services Agreement with RWE Clean Energy, enabling and ensuring the responsible recycling of solar modules from various RWE solar sites upon reaching the end of their operational life.

- March 2025: ROSI partnered with Waste Experts and City Electrical Factors (CEF) in a bid to enhance the recycling of solar panels in the UK. This move was a response to the ever-increasing demand for proper disposal of end-of-life solar panels.

- October 2024: Runergy Alabama Inc., a leading US solar panel manufacturing company, teamed up with SOLARCYCLE, which will provide a minimum of 4 GW, or a total of 30 million square meters, of top-grade glass partially produced from recycled solar panels.

- January 2023: First Solar finished the sale of Luz del Norte, a utility-scale solar power facility in Copiapó, Chile, with a 141 MW AC capacity, to Toesca, a private asset manager with its headquarters in Chile.

- January 2023: CSI Solar signed an investment agreement with the municipal body of Jiangsu Province, China, according to a statement from Canadian Solar.

Solar Panel Recycling Market Segmentation

By Type Outlook (Revenue USD Million, 2021–2034)

- Silicon

- Monocrystalline

- Polycrystalline

- Thin-Film

By Process Outlook (Revenue USD Million, 2021–2034)

- Thermal

- Mechanical

- Laser

By Shelf-Life Outlook (Revenue USD Million, 2021–2034)

- Normal Loss

- Early Loss

By Regional Outlook (Revenue USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Solar Panel Recycling Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 353.88 Million |

| Market Size in 2026 | USD 379.72 Million |

| Revenue Forecast by 2034 | USD 675.33 Million |

| CAGR | 7.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Solar Panel Recycling Market FAQ's

The global solar panel recycling market is expected to grow at a CAGR of 7.5% to reach USD 675.64 million by 2034, driven by increasing solar installations.

Mechanical recycling leads the market. It efficiently recovers glass, aluminum, and silicon using cost-effective physical methods like shredding and crushing. Mechanical processes are widely used due to their simplicity, low solar panel recycling cost, and high materials recovery value.

Recyclers extract valuable materials such as silicon, silver, aluminum, copper, and glass from panel components. More than 80% of panel weight consists of silicon and metals; hence, recycling of these components becomes economically attractive due to their high recovery rate.

North America is the fastest-growing market, while Asia Pacific, led by China and India, is rapidly expanding its PV recycling capacity and compliance with solar waste policies.

High solar panel recycling costs (USD 15–45 per panel vs. USD 1–5 for landfill disposal), limited recycling infrastructure, and inconsistent regulations in some countries slow adoption. Weak collection networks and fragmented reverse logistics remain major obstacles.

A few key players in the market are First Solar, Echo Environmental, Silcontel, Canadian Solar, Silrec, SunPower, Reiling GmbH & Co. KG, Trina Solar, Aurubis, Envaris, SiC Processing GmbH, Yingli Energy, and Hanwha Group.

Download Sample Report of Solar Panel Recycling Market

Please fill out the form to request a customized copy of the research report.