Stirling Engine Market Report Size, Share & Global Trends, 2026-2034

REPORT DETAILS

Market Statistics

What is the Current Market Size?

The Stirling engine market size was valued at USD 1060.8 million in 2025. The market is projected to grow from USD 1161.6 million in 2026 to USD 2400.9 million by 2034, exhibiting a CAGR of 9.50% during 2026–2034.

Market Statistics

- 2025 Market Size: USD 1060.8 million

- 2034 Projected Market Size: USD 1161.6 million

- CAGR (2026-2034): 9.50%

- North America: Largest market in 2025

The Stirling engines market is witnessing significant growth owing to the increasing need for low-emission alternatives to internal combustion (IC) engines. Governments and industries worldwide are prioritizing the reduction of greenhouse gas emissions and the promotion of sustainability. These engines are a promising solution because of their high efficiency and minimal environmental impact. Unlike internal combustion engines that burn fuel to generate power, Stirling engines operate on an external heat source, allowing the use of renewable energy and waste heat. Thus, they are attractive to environmentally conscious consumers and businesses.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Emerging awareness regarding environmental issues is fueling the demand for Stirling engines. Consumers are becoming more educated about the adverse impact of traditional energy sources on the environment, leading to a shift toward greener technologies. This growing awareness is prompting companies to invest in clean energy solutions, including Stirling engines, which align with the global transition toward sustainable practices. As a result, more industries are exploring these engines for applications in transportation, power generation, and heating systems, significantly broadening their market reach.

The rising demand for renewable energy sources, particularly solar power, is enhancing the Stirling engine market prospects. Solar Stirling engines convert sunlight into mechanical energy, making them ideal for solar power generation. The integration of Stirling engines enhances energy conversion, leading to increased efficiency in solar energy systems deployed worldwide. This potential of Stirling engines to meet the rising demand for renewable energy sources is a reason for optimism about the future of sustainable, low-emission solutions.

Drivers and Trends

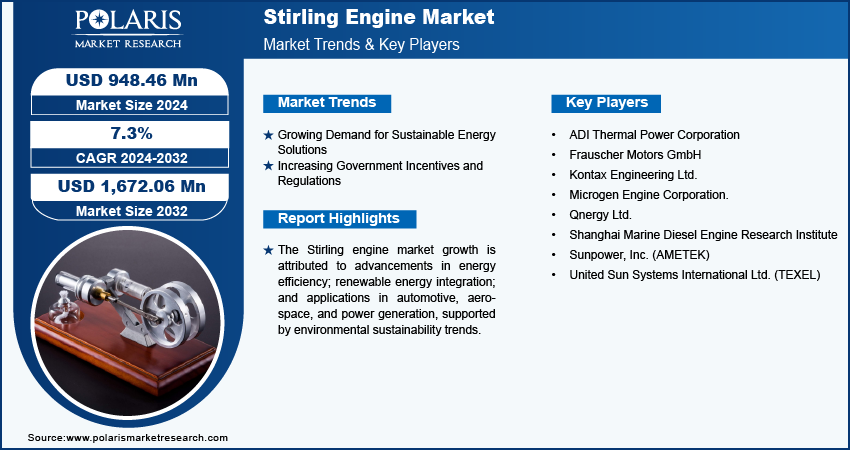

Growing Demand for Sustainable Energy Solutions

Stirling engines are gaining popularity as they can convert heat from renewable sources into electricity, meeting the increasing demand for carbon emission reduction and energy efficiency in industries and governments. These engines operate on a closed-loop system, making them highly efficient and environmentally friendly. Additionally, advancements in technology have improved their performance and cost-effectiveness, attracting investments in research and development. Stirling engines are being positioned as a viable alternative for applications ranging from renewable energy generation to automotive systems. The global shift toward greener energy continues, further fueling the growth and adoption of Stirling engines across various sectors. Therefore, the growing demand for sustainable energy solutions is significantly boosting the Stirling engines market.

Increasing Government Incentives and Regulations

Increasing government incentives and regulations are creating favorable conditions for the adoption of clean and efficient technologies. Governments worldwide are implementing policies and regulations aimed at reducing carbon emissions, enhancing energy efficiency, and promoting renewable energy sources. These measures often include subsidies, tax incentives, and grants for technologies that support environmental goals, such as Stirling engines.

Incentives such as feed-in tariffs, investment tax credits, and renewable energy mandates encourage businesses and consumers to invest in Stirling engines by offsetting some of the initial costs associated with their deployment. These financial incentives lower the barriers to entry and make Stirling engines more competitive with traditional and other renewable energy technologies. Regulatory frameworks that set stringent emission standards and efficiency requirements further drive the market by compelling industries to adopt cleaner technologies. Stirling engines, with their high efficiency and low emissions, meet these regulatory demands effectively. Governments continue to prioritize sustainability and climate action, and the regulatory environment will likely favor technologies such as Stirling engines, fostering growth and innovation in the Stirling engines market in the coming years.

Thermodynamic Performance Benchmarks by Configuration

| Configuration | Developer | Power Output (We) | Efficiency (%) | Hot-End Temp (°C) | Design Life (years) |

| TDC (Flexure-bearing) | Stirling Tech Co. | 55 | 25 | Not specified | >17 |

| ASC (Gas-bearing) | Sunpower Inc. | 80 | 40 | Not specified | >14 |

| SRSC (Gas-bearing, robust) | Sunpower Inc. | 60 | 26 | ~700 | >2.5 (TRL 5) |

| SRSC Generator (8 units, 6 GPHS) | NASA/DOE/Aerojet | 354 (BOL) | 24 | - | >17 |

| 4-Convertor Testbed (ASC-E3/SES) | NASA Glenn | 500 (input) | 16.8 | ~500 | Ongoing |

| Am-241 RPS Prototype | NASA/Univ. Leicester | Not specified | 16 | Not specified | N/A |

Source: Polaris Market Research Analysis

Government R&D Funding & Strategic Initiative Analysis

| Initiative | Agency | Period | Key Outputs | Efficiency |

| SRSC Prototypes | NASA Glenn/Sunpower | 2019-2025 | 5 units; 60 We | 26% |

| ASC Disassembly/Improvements | NASA Glenn | 2007-2015 (testing to 2025) | 17 prototypes; >14 years operation | 40% |

| Stirling RPS Generator | NASA/DOE/Aerojet | 2022 | 350+ watts electrical; 8 SRSCs | 24% |

| Small-Scale Stirling RPS | NASA Glenn | 2019-2023 | 20-50 watts electrical concepts | 15-25% |

| Controller Breadboards | NASA Glenn/DoD | 2021-2025 | Flight-ready units | N/A |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Insights

Stirling Engine Market Breakdown by Configuration Insights

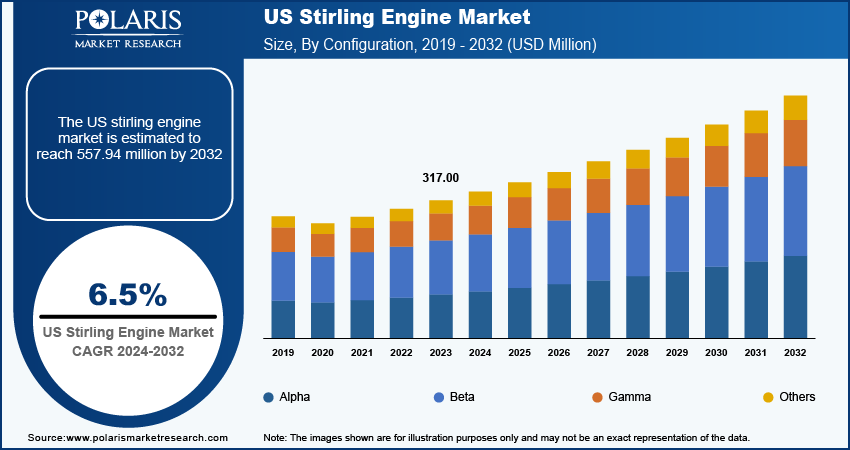

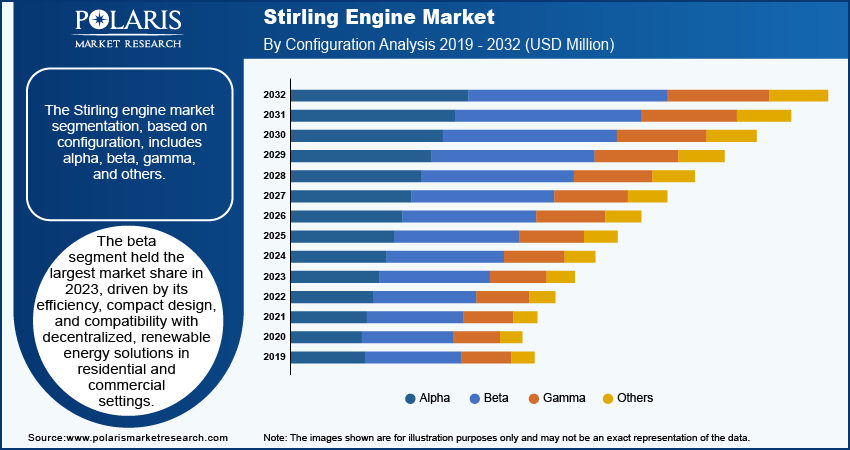

The Stirling engine market segmentation, based on configuration, includes alpha, beta, gamma, and others. In 2025, the beta segment dominated the market, accounting for 38.75% of the market revenue share (i.e. USD 342.8 million). The beta configuration of Stirling engines has captured significant market share due to its balance of efficiency, simplicity, and compact design. This design allows for easier integration into various applications, making it particularly appealing for decentralized power generation. Beta Stirling engines become increasingly relevant as the demand for sustainable and decentralized power grows, especially in residential and small commercial settings. Their ability to operate efficiently with renewable energy sources aligns with the shift toward greener energy solutions. Additionally, supportive regulatory frameworks and advancements in renewable energy technologies are facilitating the adoption of beta Stirling engines. These factors combine to position beta Stirling engines as a reliable option for consumers seeking efficient, sustainable energy solutions in an evolving market.

Stirling Engine Market Breakdown by Application Insights

The Stirling engine market segmentation, based on application, includes submarines, solar power generation, nuclear power plants, and others. The nuclear power plants segment is expected to register a CAGR of 9.4% during the forecast period. The growth is driven by the increasing adoption of Stirling engines in nuclear power applications due to their ability to operate efficiently in various energy scenarios, including low and high-temperature differentials. The engines are also being recognized for their potential to convert nuclear energy into electricity with minimal environmental impact, making them attractive in the shift toward cleaner energy solutions. Additionally, the increasing focus on reducing carbon emissions and enhancing energy efficiency in power generation is expected to boost the demand for Stirling engines in nuclear power plants. The rising global investments in sustainable energy technologies are further supporting the adoption of these engines in this sector.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Stirling Engine Market Breakdown by Regional Insights

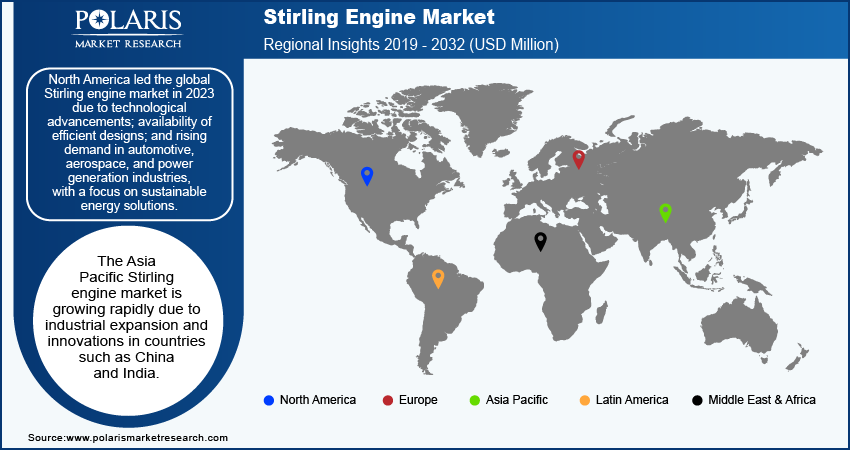

By region, the study provides market insights into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America. North America dominated the global Stirling engine market in 2025 due to the widespread adoption of engines in applications such as automotive, aerospace, and power generation. The region's growth is driven by continuous technological advancements, including the development of advanced materials and improved designs that enhance engine efficiency and performance. Countries such as the US and Canada have been at the forefront of these innovations, supporting the growing demand for Stirling engines. Additionally, the focus on sustainable energy solutions and the need for efficient power generation systems have boosted the Stirling engines market growth in North America.

Europe emerged as the second-largest market for Stirling engines globally in 2025, driven by its strong commitment to sustainable energy solutions and stringent environmental regulations. Countries such as Germany, the UK, and Sweden lead the adoption of Stirling engines in applications such as combined heat and power (CHP) systems, solar power generation, and waste heat recovery. Favorable regulatory environments, financial incentives, and advancements in Stirling engine technology position Europe as a key player in the global market.

Asia Pacific is expected to be the fastest-growing market during the forecast period. This growth is driven by significant commercial and industrial expansion in major developing economies such as India, China, and Indonesia. Additionally, there are increasing investments in the development and innovation of engines from government and private organizations. For instance, in December 2021, China State Shipbuilding announced that the company had tested the country’s first large bore engine with applications in submarine propulsion. This new prototype ran at a power of 320 KW with a power conversion efficiency of nearly 40%, making it the most powerful globally.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

Leading market players are investing heavily in research and development to expand their product lines, which will help the Stirling engine market grow even more. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments such as new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, the Stirling engine market must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the global Stirling engine market to benefit clients and increase the market sector.. A few major players in the Stirling engine market are United Sun Systems International Ltd. (TEXEL); Qnergy Ltd.; ADI Thermal Power Corporation; Shanghai Marine Diesel Engine Research Institute; Frauscher Motors GmbH; Kontax Engineering Ltd.; Sunpower, Inc. (AMETEK); and Microgen Engine Corporation.

Qnergy Ltd. develops and manufactures power system engines. The company produces a range of products based on its proprietary technology, including combined heat and power system engines, free-piston Stirling engines, solar Stirling engines, and thermoacoustic Stirling engines. Qnergy markets its products internationally. In January 2023, the company announced its grid-tied compressed air package (CAP) solution offering. Qnergy’s off-grid solutions solve the challenge of delivering CAP at off-grid wellpads via its PowerGen offering, a proprietary free piston Stirling generator with proven 100% methane destruction capability.

ADI Thermal Power Corporation, founded in 2000 in Washington State as a high-tech startup, was formed as a spin-off from Alternative Design Inc. (ADI) to focus on the development of the dual shell Stirling engine genset. The company gained attention after successfully developing an initial working prototype, which attracted funding from a prominent group of East Coast angel investors. The financial backing enabled ADI Thermal to expand operations and advance the technology further, including the development and integration of a high-temperature, high-efficiency burner into the system for enhanced performance.

List of Key Companies

- ADI Thermal Power Corporation

- Frauscher Motors GmbH

- Kontax Engineering Ltd.

- Microgen Engine Corporation.

- Qnergy Ltd.

- Shanghai Marine Diesel Engine Research Institute

- Sunpower, Inc. (AMETEK)

- United Sun Systems International Ltd. (TEXEL)

Industry Developments

February 2024: Field trials of biomass-fired Microgen Combined Heat and Power Solutions have begun, including a MEC Free Piston Stirling engine installation at a Sapporo ski resort, generating 24-28 kWh daily.

June 2024: TEXEL Technologies AB completed the acquisition of technology assets from Swedish Stirling AB for USD 41.26 million, initially agreed upon in 2023.

November 2020: Qnergy expanded its offshore installation base in the Gulf of Mexico with PowerGen 5650 systems, providing AC and DC power for various electrical loads in marine environments.

Market Segmentation

By Configuration Outlook (Revenue – USD Million, 2021–2034)

- Alpha

- Beta

- Gamma

- Others

By Application Outlook (Revenue – USD Million, 2021–2034)

- Submarines

- Solar Power Generation

- Nuclear Power Plants

- Others

By End User Outlook (Revenue – USD Million, 2021–2034)

- Marine

- Power & Energy

- Others

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Stirling Engine Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 1060.8 Million |

| Market Size Value in 2026 | USD 1161.6 Million |

| Revenue Forecast by 2034 | USD 2400.9 Million |

| CAGR | 9.50% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Stirling Engine Market FAQ's

The global Stirling engine market size was valued at USD 1060.8 million in 2025 and is projected to grow to USD 2400.9 million by 2034.

The global market is expected to register a CAGR of 9.50% during the forecast period.

North America held the largest share of the global market in 2025.

A few key players in the market are United Sun Systems International Ltd. (TEXEL); Qnergy Ltd.; ADI Thermal Power Corporation; Shanghai Marine Diesel Engine Research Institute; Frauscher Motors GmbH; Kontax Engineering Ltd.; Sunpower, Inc. (AMETEK); and Microgen Engine Corporation.

The beta segment dominated the market in 2025.

The solar power generation segment held the largest share of the global market in 2025.

Download Sample Report of Stirling Engine Market

Please fill out the form to request a customized copy of the research report.