Market Overview

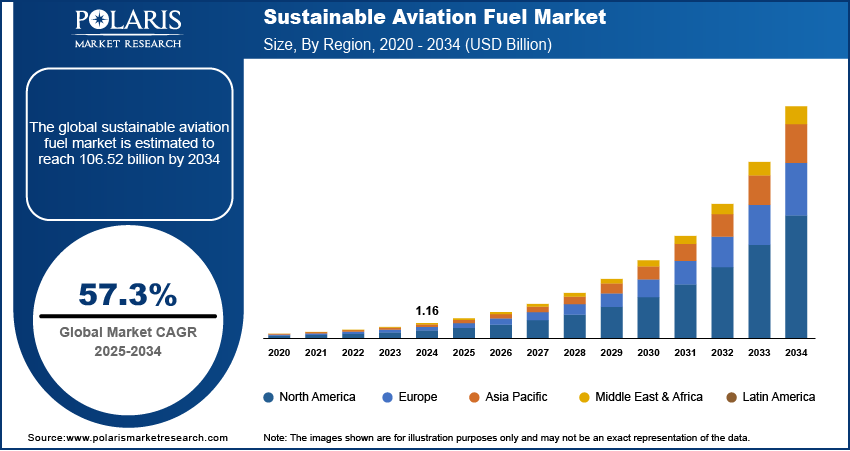

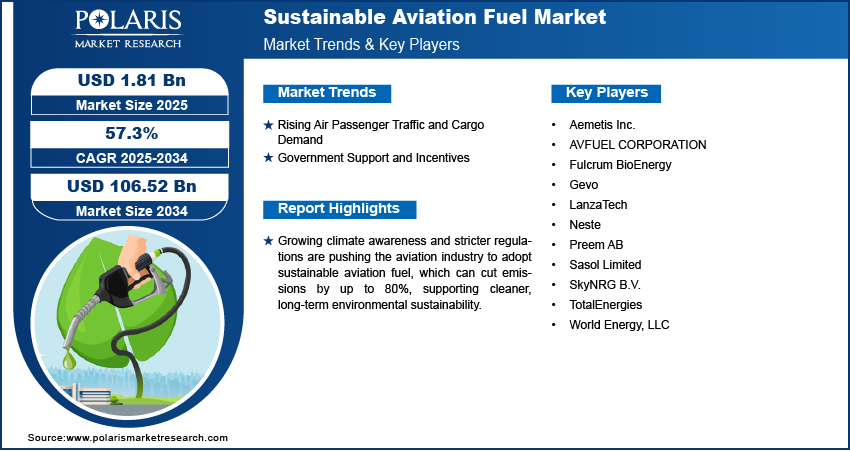

The global sustainable aviation fuel market size was valued at USD 1.81 billion in 2025, growing at a CAGR of 57.4% during 2026–2034. The growth is driven by rising focus on sustainability, government incentives, and the expansion of the aerospace industry.

The sustainable aviation fuel market is growing quickly. Airlines are making stronger commitments to aviation decarbonization. Governments are also enforcing stricter rules to reduce carbon emissions. At the same time, more regions are producing and using renewable jet fuel. These factors are driving SAF market growth and increasing the sustainable aviation fuel market size.

Key Insights

-

The biofue segment dominated the sustainable aviation fuel market in 2025. The segment held the largest share due to its advanced development, demonstrated expandability, and compatibility with in-service aircraft engines.

-

The FT-SPK segment is expected to grow significanty between 2026 and 2034. Strong certification support and the ability to use different feedstocks support the growth of this segment.

-

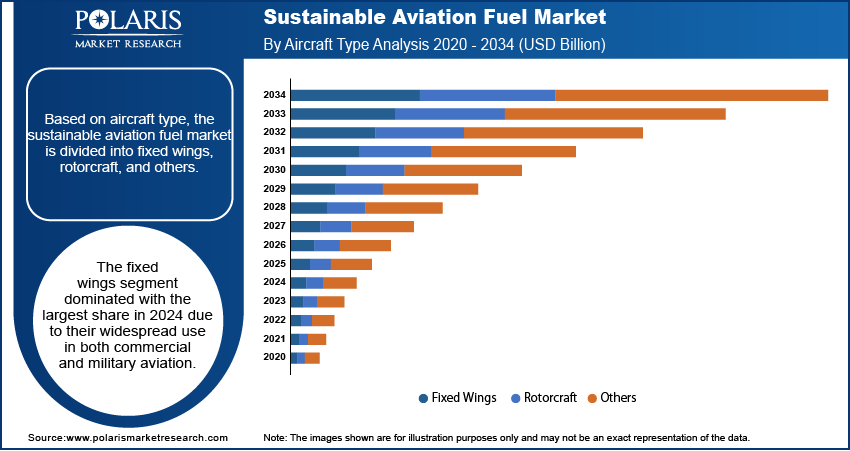

The fixed wings segment ed the market in 2025. This is mainly due to its large share in global air traffic over both commercial and defense aviation.

-

The miitary aviation segment is expected to grow rapidly. Increasing green goals(sustainability) and investments in alternative fuels by defense forces are fueling segment expansion.

-

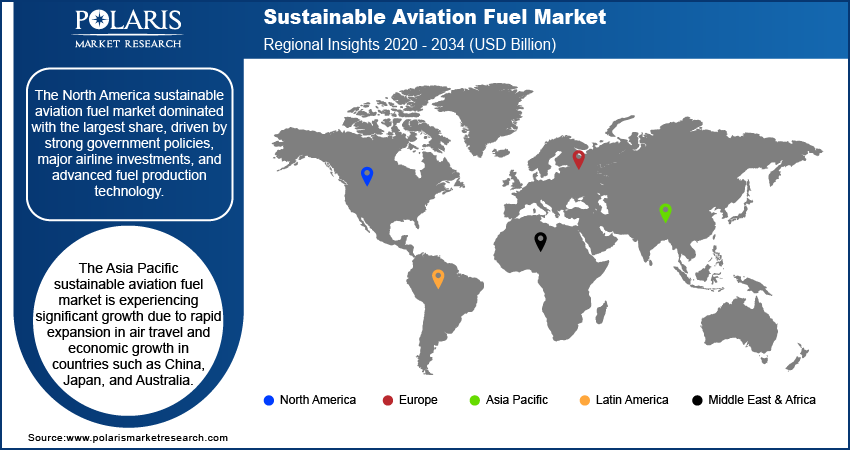

North America hed the largest regional share in 2025. National strategies, airline carbon-neutral targets, and strong renewable fuel technologies help the region’s growth.

-

Asia Pacific is projected to witness significant growth. This is due to rapid expansion in air travel in the region.

Industry Dynamics

-

The rising environmenta issues and strict carbon emission rules are increasing the adoption of sustainable aviation fuel (SAF). Growing investments in renewable fuel production technologies are also supporting the use of SAF in aviation.

-

Increasing passenger traffic is raising fue demand in the aviation sector. At the same time, airline commitments to achieve net-zero emissions by 2050 are fueling the demand for sustainable aviation fuel.

-

High production costs and imited global refining capacity are slowing the large-scale production of sustainable aviation fuel. This is restricting SAF's broader commercial use.

-

The expansion of feedstock sources is heping lower production costs. Advances in fuel processing technologies are also creating new opportunities for efficiency. These improvements can increase the availability of sustainable aviation fuel in developing aviation markets.

Market Statistics

-

2025 Market Size: USD 1.81 bilion

-

2034 Projected Market Size: USD 106.52 bilion

-

CAGR (2026-2034): 57.4%

-

North America: Largest market in 2025

To Understand More About this Research:Request a Free Sample Report

Sustainable aviation fuel (SAF) is a renewable or waste-derived fuel. This fuel can be used in existing aircraft engines to reduce greenhouse gas emissions compared to traditional jet fuel. It is produced from sustainable feedstocks. It includes used cooking oil, agricultural waste, or non-food crops. These types of feedstock offer a lower-carbon alternative for the aviation industry. Sustainable Aviation Fuel (SAF) serves as a drop-in fuel for aviation. It effectively reduces emissions. It blends easily with conventional jet fuel. Current infrastructure supports it fully. No major modifications are needed. This helps airlines reduce lifecycle emissions and move toward low-carbon aviation fuel solutions. Programs like ReFuelEU Aviation show how regulators are promoting the use of sustainable aviation fuel through blending targets and policy support.

The awareness about climate change in the world is generating immense pressure on various industries to reduce their carbon emissions. Aviation is one such industry that is responsible for a significant percentage of greenhouse gas emissions. Therefore, regulations are being imposed on airlines by various governments and international organizations. In order to achieve this, they are using SAF as it is capable of reducing carbon emissions by up to 80%. Growing environmental concerns and regulatory pressure are also pushing the aviation analytics market toward cleaner and greener solutions. With the use of SAF, airlines can promote long-term sustainability across operations. This shift is also strengthening the role of SAF in achieving aviation net zero goals. It is viewed as one of the most effective options for SAF carbon reduction in both commercial and defense sectors. The growing focus on aviation industry sustainability is driving greater sustainable aviation fuel adoption. Airlines are increasingly using SAF to reduce aviation emissions and move toward a greener future.

Technological advancements are making it easier and more cost-effective to produce SAF from a wide variety of renewable sources such as algae, used cooking oil, agricultural waste, and even carbon captured and store from the air. New methods such as Fischer-Tropsch synthesis, HEFA (Hydroprocessed Esters and Fatty Acids), and alcohol-to-jet conversion are improving fuel yield and quality. The production of SAF is becoming more efficient and scalable as technology is advancing, helping reduce costs and expand availability, thereby driving the growth of the SAF market. The HEFA-SPK process is the most advanced SAF production technology among all sustainable aviation fuel pathways. It is recommended for its high efficiency and adaptability. FT-SPK and alcohol-to-jet fuel methods are also gaining attention for their flexibility. These technologies will help increase and improve SAF production in the future.

Industry Dynamics

Rising Air Passenger Traffic and Cargo Demand

Air transportation and air express continue to grow rapidly, especially in developing regions. The Airport Council International projects that the number of air travelers may exceed 12 billion by 2030. As flight volumes increase, fuel consumption and emissions will also rise. This trend is encouraging airlines and governments to seek more sustainable solutions. Sustainable aviation fuel (SAF) provides a practical and cleaner alternative compared to fossil jet fuel. As the sector continues to grow, the demand for sustainable aviation fuel (SAF) is rising steadily. The push for sustainability in commercial aviation is driving a move toward cleaner fuel options. Airlines are increasingly focusing on reducing emissions and meeting new reporting standards. This shift is raising sustainable aviation fuel demand and supporting the broader aviation fuel transition. The use of commercial aviation SAF is now seen as a key step in achieving long-term environmental goals.

Government Support and Incentives

Many governments and organizations are promoting the use of sustainable aviation fuel (SAF). Governments offer funding, subsidies, and tax credits to boost SAF adoption. These incentives push airlines toward sustainable fuels. They also cut production costs, making SAF more affordable than traditional jet fuel. In the U.S., the Inflation Reduction Act provides tax credits for SAF producers. The EU's Fit for 55 package backs cleaner aviation fuels. These policies draw investments and upgrade fuel infrastructure. The International Air Transport Association (IATA) has launched The SAF Registry to improve transparency in fuel supply. It also helps increase SAF availability in developing regions. Programs like ReFuelEU Aviation strengthen sustainable aviation fuel policies. These initiatives make it easier for companies to produce and use SAF. Together, they are driving global SAF adoption and commercialization.

Supply Constraints and Commercialization Challenges

High production costs and limited SAF refining capacity are major SAF supply constraints. These factors are slowing down market growth. Other challenges include feedstock availability, conversion capacity, long-term offtake deals, and airport logistics. Together, these issues create obstacles for supply expansion. Such SAF commercialization challenges have widened the gap between industry goals and real output. Sustainable aviation fuel scalability remains a key concern for the next decade. Reports also indicate that SAF supply may fall short of 2030 targets without faster investment and capacity growth.

Segmental Insights

By Fuel Type Analysis

The biofuel segment kept its lead in 2025 because it is more commercially available than other options. Bio-based jet fuel is more mature and scalable than newer fuels like hydrogen and power-to-liquid. It is produced from used cooking oil, animal fats, and plant materials such as algae. Biofuel presents a viable, eco-friendly option when compared to conventional jet fuel. It substantially reduces the aviation industry's carbon footprint. It works as a drop-in fuel, meaning it fits right into existing aircraft engines without any need for modifications. This compatibility translates into significant reductions in emissions. Consequently, airlines can more readily achieve their environmental objectives. Therefore, it remains the leading segment in the sustainable aviation fuel market by fuel type. Diverse feedstocks and continuous technology improvements are helping biofuels meet large fuel demand and support growth in the biofuel SAF market.

By Technology Analysis

The FT-SPK segment is expected to witness significant growth through 2026–2034. It converts synthesis gas from biomass, municipal waste, or renewable sources into high-quality jet fuel. FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene) blends easily with conventional aviation fuel. It also brings strong performance and real emission cuts. The process works with a wide range of feedstocks. This provides flexibility for commercial scaling. Investments in gasification infrastructure and Fischer–Tropsch technologies are increasing. As a result, FT-SPK is gaining market share as airlines seek high-volume sustainable aviation fuel production. While HEFA leads current production, the FT-SPK segment is gaining strategic importance. It offers broader feedstock compatibility than other methods in the SAF technology market. Fischer-Tropsch synthetic paraffinic kerosene shows strong potential for long-term scalability among SAF conversion pathways. This positions FT-SPK as a key growth area compared to HEFA vs FT-SPK in future market development.

By Aircraft Type Analysis

The fixed wings segment held the largest sustainable aviation fuel market share in 2025. It is widely used in both commercial and military aviation. These aircraft make up the majority of the global fleet. The fleet includes passenger planes, cargo jets, and business jets. Since they consume large amounts of fuel, even small reductions in carbon emissions per flight can have a big environmental impact. SAF adoption in fixed-wing aircraft is already underway, with many airlines conducting test flights and entering long-term SAF supply agreements. The high fuel demand in fixed-wing operations is driving the segment growth. This segment is expected to remain central to fixed-wing aircraft SAF adoption. Commercial airlines are prioritizing emissions reduction in high-frequency and long-haul aviation fuel operations.

By Platform Analysis

The military aviation segment is expected to witness strong growth in upcoming time. Defense organizations worldwide are working to reduce environmental impact even when they need to maintain operational readiness. By reducing dependence on fossil fuels and SAF supports aviation energy security. Militaries in the U.S., Europe, and Asia are ramping up SAF research and test flights. They're weaving renewable fuels into long-term plans. SAF's proven durability suits tough military missions. Adoption of military aviation SAF is also supported by the need for fuel diversification. Defense agencies are strengthening domestic fuel resilience. SAF helps reduce risks from disruptions in conventional fuel supply.

Regional Analysis

North America

North America held the largest share of the sustainable aviation fuel market in 2025. Strong government policies and airline investments are supporting market growth. The U.S. plays a major role, supported by incentives under the Inflation Reduction Act. Airlines such as United Airlines and Delta Air Lines are partnering with SAF producers and signing long-term supply agreements. Canada is also supporting clean aviation, which is encouraging SAF adoption in the region. The segment is expected to remain important for fixed-wing aircraft SAF use. Airlines are working to reduce emissions on frequent and long-haul routes.

Asia Pacific

The Asia Pacific sustainable aviation fuel market is expected to grow during the forecast period. This is due to rising air travel and economic growth in China, Japan, and Australia. Governments in the region are introducing policies that support cleaner fuels. These policies target aviation emissions cuts. Airlines explore SAF partnerships and run trial flights. The region cuts reliance on imported fossil fuels. This boosts SAF uptake and market growth. The Asia Pacific sustainable aviation fuel market also offers long-term opportunities. Airlines are increasing participation in decarbonization programs and forming SAF partnerships in Asia. These factors are expected to support future SAF demand growth.

India

The market for sustainable aviation fuel in India is expanding rapidly. Aviation and environmental concerns have fueled this growth. The Indian government is promoting biofuels in key sectors like aviation. Indian airlines are also experimenting with SAF. Incentives for aviation policy are increasing. Abundant feedstocks like agricultural and municipal waste enable local production. Therefore, India’s combination of policy support, feedstock potential, and growing air travel demand is driving the market growth in the country. India is emerging as a promising market in the India sustainable aviation fuel market. The country has a large domestic aviation sector and a growing bioenergy ecosystem. It also has strong potential to produce agricultural waste aviation fuel through local SAF production.

Europe

The Europe sustainable aviation fuel market is expected to see steady growth during the forecast period. Strong environmental rules and bold climate goals drive this progress. The EU pushes ReFuelEU Aviation and the "Fit for 55" package. These policies push airlines to gradually increase SAF use in commercial flights. Major carriers like Lufthansa, Air France, and British Airways now blend SAF into daily operations. The Europe sustainable aviation fuel market invests heavily in new production plants and fuel innovations. Governments, airports, and suppliers strengthen the ecosystem. ReFuelEU Aviation drives the SAF blending mandate Europe forward. With clear policies and strong teamwork, sustainable jet fuel Europe leads global aviation emission reductions.

Key Players & Competitive Analysis Report

The sustainable aviation fuel (SAF) market is highly competitive. Key players push innovation and growth. TotalEnergies, Neste, and World Energy lead commercial SAF production. They handle global supply networks smoothly. Gevo, Fulcrum BioEnergy, and LanzaTech break new ground with feedstocks and tech like alcohol-to-jet and waste-to-fuel paths. Aemetis Inc. and Preem AB focus on renewable fuel integration into existing refineries. AVFUEL Corporation and SkyNRG B.V. act as crucial SAF distributors, linking producers with aviation clients. Sasol Limited adds synthetic fuel expertise. Strategic partnerships, feedstock sourcing, and regulatory alignment define the competitive edge in this rapidly evolving market. Competitive differentiation hinges on pathway maturity and feedstock security. Project bankability and geographic reach matter too. Airline offtake agreements secure long-term demand for SAF producers in this SAF competitive landscape.

Key Players

- Aemetis Inc.

- AVFUEL CORPORATION

- Fucrum BioEnergy

- Gevo

- LanzaTech

- Neste

- Preem AB

- Saso Limited

- SkyNRG B.V.

- TotaEnergies

- Word Energy, LLC

Industry Developments

Recent industry developments indicate that the market is moving from pilot activity toward larger-scale commercialization, with funding support, long-term supply agreements, and new production plant announcements playing a critical role in shaping future capacity. These trends show a competitive shift in scaling up supply. Companies develop local supply and make critical partnerships in the aviation fuel supply chain.

In October 2025, Gevo announced that it had received an extension of its conditional USD 1.46 billion loan guarantee from the U.S. Department of Energy for the SAF project. The deadline was extended to April 2026.

In June 2025, Neste agreed to supply 7,500 metric tons of SAF to Amazon Air for California operations. This expands their SAF partnership.

In April 2025, Bangchak opened Thailand's first 100% Neat SAF unit at Phra Khanong Refinery. This is an important milestone in the development of renewable aviation fuel technology.

In September 2024, TotalEnergies inked a 10-year deal with Air France-KKL.It intends to supply up to 1.5 million tons of SAF by 2035. It is one of the airline's largest agreements.

In August 2024, SkyNRG partnered with Skellefteå Kraft on Project SkyKraft. They aim to build an eSAF plant near Skellefteå Harbor using renewable energy and biogenic CO₂.

In February 2024, Airbus and TotalEnergies formed a strategic partnership. They advance SAF to cut aviation CO₂ emissions and develop 100% sustainable fuel solutions.

Sustainable Aviation Fuel Market Segmentation

By Fuel Type Outlook (Volume, Million Liters, Revenue, USD Billion, 2021–2034)

- Biofuel

- Hydrogen Fuel

- Power to Liquid Fuel

- Gas-to-Liquid

By Technology Outlook (Volume, Million Liters, Revenue, USD Billion, 2021–2034)

- HEFA-SPK

- FT-SPK

- HFS-SIP

- ATJ-SPK

By Aircraft Type Outlook (Volume, Million Liters, Revenue, USD Billion, 2021–2034)

- Fixed Wings

- Rotorcraft

- Others

By Platform Outlook (Volume, Million Liters, Revenue, USD Billion, 2020–2034)

- Commercial

- Regional Transport Aircraft

- Military Aviation

- Business & General Aviation

- Unmanned Aerial Vehicles

By Regional Outlook (Volume, Million Liters, Revenue, USD Billion, 2020–2034)

-

North America

-

US

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Russia

-

Rest of Europe

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Malaysia

-

South Korea

-

Indonesia

-

Australia

-

Vietnam

-

Rest of Asia Pacific

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Israel

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

Sustainable Aviation Fuel Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2025 |

USD 1.81 billion |

|

Market Size Value in 2026 |

USD 2.83 billion |

|

Revenue Forecast by 2034 |

USD 106.52 billion |

|

CAGR |

57.4% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021-2024 |

|

Forecast Period |

2026-2034 |

|

Quantitative Units |

Volume in Million Liters, Revenue in USD Billion, and CAGR from 2025 to 2034 |

|

Report Coverage |

Volume Forecast, Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

|

Segment Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The sustainable aviation fuel market was valued at USD 1.81 billion in 2025 and is expected to grow at a CAGR of 57.4% during the forecast period.

Sustainable aviation fuel is a renewable fuel that reduces lifecycle carbon emissions compared to conventional jet fuel.

The FT-SPK segment is expected to witness significant growth through 2026–2034. This is because it brings strong performance and real emission cuts.

North America leads due to strong government incentives and airline investments.

SAF is blended with jet fuel and used in commercial and military aircraft.

Government incentives increase SAF production and airline adoption.

High costs, limited feedstocks, and infrastructure gaps are major challenges.

Page last updated on:

Jun-2025

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements